Business

Aurion Pro is an IP product primarily present in banking & fintech, Transit solutions & data center businesses. Let us discuss each segment in detail

Banking & Fintech

They have a suite of offerings which help banks & fintechs in their digital transformation journey. products in Retail banking (Branch transformation: automate services disbursement by solutions like self banking kiosks, customer queue management system),

corporate banking (iCashPro: loan origination, collateral management, limit management, liquidity, trade finance & smart lender: end to end underwriting management),

and treasury management (services and project management for Capital markets, Treasury, Risk

management, and Regulatory needs)

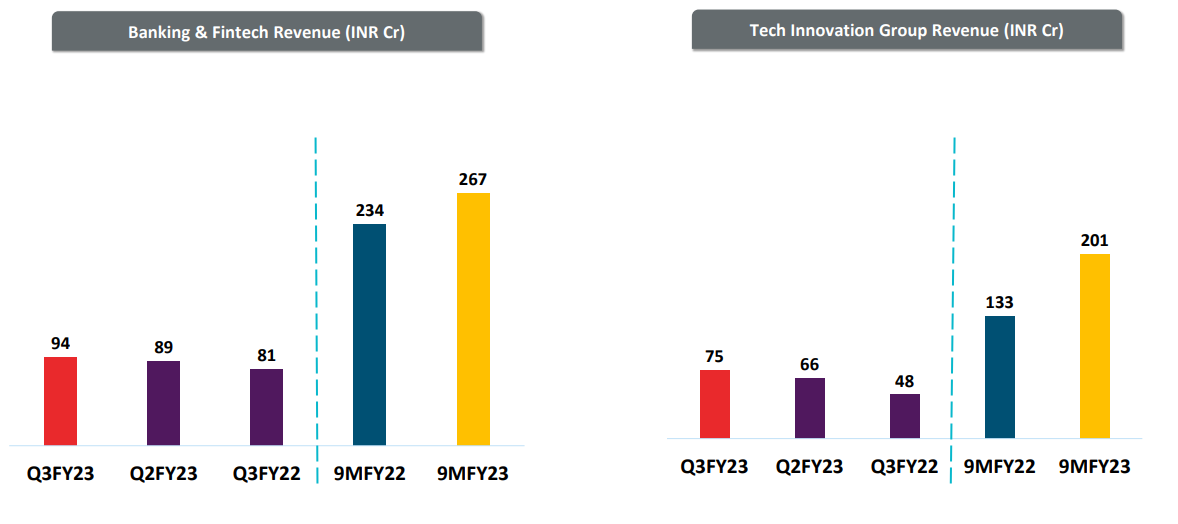

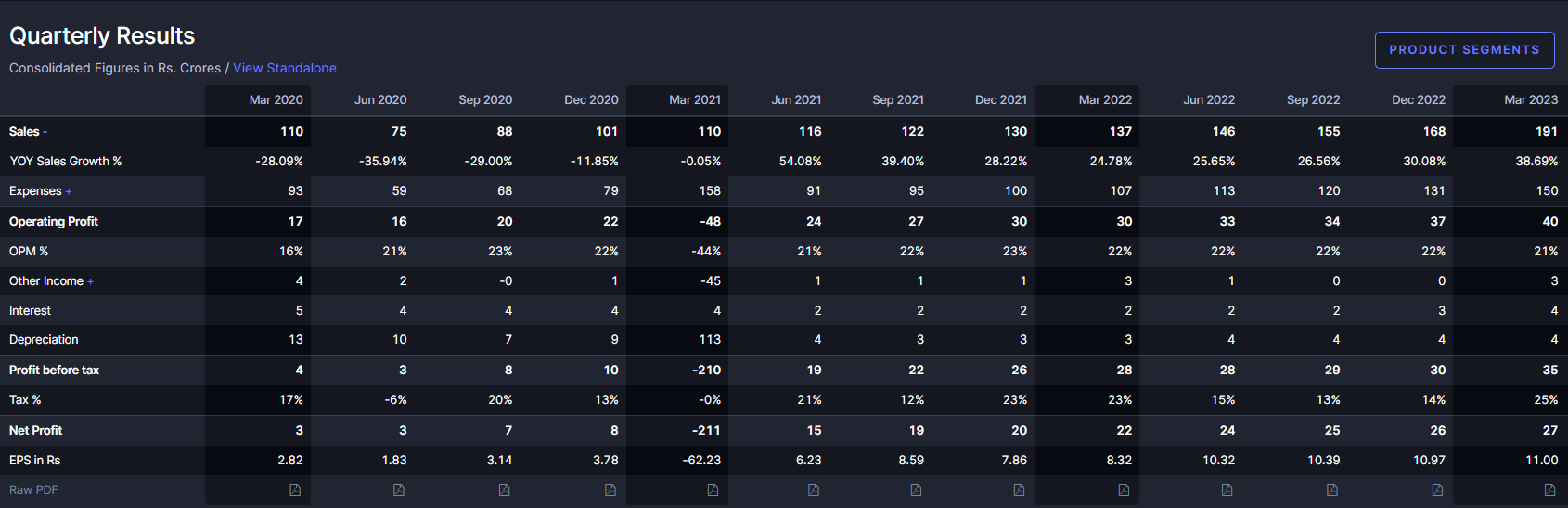

this is the mature part of the biz which has been growing around 15-20% Guidance is for accelerated growth in FY24 in Q4FY23 concall. This biz also has better margins by virtue of being mature (lot of R&D spends for developing & maturing the product have already happened). Margins in Banking are 500 bps above corporate average (so maybe 25-27%). Contribution to revenue is around 52% for this segment.

TIG: Technology innovation group

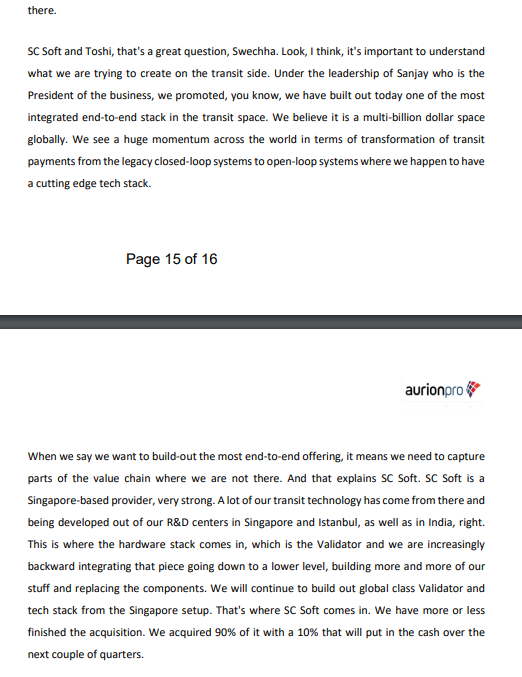

This is the younger, faster growing part of AurionPro. It has some disparate businesses. Transit open-loop payment systems are a significant part of this revenue segment. Good article to understand movement from closed loop to open loop payment systems in Transit:

This requires both the software for backend management of the transit journey of user, for managing the backend of the transit system and the hardware required for the validation of the user journey. Disbursing as well as checking tickets. The fascinating part about this biz is that they are vertically integrated and provide a complete solution to the transit customer with both hardware & software (

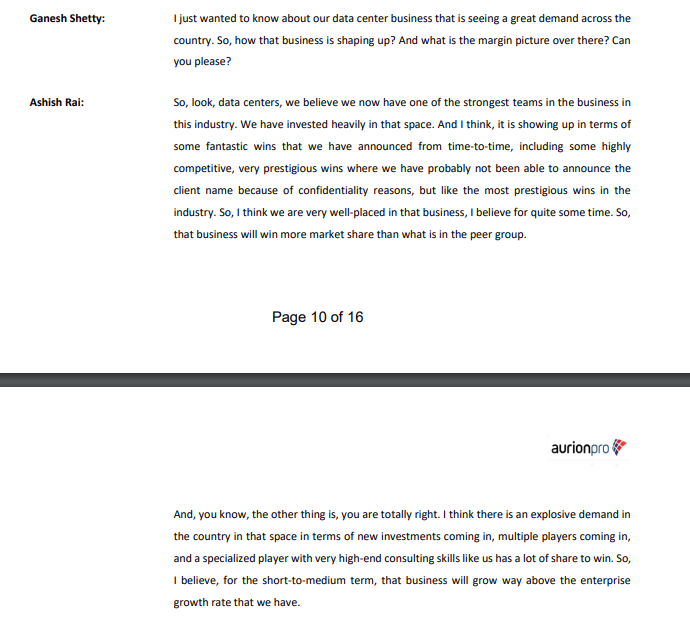

On the data center side, they seem to be playing role of consultant & designer of the software side of data center. This is a small but growing part for them.

Overall, TIG is 48% of revenue but growing at 40-50% with 15-17% margins. Due to TIG, corporate growth is lifted to 25-30%.

Revenue breakup:

Growth

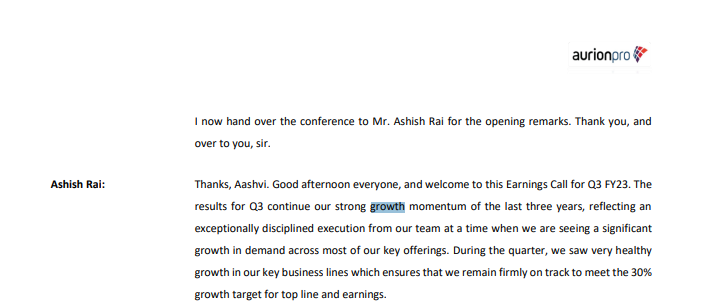

The last 8 quarters have seen good execution & growth.

I am generally very skeptical of turnarounds, but when a co has been executing for 8 quarters, i am more inclined to believe their guidance. They have been walking the talk on growth.

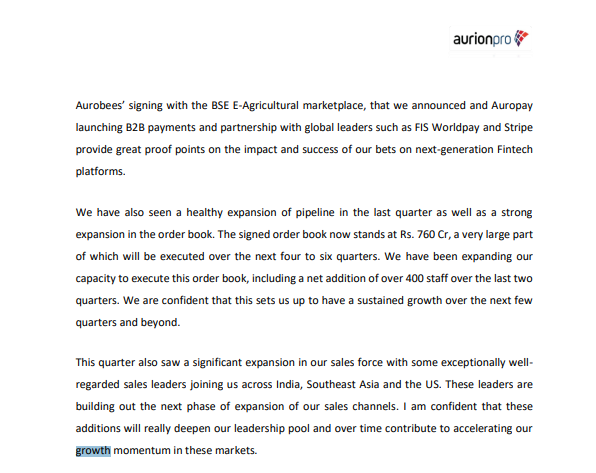

The medium term guidance is for 25-30% growth. The guidance for FY24 is for 30-35% growth. The growth will be primarily led by TIG segment growing fast.

IT companies are about converting human knowledge work into sales. One of the leading indicators of growth is staff addition which has been around 400 per quarter

on a base of 2000 employees

Longish answer on growth guidance:

Reason for growth visibility is the movement from closed loop to open loop payment systems

Profitability

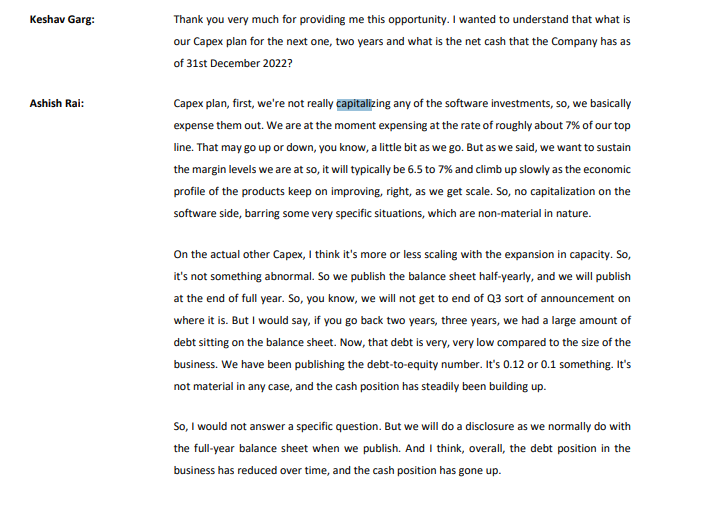

Co currently spends 7-8% of revenue as R&D spends. With operating leverage, the strategic direction is to keep the margins stable at 22% or so at corporate level & investment in R&D will accelerate to 10% of sales.

The ROE is around 22% right now with minimal debt.

Quality

I do not want to go as far as to talk about the ‘moats’ in the business but definitely important to understand the quality of the business. We are gauge of the quality of their solution through two ways:

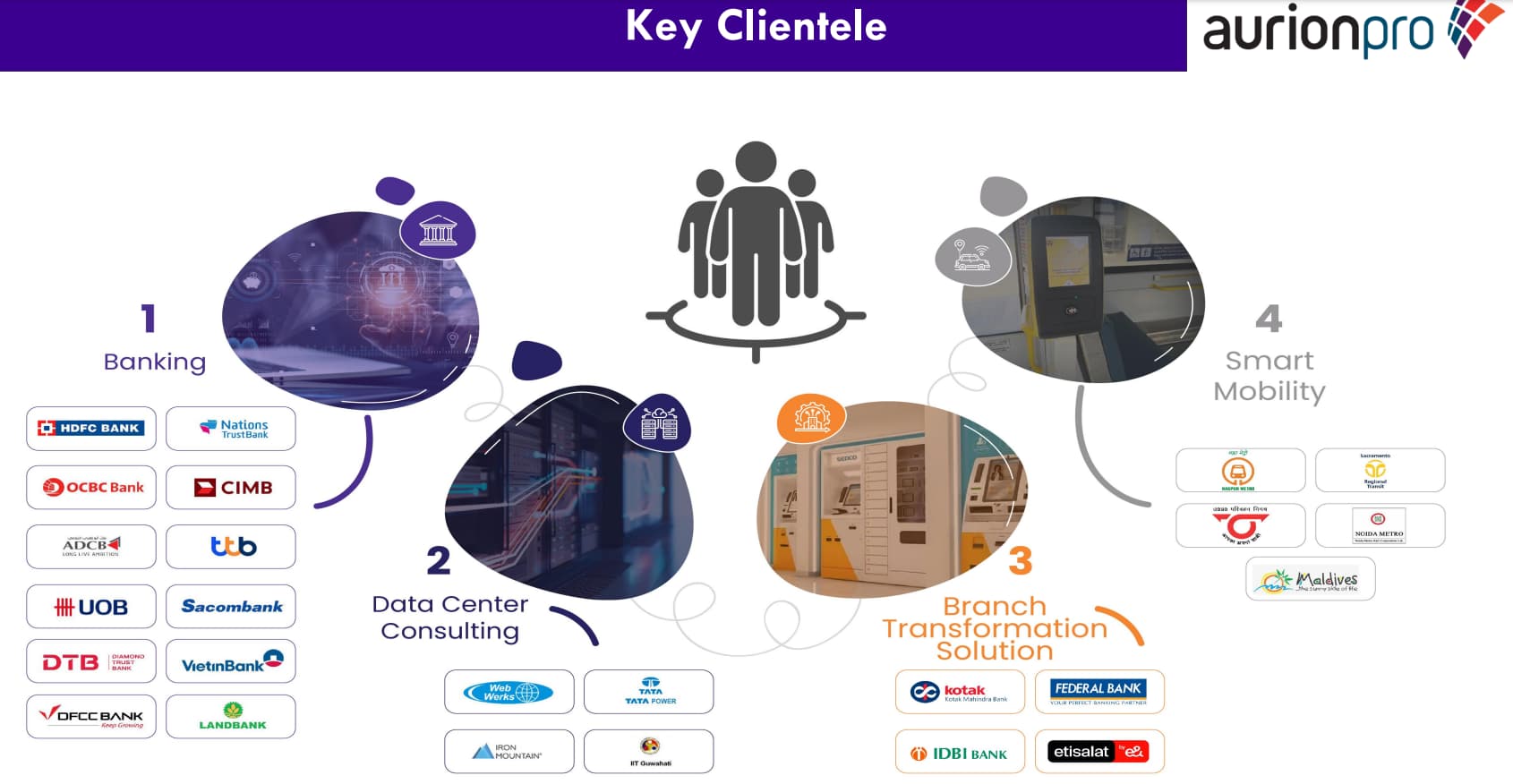

- Quality of clients. If good clients are using their products, then they must be reasonable products.

We can see that HDFC, Kotak, federal all use their products.

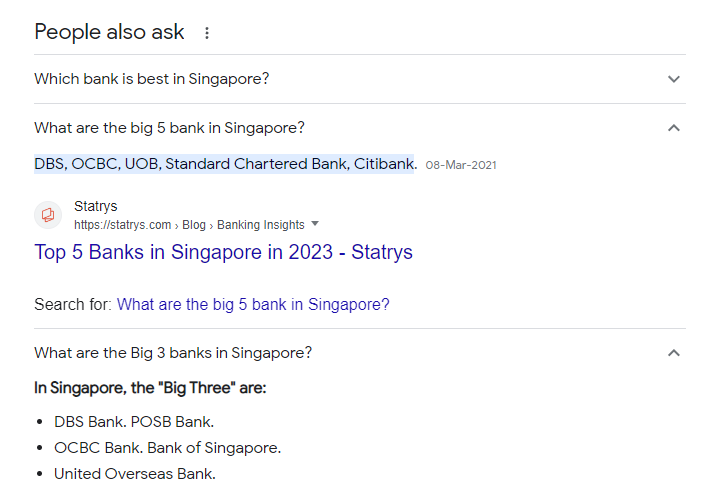

OCBC bank is 2nd largest in singapore

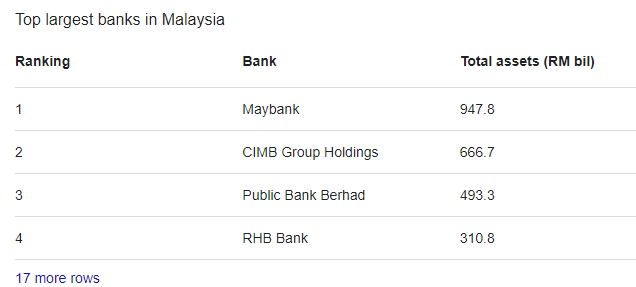

CIMB is 2nd largest in malaysia

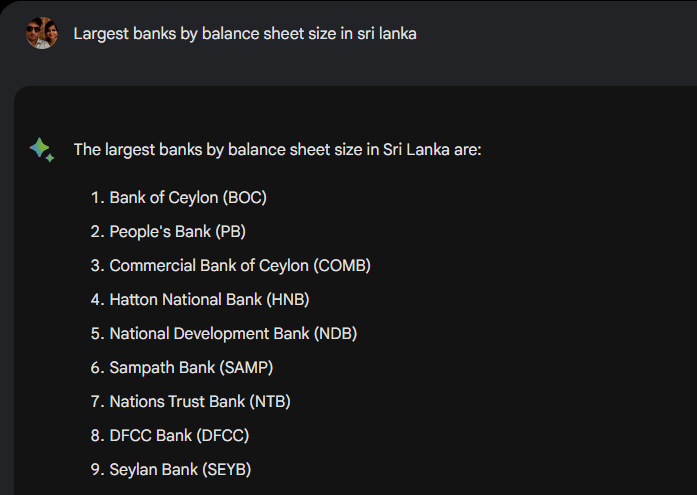

Nations trust bank is 7th largest in sri lanka

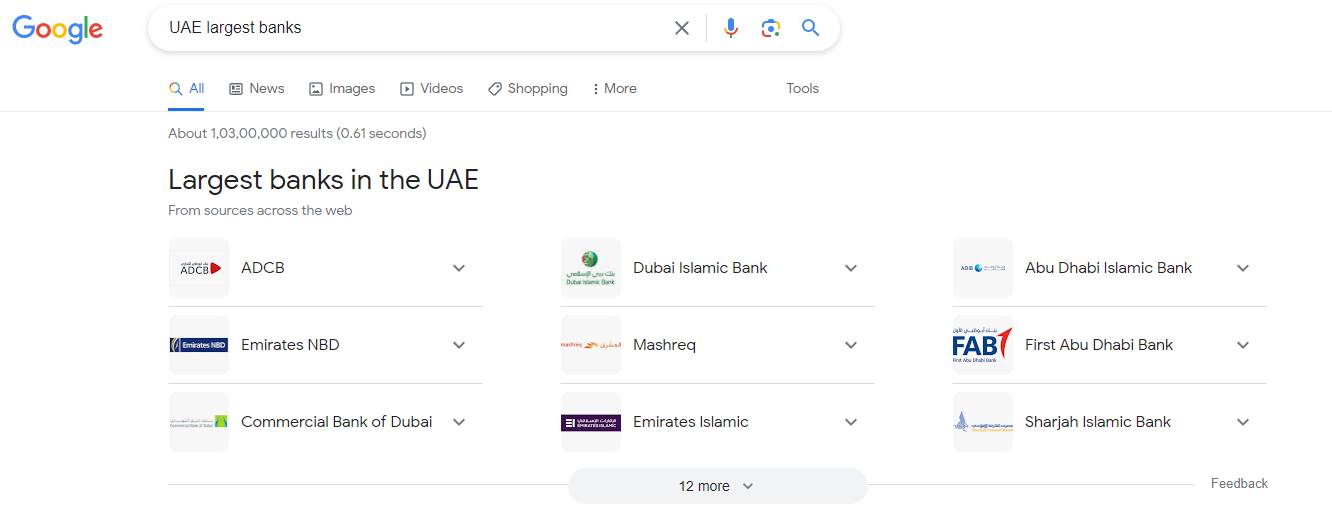

ADCB is largest bank in UAE

The important thing to note is that aurion has large established banks as customers which lends credence to quality of product

In the TIG segment, Nagpur metro, Noida metro, Kanpur metro, Haryana transport, UP transport are all clients of AurionPro

As ridership increases, they get paid on a per trip basis which IMO should expand TIG segment margins.

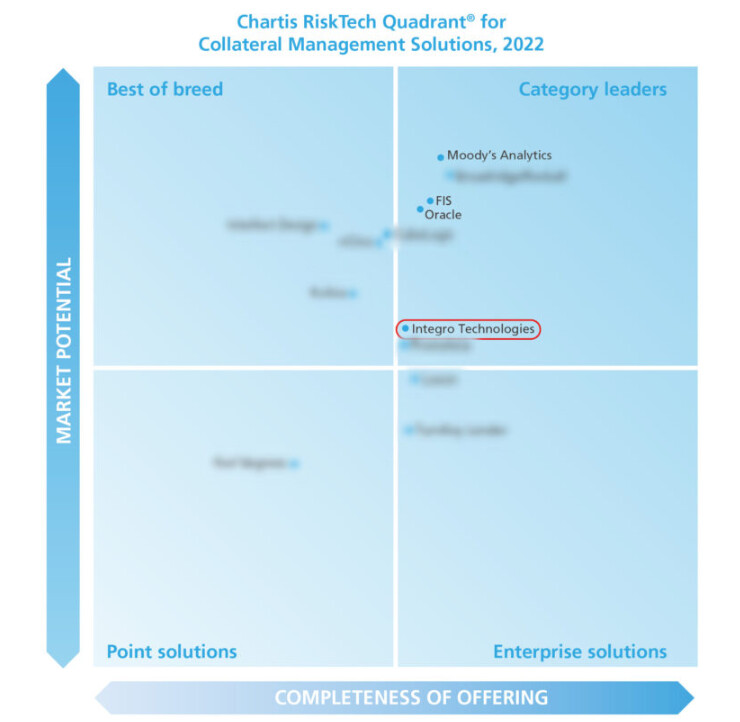

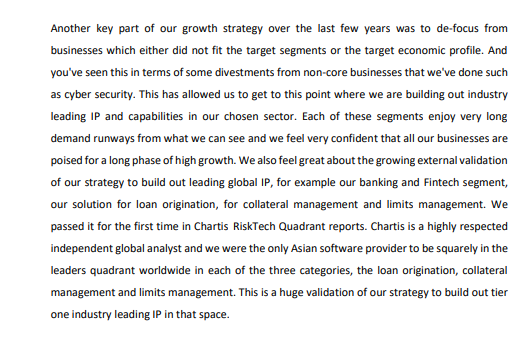

- Analyst ratings

Chartis is a risk-tech research, analysis & consultant firm.

On chartis rankings, aurionpro is in leadership quadrant for loan origination

Same for collateral management

Same for limits management

Source: https://www.aurionpro.com/news/chartis-recognizes-integro-technologies-as-a-leader-in-credit-lending-operations/

it is the only asian It company in this quadrant. FIS is an established leader. Moody’s is an established leader.

-

Partnerships with leading player Finastra: Finastra is offering Integro/Aurionpro’s SmartLender Trade Limits solution alongside its own Trade Innovation solution. https://www.aurionpro.com/news/finastra-and-integro-technologies-to-offer-comprehensive-digitalization-and-exposure-risk-offering-for-trade-finance/ The fact that finastra does this, is proof of quality for aurion pro’s product

-

Winning globally competitive transit RFPs: Aurionpro won the california-integrated travel project Transit RFP for openloop payment systems. https://www.aurionpro.com/news/sc-soft-signs-multiple-deals-under-california-integrated-travel-project-cal-itp/ This is a multi-year, multi-million-dollar opportunity as it has opened for us the market consisting more than 300 transit agencies in the city and counties in the state of California. Aurion was one of the only 3 vendors to win the bid for validators.

https://www.calitp.org/

We can verify the same on Cal-ITP website: State of California Contracts | California Mobility Marketplace

SC soft is one of the 3 payment devices vendor.

- Shared infra for payment processing: A very interesting insight came out in Q4FY23. Aurion uses the same transaction processing infra in transit payment product & the banking transaction processing product. This is from Q4FY23 concall for which we dont yet have transcript. This though imo is a core hallmark of a true product company. You should be able to leverage core capabilities across products and that is where the operating leverage of a IT product co comes in

Management

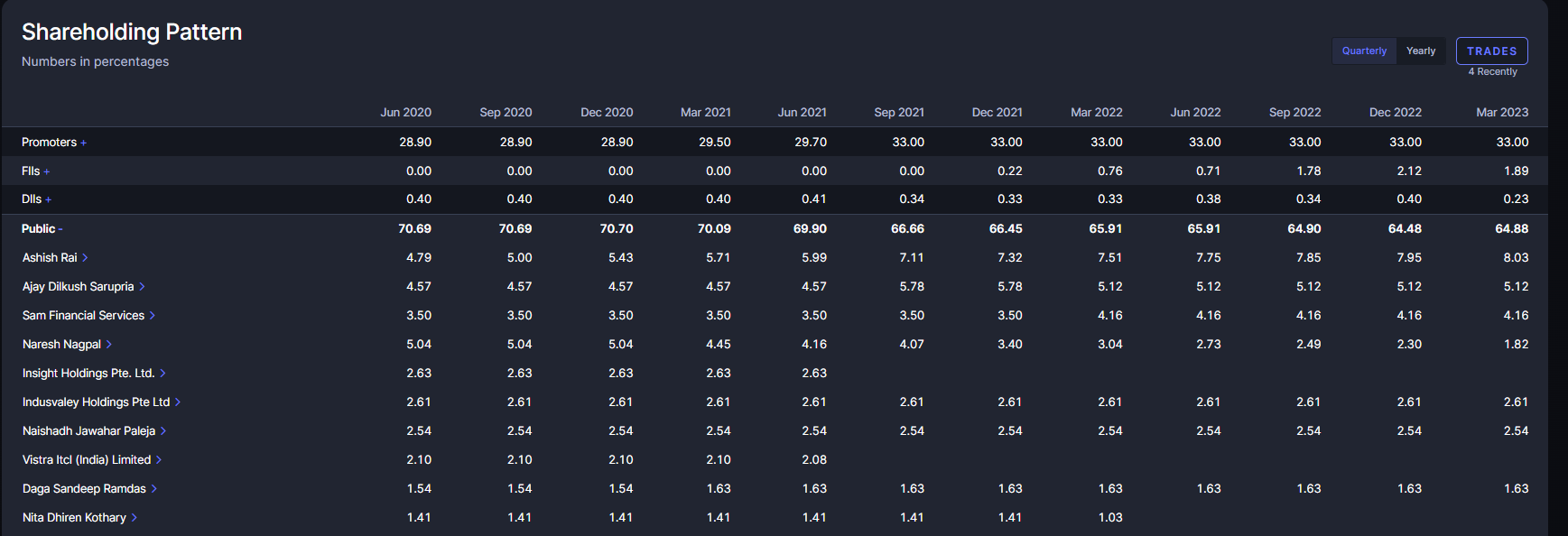

The turnaround in the fortunes of Aurionpro has been around the time that Mr ashish Rai had bought a large stake in the company:

He has been increasing his stake as well over the years and it now stands at 8% or so. He is the guy who gives interviews & answers questions on concalls.

Although as per annual report he is just another leader

but in reality i think his addition both financially & in terms of management bandwidth has been critical in helping aurionpro make the right product pivots (more on this later)

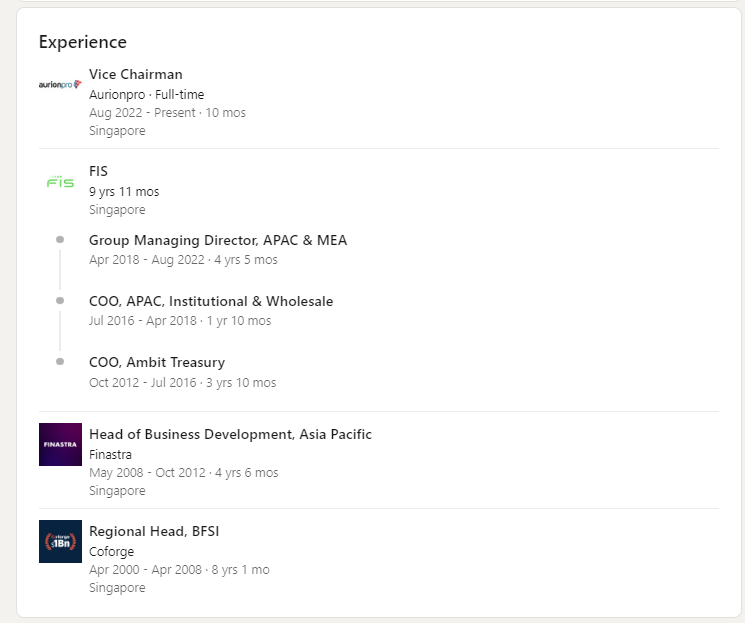

Graduate from IIM Lucknow

Importantly he has good work pedigree. Worked for 8 years at coforge, 4.5 years at finastra. 12 years at FIS as asia head

https://www.linkedin.com/in/ashishrai/?originalSubdomain=sg

He is just continuing to do more of what he did at FIS & finastra at AurionPro

This is the management change thesis. This is also a keyman risk

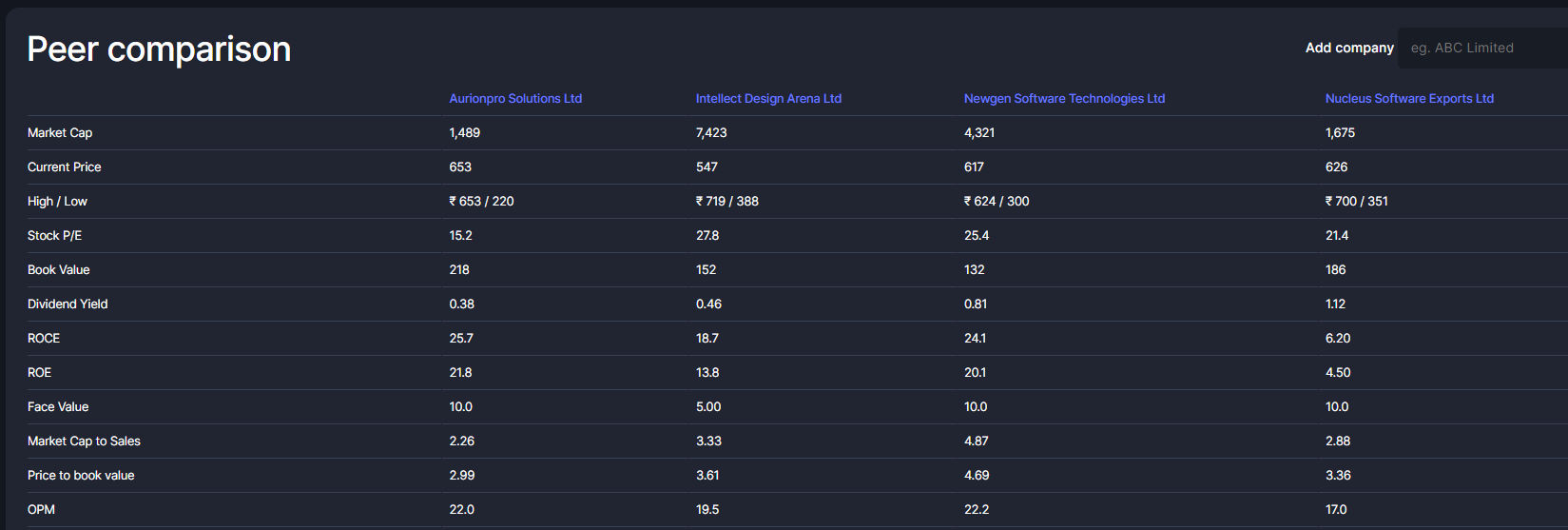

Valuation

Currently at 15x TTM earnings, 11x FY24 earnings.

Peers are at 21-27x TTM earnings and slower growth rates (last 1-3 years since this is a turnaround)

Risks

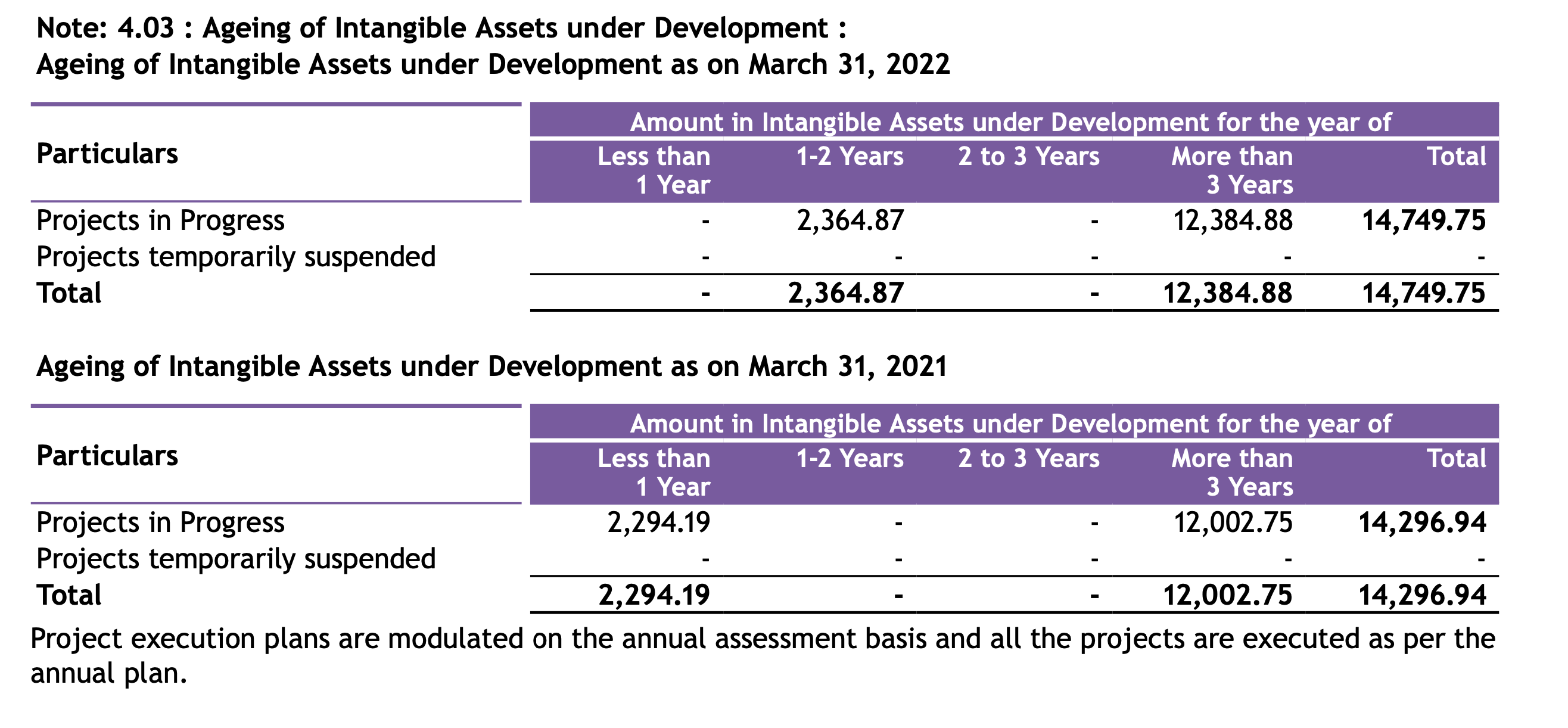

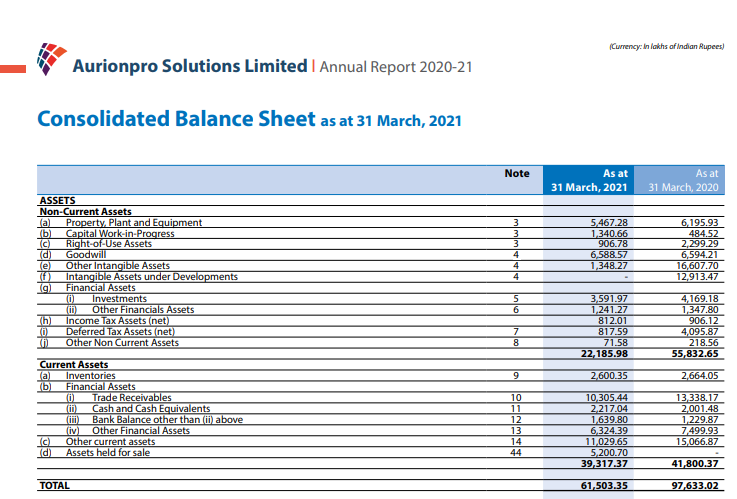

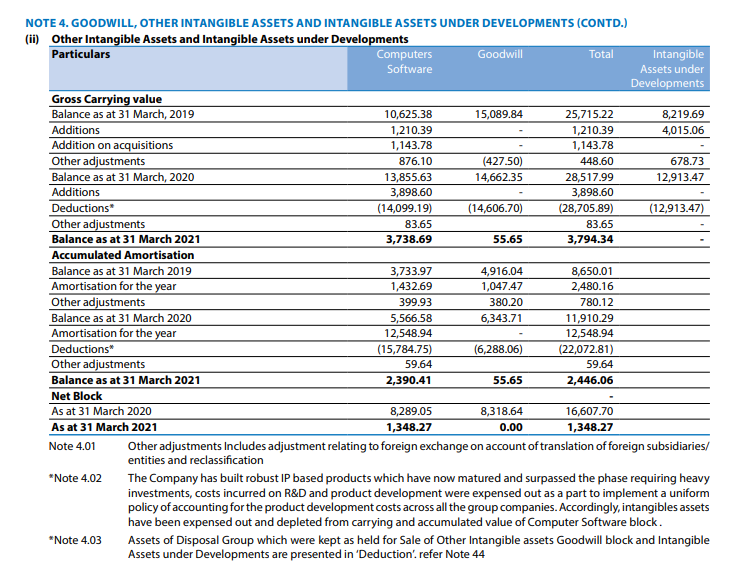

- Intangibles write down

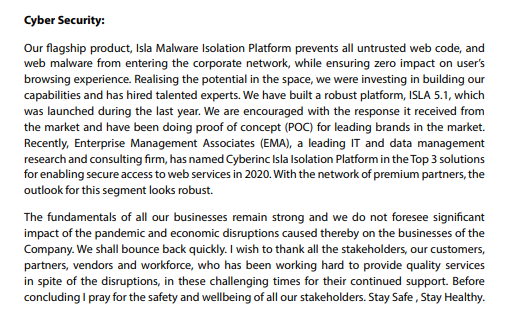

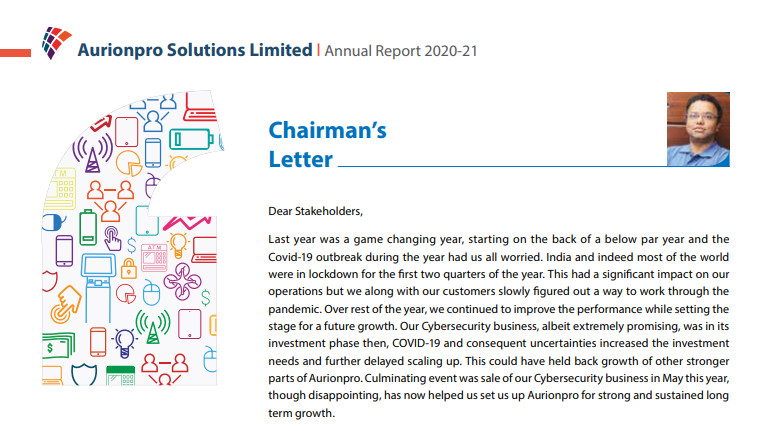

Until FY21, co used to have cybersecurity business. Screenshot from FY20 annual report.

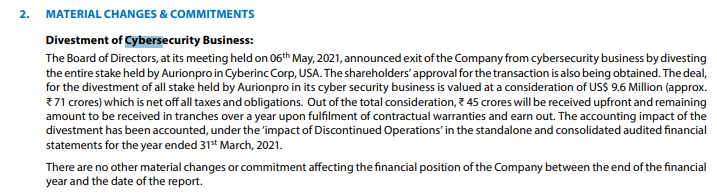

The Cybersecurity business was promising, but needed large investments and the investment needs increased due to COVID-19 and delayed scaling up. This could have held back growth of other stronger parts of Aurionpro. Co thus sold Cybersecurity business in May-21.

It sold the cybersecurity business to Austin-based software company Forcepoint LLC, USA for $9.6 million (about Rs 71 crore)

From FY21 annual report:

This is visible in balance sheet as write down of other intangible assets

THis should definitely sour the taste of any investors mouth since write down of intangibles & other goodwill can be a way to take money out of business. That is the key risk investors should be aware of. Acquisitions & capitalizing R&D creates these intangibles. Co has stopped capitalizing R&D expenses.

These changes in accounting also seem to coincide roughly with Mr ashish Rai joining which is why i would treat this as a management change.

-

Key man risk: Mr ashish has been responsible for the turnaround as far as i can tell. There is a key man risk wrt his continuation at aurionpro.

-

Most of the competition from india at least have focused on different geographies like intellect on Europe, Aurion on Asia. What happens when they collide. Mr ashish talks about Aurion IP being tier 1 (meaning best among the best). Their client wins do seem to validate that to some extent. But competition remains one of biggest risks specially as geographies overlap for Nucleus, Intellect, Aurion, Newgen

Disclaimer: Invested, biased. Do your own due diligence before investing