Established in 1997, Aurionpro Solutions Limited has been providing Software solutions based on homegrown IP. Aurionpro had a software services group, but 5 years ago they sold the business and started focusing only on the IP led business. Currently AurionPro has two core businesses

-

Banking and Fintech - Banking products for Asian Banks.

-

Technology Innovation Group - Vertically integrated in AFC (Automated Fare Collection, used for Metro train and bus ticketing), Platform solutions to Data Center & Cloud customers

AurionPro management goes deep in terms of product offering once they enter a segment. AurionPro made acquisitions in the AFC business segment, and developed fully integrated HW and SW platforms. Using these products AurionPro competes globally and has won orders from global transit customers including California. AurionPro has developed an EMV certified payment terminal. AurionPro’s Data Center Platform solutions business is new, and I am confident that they can scale this business in the coming years.

Average growth rate of Banking business is 15-20% whereas Technology Innovation business is 15%. They are growing at 30-35% in the past two years, but these growth rates may not be sustainable in the long run.

How AurionPro is different from the other SW businesses: The management has a spawner DNA. They venture into new businesses and they kill these businesses if they don’t work. For example, the Cyber Security group was killed in 2021. They have also killed SmartCity solutions business as they receive revenues from state govt. agencies and they are not predictable. Aurion acquired SC Soft which is a back bone of their AFC business.

Recurring revenue. Once Aurionpro delivers a solution, a portion of their revenues will become recurring in nature. Though management didn’t split recurring revenue contributions, it’s going be 15-20% of the order value. This is going to be a considerable part going forward as they start supporting more banks, transit systems.

Management Quality: The new CEO Ashish Rai is an amazing operator, and capital allocator. As the stock price went up, he raised the capital from the market for R&D and acquisitions. The company expends all the R&D instead of capitalizing as they launch the new platforms and solutions, hence the margins are not fully reflected for the matured businesses like Banking.

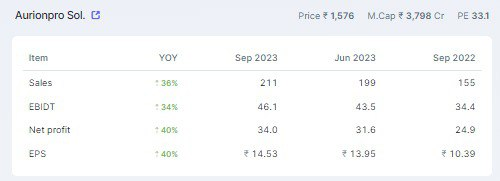

Valuation: AurionPro currently trades at 5250 Cr market cap trading at 30x EV/EBITA, and the management guides for 25-30% for the next few years. In 2023, AurionPro grew at 35%. To be on conservative side, I expect a growth rate of 20-25% is reasonable for the next 5 years.

AurionPro Corporate presentation for your reference: https://www.bseindia.com/xml-data/corpfiling/AttachHis/12e76634-22e1-4722-bcf1-8006ba4e8d22.pdf

**Disclosure: Owning the company for 5+Years with 20x return till date, my view maybe biased **