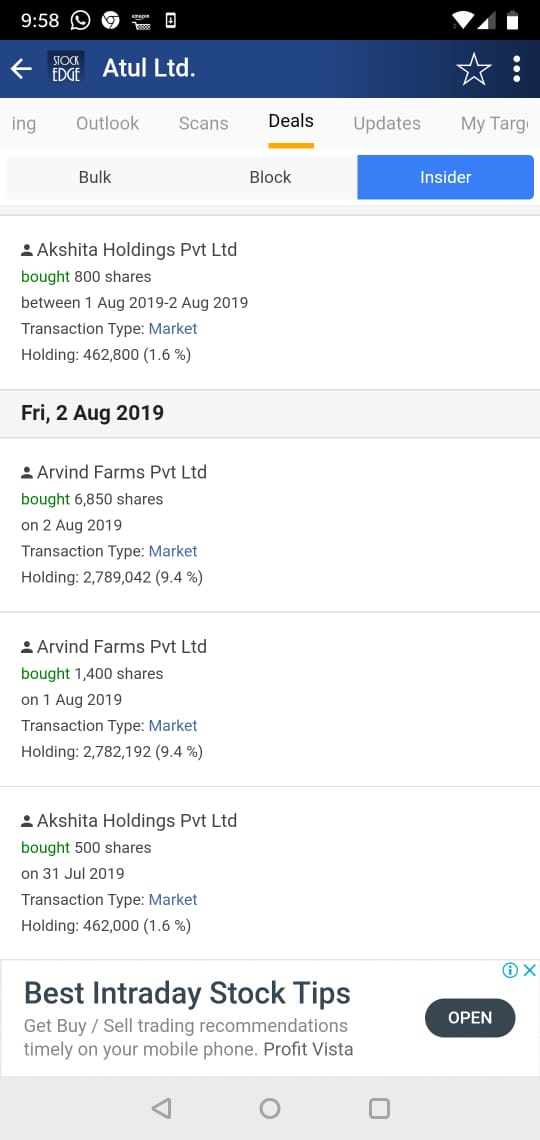

that gives a hint that they are confident of delivering good numbers and confident of share price going higher. Couple of days back, the price was 889, today it closed at 965.5.

Atul Ltd is a chemical conglomerate and one of the flagship company of Lalbhai Group(also owns Arvind Mills).

Any thoughts on the prospects of this company?

Disc:invested and increased the holding to abt 5% of portfolio 2 days back.

Though it has fell from 1027 to 978 in the last couple of days, I noted that shares to be bought were abt 2.3 times the shares to be sold in the last hour of trade today. That indicates that it may rise if market fall stops.

Someone who can understand the basic fundamentals can throw some light on this company.

I am from rubber raw material business.And this company is heavily launching products and feedback for its product in our line especially targeting Pidilite adhesive line.

They are daily tracking and taking response and also coming with attractive offers both dealer and retailer side.

Though because of overall slowdown in our line and diwali clearing of accounts by all they not getting much better response but still i am really attract by their sheer handwork in this field.

The stock has been in my watchlist for some time for being a good business where I have other interests (PI Industries is a holding for me) and has good ROCE and growth numbers

IT would be interesting to see what is driving the margin expansion.

No I am not. Generally have stayed out of the Chemicals industry as I still don’t understand it well. Tough to get into. My picks so far has been in KPO, FMCG, Agrochem, Auto, Logistics etc

Presentation started with a slide showing in last decade how was the growth and in 1st 5 years as compared to latest 5 years. For obvious reasons growth in last 5 years has to be lower because of high base but management said, they have huge headroom to grow and they are disappointed by not reflecting the same results. Management also said, profitability in FY18 could have been better but they were affected by rise in crude prices but feels they have huge potential to improve the performance.

Company has done capex of ~800crs in last 3years of which numbers are yet to reflect fully. Management said, there is lot of fixed cost sitting in the P&L which is not contributing to the topline yet and hence with increase in revenue, margins should also improve. Though didn’t give any guidance but expects with all the expansion undertaken in last 2-3 years, they should do 125-150crs of PAT every quarter. This data point was in response to a question asked regarding normalised profit post expansion

Numbers

Management expects topline from 3000crs to 4000crs will come very soon. Indicated that in 1Q19, company has delivered a topline of 900crs. So should reach 4000crs in 1-2 years’ time.

Did not specifically talked about margins but believed these should remain healthy as lot of fixed cost is still sitting idle in P&L and with increase in topline should help to improve margins

Highest ever RoCE they have done is 31% and based on 1Q numbers it comes to around 27%. Management believes they should be able to touch 31% fairly soon.

Volume growth has been 8%/5%/3%/16%/12% in last five years. 1Q volume growth is ~17%.

There is some seasonality because of crop protection business. Other than crop protection, revenues are linear.

Top 20-25 products derive majority of the sales. In all they have 900 products.

On Phosgene – Company makes Carbon monoxide, Chlorine and Phosgene derivative. These are complex products to make (actually process is complex than products) and management expands to grow the portfolio further. Phosgene is used in Crop Protection, Pharma and Speciality polymers

China Situation

Company imports on 5.2% of RM requirement from China. They have done some backward integration for few products.

Management believes Chinese companies can restart their operations but it will come at a higher cost. They don’t believe Chinese are going to be a big threat.

Partnerships, Subsidiaries & Segments:

Management did not speak about segments in much details but gave some comments.

Company has entered into a partnership (ANAVEN) with Akzo-Nobel and will start contributing by end of this fiscal. In the partnership, company will make a product called MCA where Atul will provide help in two processes Chlorination and Hydrogenation by providing raw material. These will be on Cost+ model and hence company won’t get impacted on margins. Current capacity for the product is up to 20,000tons but this plant will be much bigger in size. 1st phase of this plant will start by end of this fiscal. Total investment in this plant is 250crs of which 190crs will be in phase 1 and rest 40-50crs will be used to double the capacity going forward.

Aromatic – Performance was down last year but 1Q growth has recovered and is expected to remain same.

Rudolf Atul revenues were stagnated last year but this year (1Q) it has grown by 30% to 21crs. Management expects topline to reach 100crs+ going ahead

Similarly, for Amal, company is likely to generate healthy revenues. Current quarter topline was 9crs but management expects topline to reach 100crs+ over a period of time.

Retail sales is currently around 200crs. Management expects it to go up by don’t expect to make profits from it.

Working Capital

Receivables have gone up because we took advantage of an opportunity to sell products at a better price in 4Q.

Sales in brazil and other countries have higher receivable days.

Expects working capital to remain around long term trend

Contracts

Generally enters into 3 months contracts and RM difference is passed on quarterly.

Don’t get into Fixed price contracts. Hence margins cant be very volatile. It remains in a range

Consciously don’t enter into very long term contracts.

Competition

Have competition in all the products we produce. Few combinations that we make have less competition.

Vision

Short term vision is to achieve 4000crs topline and

Long term to achieve US$1bn.

Have been doing capex as they see lot of opportunities. Expanding capacity internally and expects future to be better. Refrained from giving 1-2-5year numbers specifically margins etc

Capex:

Board has approved total of 10 projects: Expansion (5)- 304crs, Debottlenecking (3) - 25crs and Environment (2) - 74crs. Taking the total to 403crs. These projects have potential to generate revenue of 700crs. Also, this will help company to grow beyond 4000crs topline towards the long-term goal of US$1bn.

Hi, does anyone knows why promoter has pledged 3.76% of shareholding? I recently started looking at Atul Ltd and Aarti industries and was comparing these two companies. I will appreciate if someone has already done the comparison between these two companies and can throw some light.

Honestly no idea. Probably for working capital requirements. Chemical industry is capital intensive in nature, & companies like Aarti Ind., Deepak Nitrite etc. usually take debt for that purpose. In contrast, Atul is virtually debt free and so it is quite possible that promoters have pledged a small amount for the same purpose.