Neuland thoughts

In last few months after the management analysis, I think that management is minority shareholder friendly. Neuland answered my questions and helped me understand their business.

I was astonished when someone from the EY representing Neuland came to answer about my questions that I raised over email. This conversation happened before the Karuna BMS deal. It is the first time something like has happened to me.

I have raised questions to Syngene but my email went unanswered. I assume that they made this annual report more comprehensive by including the answer to my query which is great I think.

The major questions

Q1) Why is the reduction of the commercial molecules from Q2FY23 to Q2FY24 when we have never lost a customer?

Ans) It was due to molecule going off patent and its commercial manufactoring ended.

Q2) How frequent is the situation where after going commercial with the molecule, the biotech firms with which we work change the suppliers due to any reasons like being acquired by big pharma, licensing deals with big pharma, due to constraint in capacity, etc. ?

Ans). The answer that came was before BMS Karuna deal. It is seems difficult due to whole validation and US FDA thing. Even after the biotech firm gets acquired, it works with Neuland. Management needs to quizzed more on that btw.

I have more questions which I am thinking of asking in the concall

Q1) If we have not lost any customer and our patents will not expire till 2030, does it mean that our commercialised molecule will keep on increasing?

Q2) Have we lost any customer after they got acquired by the Big pharma?

One doubt that I had about significant stake sale by the Neuland promoter. Sajal sir have answered it as the promoter who has sold their stakes is very old and hence the reasons are mostly personal.

Also, stakes sale by promoter should not be looked negatively but it was significant stake sale by the promoter hence I was little unsure.

I was already thinking of adding more of Neuland after my experience with Neuland mangement.

After the Karuna BMS deal, the probability of approval KarXT increased significantly and I had no reason to not add more.

Hence, I increased my stakes by 50 percent more making Neuland biggest position in my portfolio.

It is more than 6 percent of net worth or 25 percent of my Indian stock portfolio.

Also, I made it nearly 20 percent of my sister portfolio.

My analysis of mental diseases

-

Most people living on mental diseases have reduced cognitive ability due to side effects of current generation of medicine. It hampers their ability to live independent lives. There is some figure that more than 50 percent need some help in their day to day activities when they are on medicine.

-

Though we have medicines for schizophrenia and bipolar but the chances of working of current stream of medicines is nearly 50 percent as said by some prominent psychiatrist in Lucknow. This thing I also verified through some sources on the internet.

-

Even if the side effects gets reduced significantly by KarXt with no impact on the efficiency or even little degradation of efficiency, the demand of KarXt will remain very strong. It is the chatgpt moment in mental diseases as per my research based on internet.

There was one more company in which I was very bullish which was amplitude and had to sell it with 30 percent loss. Hence this time I am little vigilant. It was very painful to book the loss on high allocation bet. Hence this time, I have decided to do some ground work in terms of demand and the probability of Neuland getting the orders for KarXT api.

Kama Holdings Views

As it was end of the month when I increased my stakes in Neuland. I had no money and hence had to liquidate my holding of Kama Holdings. I sold Kama Holdings only as in other stocks I had some profits which I did not want to book and SRF earnings trigger might take some time based on my research.

Though, slowly till now, I have again put money into Kama Holdings though the amount is nearly 40 percent less than the earlier amount.

I have planned to increased my allocation slowly over this month as many research service are predicting correction(Note to self: No one can guess the market in the short term) and hence I might get better value for money.

For the simplicity of the understanding, I only analyse the chemical business of the SRF. Also it the place where they are doing major capex.

One thing that I came to know about SRF agrochemical business was that their contract is majorly of 3 years. From JM financial management meet notes

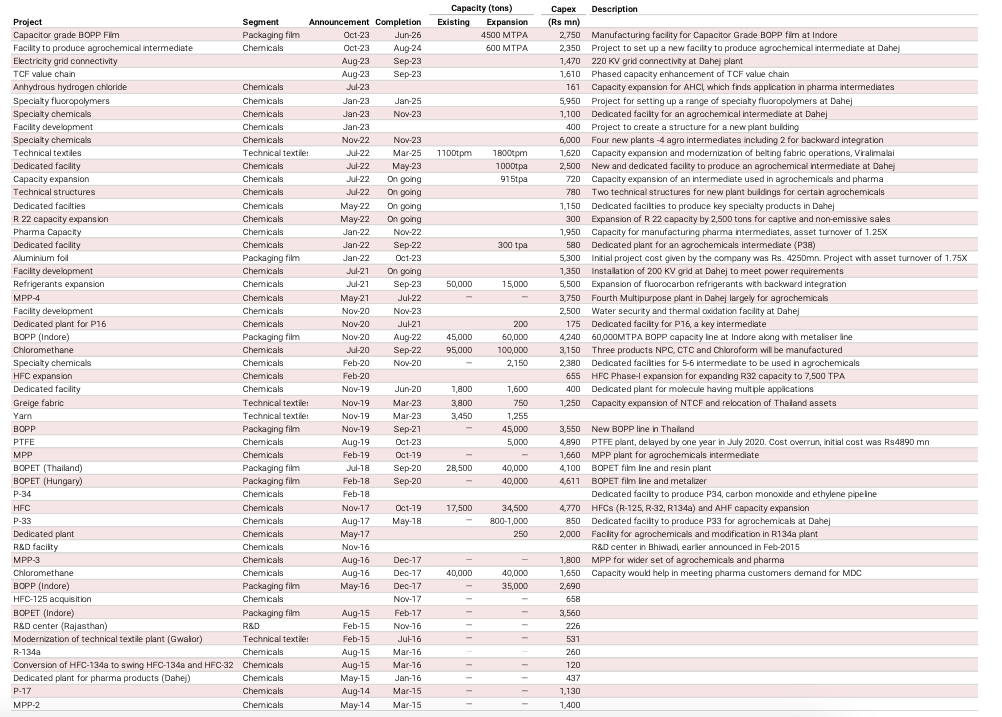

SRF’s ongoing capex includes six

dedicated projects in the fluorospecialty business, taking the dedicated plants’ count to

21. These products are likely to have a 3-year contract.

One doubt that I have about the SRF was, after the production cut of HFCs, how the refrigerant business of SRF would fare?

My doubts got answered after going through the mangement meet notes.

Mostly from Kotak management meet notes

-

Management sees world HFC demand remaining stable over the next few years, with demand growth across the developing world offsetting declines in the developed world. In contrast, HFC production is expected to decline in line with Montreal Protocol regulations(30% production cut in HFCs looming in the US from 2024), leading to tightening demand-supply— particularly in R-32, the most important HFC given its low Global Warming Potential (GWP) value.

-

SRF has the capability to make its production capacities fungible between HFC products (such as

shifting from R-134a to R-32), but not every producer in the world has that capability. This flexibility

should be an advantage for SRF in the years to come.

-

HFC production is expected to

decline amid production cuts in the developed world and production freezes in the developing world.

-

HFO patent expiry and SRF has the lead over HFO chemistry in India

-

(Negative) China would keep circumventing the anti-dumping

duties imposed by the US on China

Portfolio Updates and Others

In last 2 months or so, my portfolio has not fared well compared to small cap index or mid cap index or my mutual fund portfolio(large cap increase in December).

I have restricted myself to small set of sectors that I understand and which I find structural.

Also, the sector should be either classified as defensive or secular.

I also increased stakes in Maharastra Scooters and NH.

The reason behind increasing the stakes in Maharastra Scooters was because it was my top performer and when I added Neuland, it became the second biggest holding on current price on that day. Hence increased its stakes to keep it at the top. Though in last few days, Neuland has became my top holding due to 10 percent run up in it.

Mental model - The Neuland could have been a weed(think Amplitude) and hence wanted to give some water to the tree(Maharastra Scooter).

Allocation to fixed assets(gold and arbritage) is more than 20 percent currently and I would like to keep it same till we get some correction.

I started reading the book romancing with the balance sheet some time ago and then left it.

Now again, I have decided to finish this book to improve my knowledge on finance.

2023 was a good year though. Happy new year to all VP members.

Key highlights related to investing

- Read few books

- Increased my source of Ideas and information

- Have been writing on this platform since a year now regularly