My thought process has been changed a lot since I started writing this thread. Some thoughts that I have mentioned earlier might have changed.

Future incremental Investment in only Indian market

As I have noted down earlier few months back, after the new rules around taxation and discontinuation of sbm bank from indmoney, I have stopped direct investing in us markets with any incremental money. Alibaba that I have been adding lately was from the money that I got after booking loss in Amplitude.

One more reason behind this is that my performance in us market is sub optimal. I was not able to beat the benchmark and I don’t get too much ideas in us market.

Update in mutual fund

I have discontinued the midcap quality index and have transferred my money into parag parikh tax saver. Reason is performance and I have got little comfortable in SMID investing.

My current thought process is to invest in large caps through flexi cap mutual funds and in SMID directly. As the AUM grows, small cap and midcap mutual fund might face problem beating their index.

As parag parikh tax saver(majority in large caps) can invest in all caps and its AUM does not grow much due to 3 years lock in, I am comfortable with it.

Stopped my nasdaq 100 and debt fund sip after new rules in taxation. For alternative of debt, I am putting my money into arbitage.

Reason behind increasing sip amount in arbitage

- I am trying to focus more on direct investing and increasing allocation of direct investing to more than 25%

- need some money in near term.

- Portfolio rebalancing by increasing more incremental flow in non equity assests as equity percentage has crossed 85%.

Currently my sip looks like

35% - parag parikh tax saver

7.5% - canara robeco small cap

7.5% - navi nifty 50 index

50% - invesco arbitage

HCG update

HCG seems to be the biggest in oncology. Need to watch for increase in margins. If it does not happens, then should take an exit.

Book reading update

Currently have stopped reading investment books. Reading software domain book.

Free cash flow and dividend

Free cash flow can also be considered as good as dividend and I should try to value the company at the free cash flow.

For calculating free cash flow, I should subtract the fixed assest cost of centres producing revenue from CFO. Like in Syngene, I should not subtract the mangalore api facility cost for free cash flow.

SRF update

I have decided not to invest in SRF or kama holdings as the risk that I see are more and some things are unknown for me.

My anti thesis pointers

- Floropolymers and flouro chemicals industry growth is single digit and all players are doing huge capex. Source : annual reports

- Not sure when old agrochemicals molecule patent will expire and hence drop in revenue due to off patent molecule economics. Suspecting some might expire soon considering 10 years patent life cycle.

- Agrochemicals custom synthesis market size is small and according to my calculation, there is not much opportunity of growth over 20 percent after few years.

- Not sure whether the process is PFOS free and the regulations that can come.

- Gujurat florochemicals have capitive mines but SRF does not have it, therfore may face margin pressure from Gujurat flourochemicals in flouropolymers when competition arises.

- Refrigerant is not a consumable element that needs to be replaced over time and hence demand will be from new products that are made requiring the refrigerant gases. Same can be said about fluorpolymers as the nature of them being stable and hence it might not require replacement.

I though have bought small quantity of Kama holdings from my mother account. Though reasons for buying is more of discount narrowing than the capex. As the promoter of SRF might want to sell some stocks of kama holdings as the growth flatten(and due to personal capital requirements) and they would want a reasonable valuation for their share in kama holdings. There is two ways to do this, either the discount will narrow or the kama holdings will be merged with the SRF according to my opinion.

Promoter holding has gone to more than 75 percent therefore they are looking for selling some shares due to regulation and hence work for reducing the discount according to my opinion. Also we can not rule out the increase in the revenue and profits of SRF considering some capex is going live.

My mother also have Equitas, ITC and Maharastra Scooters. Her direct stock portfolio account is comparatively a lot smaller than mine.

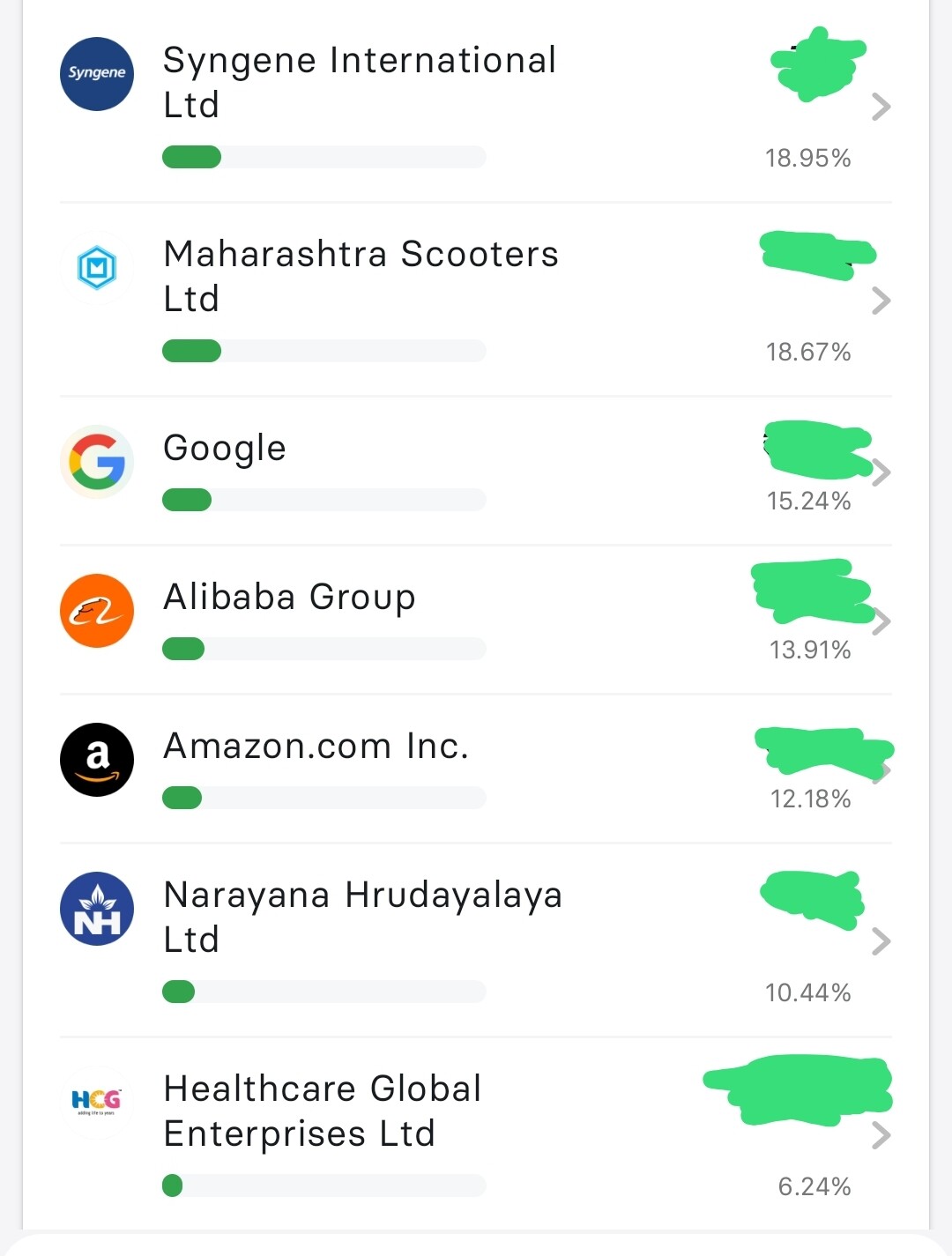

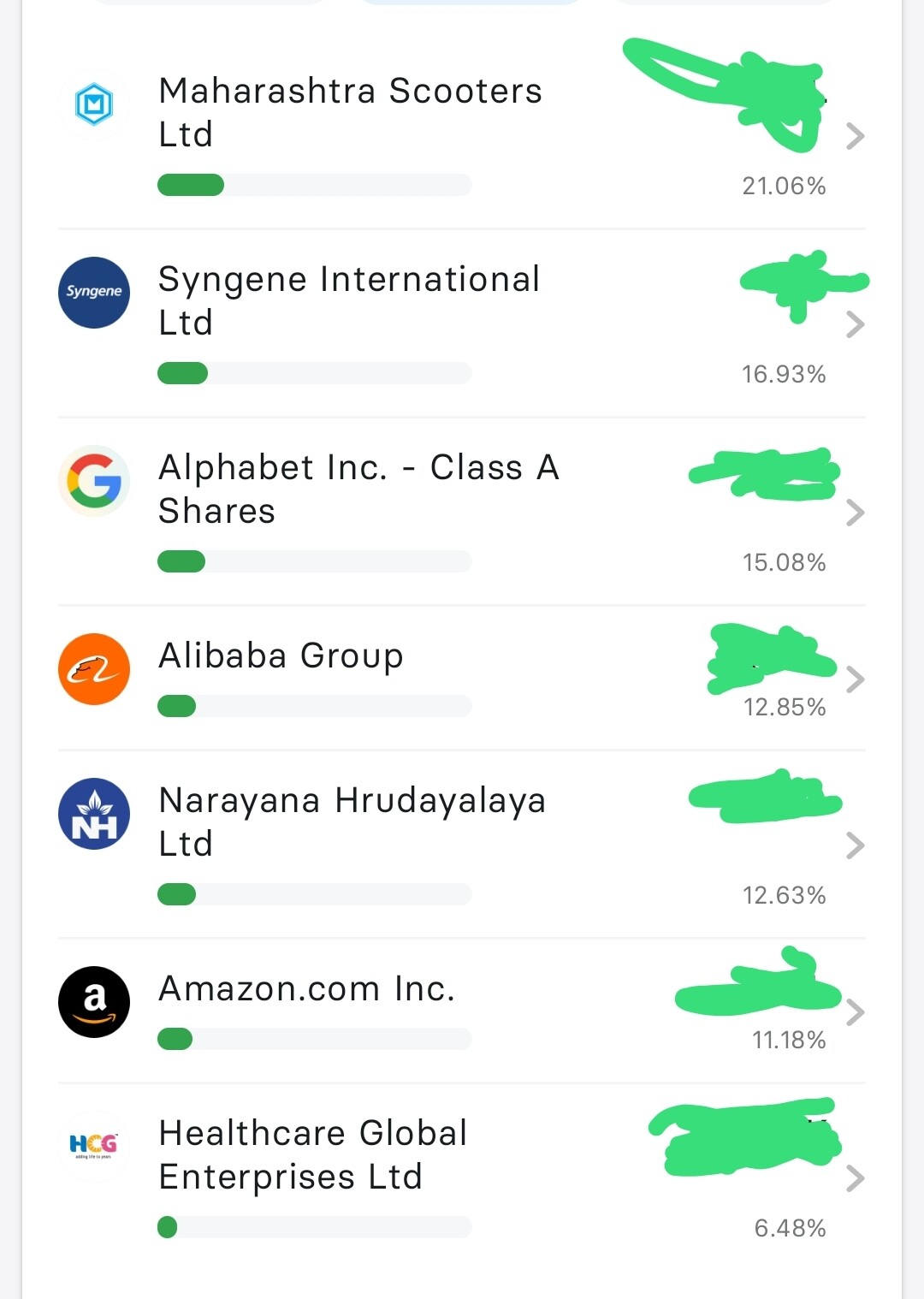

Current stock portfolio

Disclaimer

I might be talking stupid things which I may or may not realise later, therefore please correct me if you think so.