Now ICICI Direct came up with research report with target price of 2120

https://www.icicidirect.com/mailimages/IDirect_AstecLifesciences_Q3FY22.pdf

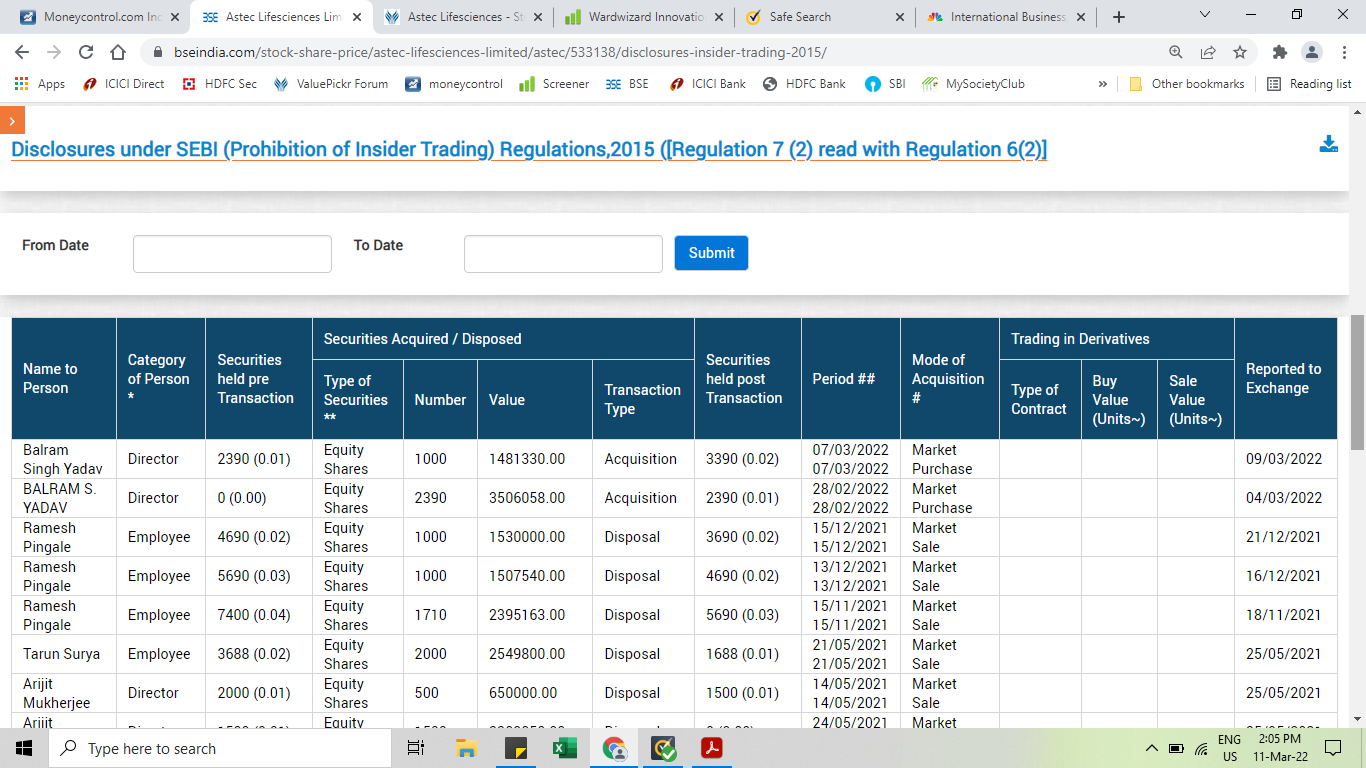

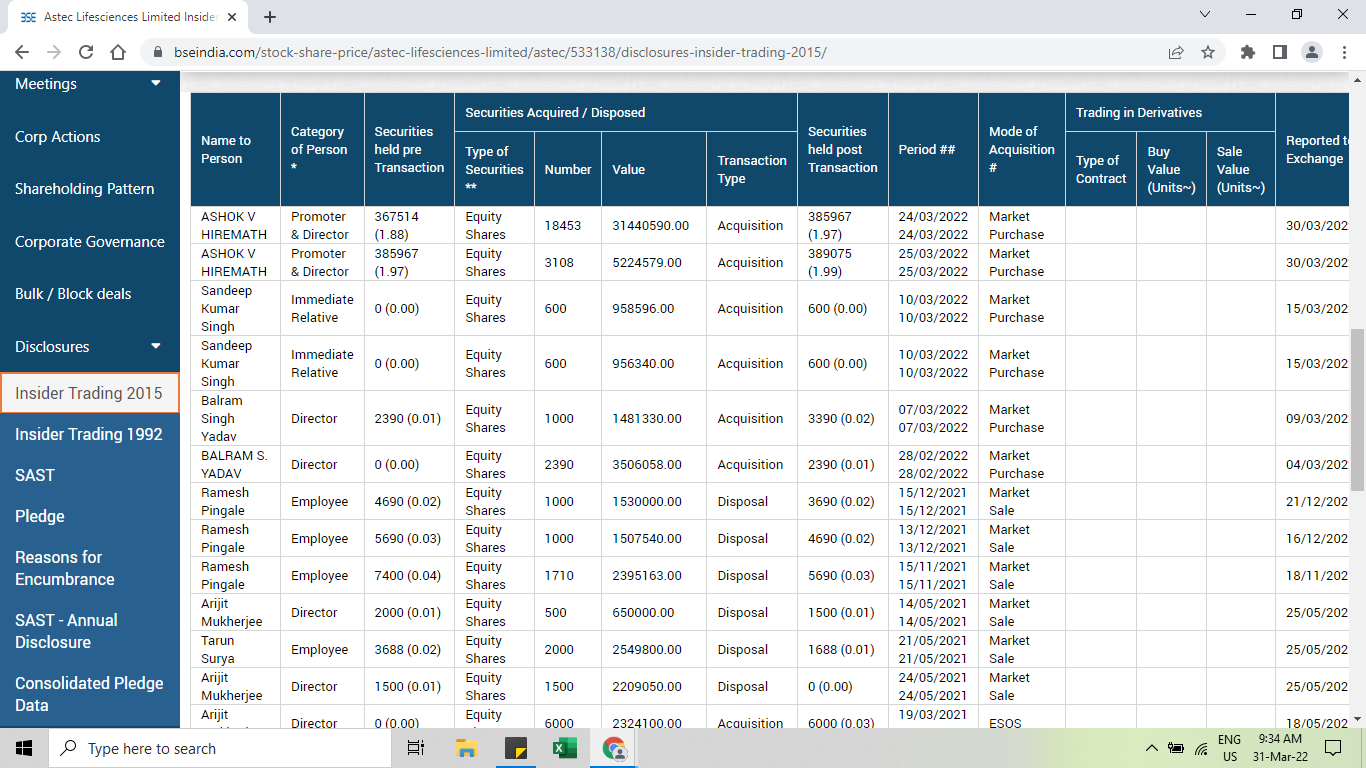

Balram Yadav started buying from market…first time I guess

Very interesting development. MD Mr. Hiremath who will be stepping down today i.e. 31st March has started purchasing Astec shares from market at current valuation… ![]() and quantity is quite substantial i.e 21500

and quantity is quite substantial i.e 21500

Now announcement of Hiremath stepping down as MD

3 Likes

Great results from Astec in current environment!! Revenue up 61% (YoY) and PAT up 80% YoY. Highest ever quarterly sales recorded by the company. For the first time , company is holding concall on the very next day of results i.e. tomorrow. First concall without promoter MD Hiremath (as he stepped down on 31st March) and new CEO Mr. Anurag Roy (ex Navine Fluorine). So lot to look forward to…

Update - Good concall. Few highlights below

- No plans for merger with Godrej Agrovet as Astec has sound balance sheet and can stand on its own

- Plant to spend 350-400 Cr Capex in FY 23 - R&D plant -115, Further herbicide plant expansion - 35, Facility upgradation & Safety - 80, Multi purpose plant - 150

- Company with gross block of 450 Cr , planning for capex of 350Cr+ in a year shows confidence of management towards its future

Concall audio recording

10 Likes

Concall transcript

ICRA credit rating. Outlook revised to Positive from Stable

credit rating rationale.pdf (438.5 KB)

1 Like

Any reason why Trade receivable as a percent of sales is high for F.Y 2021-22?

Another example of How peak PE+Peak Margins+Peak narrative can be deadly in the short term.

Realizations led growth in Q4 and that has reversed. Thus, it pays to track end product pricing in B2B businessess. Severe margin contraction in Q4 results

Disc: invested with 1% allocation. Looking for pain here as medium term seems solid.

13 Likes

Promoters (Godrej Agrovet) have once again started buying shares from market. They have increased their shareholding by more than 1% in last 15 days. See link below

Great result from Astec. Doubling of Sales and Profit on YoY basis. On QoQ basis, whiles sales are up by 10%, PAT is up by 60%… will be interesting to listen to concall on Monday

3 Likes

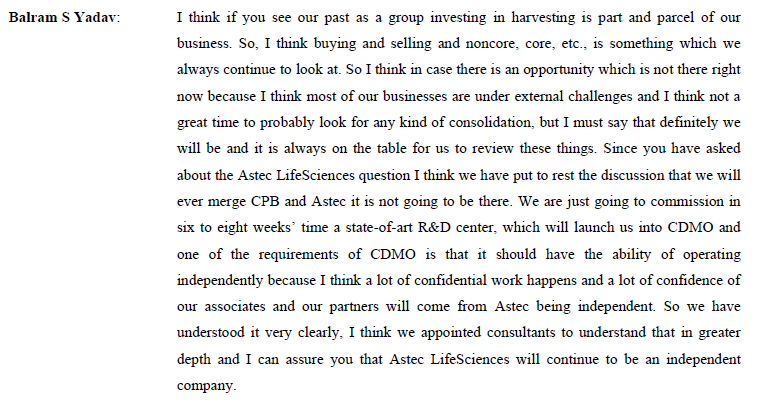

In yesterday’s Godrej Agrovet concall , which was attended by Anurag Roy of Astec (looks like promoters are going back to not having separate concall for Astec but covering it in Godrej Agrovet concall), Mr. Balram Yadav has categorically clarified that Astec would continue to remain independent company and possibility of merger with Godrej Agrovet is off the table. He said that they have hired third party consultant who have advised them to keep Astec separate in view of confidentiality concerns of innovator customers in CDMO business.

So finally this monkey off the back… one of the biggest risk for this stock gone away…

Extract from Godrej Agrovet concall transcript as below

disclosure : invested for last 5 years. Transactions in last 30 days. part of my core PF

7 Likes

Astec life - Credit rating update (march 2023)

1…CAPEX

Company has planned a sizeable

capital expenditure over FY2023-FY2024, which will be funded by a mix of debt and internal accruals.

2…NEAR TERM CONSTRAINED PERFORMANCE

=Near-term operating performance is likely to remain constrained on account of challenges faced in

its key product segments of triazole fungicides.

=With higher than average channel inventory in these product segments in domestic and overseas markets on account of multiple reasons over the recent past (such as lower liquidation, unfavourable weather conditions and destocking strategies), the volume off-take as well as realisations have been muted over the past few

months, and expected to remain so over the near-term till the situation normalises.

=Consequently, Astec’s operating profit margin (OPM) has reduced from 23.9% (FY2022) to 14.1% (9M FY2023).

=Coupled with continued debt-funded capex, the credit metrics of the company are unlikely to materially improve over the near term.

3…NEW R&D CENTRE

=The company has also made investments towards a new R&D facility, which would augment its new product development capabilities and thus benefit from the opportunities that the global demand shift from China may present for the Indian entities.

=Company is commissioning a research and development (R&D) center in the coming months, and expanding its presence in the higher

margin contract development and manufacturing (CDMO)segment so as to mitigate the risks related to product concentration and protect itself from the volatilities of the commoditised enterprise market.

4…COMMODITY PRODUCTS AND CDMO

=Astec operates in the off-patent and commodity chemical markets, its

revenues remain susceptible to global demand and supply dynamics and the resultant pricing pressures as visible in the current year performance.

=As part of its efforts to

strengthen its business profile by reducing its dependence on commoditised enterprise products, the company has been focussing on increasing its revenue share from the higher-margin and predictable

CDMO segment.

= Accordingly, the share of CDMO segment in Astec’s revenues increased in 9M FY2023, and is expected to

further increase going forward.

5…RAW MATERIAL AND BACKWARD INTEGRATION

The ratings also consider the vulnerability of Astec’s profit margins to the fluctuations in raw material prices and its ability to pass on the same to its customers in a timely manner.

= Astec’s backward-integrated operations and continuous investments towards the same mitigates this risk also to an extent

6…PRODUCT DIVERSIFICATION

=Astec currently has a concentrated portfolio of products in the triazole segment

=Company’s planned efforts towards diversification by expanding in the herbicide segment, with the new products likely to result in margin expansion and reduce product concentration risk going forward.

=Astec ventured into herbicide manufacturing in August 2021, and has seen steady ramp up in the volume offtake for its herbicide product offerings.

= Furthermore, the company continues to invest in expanding capacities in this space. Such efforts undertaken by the company are expected to strengthen its business profile

over the medium term.

7…GEOGRAPHY DIVERSIFICATION (EXPORT)

=Revenues remain susceptible to the vagaries of monsoons and the seasonality associated with the agrochemicals sector;

=However, the latter is mitigated to an extent by its diversified geographical presence.

=Exports contributed 63% to Astec’s revenues in 9M FY2023, highlighting

the healthy geographic diversification

8…GODREJ PROMOTER

=Godrej Agrovet LimitedAstec’s parent entity, has been gradually increasing its stake in Astec (64.77% as on

December 31, 2022), which indicates the company’s strategic importance to GAVL and the Godrej Group.

=GAVL has also been providing financial support to Astec by way of inter corporate deposits (ICDs) in case of a need, and ICRA expects GAVL to

continue to do so, whenever needed.

Disc…invested and added recently

My latest portfolio

2 Likes

ICRA credit rating report.pdf (422.4 KB)

New R&D Centre opened. Planning to double workforce of engineers and scientist in FY 23-24 (from current 100). This will help company enter into new chemistries like fluorination

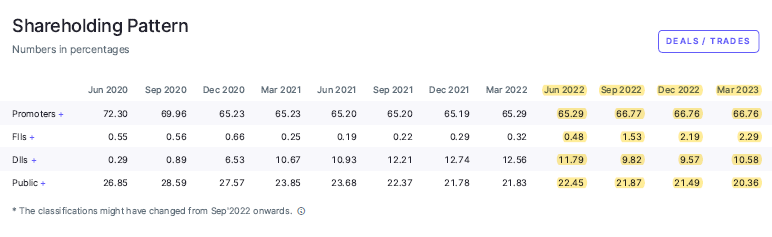

Last 4 quarter promoters and FII and DIIs are increasing stakes as per SHP below

1 Like

Very bad result by astec in consecutive 2 quarters .

No pricing power

Behaving like cyclical company .

Disc…invested

2 Likes

If there is latest investor presentation or con call available, please share

Thanks

Agrovet’s Conf call has some commentary - https://www.bseindia.com/xml-data/corpfiling/AttachLive/9b353407-ab98-4ec9-b64f-633d7969c3c6.pdf

They have stopped astec’s seperate concall and investor presentation since nov 2022?

I cannot see in screener

Q1-2024(aug 2023) con call on astec life

(from godrej agrovet)

1…PERFORMANCE

There are 2 segments of the business.

A…Enterprise business

B…CDMO segment

A…Enterprise business

Poor performance was due to

A1 -Demand-supply imbalance and depressed realizations

in enterprise products portfolio in both domestic as well as global markets

=Topline and profitability were severely impacted due to sluggish demand, lower realizations and high-cost inventories of

enterprise products

A2 -High-cost inventories further impacted profitability

B…CDMO business

=Revenues grew 3.0x y-o-y led by new product development while profitability also improved

2…CDMO BUSINESS

=CDMO business in Astec LifeSciences expected to see 20-30% growth YoY.

=Capex plans include expansion in Mahad and new multipurpose plant.

=If you look historically for the CDMO business, we have been doubling our revenue, obviously from a smaller base, but we have been doubling our revenue year-on-year. So our revenue was close to INR 84 crores a couple of years back, last year we closed at INR 162 crores. And coming year,

we would like to maintain almost similar or closer to that run rate. So that is our guidance on

how it looks like.

= I think one of the key requirements for a successful CDMO portfolio is R&D, and I can definitely say that within 6 months of submissions R&D center, we are hand full with several projects And as you were aware that the new R&D center, which has come up, we are almost doubling

down our efforts on CDMO component of the business, which lead us to believe that we would

like to work on 20%, 30% growth at least year-on-year on the CDMO side of the business

=Some of these products have gone from the development piloting to commercial, which has

added to the revenue. But in other cases, we have also built the newer pipeline under the new

R&D center now, we are in a very good situation to double down or triple down on those pipelines.

=This cycle for CDMO, as you know, right from development or scale up to commercial take 3 to 4 years. So there has been a lot of activities that has been done over the

last couple of years to build this pipeline. And with the new R&D center coming up, this will only expedite that entire pipeline generation process. And we expect to reap benefits as we move forward in the coming years.

= On a small base, initially, we may double it once or twice. But on a steady state basis, we are looking at, when steady state is FY 25 onwards. We are looking at the 20% to 25%

increase in CDMO business because that will be our focus.

=And not only the focus on sales, but also focus on investments. Because whatever comes out of

our R&D center in terms of co-creation or working with some partners, it would require us to

put production infrastructure also in time to come. So we have a very aggressive plan.

=And I’m very sure that we are likely to make CDMO a significant part of Astec business in time to come.

Q: We have time let say in the next couple of 3-4 years. So in the

Astec LifeSciences, CDMO business will be bigger than the enterprise business?

Management : So that is our plan and hope, but I cannot say what will happen in future, like we could not

predict for the last 3-4 quarters, what has happened in the pesticides market across the world. So

I think that said that on a long-term basis, the answer is a very big yes.

3…ENTERPRISE BUSINESS

=Astec along with other companies in the market are facing similar headwinds of high inventory, there’s been destocking, which is

happening at the customer level.

=For some of the enterprise products, we believe that the bottom has already reached. We still see some muted prices on to enterprise products. On the others, we are still seeing that the

liquidation in the inventories and the market might take a few more months. And then the market

from the supply demand side could balance out.

=So overall, I would say that things have improved from the last few quarters. It might take you a few more months to achieve normalcy

we see it currently.

=Obviously, we were thinking of the downtrend, but the extent of this huge downtrend was unexpected. We have taken few steps to prevent further down trend

A…We have planned for diversifying our product portfolio with the new R&D center coming in, it has offered us enough flexibility now to experiment and put some of the new product at a much profitable.

B…We are heavily focusing on building sustainable margins from CDMO business and also trying to push some of the new products as soon as what

to mitigate this downtrend from our existing portfolio

C…While our focus primarily on the CDMO business, on the enterprise business, since we have a

very strong triazole platform, technology platform, and we are also investing heavily on some

of the other adjacent platform with the new R&D center. We’ll be strategically looking at molecules within that segment as well to work on and launch in the coming years. While the

focus is more on building the pipeline on CDMO, we’ll also take strategic bets within the enterprise segment.

4…HERBICIDE PLANT

=We will utilize this plant within 3 years and ramp up accordingly and with an asset turn generating 1.6 to 1.8 roughly in that range. We are very much on target or exceeding those targets on the herbicide plant.

5…CAPEX

A=The herbicides Phase I

Phase 1@INR 120 - 130 crores is what we are estimating. And we expect that to be commercialized by end of this year.

There’ll be 2 more capex.

B…Mahad

= We have some more ability to expand in Mahad. So we will set up another facility in Mahad, which will be very similar in size in capex as the one which we have already established.

C… But the big capex will

come – which will drive our CDMO, that will take a long time.

=I think we are still working out

what kind of multipurpose plant we have. But I think that should be finalized in 3 to 4 months’

time.

Disc…invested

1 Like

I bought astec life considering growth stock having 80% enterprise business and 20% CDMO business.My investment thesis was cdmo business as management guided increasing cdmo business gradually.

=However, since last 2 yrs enterprise business worsened due to

A…Demand-supply mismatch

B…High cost inventories.

=Future growth triggers are

A…Increasing Cdmo business

B…Completion of herbicide plant

C…Diversification into herbicides and development of more triazole molecules in enterprise business.

C…Completion of R and D centre

= R&D Center will catalyze Godrej Group’s ambition to be an application-agnostic partner of choice for innovator companies in the rapidly growing chemical industry in Cdmo business.

D…Management guided huge expansion for CDMO business in 2025(Howeve

r it is still not finally decided)

E…Recovery from enterprising business

=I think, this is best time to buy astec life at p/e ratio of 442(buy cyclicals at high PE)

=Though astec is growth stock, its financials of last 1.5 yrs are like cyclical stock.

=I think, as recovery from enterprise business will take place and cdmo business will grow gradually, its operating margin will become stable with15-20% growth in profit in long run.

2 Likes

→ Overall: Intent of proudly manufacturing Agrochem in India for the world. FY23 stats:

- Revenue: Export: 61% & Domestic: 39% | Enterprise: 74% & Contract Mfg.(CDMO): 26%

- Industry expected to grow at a CAGR of 8-10% by 2025.

- Leadership position in triazole fungicides

- CDMO strategy took 5~7 Yrs. to implement- Reguatory Approval, R&D Center etc.

- 4 Mfg. Plants @ Mahad, MH | R&D Center - In Rabale, MH (commissioned in April 2023)

- Expenditure on R&D: Capital – 68 Cr. Vs 16 Cr. [FY22]

- Permanent Employees: 551 & WORKERS: 200

- Number of Shareholders: 18,097. No. of Equity Shares: 1.99 Cr. | Promoter Holding: 66.76 %.

- Key Products: Enterprise & Contract Mfg.(CDMO)

→ Enterprise product: Over-reliance on few of the enterprise products. Strategies: Maintain cost position and broaden the portfolio (fungicides + herbicide). New product development launch in FY24. - Feb 09, 2023: demand headwinds [high inventories with customers due to poor kharif season in the domestic market] & pricing erosion [China’s excess supplies & lower internal demand]

- May 15, 2023: Tebuconazole- price decline 69% [Muted demand in China and overcapacity situation]. Price pressure will continue in FY24. Propiconazole- price decline 44% [inventory pileup & erratic weather condition] | Demand-Supply balanced and should recover with season

- August 10, 2023: Few more months to achieve normalcy

→ Contract Mfg.(CDMO): In long run, this business shall be bigger than enterprise business and will help to attain sustainable revenue and margins. - Revenue 84 Cr., 162 Cr., ~320Cr.(E), and ~550 Cr.(E) in FY22, FY23, FY24 and FY25 respectively

- After steady state (i.e., FY 25 onwards), revenue CAGR of 20~25%

- Within 6 months of R&D center, hand full with several projects

→ Capex: 2nd herbicide facility [INR 120 - 130 crores] to be commercialized by Dec 23 & multipurpose plant - Capex [500Cr.] for CDMO to be finalized by Dec 2023 and commissioned by ~Dec 24.

→ Concerns: Unfavorable and erratic weather patterns | Unavailability of raw materials | Foreign currency volatility and interest rates | Contingent liabilities: ~ 200 Cr.

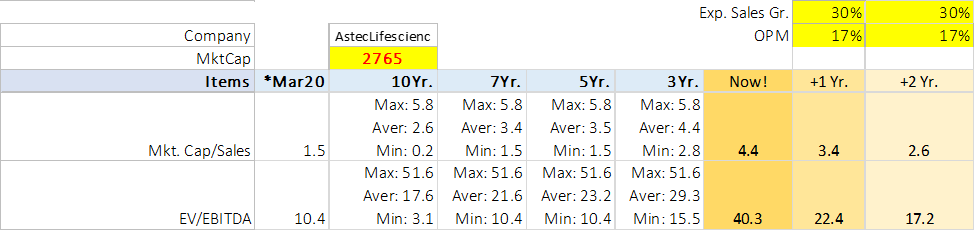

→ Valuation Snapshot:

Sources: FY23 AR, Agrovet’s Conference Calls of Q3 and Q4FY23, Q1FY24

Disc: No position

6 Likes