Management guidance is for 20% YoY growth for annual numbers.

That works out to Q4 EPS of (-0.57+2.70+6.21+15.93)*1.2-(8.27+9.12+3.61) = 8.124. Anything more would be a surprise on the upside. In essence, the base does not matter because they have already delivered fabulous profits in rest of the year.

1 Like

That is true but you have to also consider the fact that the share price also has gone up 4x in one year. So in the short term there might be some time correction if not price correction unless there are new triggers. Just my view and not a buy or sell advise. Thanks!

1 Like

It seems, Varun is son of MD of Astec so it would be sentiment negative for the stock.

1 Like

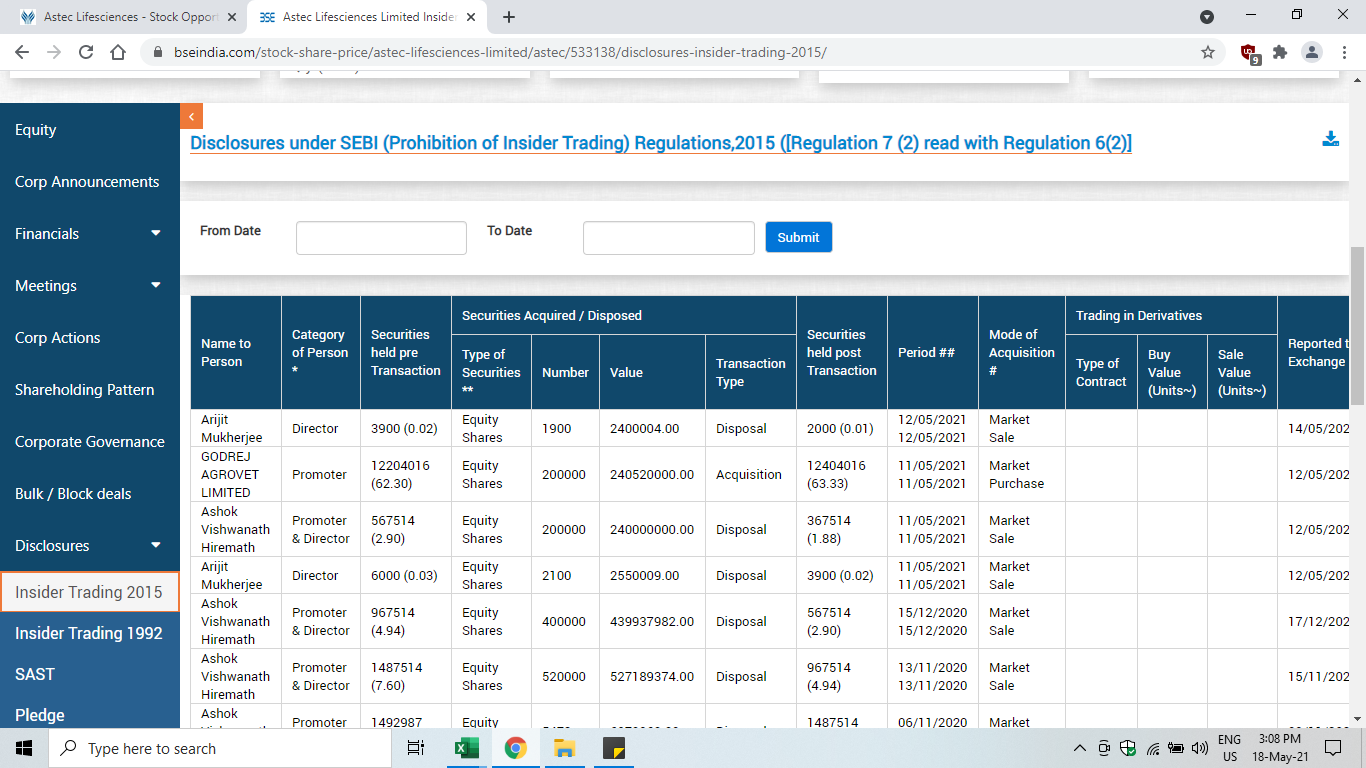

Can someone please tell me why the promoter - Ashok Hiremath has been selling shares over the last two quarters? His stake is down from almost 10% to 3%.

@Rohit_Kadam Please read the thread and you’ll find all the information you need on the selling

3 Likes

As per the news article, even Ashok Hiremath (father of Varun and MD of Astec Life) also has gone missing !!  This is clearly impacting company’s stock price in the short term. Hopefully this should not have any impact on long term future of the company since now it is in Godrej’s hand. But overhang may remain for next few quarters.

This is clearly impacting company’s stock price in the short term. Hopefully this should not have any impact on long term future of the company since now it is in Godrej’s hand. But overhang may remain for next few quarters.

1 Like

Hopefully, we will have the other version on conference call tomorrow @ 3pm , assuming the MD joins the call. Company results have been good but this could be dampener, lets wait to hear from them.

Q4FY21 Concall Notes

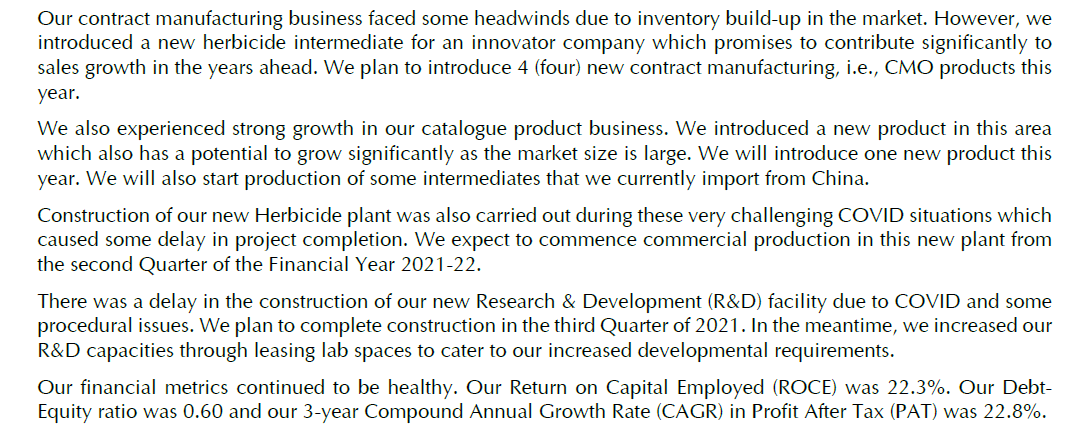

- (Future growth drivers): Launched a new CRAMS product. Herbicide CRAMS plant will be a key future growth driver. In the process of constructing a SOTA R&D facility which will enhance our capabilities manifold. Facility will be completed by July 2022.

- (Merging agrovet and Astec): Looking at the option of merging astec into godrej agrovet. In the long term it would be beneficial since we also have agrochemical business. But no plans in the immediate/short term future. Godrej agrovet is also fast growing and will also get high P/E multiples. So we dont see any problem in merging astec into agrovet. Both are agri related businesses.

- (New herbicide plant): got delayed a bit. Plant is ready, waiting for govt permissions. Commissioning by early june. 25-30% utilization in FY22. 100% utilization by FY24. 50% revenue from CMO and enterprise product in 1st year. At 100% utilization, CMO business will be a higher contribution.

- (New molecules): Last year we introduced 3 new molecules. This year we plan to introduce 4 new molecules. 2 in CMO. 2 for enterprise products. We are working on the biggest triazole fungicide. Will bring it out next year. Best cost position.

- (Operating Cash flow): is slightly negative due to increased WC due to increased domestic sales. Wont sacrifice profits to get cash.

- (Guidance) Guidance of Compounding profits at 20%. Expect that EBITDA margins of 20%+ would be maintained. CMO is 20% of sales. Will try to bring it to 30% in 3 years. Once R&D facility is there, the whole scenario could change.

- (CMO/CRAMS business): had a decline. Key customer had inventory. Didnt order that much. 6.8% decline in CRAMS business this year. This year, we’re gonna make it up with new products and when inventory expires for the client.

- (Capex) 180cr in coming year for R&D center and a new plant will be constructed. New plant will do both CMO and enterprise products.

- (R&D Center): Fluorination will be the first chemistry we will get into in the new R&D center. That involves KF and HF chemistry. We will be more customer and product led. Not very married to chemistry.

- (Concerns about triazole fungicides): were about the older products and chemistries. The remaining/current ones are good from a safety standpoint.

My takeaway: Biggest concern as minority shareholder I have is regarding merger with agrovet. This remains the key risk to investment thesis. Apart from that, astec is a multi year story. New R&D center should accelerate the path to new products, new chemistries and higher profit margins and growth.

Disc: Invested

15 Likes

Mr. Hiremath sold 2,00,000 shares and Godrej Agrovet purchased the same. This brings Mr. Hiremath’s stake in the company below 2%. Since it was purchased by Godrej Agrovet, its a good news for the company. So as I mentioned in the past, Mr. Hiremath is getting out for sure…Will give free hand to Godrej to grow the company faster…

5 Likes

https://www.icra.in/Rationale/ShowRationaleReport?Id=104317

Credit rating report of Astec from ICRA. gives overall picture of company’s strengths and weaknesses

Astec life future growth triggers

Disc…invested

3 Likes

Q1 results on expected lines

Big news is they have hired new CEO Mr. Anurag Roy who was earlier with Navine Fluorine as COO - CRAMS - Pharmaceuticals. He has worked in DSM, Dr. Reddy’s Lab, BASF and Jubilant Life Science earlier. Mr. Arijit Mukherjee will continue to work as COO. This clearly is a road map for MD Mr. Hiremath’s exit. Mr. Hiremath attended today’s AGM and answered all the questions but it could be his last AGM (pure speculation!)

Edit - Astec is interested in fluorine chemistry as reiterated by Mr. Hiremath in the past concalls (post new R&D centre) and now they have hired person who was heading CRAMS unit of Navin Fluorine

13 Likes

Concall Transcript

Herbicide plant commercial production started

2 Likes

Plant stopped due to floods restarted now

1 Like

Very bad result in Q2 2022

9cr/12cr/17cr

Sept2021/june 2021/sept 2020

1 Like

Very bullish concall commentary. They are sure of growing annual profit by 15-20%. Knowing company had poor H1, this means H2 will be a blockbuster. More price increases, more product launches, more higher margin CMO products, Herbicide plant production getting dispatched in H2, 30 Cr of sale will get deferred from Q2 to Q3 (due to customer and logistic delays)

Also Mr. Hiremath is stepping down by 31st March. This will remove one major issue with this company, in my opinion. I think stock will get rerated post Q3 results (if results are indeed good)

1 Like

Kindly share concall transcript or concall summary

Thanks

Great results. Revenue up 47% YoY and 70% QoQ. PAT of 24.71 Cr vs 9 Cr last quarter and 7 Cr last year same quarter… Some of this was expected due to dispatch delays and price increase lag as explained on last concall. But this is much better.

Edit - Press release added today

6 Likes