Sharing my summary notes on the company.

What is the outlook for triazole fungicide market? Long term growth potential and near term tailwinds aiding this type of products?

- Triazole is one of the oldest chemistry. Newer chemistries such as SDHI have come. SDHI has wider applications.

- Triazole market size: $3bn growing at 3%

- Top products are Tebuconazole, Propiconazole.

- Globally China is the largest producer for Triazole. 65% of production happens in China.

- India is also leading producer. Astec is the largest producer in India. Excel Crop Care is another player in triazole market.

- In terms of consumption US and EU are biggest. India also consumes 5-7% of global demand.

- Earlier triazole fungicide was losing market share to SDHI fungicide. But as the fungi has developed some resistance to some of these chemistries, triazole segment is coming back (in a limited way) in form of mixture with SDHI and some other segments.

- Astec is primarily in triazole chemistry. It does not have presence in SDHI.

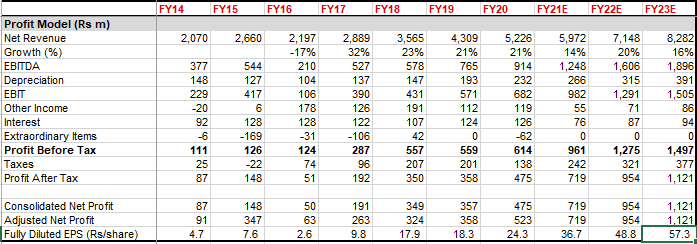

Enterprise segment (FY20 Sales: INR420cr)

- Growth rate should be similar to what the company has been clocking. Higher growth should come from exports.

- Drivers of growth would be 1) Higher market share gain due to China+1.

- Astec is a leading player in triazole. Company claims in triazole it is as competitive as China.

- H2 is seasonally stronger for Astec.

- For the area where Astec focuses climate is not a major factor. Fungal infection is common in India. So domestic business should have less volatility and dependency on monsoon compared to that seen by some other agri companies.

Is Astec benefiting from China +1 strategy?

- China + 1 theme been taking place since 2015-16. It is not a new theme. It is only expected to accelerate post pandemic.

- Astec has gained more business in LatAM, Russia. IN EU, propiconazole was banned. Despite that company maintained its growth in EU. So that tells that ex-propiconazole, it gained business.

- Japan is not a big market for Astec yet. Japan market may grow inline with rest of the markets. In Japan, Astec is likely to get CRAMS business.

Concentration Risk

- Client concentration is not there. That is not a risk.

- Product and chemistry concentration risk is there. It is less of a risk from substitution stand point but more a risk from pricing standpoint if China becomes aggressive and wants to increase its share.

CRAMS Business (20% of top line)

- High margin business which can grow at 30-35% CAGR over next 2-3 years.

- Venturing into herbicide now. Will have presence in herbicide and triazole fungicides. Orders for 30-35% of capacity should be there as soon as the plant commissions. Fixed asset turnover may ramp up to 1.6x in 12-15 months time frame when the herbicide plant gets commissioned. INR80cr capex has been done on herbicide plant.

- Astec is a small player in CMO space but have seen increase in enquires post the onset of Covid-19. Deal closures have not been impacted.

- These are long term contracts. Pricing is negotiated on periodic basis.

Other details

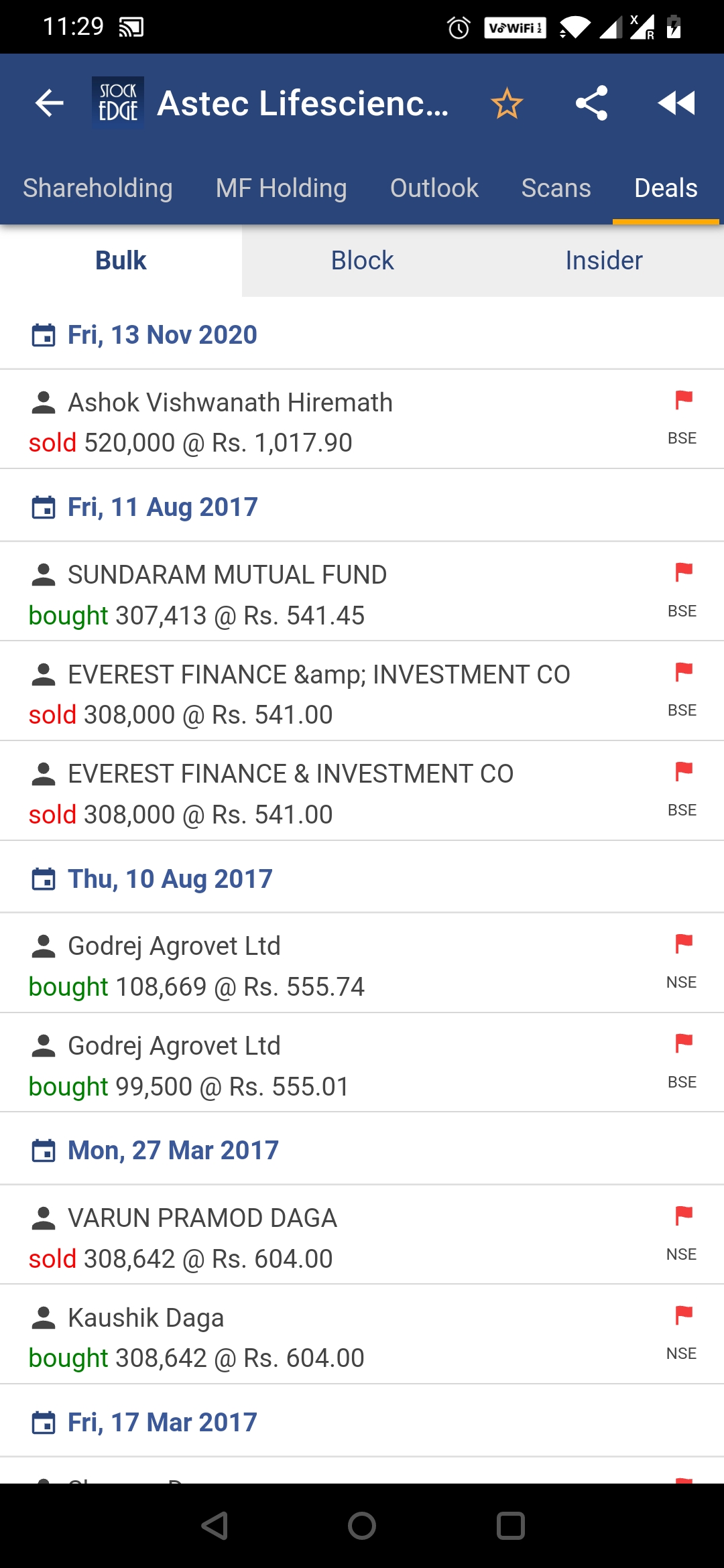

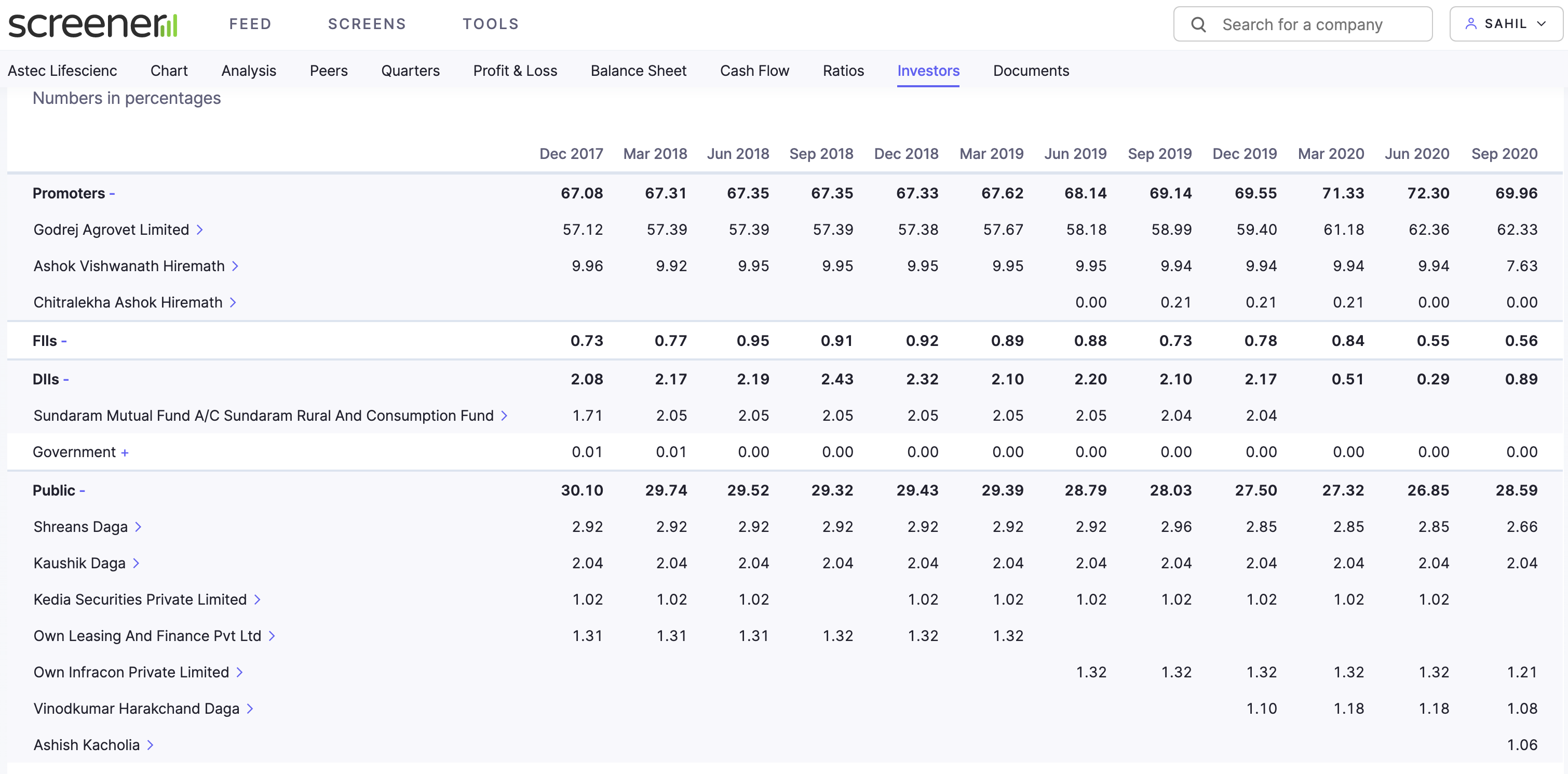

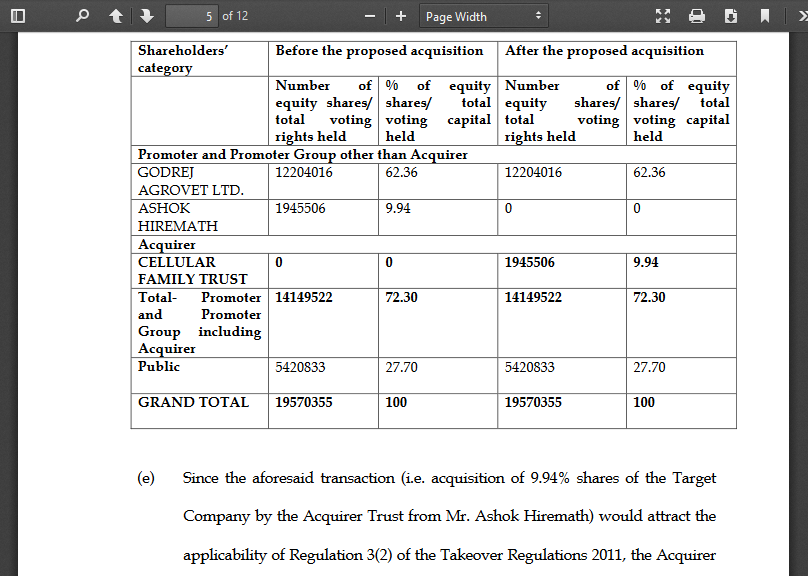

- Wanted a B2B business. Astec was under block. Godrej Agrovet has been buying

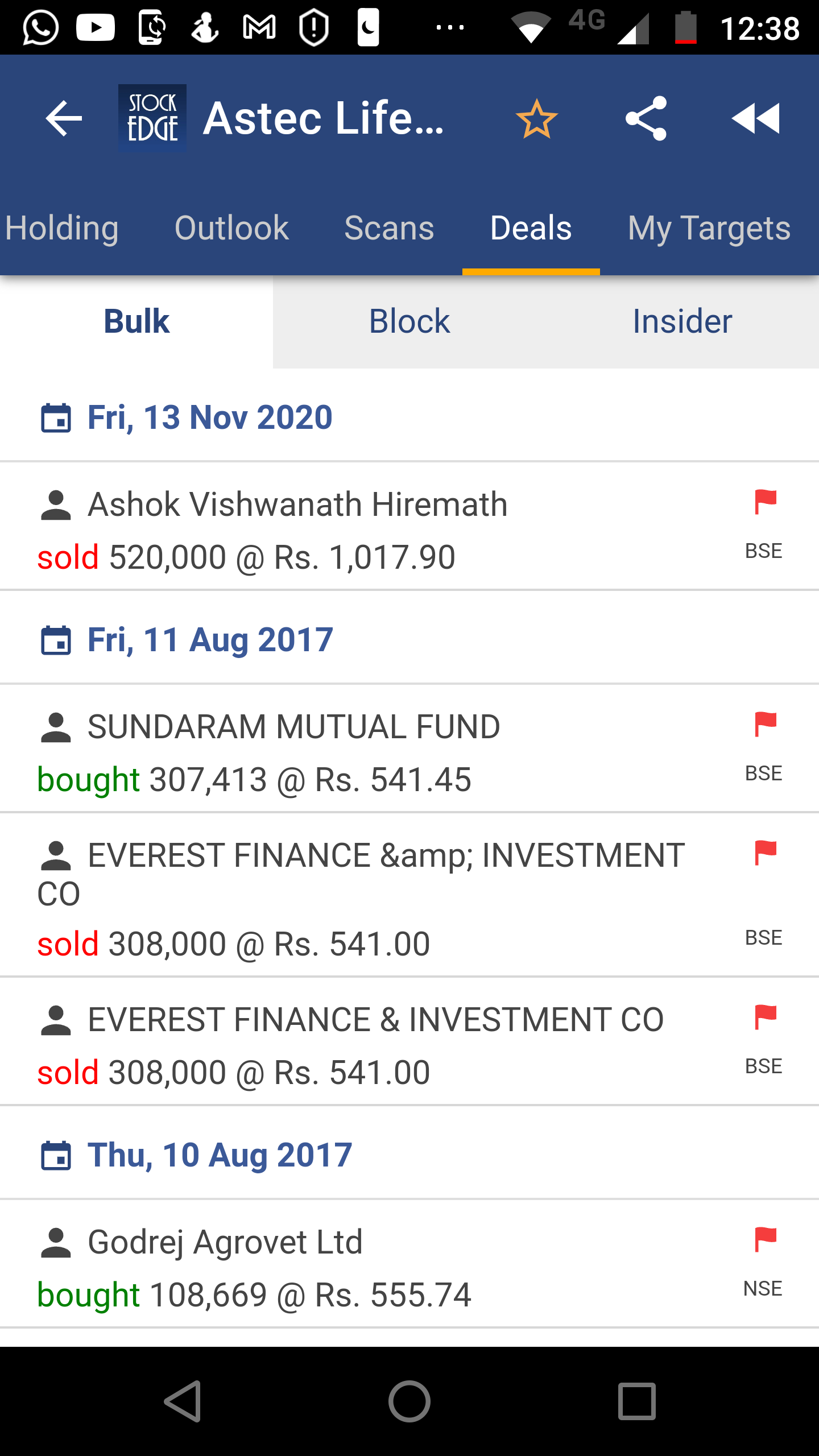

- Ashok Hiremath – Self made entrepreneur. He was free to sell after 2017. He needs money

- He is definitely looking to offload 4-5%. Not sure if he intends to sell completely and exit the business. Second generation from Ashok Hiremath’s family has not joined the business. It is reasonable to assume that Godrej Agrovet will not buy the stake that Ashok Hiremath may sell in near future keeping in mind that Godrej Agrovet had bought at a much lower price and there has been a significant rally in the stock since then.

- Ashok Hiremath is the MD till 2022. Involved more at strategy level.

- Arijit Mukherjee, who had moved to Astec close to 5 years back is driving daily operations. Arijit has been associated with Godrej Agrovet since 2005.

- Company may still go with amalgamation of Astec with Godrej Agrovet. Last year many stakeholders were not happy with amalgamation.

Overall Growth Prospects

- Capex of 300cr is being done which includes 80-90cr on R&D facility. FCF will be negative for few years as company would invest for growth in next few years.

- CMO growth will be faster. Herbicide plant will start by Q4FY21 or Q1FY22. Company is on track to launch new products as well and is pursuing programme to reduce dependency on China.

- Astec is likely to grow top line in mid to high teens and bottom line growth can be higher driven by margin improvement owing to higher mix of CMO business.

Disclosure: 3% position in my equity portfolio

{kind=link}