Archean Chemical Industries Limited is a leading specialty chemicals manufacturing company based in India with a wide presence in the global markets.They are the first of its kind integrated plant in India to produce Industrial Salt, Bromine and Sulfate of Potash.

Following is the product category which the company produces:-

a) Bromine (Br2) is a reactive halogen with a wide range of uses from fire retardants to disinfectants.

b) Sulphate of potash (SOP) is an inorganic compound which is a key ingredients in fertilizers.

c) Industrial salt is a base chemicals which is highly used across industries from glass manufacturing to case-hardened steel.

We can consider Bromine as a Specialty Chemicals and remaining as a Commoditized Chemical.

Bromine

a) It is a member of the halogen family and is found naturally in seawater, underground

brine deposits and other water reservoirs.

b) As per Annual Report 2022-23, Bromine has leadership position in Indian Bromine

merchant sales and Export Business of ~ 48%.

c) The end user of the product being Pharmaceutical Industry, Agrochemicals, Fire Retardants, Water Treatment.

d) From FY19 to FY23, company has been able to grow its Bromine business by CAGR 33%.

SOP

a) Sulphate of Potash, also known as potassium sulphate, is a high-end, specialty fertilizer for

chlorine-sensitive crops.

b) Only manufacture of SOP from natural sea brine, in India which make the product quality to be good.

c) Export Business ~ 70%

d) The end user of the product being Agrochemicals, glass industry, cosmetics, etc.

e) From FY19 to FY23, company business has softened from Rs.40cr to Rs.3cr.

Industrial Salt

a) There are 14,000 commercial uses of Salt, a source of Sodium and Chlorine which are basic components of an array of materials – such as plastics, glass, synthetic rubber, cleansers, pesticides, paints, adhesives, fertilizers etc.

b) Export Business - 100%

c) The end user of the product being Food & Beverage Industry, Water Treatment, Oil & Gas, etc.

d) From FY19 to FY23, company has been able to grow its Industrial Salt business by CAGR 25%

The company has integrated plant in Hajipir (Gujarat), which is located in close proximity to the captive Jakhau Jetty and Mundra Port. Their facility and its surrounding salt fields and brine reservoirs span approximately 240 sq. km. It has a designed capacity of 5 million MT per annum and a capacity to load 28,000 MT equipped with a twin conveyor system, diesel generator set. Globally, two most popular Bromine production sites are near the Dead Sea (Israel & Jordan) and the underground well in Arkansas region in the USA. India is well placed with brine resources at the Great Rann of Kutch in Gujarat

Revenue Mix

a) The company has total 55 clients (Export - 27 clients), Export Revenue - 73%, 64% of Total Revenue coming from Top 10 customers.

b) One of its major clients includes Sojitz Corporation Japan which is also a shareholder in the company with 2.03% shareholding as on 30/06/2023.

Shareholding as on 30/06/2023

a) Promoter Group holds around 53.60%

b) Mutual Fund including Domestic Institutions holds around 30.78%

c) FIIs - 4.06%

d) Large Investors (includes Sozitz Corporation & Piramal Natural Resource Pvt Ltd) - 6.18%

e) Others - 5.38%

Management

a) Ranjit Pendurthi - Managing Director - Bachelor in Economics from New York University & MBA from University of Chicago Booth School of Business.

b) Sairam Edara - CFO - Chartered Accountant

Financials

a) In FY 2022-23, the company generated a total revenue of Rs.1,485 crore of which revenue from sale of core products being Rs.1,440 crore (97%)

b) Revenue from Bromine - 49.2%, Industrial Salt - 50.6%, SOP - 0.2%

c) Export Revenue ~ 72.52%. Revenue from one major customer being 23.4% as on 31/03/2023.

d) The company serves 8 states (India) and exposure to 10 countries.

e) The company has total 636 employees (including outsourced 371).

f) Demand from Statutory authorities under dispute is Rs.6.54 crore as on 31/03/2023. The same is pending with CIT and respective appellate authority.

g) The company is almost debt free with borrowing of merely Rs.21 crore as on 31/03/2023 with banks @ 8.90% p.a.

h) The company has been able to maintain an operating margin of above 40% from last 2 years.

i) The EBIDTA to Cash Flow Conversion is above 70%.

j) The employee benefit expenses of Rs.72 crore includes ~ Rs.23 crore paid to Managing Director (Commission of Rs.18.6 crore has been paid).

Key Opportunities

a) In 2021, the market volume of bromine worldwide amounted to 0.93 metric tons. It is forecasted that the market volume of this halogen will grow to around 1.18 million metric tons worldwide in the year 2029.

b) According to industry report, the bromine global market size was US$3.13 billion in CY2021, and the market is expected to grow at a CAGR of 5.8% between CY2020 and CY2025.

c) The current bromine capacity is at 43,000 MTPA. The incremental capacity added in FY23 (includes 14,500 MTPA) will be captively used for derivatives downstream products which would be in form of fire retardants, etc.

d) To set up a new facility at Jhagadia, GIDC through Acume Chemicals Private Limited

(Subsidiary) to manufacture Bromine Performance Derivatives. Primarily Brominated flame retardants, Clear Brine Fluids & Bromine Catalysts. Global market share for high end flame retardants is expected to grow at 11% CAGR from CY21 to CY25.

Key Risks

a) Dependency on Major customer which accounts for ~ 24% of sales

b) Major geography being China for the company.

c) Promoter salary being major component of employee costs.

d) Downstream expansion and its execution being the trigger as it is a new segment for the company.

Valuation

a) The company recently came up with an IPO priced at Rs.407/- per share. Current market price being Rs.650/- per share with market capitalization of Rs.8,000/- crore.

b) The trailing 12 months PE is at 21.

c) The last few quarters has been soft for the company due to destocking in Bromine. The management feels that export market should come back which would eventually improve the demand and realization.

Note: This is my first thread so please correct me for any errors made. I recently invested in this company so my recommendations might be biased.

I have been researching this stock for a while now.

Below are few risks apart from the ones you pointed out.

The company had a single location in Rann of kutch and the lease agreement with the government ended in 2018 and it never got renewed till date. They didn’t mention this in the IPO document but auditor flagged it in latest annual report

IPO proceeds, i have this bad habit of chasing after money, when loads of it falls into balance sheet.

If you do a basic triangulation of IPO proceeds and profits earned using cash flow statement and balance sheet, you will see (Edited:some money missing probably)

If you read the last 2 concalls there is a book keeping question asked by an analyst which is at the end of the concall transcript.

Q: why did your employee costs suddenly increase?

The finance folk from company said, the promoter takes 2-3% of revenue as commission. This information not mentioned in agm or ipo document anywhere.

The Company entered into Memorandum of Undertaking (MOU) dated August 10,2010, with Government of Gujarat (GOG) for the Land lease which expired on July 31, 2018 and the Company had made an application for renewal on December 28, 2017. As per the MOU with GOG, the lease term can be further extended for a duration and conditions as mutually agreed at that time. There is also a GOG circular no 1597/1372/ dated October 9, 2017 which states that such leases can be extended for a period of thirty years. The company has also been receiving demand note annually for the revised lease rents as per GoG circular and the company has been meeting this payment.

Management made an assessment of the facts disclosed above and taking into consideration

of similar experiences during renewal in group company, is confident of obtaining the renewal of land lease. The Useful life of PPE and ROU assets have been determined by the management considering that the lease would be extended. The entire production facility is located on this leased land.

The table is being published in quarterly PPT but if you can show me how you are getting this number.

This is being answered and we can see this in Annual Report as well. Around Rs.18.60 crore as commission to MD which is obviously odd but not hidden.

@Aditya_Bajoria : Thank you for cross checking the IPO document, which i could have missed.

They are paying money but in last 5 years lease didn’t extend. As you know all industrial salt, Bromine everything comes from this one location. They can clearly write that.

Lets consider this case of taking 2-3% in revenue as commission, if you go through RHP you will see that in the last 5 years (2018-22) . They have 2 bad years where they are negative profits and excessive rains erased all their margins on both the years. 2022 is where ACL had good profits and also inventory turnover. They raised cash at their peak year at 27~28PE to 2022 profits which is their peak year probably. After IPO proceeds they retired debt and all interest costs came to bottom line.

To think through what i surfaced, promoters just raised money from people at a very good valuation(check interest rates they are paying on their previous loans and valuations at which they diluted equity). ACL made good money through IPO and even before first year got completed Promoter had his eyes money.

IPO proceeds are 1462 crores according to RHP.(Page 78) (657Cr to Promoters and 802 Cr new issue).

Lets look at their net cash rough estimate

ipo proceeds 807 cr

Net Profit is 384 cr (not adjusted for recievables)

underwriting expense -40 cr

total 1151 Cr

retirement in debt 828 cr

so total remaining is 323 crores(1151 - 828)

how much did the balance sheet swell by (1756-1532Cr) = 224 Crores.

we now see a differential of ~100 crores.

Lets look at Cash flow statement (FY2023 - FY2022).

Inventories changed by -37 crores

Trade receivables changed by 120 crores

Trade payables changed by 20 crores

Other liabilities changed by 70 crores

Balance sheet

Inventories changed by 47 crores

Trade receivables changed by -40 crores

I was unable to understand how did the numbers differ here between balance sheet and cashflow.

I was probably wrong in using the number 250 Cr, it could be lesser or i could be wrong with my assumption. The numbers didn’t tally for me, so i gave it a pass.

i wasted almost 1.5 month on this, If you could point out what is wrong in my calculation i will change my mind as well, because you rarely get 10x inventory turnover and 40% opm hand in hand.

Edit: Provisions of 8.5 crores were not included in cost…

Hi just one clarification regarding questions raise on mismatch in financial statements

They are also Net investment of 199 crores in Mutual funds during 2023

Thanks

How do you think the Israel-Palestine conflict is going to impact the Bromine industry and Archean Chemicals in particular? As producers at Dead Sea are the largest and lowest cost producers of Bromine globally.

Healthy demand for bromine and industrial salt, and reduced Chinese production due to resource depletion, have resulted in firming up of realisations in the recent past.

The company entered into a (MOU with Government of Gujarat (“GOG”) during the Vibrant Gujarat Summit dated January 13, 2005 and subsequently entered into a land lease agreement with GOG on July 14, 2008 and further executed a supplementary agreement (MOU) dated August 10, 2010, with GoG. Subsequent to the expiry on July 31, 2018, a renewal application was filed on December 28, 2017 as per the guidelines laid down by GOG. As per the MOU and lease agreement executed with GOG, the lease term can be further extended for a duration and conditions as mutually agreed at that time. ACIL has been receiving demand notes annually for the revised lease rents as per GOG circular and the management has been making these payment obligations on a regular basis. If the land lease is not renewed or terminated by the GOG, ACIL may be required to relocate its business operations or shut down its manufacturing facility, which may adversely impact its business.

The company supposedly has favorable political linkages which might be why authorities are mum about lease validity. Nonetheless near term outlook looks good due to war in Israel

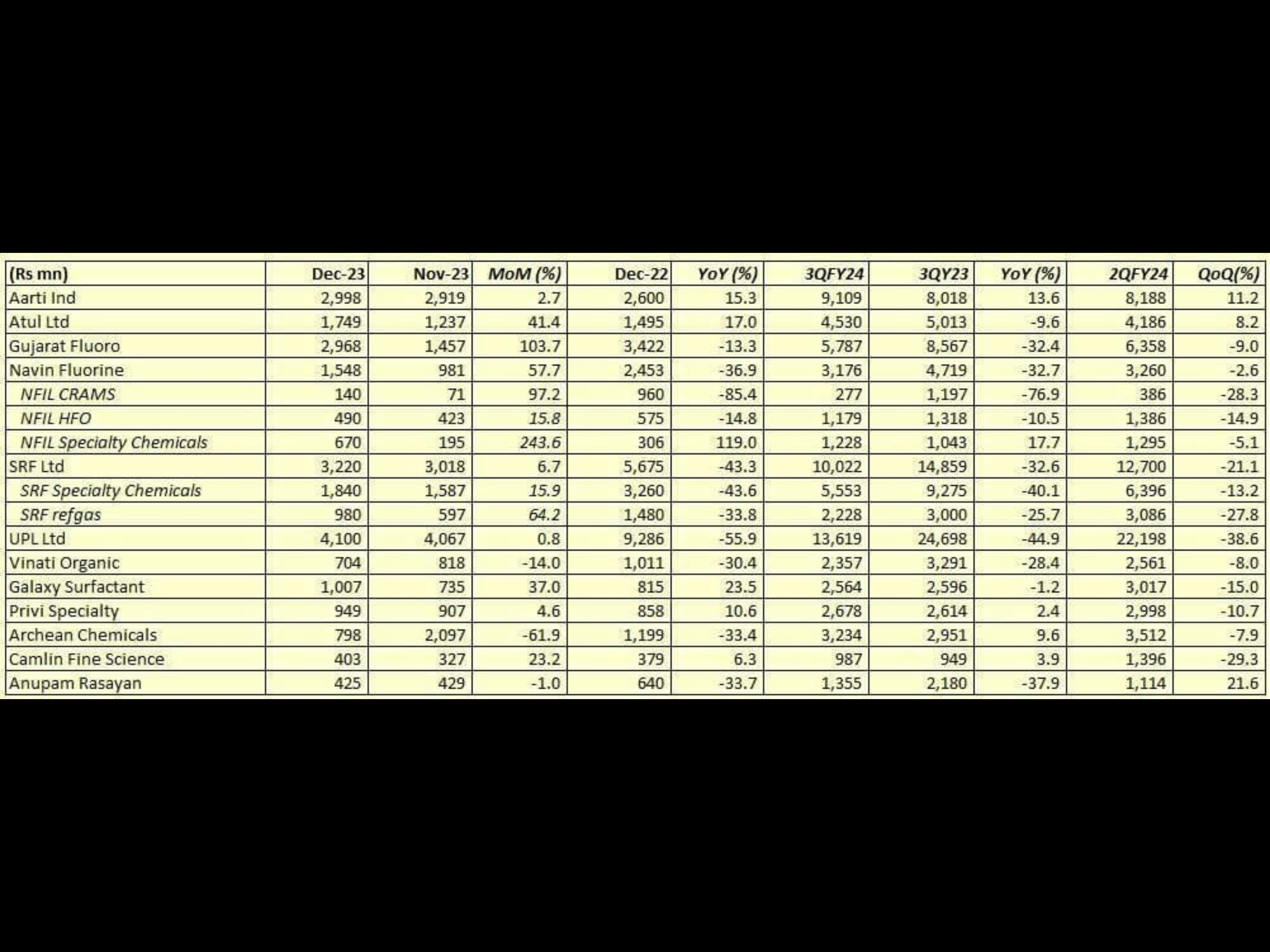

Any opinion on results, it seems below expectation. Revenue down both QNQ and YNY

Ebitda down qnq but stable yoy. Seems same story like other chemical co - but is this slightly more resilient - can we say? Thanks

The affect of War on Bromine realisation will be seen in Q3 results as conflict escalated from first week of October and Q2 was normal quarter and resluts are in line with other chemical companies?

Management guided that he is observing debottlenecking and guided for green shoots. So, more important to listen this concall to get clear picture as apart from media report, nothing is discussed about affect of War for this business in this or any other forum.

Also, there is a mention of upcoming selling pressure as lock-in period for shares will get over (read somewhere on twitter).

My question here for the more informed and experienced members is what is the average reaction on short term price due to this?

Disclaimer: New to investing have minimal knowledge.

I don’t think the war affected the bromine supply from Israel. Very limited operational issues arised which according to reports on FT seem to be in the past. An increased complication in the war could lead to Supply chain issues but for now it seems to be an non event.

the route for their majority export that is china is different orignating from bay of bengal although some impact on japan(8% of export revenue) going from red sea route can be there

source of info: DRHP