What is this information and the source behind it?

Why promoters pledged 4.55% of its holding in Dec '23 quarter? Any info?

Is Archean chemical enjoying these war like situation taking place between Israel and Iran ?

I find this company rather interesting, from a long term perspective. As per the DRHP the Rann of Kutch where Archean leases 6,50,000 acres of land is the second lowest cost source of bromine after the Dead Sea. While even long term contracts will be impacted by spot prices of bromine, the cyclicity should be much lower than that of other chemical companies. Further as this company moves into downstream bromine, the internal source of bromine would give a cost advantage over competition. It’s a nice little long term moat - while 3-4 companies have similar leases on smaller parcels in Gujarat there wouldn’t be too many places in the world which have this kind of advantage - it is a somewhat unique advantage as far as speciality chemicals cos go.

IMO renewal of leases is the long term concern otherwise with 20% + ROCE & 24% net margin in 2023-24 which is like a really poor year in the cycle, the company looks like a long term compounder. 2023 ROCE was 38%+. EvenPE of 24 times (again in a downcycle on low earnings) on CMP of 616 looks quite decent.

10 Likes

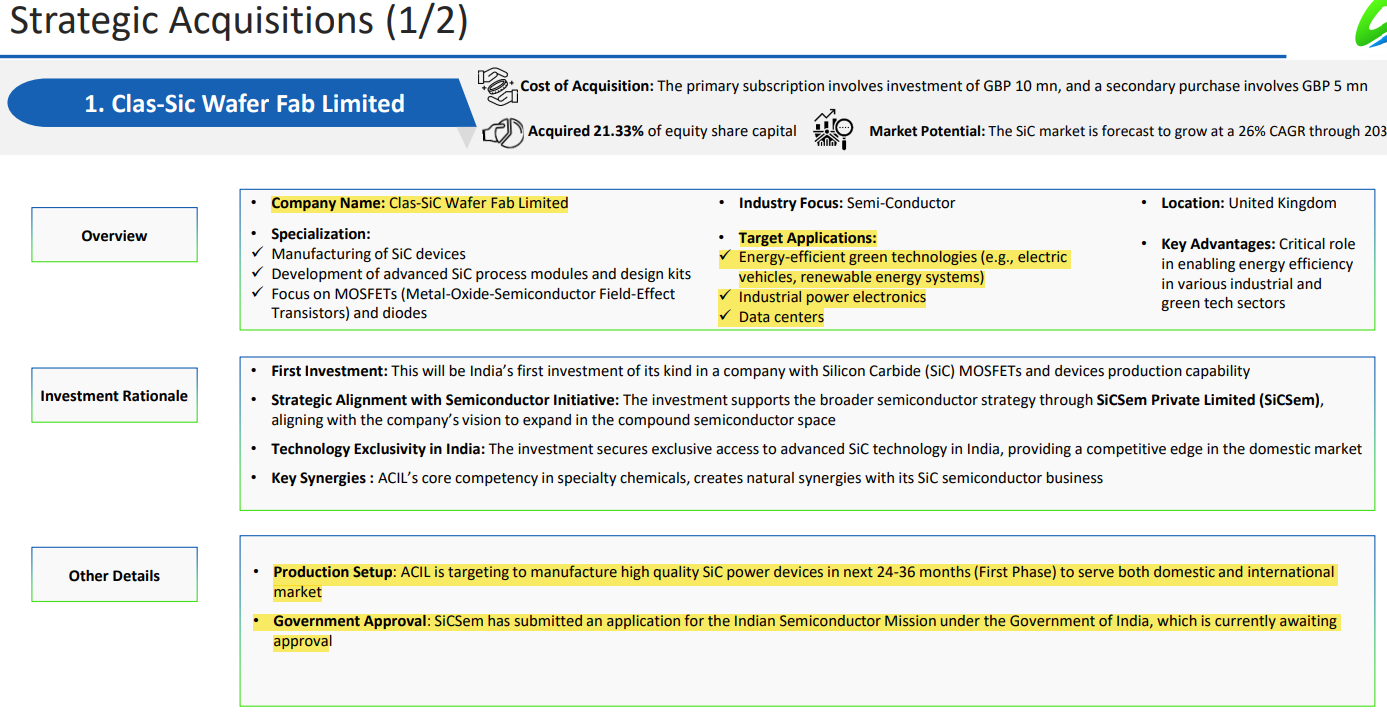

Anybody got any insights on SicSim (a subsidary of Neun Infra Private Limited, which is WOS of Archean Chemical and owns 70% SicSim) and its foray into manufacturing semiconductors?(SiCSem plans plant in Odisha, ties up with IIT)

10%+ shares changed hands in the block deal today done at average 658/-. Sellers were India Resurgence Fund and Piramal Natural Resources Pvt Ltd. Buyers included Goldman Sachs and Nistha Investment

5 Likes

Interesting Update

2 Likes

detailed initiating coverage report on Archean chemical by DRChoksey.

DRChoksey_Initiating_Coverage_on_Archean_Chemical_Ltd_with_24%_UPSIDE.pdf (876.4 KB)

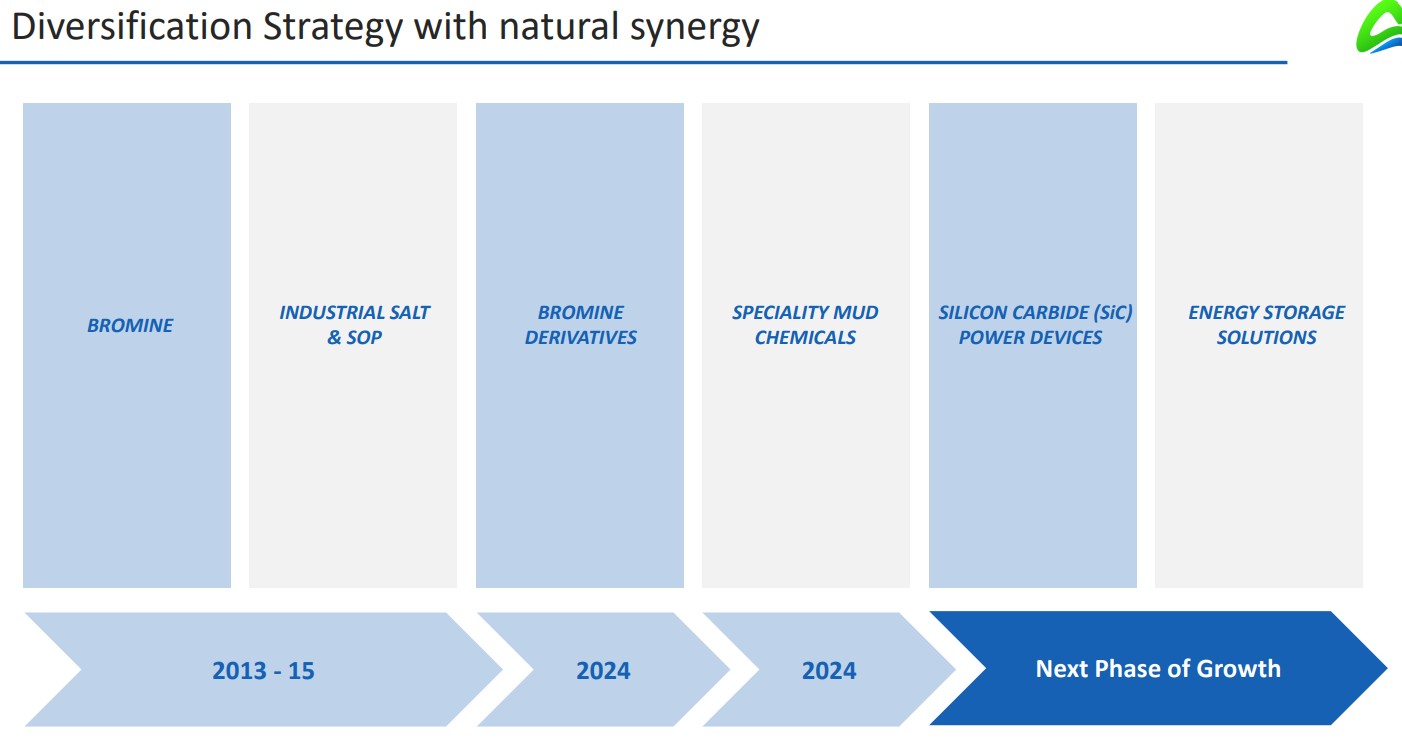

next leg of growth will come from bromine derivatives, 50% capex spending is done and benefits will come from FY25.

below is valuation summary

Archean Chemical demonstrated strong resilience in FY24,

maintaining a 35% margin despite revenue and profit growth

moderation. The industrial salt segment’s robust performance

offset declines in bromine revenue. With INR 130-140 crore

already spent on capex, benefits from the bromine derivative

business are expected to materialize starting FY25E. We

project a CAGR of 34% in revenue and 44% in net profit

during FY24-FY26E, driven by volume recovery and new

product lines. Valuing the stock at a P/E multiple of 17.5x

on FY26E EPS, we recommend a BUY with a target price of

INR 943.

8 Likes

Interesting developments - https://www.bseindia.com/stockinfo/AnnPdfOpen.aspx?Pname=408b5c18-65f9-40be-8b57-3e80ad57cc4d.pdf

This seems to make sense - previous collobration with IIT - diligence + research?

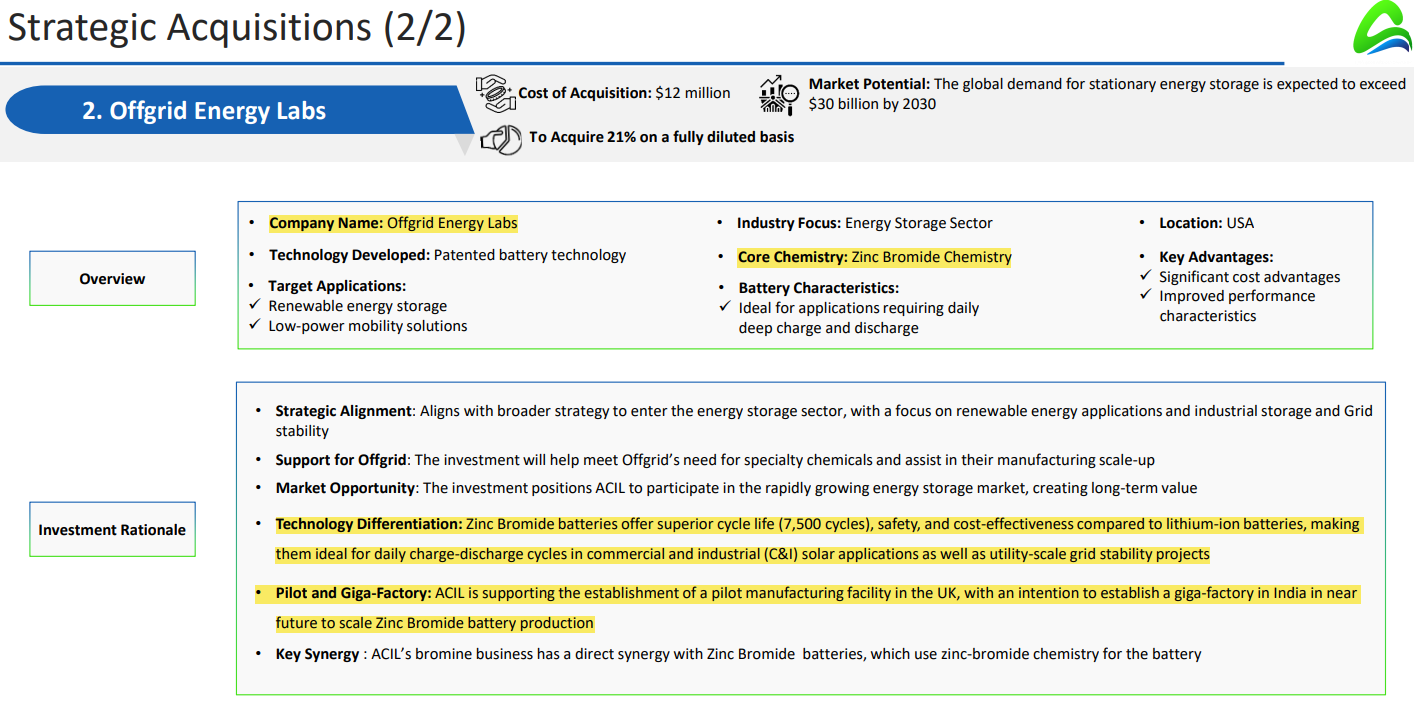

From what I can understand, their bromine derivative products has some key usecase and they are making investments which align with renewable/ev sector and uses their bromine deratives. Offgrid is a pre-revenue company.

Wondering how this will play out.

Disc- Invested

1 Like

Thanks for sharing, It shows management intention to go for new industry uses of their products in Battery storage and semiconductor manufacturing, investment is for 20% stake.

ACI_27102024085050_SEIntimation.pdf (1004.5 KB)

1 Like

In ACIs Bromine business, who are domestic competitors?

In latest concall, one analyst ask the question of increase capacity by competitors in next 2-3 years. Neogen chemicals is there competitor or their client? Anyone here knows about it ?

1 Like

Not many listed players in the bromine space that are competing with ACI. Yes, Neogen is one of their competitors. The silver lining with all its competitors is, Bromine production is correlated to Brine field availability, which is quite limited, and ACI has a huge advantage as it has its own reservoirs which is very cost effective. ACI has a huge land parcel which is very rich in brine, and a lot closer to the ports. Again cost effective. Neogen does not have any such brine fields, and currently they’re running in different circles as their priority right now is to focus on the battery chemistry. It seems as if Neogen could be one of ACI’s clients, as they use bromine to create organic compounds.

4 Likes

management is continuously investing in new companies of battery, Semiconductors , start up to increase the usage of Bromine products, they are trying to expand the market with tie up and investments, this approach is appreciable

1 Like

From Q2FY25 PPT. Company’s positioning looks really interesting. Of course, there are certain risks such revenue concentration, global factors on Bromine supply, Chinese dependency etc. but i believe that management is taking right steps for expanding into new streams as shown in one of the pictures. Valuation looks decent at this point.

DISC: Tracking closely. Not invested.

4 Likes

Can you please let me know what you mean by Chinese dependency? As per my understanding, Bromine is the only element that China doesnt have reserve of (They do have some reserves - but its hard to extract).

Also,I think the next leg of growth will come from ACI foray into Semiconducter facility. This was recently announced.

The plant is supposedly expected to be a 3000cr investment to setup.

(https://www.bseindia.com/xml-data/corpfiling/AttachHis/999f6165-66b9-4954-a8ef-7623f363cb4b.pdf)

Chinese economy would need to do better & revive for Archean to do well. That’s what i meant by Chinese dependency.

1 Like

Here’s a summary of Archean Chemical Industries Limited’s financial performance, growth drivers, and future outlook based on the provided transcript and our conversation history:

Please feel free to add views/comments for improvements.

Financial Performance:

• Q3 FY’25: Total income increased to Rs. 2,547 million from Rs. 2,520 million in Q2 FY’251. Operational profit increased to Rs. 755 million in Q3 FY’25 from Rs. 698 million in Q2 FY’251. EBITDA stood at Rs. 963 million with a margin of 38%, an improvement over the last quarter2.

•9 Months FY’25: Total income stood at Rs. 7,301 million, compared to Rs. 10,791 million in the previous year. Operational profit was Rs. 2,104 million, compared to Rs. 3,491 million in the previous year. EBITDA stood at Rs. 2,710 million, with a margin of 37.1%3.

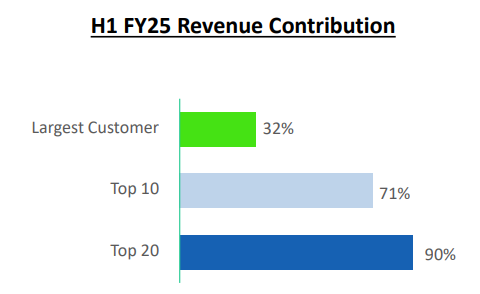

•Revenue Mix: Bromine contributed 38% of the operating revenue, while industrial salt contributed 61% in Q3 FY’252. For the nine months of FY’25, bromine contributed 40% and industrial salts 60% of total revenue.

•Export vs. Domestic: Export markets contributed approximately 75% of total revenue, with the remaining 25% from the domestic market.

•Net Debt-Free: The company continues to be net debt-free with a strong balance sheet…

Growth Drivers:

•Bromine Business: The bromine business is showing signs of recovery with an anticipated gradual pickup in demand. The company expects to produce nearly 20,000 to 25,000 tons of bromine in FY '26, including captive consumption.

•Industrial Salt: The company is optimistic about achieving 1 million to 1.2 million tons run rate in the coming quarters and is constantly working on improving the supply chain.

•Bromine Derivatives: Ramp-up of the bromine derivatives plant is progressing steadily, and meaningful revenue growth is anticipated in FY '268. The company expects a healthy contribution from the Clear Brine Fluids (CBF) segment in the coming quarters9.

•Oren Hydrocarbon: Two units are planned to restart this quarter, with two more in the coming months. This business complements the CBF, primarily catering to the oil and gas industry.

•Semiconductor Manufacturing: Investment in a semiconductor facility through SiCSem Private Limited, with an expected investment of Rs. 3,000 crores. The facility will focus on wafer fabrication for key industries.

•Energy Storage Solutions: Investment in Offgrid Energy Labs Inc, specializing in zinc bromide battery technology, aligns with the company’s broader strategy to enter the energy storage sector

•Responsible Care Certification: The company has been awarded the Responsible Care certification by the Indian Chemical Council, demonstrating its commitment to sustainability, safety, and ethical business practices

•Spot Market Opportunities: There is an opportunity to make a little bit more on pricing doing business on more spot basis

Demand and Future Outlook:

•Overall: Despite macroeconomic challenges and uncertainties in the chemical industry, the company remains confident about its long-term trajectory and growth vision.

•Bromine: Expects a gradual pickup in demand, especially with China’s recent stimulus measures. Prices have remained stable, and in some cases, slight improvements have been observed.

•Industrial Salt: India remains a strong structural growth story within the emerging markets, offering new opportunities.

•Double-Digit Revenue Growth: Archean anticipates double-digit revenue growth in FY '26, driven by pickup in base business and derivatives18.

•Semiconductor and Energy Storage: The investments in the semiconductor and energy storage sectors are expected to contribute to long-term value creation.

•Net Debt-Free Status: The company intends to maintain a net debt-free status and utilize its strong balance sheet for strategic investments4…

•Healthy Order Book: Order book continues to be healthy, with locked-in volumes for bromine and salt for the next six to 12 months. The company has been successful in onboarding new clients, indicating future growth and confidence from buyers for the long term.

Disc: Not invested, Tracking closely

4 Likes

Any insight into who this new entrant might be?

https://x.com/JoshiEien/status/1902530599845556571?t=qwmd7V13gOP7jLMNzflcpQ&s=19