I could not find any thread on this co – so starting fresh - please free to add more for everyone to learn more on this co

Apollo Sindhoori Hotel

M-cap 170 cr (Listed only on NSE)

FY18 Consolidated PAT at 15.2 cr

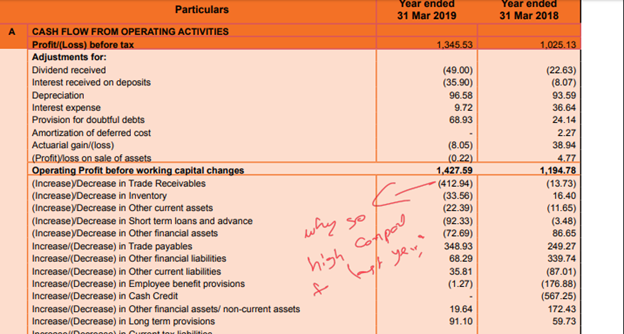

FY18 Cash flow from operation was 17.8 cr

Stock trading at less than 10x FY19e EPS

Zero debt

ROE: 35%

WC days: 60

Cash flow from operations has always been positive and increasing for the co

Promoter holding: 65.77 %

The co belongs to Apollo Group with Ms. Suneeta Reddy on the board as the director

About The Business

The co is majorly into Management Services like Manpower, Utensils, Equipment, Cleaning, Training etc focused on food industry. Management services is a v low capex business and huge cash generation happens

Other vertical is Food & Beverages which includes catering to hospitals,Café (Sketch). This vertical can grow without much capex with Apollo setting small cafes at their own hospital and F&B business growing into non-Apollo business

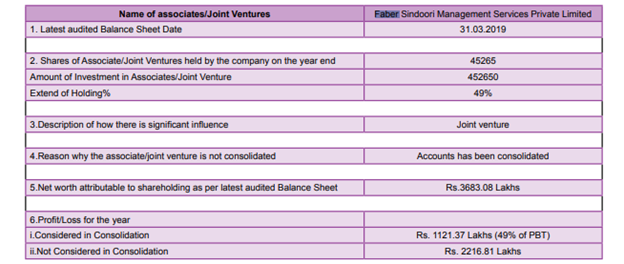

3rd vertical which is the cash cow is the Bio-medical JV with Faber (Malaysian co backed by the government): 51% with Faber and 49% with Apollo Sindhoori Hotel. This is a cash cow business for the company and has been growing vvv strong

http://www.apollosindoori.com/overview.php

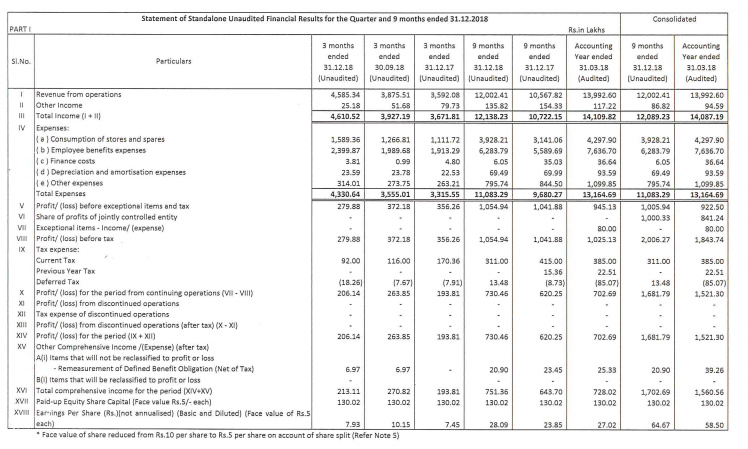

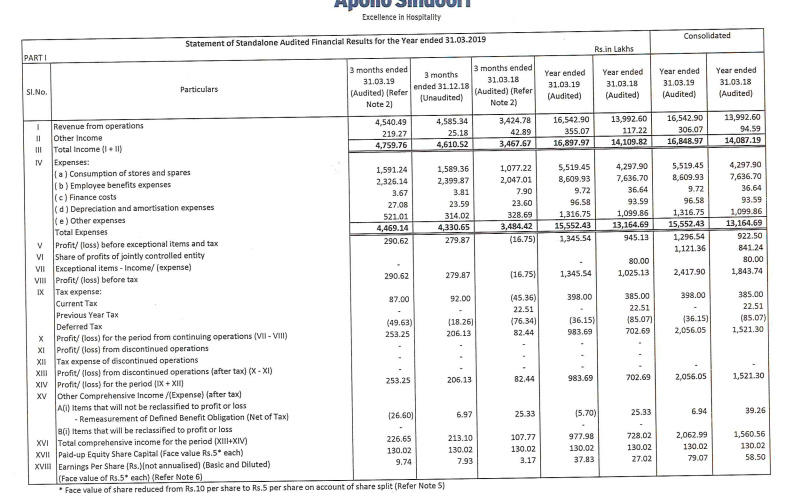

Segmental Results

As per accounting norms, Faber JV sales are not shown in the topline but profits are added in the bottom line as share of profits of jointly controlled entity. So standalone results will not have Faber JV.

FY18 CONS sales 140.87 cr Vs 132.9 cr

• Management services sales at 60 cr Vs 54 cr; EBIT at 4.8 cr at 6.51 cr

• F&B sales at 79 cr (Sketch Café likely around 5 cr) Vs Rs 78.5 cr, EBIT at 5.7 cr Vs 4.06 cr

FY18 CONS PAT at 15.2 cr vs 12.1 cr

• Share of Faber JV at 8 cr vs 5.5 cr

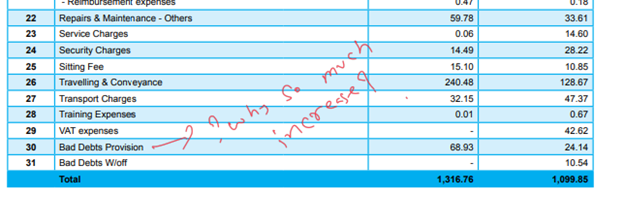

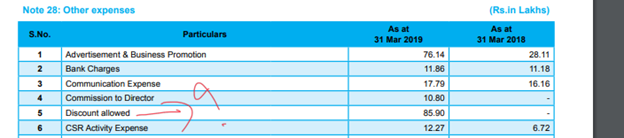

There was 10 cr increase in employee expenses in FY18 Vs FY17 which impacted the management services business (Read note no 6 in March results)

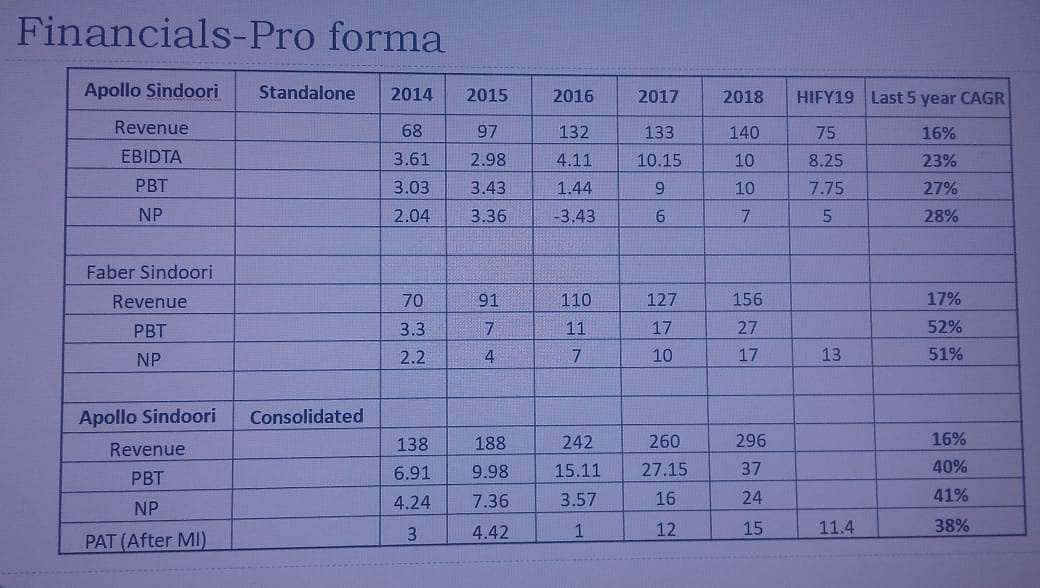

Faber JV

FY18 sales was 167 cr vs 127 cr

Total FY18 PAT at 17 cr vs 11.2 cr

GOING AHEAD

The share of Apollo Group business is around 75%, and non-Apollo is 25%

The challenge going ahead is to increase share of Non-Apollo business

We believe that in FY19 – Non-Apollo should be 35%

As per scuttle butt with industry & company - FY19e CONS sales could be Rs 200 cr (170 cr from existing business and 30 cr from new Non-Apollo business)

On Management + F&B = expected PAT margin 5% = so co can do PAT of nearly 10 cr

Faber JV PAT expected 10 cr in FY19

So total FY19e Cons PAT at 20 cr

We take comfort in the valuations with low risk at current levels

If the management is able to execute with Management services + F&B business (with Apollo background) and some fresh big hires recently – this could be an interesting co for the long-term to track

Detailed financials can be accessed on Screener.in or the co’s web-site