I think they said it will go on stream in Q3 but ramp up will take some more time. Will reconfirm once transcript is available.

4 Likes

Apcotex concall April 2022

1…The growth in fourth quarter and for the year was driven by strong volume across all the industries, geographies product group and also increase in realization.

2…Exportation contribution grew to 21% of the overall revenue

3…Revenue target

=We have potential to grow this business to over the next five years to maybe two and half times the current revenue.

4…Capacity utilization

=We are running at 100% capacity utilization right now even the debottlenecking projects that we took up in this financial year early in the

financial year are fully utilized now.

=Last year meaning in the

middle of 2021 we finished that was small debottlenecking projects to the extent of 10 crores, 15 crores investment which we already completed in that is already on stream and fully utilized.

=Now so we do not have capacity and the new capacity will all start coming on stream from Q3 onwards

when our two big projects are coming on stream

5…Focus on volume growth

=We focus more on our volumes because in our kind of business given their huge volatility their oil prices

and therefore the downstream petrochemicals which are our main raw materials so revenue can vary.

=So, for example, if oil falls to half then you could see a dip in revenue, but what we are more interested in is focusing on our EBITDA margins on our contribution margins and of

course per ton margins as well more than anything.

6…Apcobuild

=I would say for the year for ApcoBuild we are in terms of volume higher by more than a 100% I think 120%, 130% so we feel it is still a small part of a business and we do not give out numbers separately for ApcoBuild, but as and when it becomes we feel it is a reasonable portion we will talk about it more, but as of now we are very happy with the development in sort of

construction chemical ApcoBuild

=For apcobuild, we have clients in Maharashtra, Gujarat, Madhya Pradesh, and Goa was the latest state we entered.

= Obviously since we are backward integrated so we do have some advantage there

=Distribution scale up is really the challenge in the sort of B2C space

where ApcoBuild and we just want to ensure we do slowly profitably and of course we have added some products and we are outsourcing and adding to our product portfolio

=But we want to ensure that what we deliver to the customers is at a price point and the quality that not

available in the market anywhere. So we are focused on the few products and as of now we are still learning and growing in the western part of India.

=We feel pretty confident that the business model that we have being backward integrated and focusing

on few products and few specific niche applications around waterproofing, I think we should

feel confident that over the next few years we will grow our geographically a lot of scope to grow.

7…Capex

… We are doing two projects one in Walia, one in Taloja the one in Walia is completely for gloves there will be some flexibility that we will try and build in, but the one in

Taloja is a multipurpose latex plant and at this stage we are not sure depending on again the

margins we can use it for our styrene butadiene latex products that go into carpet construction

paper and so on or uses for nitrile latex for gloves so I just want to clarify that

A=Taloja @ Latex@ 10,000 tons

=gloves manufact capex will be completed by q2 2022

B=Walia@ NBR@50,000 tons

NBR capex by q3 2022

=We are waiting on the final environmental clearance for NBR project which should come

through we are expecting this quarter by the end of this quarter after which we need to take a call.

=Our new projects revenue would start kicking in from Q3, but obviously it will not be overnight a 100% it would build up over we hope 6 months or it could take a little longer because some of the re-approval cycles from a new plant even for existing customers they would want to test it out for a two, three months before completely moving whole hog

C=We feel bullish as I said, but we have not taken a final call there is no major update. Our focus is just to get these two projects of the ground this in the next 6 months and hopefully as

and when we take a call I will let you know, but it is certainty as part of our strategic plan it is on the cards and one more thing that

=So the cash outflow up to March 31st out of our total project size is about 190 odd crores

between both plants and we are investing in a zero liquid discharge plant in Walia as well so

everything put together out of which we would have spent about 40%.

8…Demand cycle is quite strong

=Unfortunately there are customers that are asking us for materials, but we are not able to go through the approval cycle because we just do not have material to give them even few tons we do not have today

9…Margin

=There could be one or two quarters the margins will fall, but our endeavor is to stay between these 13% and 17% margin

10…Long term growth sustainability

=We feel pretty confident that we can we have developed a set of products, set of customers there are now quite sticky and as I said look there could be a certain situation where for one

quarter or few months where there is certain drop in prices and we are stuck with some high cost raw material inventory because we have no choice, but to stock up on imported raw

material. So, that could happen but in the long term I think as a business we have from strength-to-strength, we have grown our volumes, we have grown our customer base, we have

grown our geographic base within customers we have increased market share overall we have

increased market share we have gone into new industries and steels that we are not in so we have done a lot of work over the last three, four years.

= So, we feel pretty confident in the long run that these kinds of margins between as I have always said between 13% and 17% are

sustainable and we focus on EBITDA per ton. So, I think the bottom line numbers is what we

focus on and I think we feel confident that it is sustainable in the long run.

11…Past few yrs growth

=I think so and if you see the last 6 quarters, 7 quarters I mean we have delivered quarter-on quarter no matter what is happening in the world whether there was a second wave in India, no matter what is happening in China, no matter what is happening due to the war all these

brands of Russian, European we have sort of kept our heads down and focused on our business

and show there are some tailwinds as I mentioned right now for sure whether they last or not we are quite confident that we are quite happy with where the business is.

13…Why growth in last 5 yrs

A…Less Import

=Certainly imports have become harder for everyone and everyone prefer local supply as far as the India market is concerned which is

almost 80% of our total turnover.

=We have certainly benefitted from imports being more expensive due to higher shifting rate, higher detention charges and so on, availability is also an issue in many cases. So, we are certainly benefitted so that is the external factors.

B…Gaining market share

=On the internal side we have done so much work over the last 5 years, 6 years since we acquire on

OMNOVA Solutions India. In our Walia plant as well as in our older business

in Taloja and so we have grown market share across the board and at this point I am fairly confident that across

all the product categories that we have almost all we are number one in India or a joint number one let me put it this way where market share is very close to somebody else.

=So, we are quite confident and if you compare this about five, six years ago I would say you are number one in

the few categories, but a strong number two in most categories.

=So, I think we have grown

market share here in India

C…Export

=We have obviously 200 plus crore of our sales this year is from

export which if you compared to few years ago has been a phenomenal growth multiple what we were, at that time only 30 crores, 40 crores maximum would been our exports at that time.

14…Raw material availability

Overall we are we spent a lot of time these days much more than we are in the past looking at all our supply chain and making sure raw materials arrive on time and we have enough so that the production does not hassle.

Disc…invested since 4 yrs and added recently

My latest portfolio

10 Likes

Good result. Sales up 16% and PAT up 38% YoY

Margins have also improved yoy.

Anywhere in q3 if this comes, revenue and profit will show a marked improvement

Weakening rupee is a challenge for importing raw materials from europe/china. Inflation globally is challenge to export for b2b customer at foreign country.

Disc - holding from much lower level

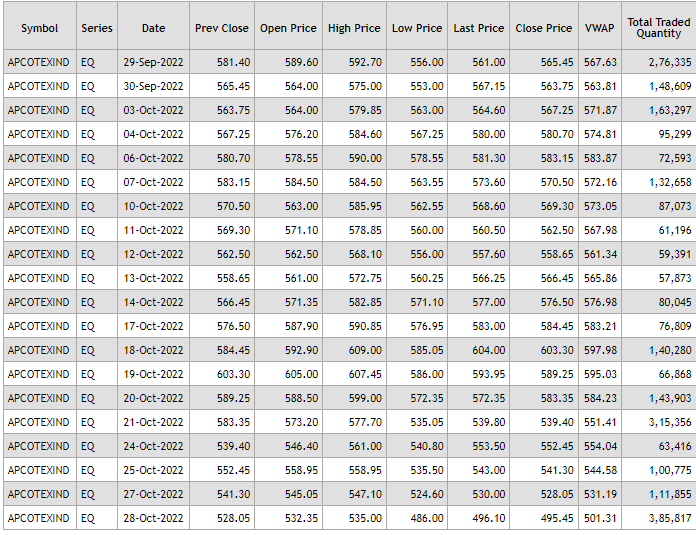

Anybody has idea on the reason for today fall ?

Axis securities came out with a sell report citing head winds due to decline in demand for their products yesterday

2 Likes

Axis target price on sell leg is too near, it reached there in 1 day

There seems good probability of it not holding there and go as down as 415

If such price target text is not allowed in this thread, then let me add some fundamental related lines.

July-Aug-Sep-2022 result was announced 20-Oct, since that number announcement the stock price is losing relentlessly, -20% cumulative from pre-result level.

There is something seriously negative in the numbers which learned people can make out.

I could only find a large increase in borrowing and CWIP during this quarter.

If someone who has understood any major red flag in quarterly result can give some color.

Not a very huge quantity selling compared to the other sessions this month.

Need to track volumes next few sessions.

I feel selling will not be huge. Let us see.

Please listen to the concall, mgmt has said that next 2 qtrs will be challenging … they dont see the rubber gloves business in a bit of trouble. The selling started big time post the concall.

5 Likes

No red flags in this company. Management is honest, open and transparent. Their Nitrile latex plant is coming on stream at a time, where there is tepid demand for latex gloves. This is the reason why management feels margins would be under pressure for next 2-3 quarters. So its demand issue which every company has to face from time to time. Correction in stock price is due to weak hands exiting and will provide opportunity to long term investors to accumulate at attractive valuation.

Disclosure - invested for long term and accumulating at every price drop.

9 Likes

Rightly said. Wish can add at 400 too ![]()

Disc: Invested from Rs 20-21 levels, hence biased.

7 Likes

The main reason why stock has reacted negatively in last 8-10 days after the Q2FY23 concall is due to the uncertainty regarding the ramp up and profitability of the XNB latex project. While Abhiraj was as candid as possible, I suggest members to read more on Topgloves (world’s largest manufacturer of gloves).

Topgloves always used to work on cost plus model (at least since its listing 21 years back). So margins were always range bound (±14-15%). During COVID they abandoned that formula and moved to market linked pricing since demand was very high and supply was not able to catch up. Due to that we saw operating margins moving beyond 50% (we have seen this happening in HEG and Graphite also). The fallout of this was that lot of players announced new capacities and expanding the existing ones.

Now with COVID easing out and with that demand normalizing, Togloves made a loss for the first time in last 21 years. This forced them to go back to cost plus pricing. Also, I believe if leader in the industry is under pain, lot of small players will get wiped out very fast. With that lot of new capacity that became operational in last few qtrs will shut down. Also a lot of planned capacity will be shelved. And with that normalization will be faster than earlier imagined.

Some analyst tracking these companies and sector in South East Asia expect industry to return to normalcy in 6-8 years. I believe in next 12 months, we will have the equilibrium.

Disclosure - invested for last 5-6 years.

14 Likes

Imp Point i noted from this is : The energy crisis can compel several nitrile glove manufacturing units in Europe to scale down operations. A potential increase in nitrile latex prices and disruption of nitrile latex manufacturing in Europe provide opportunities for natural rubber latex, at least for a few months ahead

- “The surge in COVID-19 infections across China can potentially raise the demand for latex-based rubber gloves and other healthcare products manufactured from latex,”

2 Likes

=Promoters are buying constantly from open market

=Apcotex Q2 /2022 -2023 concall

1…We witnessed balanced growth in first half across all the industries and product groups. We continue to run at nearly 100% capacity utilization.

2…Both projects in Valia and Taloja expected to be completed in Q3 of financial year '22, '23.

3…Also happy to inform that the company received the succeeded recognition of Best Under a Billion Company for '22, '23. We are one of 200 companies from all over Asia.

4…Full capacity

=One is on the volume growth. So we’ve seen, as we have been mentioning for the last many quarters that we’ve been running at almost full capacity utilization.

= So compared to the same period quarter last year, it’s been about a 5% – 5% to 6% volume growth. In terms of value, approximately 16% volume – value of revenue growth for the quarter.

= it’s in fact the next 3 quarters that we are going to – we are at 100% capacity utilization.

5…margin and roe

=Obviously the commodity prices have gone up and then for us raw materials have gone up, but we’ve largely been able to pass it through.

=As I told you earlier that percentage margin varies quite dramatically in our kind of business. We would be satisfied with anywhere between 13% to 18% is what – 12% to 18% even is fine depending on where oil prices are.

= The most important metric for us is return on capital and as long as we’re delivering a healthy return on capital, EBITDA margins we are happy to let it vary.

6… Look, first of all, the company compared to the past and now the company is also different.

= The different strategies that we have executed over the last 2, 3 years after the acquisition along with a lot of debottlenecking projects, product mix, customer mix and so on, new products that we’ve introduced. So we feel a lot more comfortable. We are also at a much higher capacity utilization.

7…Apcobuild

=Gujarat, Madhya Pradesh, within Maharashtra also increased our footprint and Goa. So we’re in 4 states. We’re also doing small business in the south a little bit. But I would say largely these 3 states, Maharashtra expanding our footprint and entered Gujarat and Madhya Pradesh over the last year.

=growth will be over – it will be almost 150% to 200% for ApcoBuild this year, 150% at least.

=We don’t give separate numbers for ApcoBuild. It is – as I mentioned before, it’s a small part of our company so far. We believe in the next 3 to 5 years it will become a larger chunk and as and when we feel it has some critical mass which is worth reporting as a separate segment, we will do that.

8…Domestic v/s export

=On the latex side of course, I think it’s more of a regional play. That means we focus on Southeast Asia, Middle East and India because latex is about 50% water so to transport it over very long distances may not make sense.

=our export was close to 0 10 years ago. Now it’s at 21% of the total revenue

9…Capex

= I would say between FY '22 and FY '23, we are looking at about INR 225 crores

=We are working on a few products. As I mentioned last time, as of now our focus and what we’ve announced is the current CapEx for latex products, which is nitrile latex in Valia and a multipurpose latex plant in Taloja, which will include all our current products as well.

=And in addition to that, after that we also – we only have about 30% or less market share in the NBR business in India and we are largely exporting. We believe that in the long run even though it’s not a very high growth industry compared to, let’s say, nitrile latex or some of the latex products, we believe there is a good opportunity for import substitution – further import substitution in India as well as export into Southeast Asia, Middle East and Asia.

=we are doing 2 projects. One is mostly nitrile latex in our Gujarat facility and in Taloja is a multipurpose latex plant. In the beginning, initially we are looking at a total of additional 60,000 tons which would give us about INR 500 crores of revenue. But as I mentioned before that the additional CapEx that will be required for an additional revenue that will come, another INR 300 crores, INR 400 crores will be at a marginal cost. So it will be about INR 500 crores of revenue once both the plants are fully utilized. And as far as EBITDA margin is concerned, obviously EBITDA margins should only improve because our fixed costs will not increase by that much. So we are hoping as we grow the capacity utilization, as we increase the capacity utilization of the new plants, EBITDA margins should only go up.

10…Diversified industries

A=one of the large industries would be paper and paperboard, but even that would not be more than 20% of our overall sales, maybe less than 20% in fact now in the current context, 17%, 18%

B=. Then followed by construction, which includes construction chemicals and paints

C=. Then followed by tire industry, carpet – there’s also NBR, which goes into several industries, right, which is a lot of rubber industries. So that would be another 25% of our sales.

=So fairly well diversified. We’re not dependent on any one major industry. Nothing is more than 20% of our overall sales.

11…Next few quarters @less volume growth due to almost full capacity utilization

=Look, the volume growth, as I mentioned that most of the debottlenecking projects were completed in Q2 and Q3. So Q4 of course we would have a little bit more headroom for volume growth not significantly more, but little bit more. And as I mentioned to one of the previous callers that Q4 onwards maybe for another 2 quarters, we may not have headroom for volume growth

12…X nbr latex

=we have many customers other than pawa gloves.

There was just 1 or 2 that we have mentioned in our presentation because they’re well-known customers. The other problem that we have is a lot of other customers are telling us that look, you don’t have the capacity now, why would we go through this whole process and you won’t be able to give us anything for another 9 months? So why don’t you come to us closer to the date and then we will go through the process. But a lot of them we have done lab trials and whatever we could, but unfortunately, we’re not able to give bulk quantities because we just don’t have the capacity today and it would be at the expense of other customers, which also we don’t want to do which is not a good idea as well.

=Look, when we initially made a decision to get into the nitrile latex market, there was no COVID. This was back in 2016, '17 when we started developing it. Obviously during 2020 and the first half of '21, glove availability and – glove demand and glove availability and therefore glove prices, whether it’s natural gloves or nitrile gloves, were at historic highs. And therefore, obviously the players that were in the nitrile latex market also got good margins.

Now the margins I would say have normalized. They are not under pressure, but they have normalized than what they were earlier –

13…Revenue

=So we think at the peak we can do INR 1,500 crores, INR 1,600 crores as much as INR 2,000 crores once we do the second phase of expansion.

14…Raw material

= I mean I just said we have many different raw materials from some of our A class raw materials like – I’ll just give you an example of styrene. That largely comes from Middle East and Southeast Asia. Another raw material comes from Europe, East Asia, [indiscernible] Nitrile, all over the place. And yes, I mean we don’t have a specific sort of geography of imports from everywhere.

15…Entry barrier

we believe that the product that we have developed, and we are working with our – a harder – it’s quite hard for people to get into barriers to [ enter a high ] – approvals take a long time.

16…Bad case scenerio

= we can use part of the latex manufacturing capacity towards our captive NBR production, of course. But for that, there is reasonable and sizable investments required. So we’re working through the different options right now and seeing in the worst-case scenario. But frankly, we have worked out a pretty bad case scenario

.=But frankly, we have worked out a pretty bad case scenario. And even with those bad scenario, we’re looking at 20% to 25% ROCE on Nitrile Latex. So our focus will be to try and ramp up Nitrile Latex production, get to full capacity as soon as possible.

=So if it goes back to normal, then we can see reasonably good ROCEs and focus on this business itself without looking at contingency plans.

Disc…invested since 3 yrs and recently added more

My latest portfolio

10 Likes

Hi All,

I am a new member of the VP. For the past month or so, I have been in the read-only mode of a few fantastic posts in this community. I am truly grateful to Ishmohit that I stumbled upon this forum thanks to his SOIC course.

This is my first post/question on this forum. I was analyzing Apcotex Industries and I got really intrigued by the strong numbers it was posting.

High ROCE%, good ROE% decent NPM %, reinvestment rate of a whopping 92% over the last 10 years, ROIIC of 26%, and

10-year average ROIC of 16%. The management consists of members with strong credentials. I am considering investing in this company as it is at an attractive price point right now. I am planning to wait a bit for the base to form in terms of the stock price fall currently.

However, while going through the Annual report of FY’22, I also found a few anti-thesis pointers. I will list them here - I tried searching if anyone had asked this question and I couldn’t find it. My apologies if this is a repeat question for you all. Can anyone help me with this?

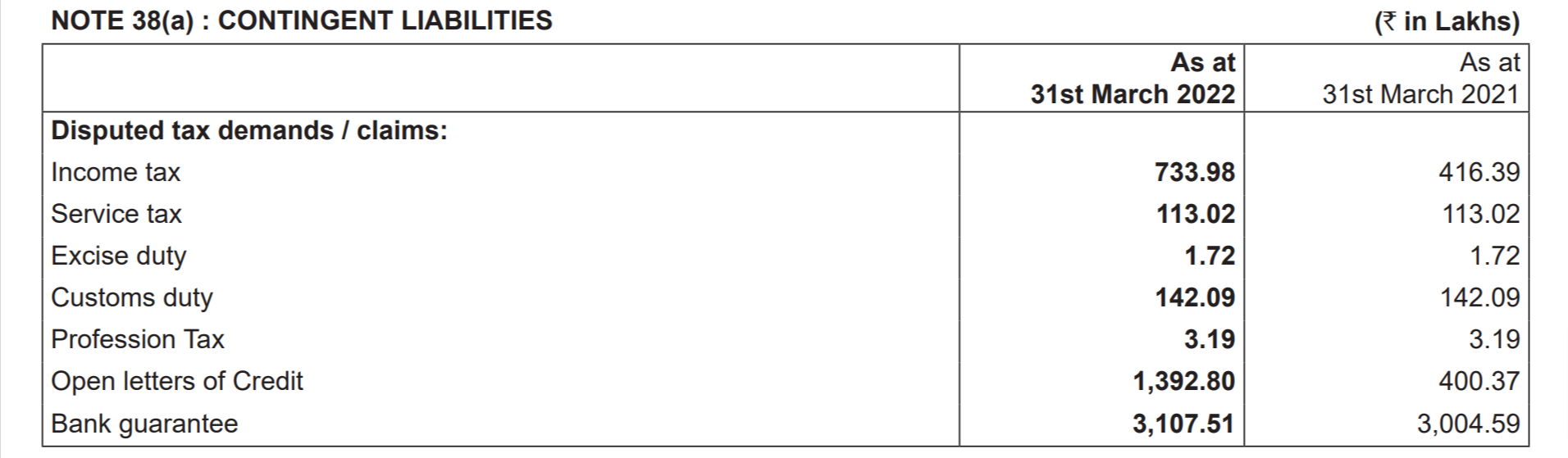

- Consistently high contingent liabilities: The contingent liabilities have been consistently high for the past 6-7 years when looked at as a % of Net worth. Is anyone else concerned about this or has an opinion about this? Bank guarantees and Open letters of Credit constitute ~80% of the FY’22 contingent liability of 54 Cr. Is this normal in this line of business? Are the peers too susceptible to these costs as well?

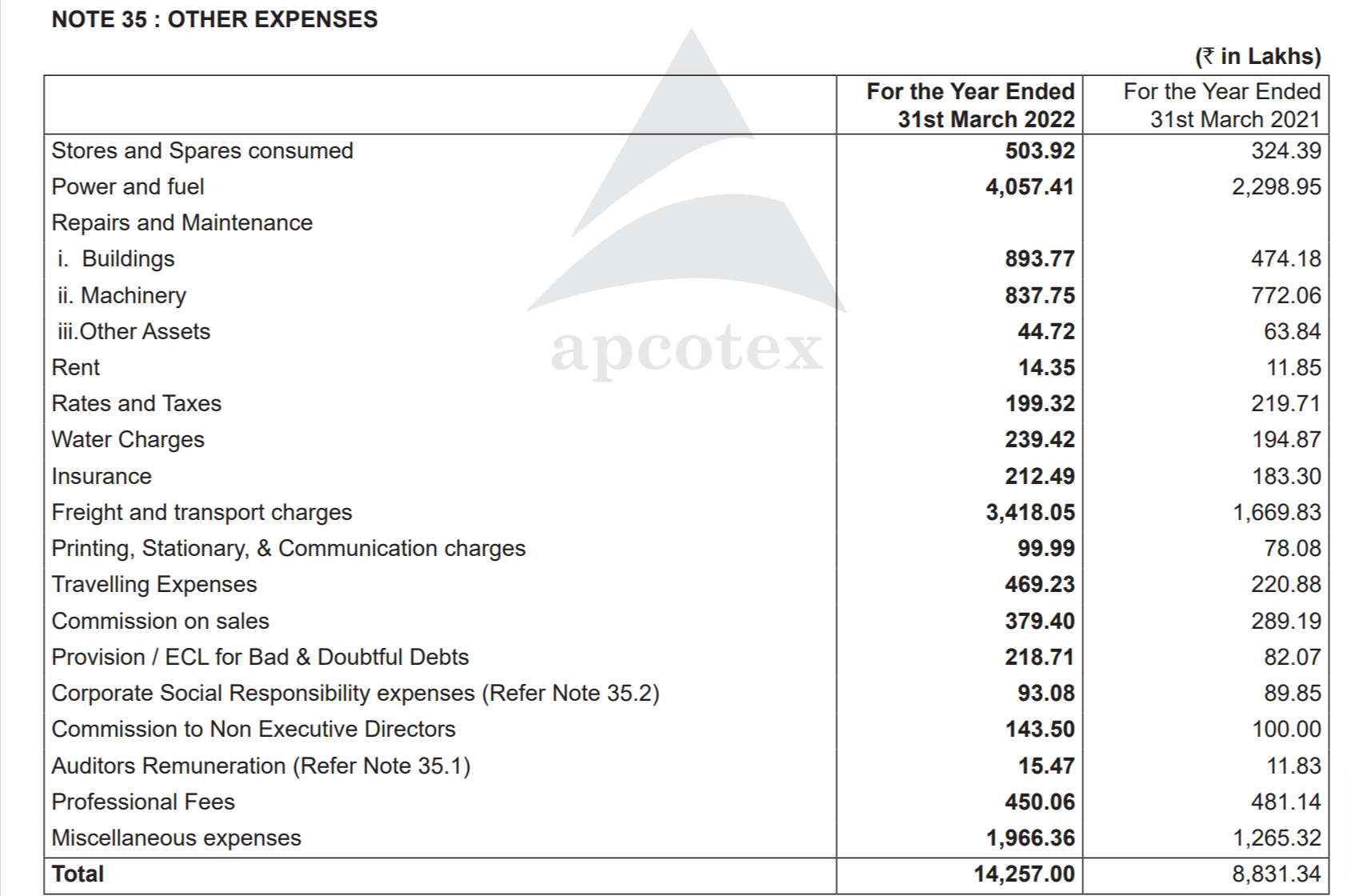

- Increase in Other Expenses YoY : There has been a 54Cr increase in the Other expenses from 88 Cr in FY 21 to 142 Cr in FY’22. Doing a Pareto of the same suggests that the majority of it comes from increasing in Power and fuel by 18 Cr (is it due to a predominantly increase in Crude oil prices?), an 18 Cr increase in Freight and transport charges (is it mainly due to supply chain constraints) and a 7 Cr increase in Miscellaneous expenses (I am unable to find a reason for this increase). Any perspective on this?

Thanks in advance for the help!

3 Likes

Hi, I am a newbie as well and tracking the company. My assumption would be the rise in expenses in power and fuel maybe due to a rise in operational capacity as well. Could you please check if there has been a significant spike in expenses as a % of sales, that might give a clearer picture

1 Like

Thanks, Akashdeep. You are right about the Expenses moving in the same proportion as Sales. I missed seeing it ![]()

Any idea the reason why Contingent liabilities are so high as a % of Net Worth?