Apcotex Industries is a small cap with a mcap of 750 cr. They are mainly involved in the manufacture of performance emulsion polymers which are mainly used in the automotive industry(v-belts, conveyor belts, hoses) ,the footwear industry ,and in gloves etc . The balance sheet looks healthy. The valuation is a bit rich at the moment with a PE of 32. Looking at the other numbers.

The margins have been improving over the years

Good cash flow

ROE and ROCE of 20 plus

The debt halved in 2016 and now the debt to equity stands at 0.26

The sales though have not grown much in the last 5 years. But that could possibly change after the recent acquisition of Omnova Solutions and now they have a monopoly position in Synthetic Rubber . I think they are the only manufacturer of Nitrile Latex in India.

Now looking at the future of Synthetic rubber in India. Though India is the 4th largest producer of natural rubber , India is still deficient in Synthetic rubber production.

Synthetic rubber has a few advantages over natural rubber other than being cheaper.It has greater resistance to abrasion, wear and water, better wet grip,more resistant to oil, certain chemicals and oxygen ,resilience over a wider temperature range and better ageing.

Synthetic rubber Opportunity in India

-2.5 billion square meters of roads will have to be paved, 20 times the capacity added in the past decade -per capital income increasing and thus more demand for auto mobiles

-Growing auto mobile and Tyre industry

The Tyre industry in India has strong domestic manufacturing capabilities and with the fluctuating natural rubber prices , the usage of synthetic rubber is increasing.

Currently India relies heavily on import of Synthetic rubber. So companies like Apcotex industries stand to benefit.

The promoter is the Choksey family. Atul Champaklal Choksey was earlier also a promoter of Asian Paints i think.

Top public shareholders include Vijay Kedia

I have been looking into investing in Apcotex due to the management pedigree and the niche business.

But, performance in the past 1 year has been lackluster. It’s not just this quarter or the one before that - the worrying trend is long standing it seems. Your views @kk82 ?

Revenue was down around 24 % in 2016 compared to 2015. The reason given by the management was higher imports into India because of the lower Petrochemical prices in Europe…

Quoting from AR "The major reason for reduction in Revenue is due to of adjustment of lower prices of oil and oil derivatives. Volumes were also affected due to lower petrochemical prices in Europe leading to lower exports and higher imports into India from Europe."

Also according to the management after the acquisition of Omnova, they expect 2016-17 to be a much better year. Have to see how this pans out in the next few quarters…

Loss in revenues due to lower sales to Paper & Paper board customer affected sales while margins were affected by

higher Butadiene prices

Consolidated net sales for the company for Sep’16 quarter stood at around Rs 67.84 crore, down by 36% on YoY basis with Ebidta at Rs 4.62 crore as compared to Ebidta of Rs 9.5 crore for Sep’15 quarter.

Around 50% of total sales come from synthetic rubber and roughly around the remaining 50% from latex rubber. Key sectors which are users for company’s products include Paper and Paper boards, construction, carpets, tyres, leather, speciality chemicals etc.

On sales side, one of the major customer of the company in Paper and Paper Boards segment did not operate its plant in Sep’16 quarter and thus, Paper and Paper Boards segment which account for around 33% of company’s total sales, got severely affected in Sep’16 quarter.

Further, Butadiene, one of the major raw materials for the company saw a steep price increase in Sep’16 quarter in international market which was unexpected. It was due to a sudden shut down in supply in global market due to an emergency plant shut down by the supplier. The rise was so sharp and sudden that the company was not able to pass it on in very short term. All these, lead to lower Ebidta margin for Sep’16 quarter.

Further, the high styrene rubber (HSR) plant at Taloja continued to remain shut down for repairs and maintenance activities during the entire Sep’16 quarter and the manufacturing activity of HSR was shifted to Apoctex Solutions (AS) (erstwhile Omnova Solutions) in Valia plant.

*** Management expects some volume pick up from Paper and Paper Board segment to start from Dec’16 onwards on QoQ basis and then gradually things will get better by end of FY’17.**

The company was able to increase its market share in Tyre segment. 75% of total revenues still come from India while remaining from international market. Middle East and South East Asia constitute around 75% of total exports for the company while rest from markets like US, EU and Australia.

The company has a gross debt of around Rs 32 crore and net debt of around Rs 7 crore.

The scheme of amalgamation between 100% subsidiary Apcotex solutions India pvt ltd (AS) and Apcotex industries was approved by the high court and date of merger will be effective from 1st April’16.

Management expects the things to improve gradually on QoQ basis going forward.

The company was able to turnaround the business of AS in just 4 months from the date of acquisition.

There is a continuous effort on increase in market share of AS products, increase in reach, betterment of quality, increase in sale of value added products, rationalization of costs, reduction of working capital etc.

Going forward, for Apcotex Industries, there is a good potential in exports markets, while domestic market was more or less at steady state. For AS, there is a tremendous scope to increase the market share in domestic market and also in exports.

Yes, I have been invested in Apcotex from lower levels. Last couple of quarters have been tepid and business environment has been challenging for the company due to both internal as well as external factors. However, I feel the medium/long term attractiveness of the business is because of its presence in niche where entry barriers are high. This in turn allows it to operate in virtual monopoly/duopoly in most of its segments in domestic market. Management has scaled up this business efficiently over last many years and has been expanding its size of opportunity through introduction of new products. So management has demonstrated its competence over reasonably long period.

At the same time, valuation mismatch that existed at 200 odd levels, has been largely bridged and my hunch is that market seems to have built in expectation of turnaround of Omnova acquisition in price. So the key monitor able in the story remains the margin improvement trajectory of Omnova’s business (which will become difficult to track post amalgamation). If they are able to grow the business on consolidated level at decent rate (10-15%) while improving Omnova’s margin to 12-14% as per management plan, there seems decent value on the table even from current price.

Another factor to watch out for how new management handles the dumping from Malaysian/Korean players which has led to significant market share erosion for erstwhile Omnova in nitrile rubber business.

Disl: Invested from lower levels with decent allocation in portfolio.

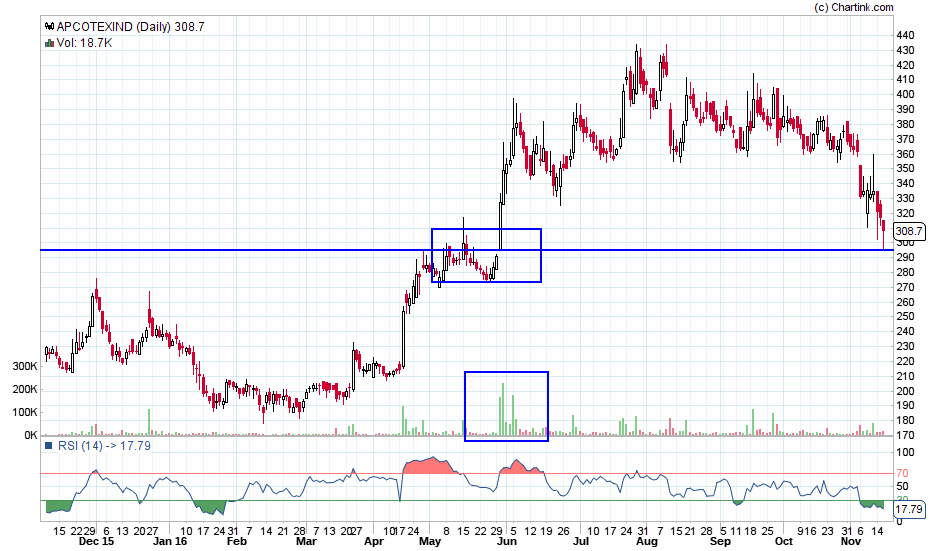

This is a good stock to add on corrections. Over valued at the moment. Dont know if it will ever reach there but the trendline at around 240 would be a good place to add/buy.

While the Chinese government has come down harshly the polluting

chemicals industry, it is keen to provide adequate facilities for complex

chemistry R&D. Within this, its focus is towards segments that can achieve

global scale, but not on segments that require more customisation.

• Focus areas for China include – organosilicon, organic fluorine compounds

(not refrigerants), engineering plastics, thermoplastic elastomers,

composite materials, polyurethane, synthetic rubber (isoprene rubber),

high‐performance carbon fibre, membranes for water treatment, coal

chemicals including downstream derivatives, water‐treatment chemicals

and solutions, and electronic chemicals.

I know that Apcotex produces Styrene rubber & Nitrile Rubber, not Isoprene Rubber.

The production process itself is not overly complex; the polymerization,

monomer recovery, and coagulation processes require some additives and

equipment, but they are typical of the production of most rubbers. The necessary apparatus is simple and easy to obtain. For these reasons, the

substance is widely produced in poorer countries where labor is

relatively cheap. Among the highest producers of NBR are mainland China

and Taiwan.

If I’m not wrong, most of the Nitrile Rubber used in India is imported. The aim of the Omnova acquisition was to achieve Import Substitution for Nitrile Rubber. By Apcotex’s own admission (at the conference mentioned above), the Synthetic rubber’s growth will be flat while Nitrile Rubber is expected to grow 10-15% in the medium term. Will Apcotex be able to get decent margins for Nitrile Rubber?

Also, one of their major clients for Paper & Paper Board Coating - BILT is neither willing to sell its plants nor reopen them.

BATA isn’t one of their clients for High styrene butadiene rubber. Any idea who BATA buys HSB rubber from?

Kerala produces 92% of India’s natural rubber and is devastated by floods. Does it have any +ve or -ve impact on Apcotex that produces synthetic rubber?