Antony Waste Handling bags contract worth approximately Rs 80 cr from Pimpri Chinchwad Municipal Corporation (PCMC) for 7 years

6 Likes

Q3 updates.

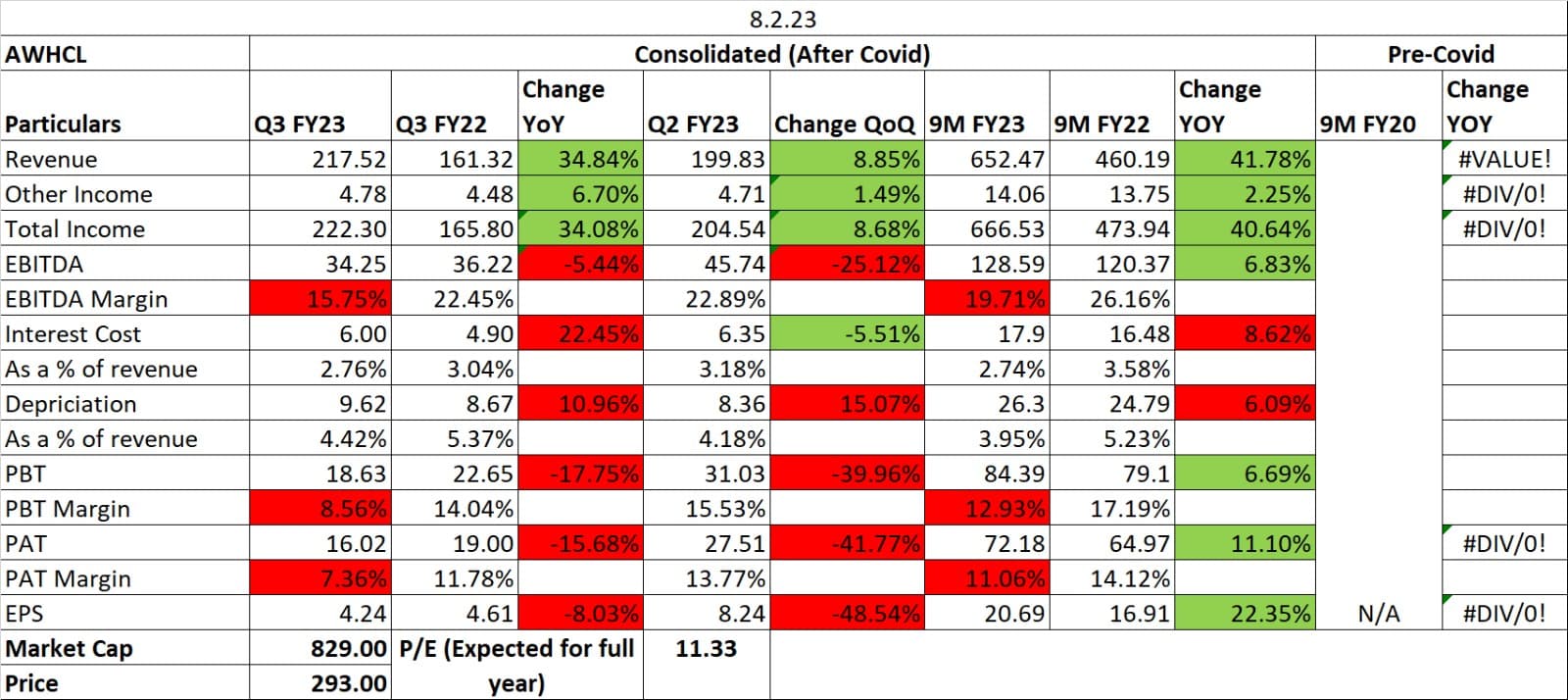

- In its C&T business for Q3 FY23 the Company managed approximately 0.40 million tons (almost flat on a YoY basis), while Waste Processing handled about 0.64 million tons, an increase of 7% YoY.

- The total sale of compost were down at 1,716 tons vs. 3,144 tons in the same quarter of previous year

- The quarter witnessed record sales of Refuse Derived Fuel (“RDF”) which stood at 15,337 tons.

- Total Operating Revenue (tipping revenue from C&T, Waste Processing and Mechanical Power Sweeping) for Q3FY23 has improved by approximately 7% YoY (including various escalations and revenues from fixed shifts/trips/household fees).

https://www.bseindia.com/xml-data/corpfiling/AttachLive/a4e7a7f7-354d-45af-ae71-d03574bcf0e4.pdf

3 Likes

I collated the tonnage numbers from all the business updates co. provided and found that for the past 6 qtrs C&T volumes are flat at avg 0.4 mn tons and MSW processing tonnage is avg .61 mn tons. This means there is no increase in the existing projects in terms of tonnage handled. I felt that due to increased economic activity in the past 18 months atleast the C&T volumes should have been on an uptrend. Also compost sales (though revenue could be insignificant relatively) have fallen significantly this quarter.

8 Likes

They announced receipt of another contract for INR 1024 Crores from BMC yesterday

3 Likes

| - | They use a cluster based approach. Privatization of MSW management industry is a very huge potential to tap into. |

|---|---|

| - | Continue to focus on bidding projects in new states in clusters to increase profitability and efficiency. |

| - | Experience, credentials & financial strength makes us eligible to bid for most projects in MSW sector. |

| - | EBITDA reduced due to higher provisions. |

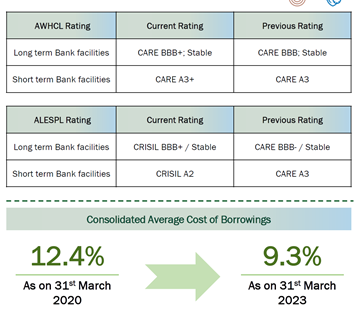

| - | Cost of borrowings reduced from 12.4% in March, 2020 to 9.7% in Dec, 2022. |

| - | C&T volumes have remained flattish. There are 16 ongoing projects. The Nashik C&T project started operations in Dec, 2022, revenues of which will be recognized from Q4 FY23. |

| - | MSW processing tonnage saw an uptick of 7%. Waste to Energy plant at Pimpri-Chinchwad will start operation in Q1 FY24. |

| - | The company under the guidance of its Board has initiated a process of creating a receivable reserve to reflect the nature of our business, which is aimed at providing comfort to the balance sheet and some cushion thereof. We have initiated disposal by creating a reserve of INR 14.2 crores in the quarter. As we go along, we hope to refine this receivable reserve calculation based on historical track record of managing receivables and adopting a credit default strategy in this limited space. These are expected to be realized in a forthcoming time. |

| - | New segment entered: collection, transportation, processing and disposal of construction and demolition waste in Mumbai City of 600 tons per day. This 20-year construction contract with BMC is worth INR 1,024 crores, that’s little over INR 1,000 crores over the 20-year of commissioning period. This is just the tipping fees. Processing of this waste and then sale of the same will generate more revenue. They are assuming that selling of processed waste will given additional 10% revenue of tipping fees. |

| - | Due to the high calorific value of our RDF, demands have been strong, resulting in record RDF sales of over 15,000 tons during the quarter. This trend is looking up based on the response we’re getting from our clients. |

| - | Vehicle scarppage facility will be announced mostly by end of 2023 and revenue generation will start in FY25. |

| - | They were expecting margins to normalize to 25-26% by Q4 FY23 or Q1FY24. This quarter margins have reduced due to provisions. Let’s see if they can manage the same. |

7 Likes

Analysis report

https://drive.google.com/file/d/1CZFjceumgiXZRAlgjlPgIg6o_JvqAYqG/view?usp=drivesdk

I think it will helpful.

Correct if I made any mistake.

5 Likes

"We would also like to address the key point which underlines this quarter’s performance. As

you are aware, we work with a lot of municipalities and government agencies in over 14

municipalities to provide integrated solid waste management solutions. This sometimes

increases are receivables challenges. The company under the guidance of its Board has initiated

a process of creating a receivable reserve to reflect the nature of our business, which is aimed at

providing comfort to the balance sheet and some cushion thereof. We have initiated disposal by

creating a reserve of INR 14.2 crores in the quarter. As we go along, we hope to refine this

receivable reserve calculation based on historical track record of managing receivables and

adopting a credit default strategy in this limited space. "

Can someone share their views on this? How should we think about this provisioning? Does this mean that they expect a default on the receivables or is this just a safety measure?

3 Likes

In the con call management was asked the same question. They said this is not the area where they expect defaults, but the receivables have been delayed. Looks like this is just to smooth out the lumpy results which management expects in this type of business.

3 Likes

Technically, it is likely that AWHCL has made a third bottom over long term chart. All time lows at 240 levels. It has bounced back twice from this level in the past. Could this be a triple bottom?

Fundamentally, for a sales growth of 20+% cagr, roe of 15+ %, profitable company, the company deserves a valuation greater than single digit PE that it is now.

Waste management Inc and other US companies operating in the same waste mgmt industry are priced at 30x PE valuation. Although the structure of business may not be exactly comparable between US and India , the point I am trying to make here is that AWHCL does have a possibility of getting re-rated in the future.

Any counter and supporting views are welcome.

Disc: Invested at 270 avg price and slowly adding more. 5% of portfolio

10 Likes

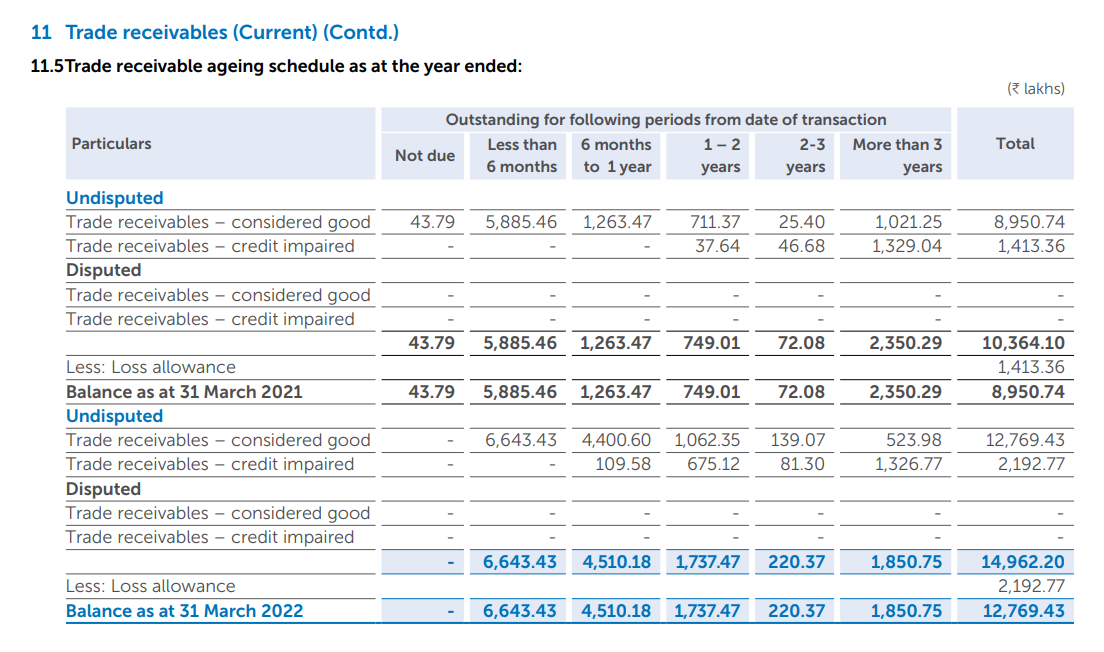

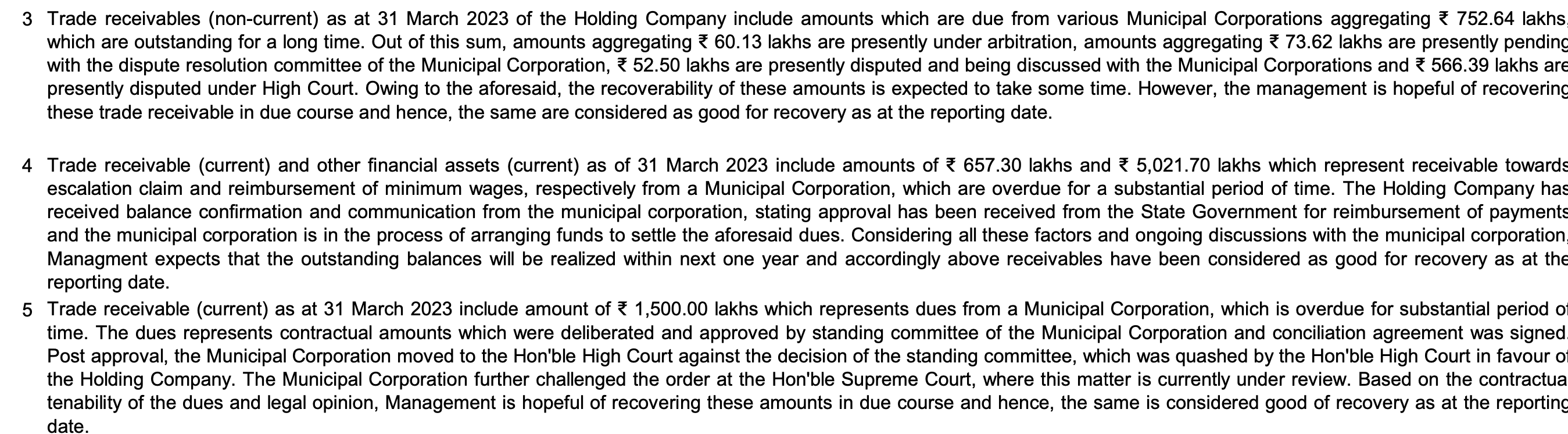

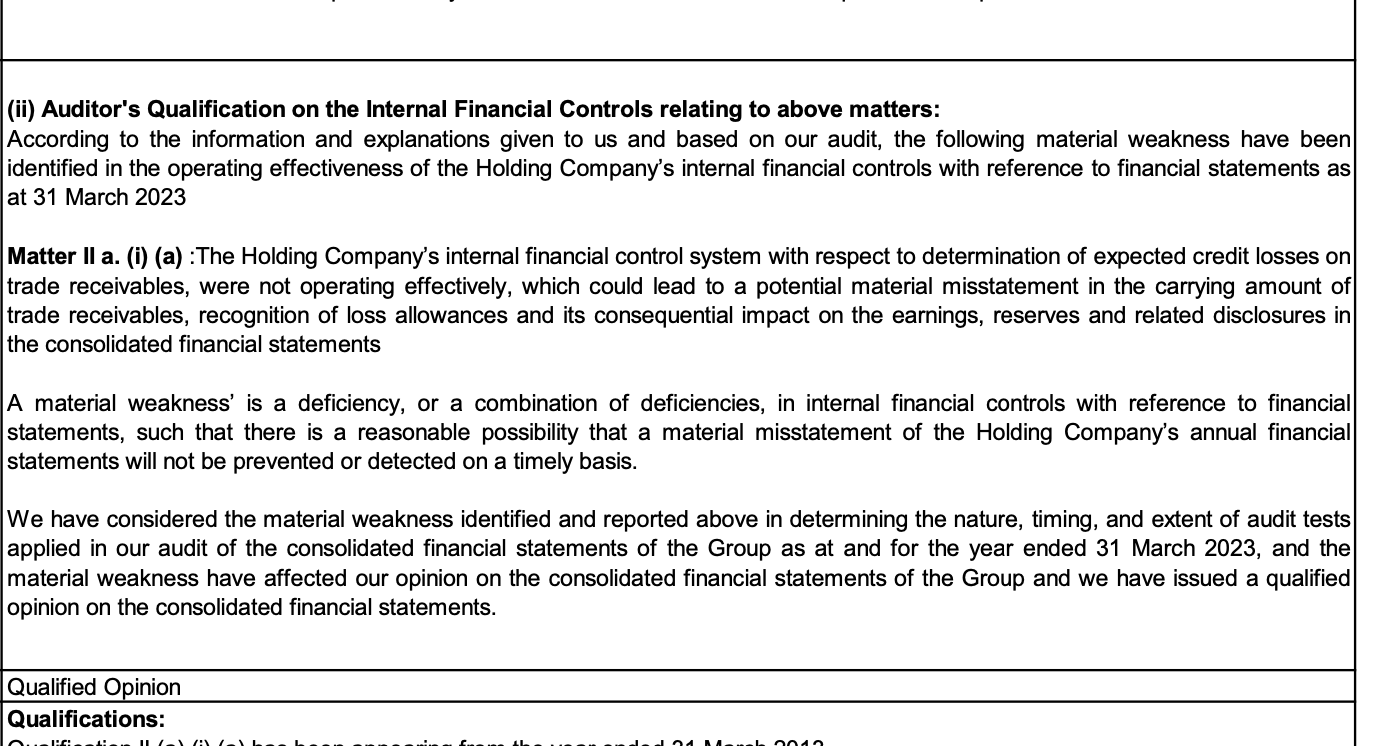

Qualified opinion, recoverability of receivables, age of receivables all point to poor quality of reporting and poor quality of earnings.

4 Likes

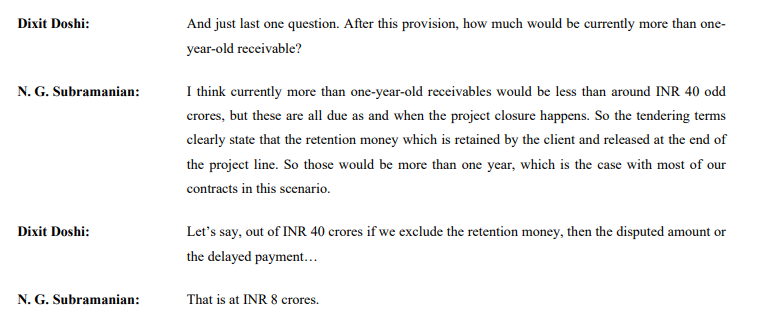

As per management this is how their contract is they will receive this payment only after the project closure. Adjusting for all of this there is INR 8cr of receivables which is dew for more than a year.

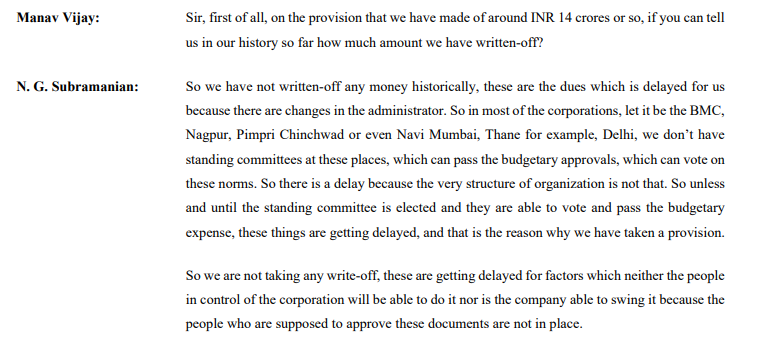

As per management historically they have never written off receivables. What I understand is there is always going to be delay in payment when your are dealing with government. This is the case in each and every industry what we have to see is weather there will be write off or not.

Please Note: I am still in the process of understanding this industry and above is just a copy paste form concall . I am going through their DHRP, 2 AR, All quarterly report ( 10 ), credit rating report and few industry report.

For concall what I understand is they don’t have a linear growth in revenue but have a step up or a lump sum growth so they are confident of 20% to 25% over 4yrs to 5yrs.

Their way of dealing with government looks same as how krsnaa and currently looks like it is at good valuation. Will be coming with a detailed report here.

Disclosure - No investment

9 Likes

Looking forward to your notes and I will be happy to be corrected

I was briefly invested in the company in 2021. I was also impressed by the business prospects. but exited in late 2021 as I was not convinced by some factors associated with the business.

- I believe there is huge competition from unorganised players and unlisted player.

- There is a lot of political involvement in awarding of contracts. There are issues or delay in payment when the political party in power at the municipality changes.

- Why has the EBITDA margins gone down since 2021? I think it has to do with provisions. These provisions started showing in P & L since Elliot capital made exit from the company in Sept’21. Was they painting a rosy picture to provide them a complete exit which they couldn’t do at the time of IPO?

- Qualified opinion from Auditors: I think the company proposed receivable reserve concept to combat the qualified opinion at least this FY. I think this is a good step in this direction. Wont this impact P & L?

- Keeping retention money is a regular concept. I don’t think this could be a reason why auditors gave a qualified opinion. Retention money is a significant part of non current receivable. But there is current receivables in addition to this. Look at the age of current receivable and allowance for loss.

- CWIP as of Sept 22 is 50 crores. WTE project was initially envisaged at around 240 crores. So I think the bulk of investment is yet to take place.

Discl: Not invested. I have not gone fully through the AR. I may have some biases. I will try to update more on the trade receivable situation. Let me know if there is any mistakes above. I was spooked by the IT raid as well.

9 Likes

For me 40-50% of balance sheet is doubtful.

170 cr of Intangible Assets—No explanation given in AR

165 cr of Total Receivables – (current and non current)

49.65 cr (Reimbursement receivables from Authorities (other financial assets)

54 cr of contingent liability

Too many doubtful entries

8 Likes

ng-accounting-for-service-concession-arrangement-1-of-3.pdf (47.7 KB)

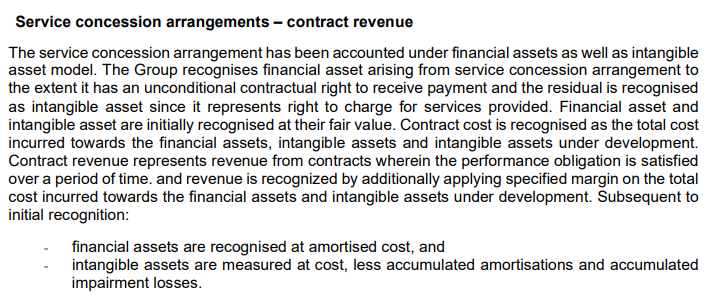

@Saurabh_Varshney Sir though I have not been able to fully understand this but the answer to intangible asset lies in my post. If the answer is not in the post plz wait for few more days I will come with some good findings

If anybody can explain this to me by giving a simple example @diffsoft Sir if you can take out some time and explain me this would be grateful

2 Likes

Thanks @manhar. I missed this. But I did notice some amount mentioned as receivables against these agreements

But did not deep dive. I will try to dig deeper.

1 Like

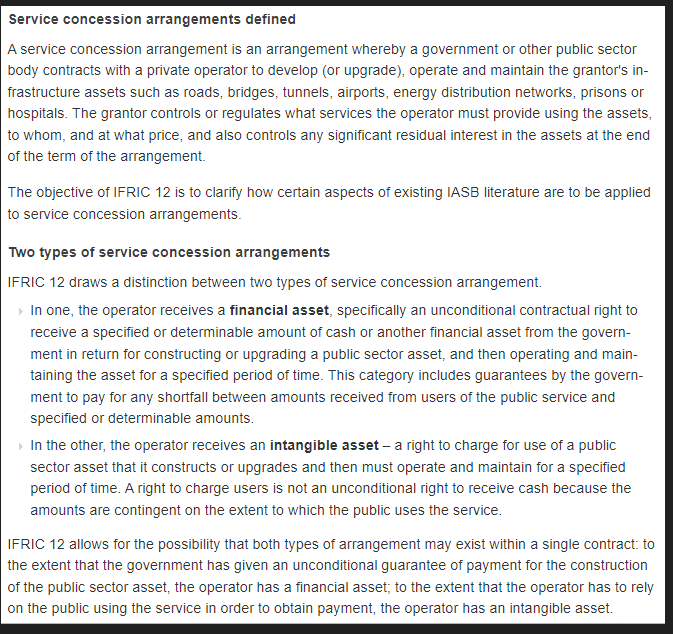

Companies like Antony Waste Handling Cell Ltd. have very special types of commercial arrangements with some Govt / quasi-Govt entity. Anything Govt / quasi-Govt dampens my interest to learn more since it truly cannot be a fair arrangement (atleast in India).

The essential substance of these arrangement is that the Govt wants to build and provide certain services but does not have the capability and to a certain degree, capital; but has a certain kind of monopoly power over services (like giving public utilities) and basic resources like land. Businesses have the capability to build and provide these services but want to seek a fair profit for the risk they undertake. So a public-private partnership is envisaged.

In such partnerships, the transaction runs as follow:

Govt says, “I will give you the authority to build and run this to provide services to my citizens.”.

The business will say, “This will cost Rs xxx at today’s price to build and subsequently operate; and I need to make atleast n% profit”.

The Govt will then say, “OK, I will give you Rs yyy (less than Rs xxx) at today’s price; the rest you can charge from my users as you wish within some guardrails”

Thus the business, which spends Rs xxx at today’s price finds that it can enter into a transaction where it will get Rs yyy at today’s price from the Govt and will recover the rest by charging for usage from its users. The former is a financial transaction (there are no risks other than financial risks) and the latter is a non-financial transaction (meaning there are risks besides financial risks)

Here Rs yyy is treated as a financial asset and balance i.e. Rs yyy - xxx is treated as an intangible asset. This is the substance of accounting these arrangements. Each such arrangement will have nuances and situations relevant to it; and that will be negotiated.

Consequently revenue is recognized for “creation of the financial asset” including embedded interest as if it were a construction contract, till the value of the asset reashes Rs yyy in today’s price. Subsequently revenue is for creating the intangible asset (no embedded interest here) at cost; which is xxx - yyy at today’s price. (Intangible asset under development)

When the ‘build’ is over, the ‘Intangible assets under development’ becomes ‘Intangible assets’.

When the usage of this service starts; then revenue is recognized on usage as per the terms and the Intangible asset gets depleted. If they don’t match over time the Intangile asset is revised.

That’s all. You may read chapter 6 (pages 41 / 42 ) for a concrete example; though I would recommend you read the whole IFRIC 12 document. 1102ifric12guide.pdf (241.0 KB)

For a business the real risk is in demand+price combination that could delay revenues; which inturn puts more pressure because you now have to recover more in nominal terms; and that would in turn affect demand.

Disc: Not invested

18 Likes

Antony Result discloses perils of having Govt as sole customer .

Collapse of margin why because responsible authority is absent …

The problem does not stop there the new chap does not approve what old employee had approved leading to disputes that remain unresolved for ages

The receivables keep on increasing YOY at level equivalent to annual profits … making you doubt if profits are for real … That is what auditors are saying now …

So what should management do // Recognise profits/ sales when money has been received and not what it may receive …

Rest is unbilled receivables …

22 Likes

- Revenue recognition was less due to absence of reimbursements and delayed escalations.

- Strong demand for RDF refuse-derived fuel.

- The company expects employee costs to stabilize over the next 18 to 24 months.

- Outlook remain positive and strong margins are expected.

- Will consider Dividend Payout in the coming AGM.

- Revenue for the waste-to-energy project is expected to be around 60-65 Crores annually, with higher EBITDA than consolidated numbers.

- Other expenses have increased due to a significant spike in transportation expenses related to RDF and hiring costs of vehicles which has reduced margins.

- The escalation claims of 50 Crores and 6.57 Crores are confirmed by municipalities and the state government, and will be paid in instalments.

6 Likes

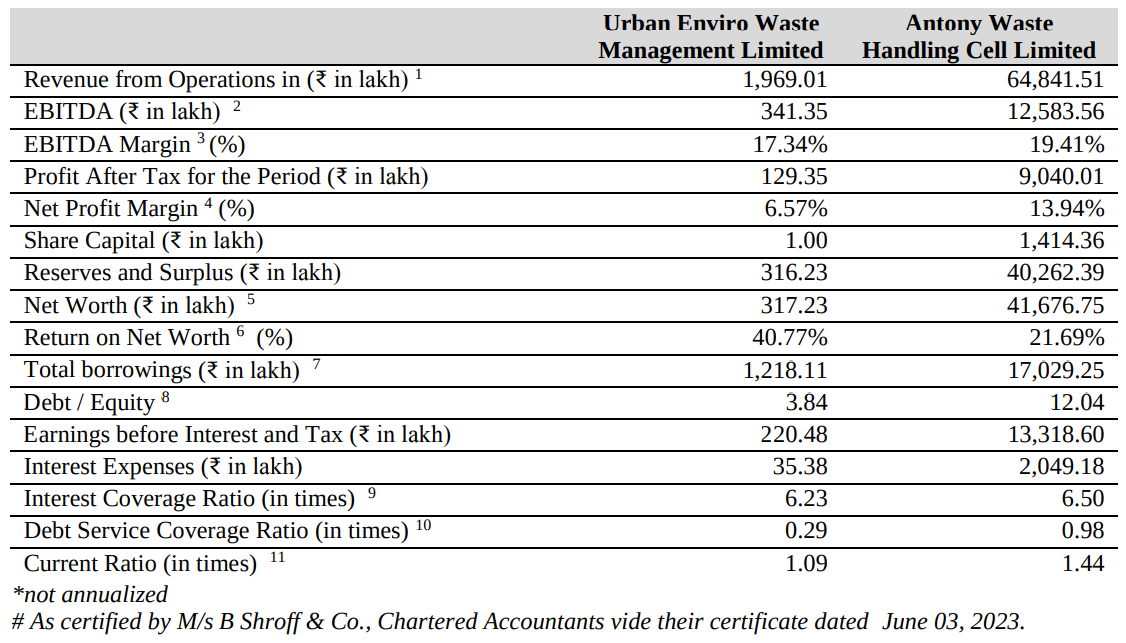

Urban enviro prospectus is released. The IPO is over subscribed by 200x!

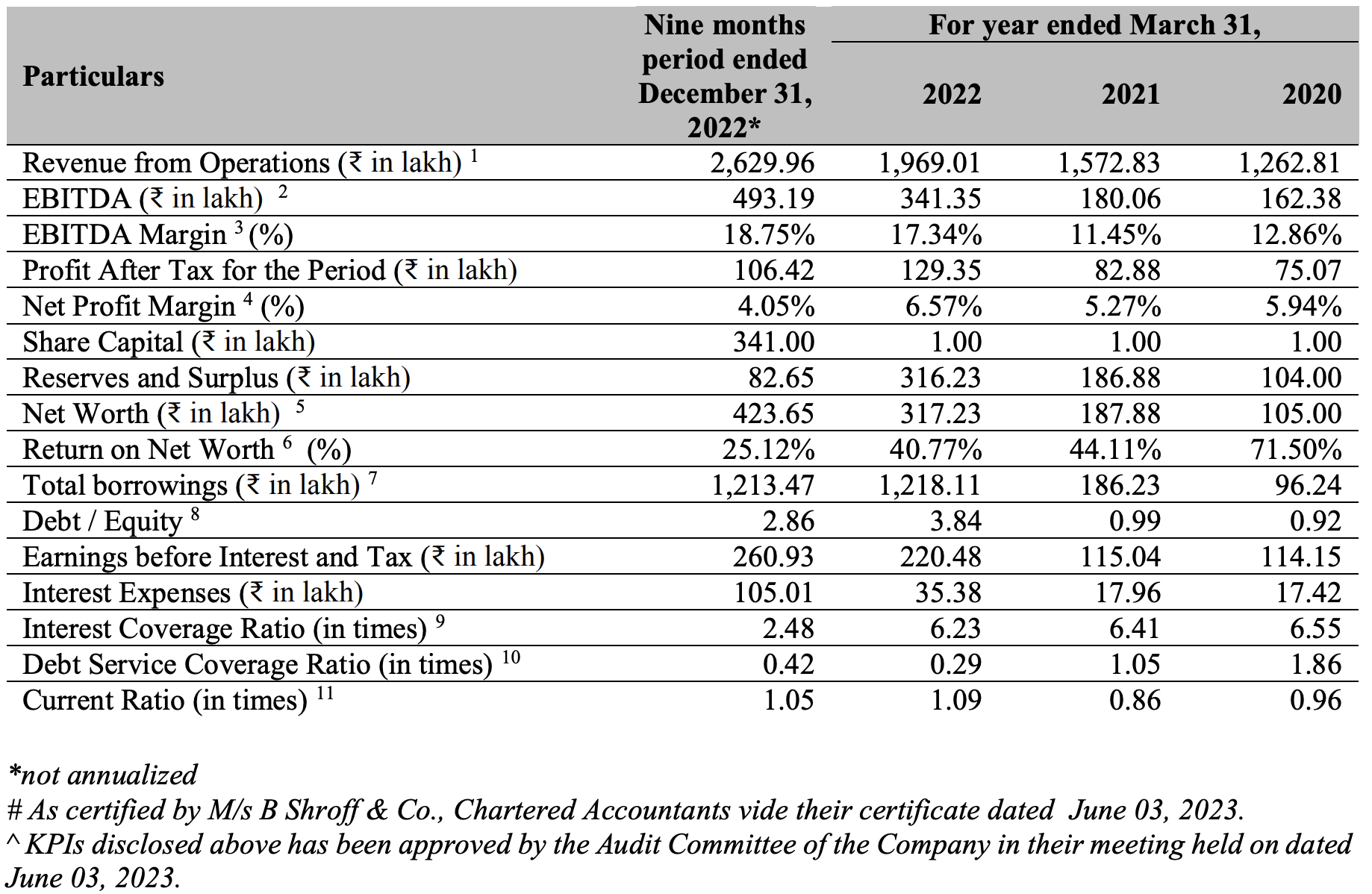

Did a cursory look at the numbers and compared with Antony’s (trendlyne). A few points (as on Dec 2022):

- Their receivables are quite high (473.32 L) which is higher than shareholder equity (423 L)

- Debt to equity is 2.86 (Antony Waste has 0.7)

- Current ratio: 1.05 (Antony 1.3)

- Interest coverage: 2.48 (Antony - 6.3)

- PE Ratio (at issue price of 100): 20+ (Antony - 10.5)

- EBITA margin: 18.75% (Antony - 19.62, note that historically it was 25-30)

They took on large debt in 2021-22. Haven’t dug through on what they deployed the proceeds into.

The prospectus also has a comparison with their peer - Antony. Am a bit confused on Debt to Equity computation on how it is 12x as against 0.7 in trendlyne and screener.in,

Looking at numbers, I see that AWHCL is a better valuation with only risk being the receivables (which is very likely same case in urban enviro). Not sure what else is being priced by the market.

Disc: Have tracking position. Might add more if nothing else holds against Antony.

12 Likes