There are 3 contingent liabilities mentioned in the AR:

The payment of Income Tax which is disputed right now- INR 2.53 crore. This is pretty common in a lot of companies but should be included as per conservatism.

The payment of allowances to workers as per the SC judgment and the changes in the definition of “basic wages”: INR 5.74 crore The change can be accessed at the brief by Deloitte. [Link]

Regarding this, the best resource I could find was this article by Grant Thornton: Link.

It is reagrding the meaning and example of a Capital Commitment: “A company has committed to purchase several items of property, plant and equipment. Individually each purchase is immaterial. However, the total amounts to a material commitment for the company and therefore some disclosure should be made regarding this commitment.”

Now, contingent liabilities as a measure of Net Worth should be < 10%. But in multiple other companies that I saw, there were these purchases mentioned. So, I guess it is pretty common and not a red flag per se. [Please correct me if I am wrong, not having expertise in accountning.]

.

I have recently seen a huge sell off along with reduction on balance volume during a bull market. Will there be any income-tax department tip off to Institutional investors.

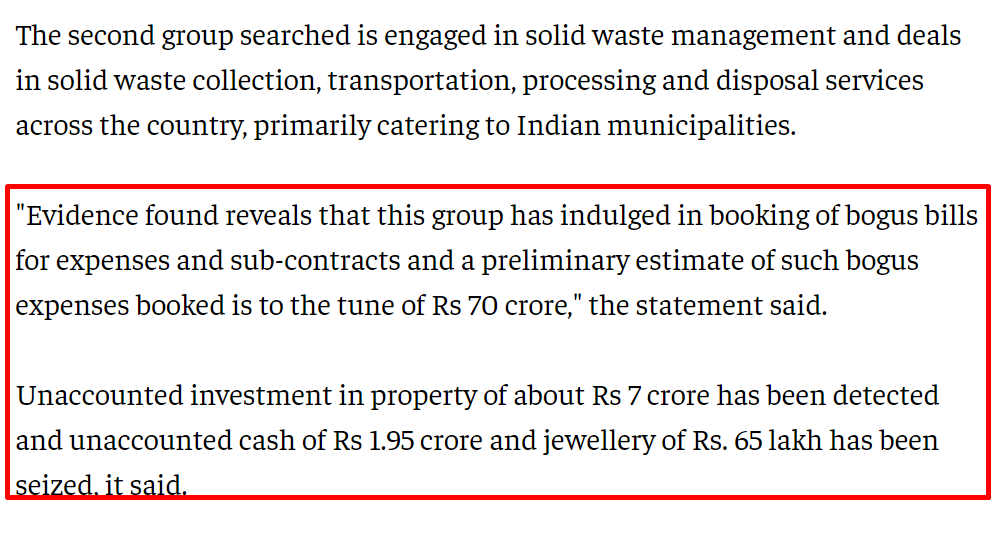

Per 3rd article The I-T department said they found evidence that the group was obtaining accommodation entries using an entry operator.

“The entry operator has admitted to having facilitated the transfer of cash and unaccounted income of the group through hawala operators,” said the officials in a statement.

33% of revenues are from Kanjurmarg project. They refrained from sharing Project by project EBITDA.

PCMC should get 65-70 crores by 2024. IRR : 15-16% which implies on a Capex of 248 crores (grant of 50 crores), lower turn but higher than average margin project.

Just read the Q2 FY22 Concall Transcript. These are some of the big triggers for the company that I noticed:

Their PMC waste to energy project CAPEX will be finished by March 2023 and from then it can generate significant RFO and EBIDTA. Just a rough estimation: their asset turnover on waste processing contracts are around 0.4x, the CAPEX for the project is 120 Cr. , so that would roughly generate a revenue of 48 Cr.

NOTE: This is based on their asset turnover ratio of waste processing contracts, so its actual turnover might be less or more than it. I wasn’t able to find the asset turnover of this contract. If someone has any knowledge in regard to this please share.

One of their major costs is the fuel which is usually 15% of their operating expenses that went up to 18% in the last two quarters. Now, as the fuel prices have been cut this could lead to major savings on their costs. The management also said that the municipalities also take this into consideration when increasing the company’s fees.

I am a relatively new and young investor and thus wasn’t able to understand certain things, if someone has info about this please share.

Can someone please explain what is this difference between PAT(which was 24 cr.) and PAT after minority shareholder interest (which was 18 cr.), as mentioned by the CFO at the opening of the concall?

The management has sufficiently justified how they are not in any way guilty in regard to the income tax raids, and this was the major reason why their share price fell drastically. Why hasn’t it recovered,? Are there any other headwinds that have come up?

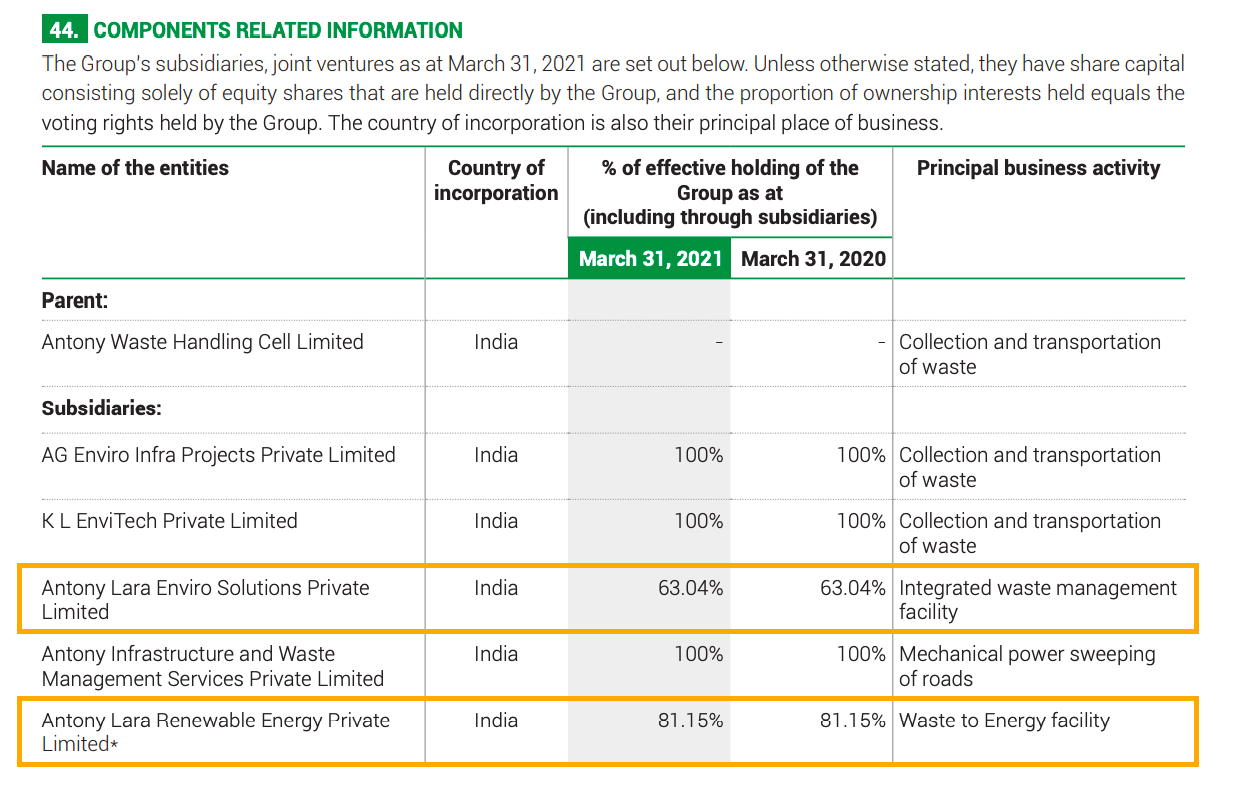

Antony Waste Handling Cell owns 63.04% in Antony Lara Enviro Solutions Private Ltd and 81.15% in Antony Lara Renewable Energy Private Ltd. I think when accounting, the total profits from the subsidiary is calculated and then the share of profits to other share holders of these subsidiaries is subtracted as minority interest/non-controlling interest. Hence the 23.5Cr. in total PAT - 5.5Cr. in minority interest, netting18Cr.

The annual revenue increment resulting from this project would be sizeable with respect to current annual revenues. Two questions we should ask here:

a. Is it safe to assume that this contract would have quarterly price escalation mechanism?

b. User fee collection is a nice optionality over and above the INR ~1000 Cr project revenue. Is there any way to estimate how much this could be? And is this enforced on waste generators or is it optional for them (like a “tip”)

Overall, we can appreciate that the management is being forthcoming about new contracts. Let’s see if this restores the market faith in the business against the backdrop of the income tax raids. Management has already clarified that operations wouldn’t be affected by these proceedings and in the long term, cash generated by the business is all that should matter

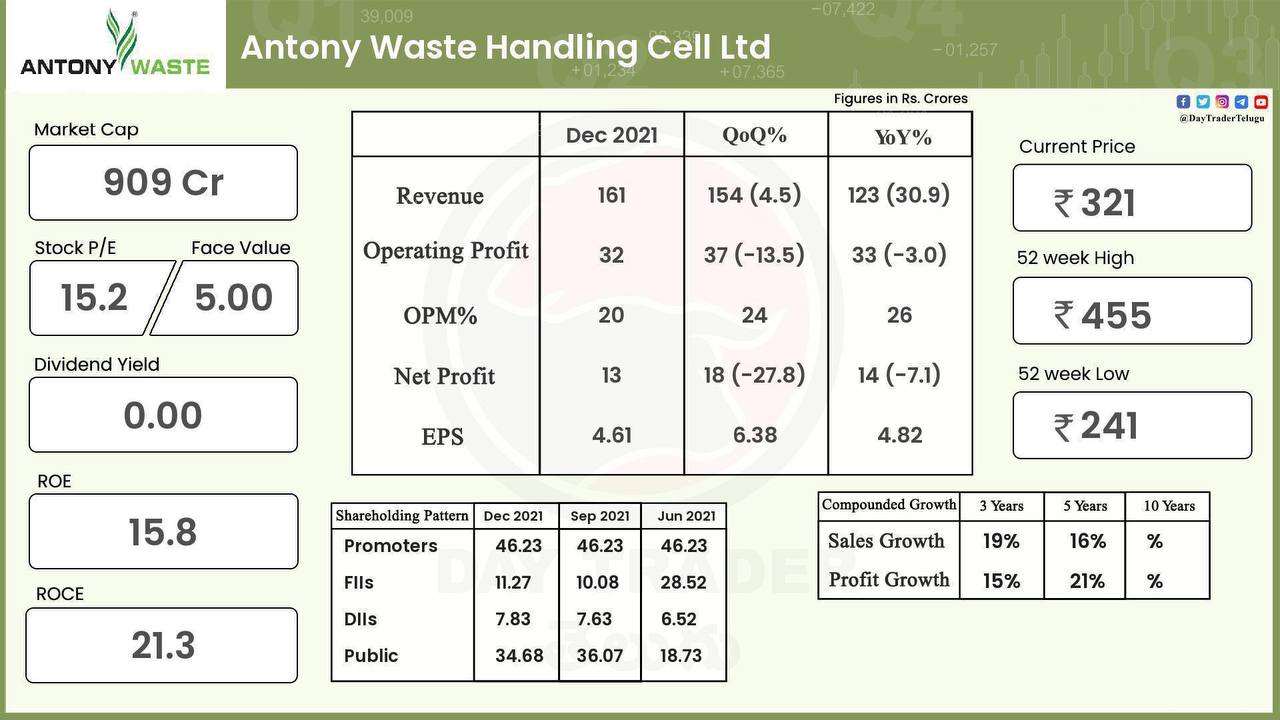

Q3 Business Update - Antony Waste Handling Cell (The company reported growth of 22% in Q3 in operating revenue on YoY and sequential basis is flat. Total tonnage handled by the Collection & Transportation reported around 13% growth YoY and around 3% growth sequentially, while total waste processed by the company during the quarter has improved by around 6% YoY and around 4% sequentially. Total compost sales rose 8.11% to 3,144 tons versus 2,908 tons in Q2)

not a good job with numbers after posting the decent outlook in recent days. employee expenses are way higher this quarter, and this doesn’t contributed to ESOPS or alike procedures, really need to know the reason,and hopefully management clarify this during the Concall…

Employee cost higher due to revision in minimum wage rates, the same will be reimbursed to the company in the forthcoming quarters.

Provisions are on account of our conservative approach towards delay in the reconciliation of billings in User Collection Fee model projects. Provision of approximately Rs. 6.8 crore made during the quarter. Closely working with clients to

help smoothen and speed-up the billing process and enhance its accuracy and ease of verification

seemingly very good result provided company gets provisioned amount and addl amount spent on wage hike…both add together becomes 11.2 corore…

This does explain the fall in the operating margins. It also showcases that the management is quite conservative. However, this also shows the problem in doing contracts with municipal bodies and other government entities. If this keeps happening regularly, then this is not a one-off l, but a regular occurrence. We should keep a watch in this.

Company’s plan :- 1. Study of financial viability

of rewarding authority

Focus on municipal corporations with

strong financials/ credit ratings.

2. Rational bidding after background

research. Focus on contracts with pass-through

escalations for major costs.

3. Targeting specific clusters to

improve efficiency and

profitability

These strategies likely to mitigate the risk, however market is not yet convinced. hence trading at a lower PE, even though assured of consistent future revenues…

You are right that they do have a good strategy of focusing on rich municipalities, and that is one of the reasons why I am invested in it despite the clear problems. However, the problem is that govt. entities even after having massive amounts of liquidities have a tendency to create problems. They will definitely pay, but it can take a lot time.

Just have a look at the case of DMRC and Reliance Infrastructure. The DMRC was a very rich institution before the pandemic, even now it is but relatively less, still they dragged on a clear cut case with Reliance Infra for over 6-8 years. The Supreme court had directed the DMRC to pay Reliance infra a few months but still they haven’t. This is a very big risk. Antony’s business is quite capital intensive. Even if one big payment gets stuck, they could get a big hit on the working capital and debt side. These companies can grow quite fast, but one big roadblock can stop them in their tracks.

That is why we should track whether this is a regular occurrence or just a one off.

I doubt if any municipality would want to stall the payments to Waste Mgmt Companies. If a WMC does NOT collect waste for a week, the city or town will become a garbage dump. No municipality would want that.

I am still tracking Antony Waste and yet to make an investment.

I am not saying that they will not pay it but they can stall it and the WMC might continue with their work. This is what seems to have happened over here.

Rational bidding after background

Rational bidding after background