Can you pls refer me to the exact place where they said to double in fy25 relative to fy24. I am not able to find that. I can only find their statement regarding 50% CAGR over next 4-5 years.

1 Like

Sorry … may be i got confused between financial years or news publishing date … i dont know… but if we calculate with 50% CAGR its 400cr in FY25 100cr per qtr… there Is still a shortfall of 10-11%… hope they will cover up in the upcoming qtrs

It is a company run by humans in a living world full of ever changing dynamics. It is not a robot in a programmed equation.

4 Likes

There was an interaction with Arihant Capital Bharat Connect Conference in April 2024 : https://www.youtube.com/watch?v=FKiEB78ieKA

Check 42:06 timestamp, management mentioned total 550-600 Cr guidance for FY25 , including 70-100 Cr for oil business acquisition which got scrapped. So then the targeted number is 450 Cr -480 cr maybe. Current annualized run rate is already 360 Cr vs 265 Cr in Fy24. H1 results might provide a better idea for FY25 trajectory.

5 Likes

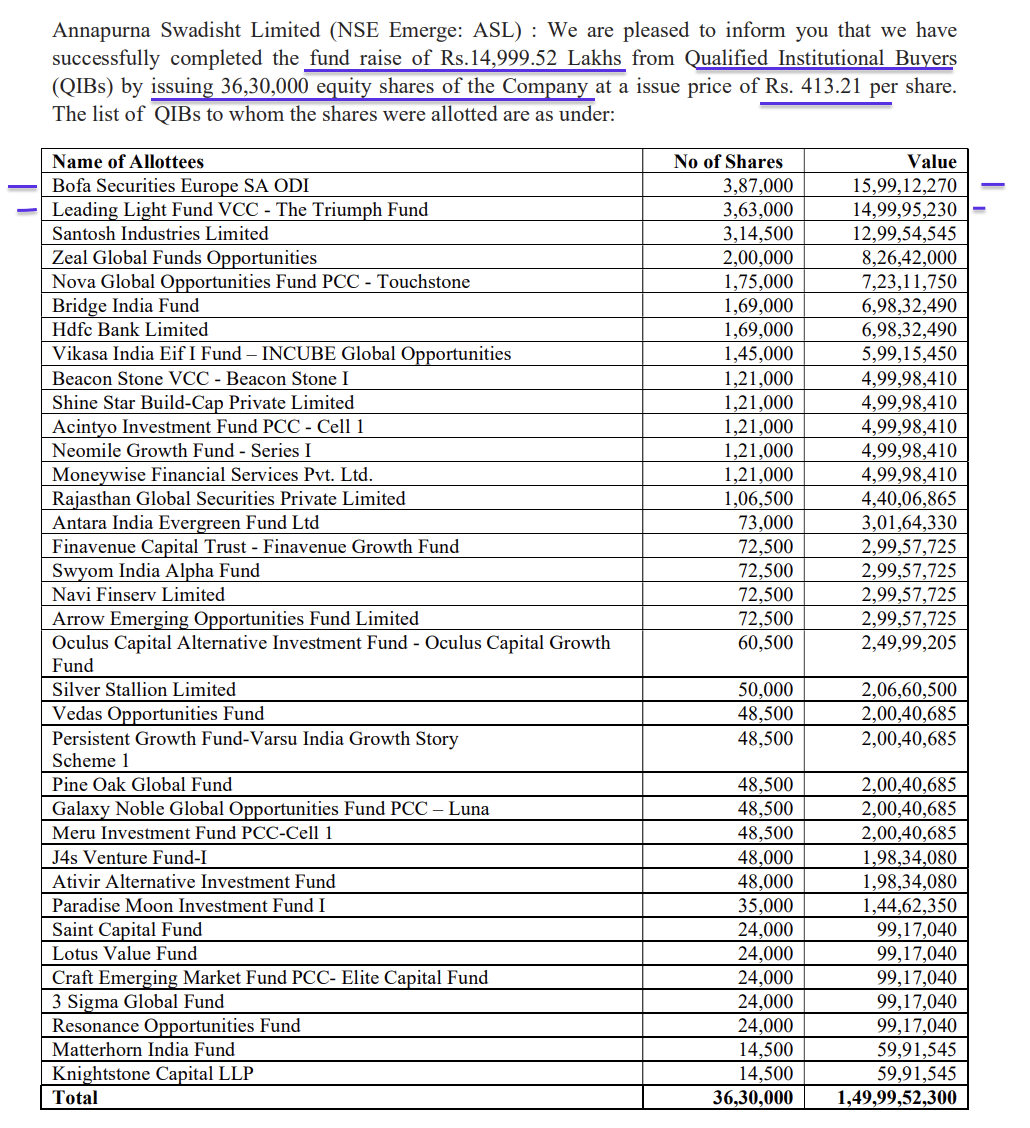

Company announces QIP for 150 Cr, will be interesting to note the incoming investors and use of the QIP proceeds.

https://nsearchives.nseindia.com/corporate/ANNAPURNA_27072024135731_ASL_intimation.pdf

4 Likes

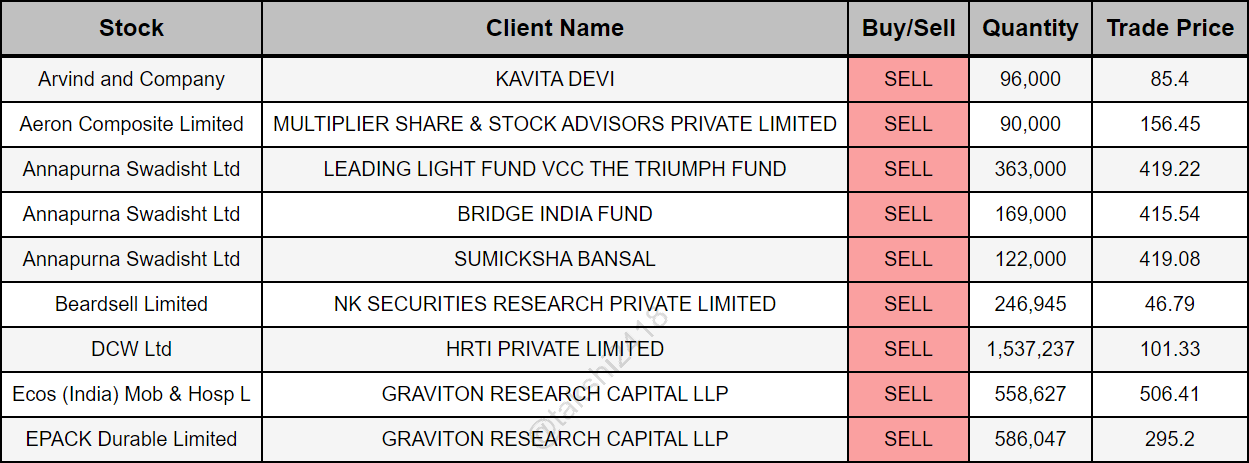

Why some funds have sold their shares immediately after QIP?

Leading light and bridge have sold exact same quantity of shares which are mentioned in QIP details

1 Like

Very interesting post on Twitter by Ashish (InvestorAshishK) on Annapurna

Annapurna Swadisht’s Sweet Deal: How Acquiring Madhur Confectioners Could Triple Their Revenue!

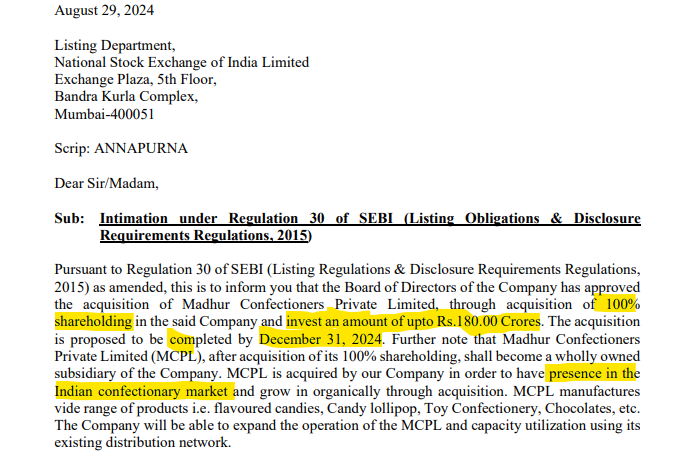

Annapurna Swadisht Ltd. has recently acquired Madhur Confectioners Private Limited (MCPL), a well-known manufacturer in the confectionery sector, for ₹180 crores. MCPL specializes in a diverse range of products including flavored candies, lollipops, and toy chocolates.

Distribution Network Expansion: This acquisition has expanded Annapurna’s distribution network by adding 300 new distributors to its existing 550.

Improved Unit Economics: Annapurna, which previously operated at an EBITDA margin of approximately 11%, will now benefit from MCPL’s higher adjusted EBITDA margin of 17.6%. This improvement in margins at a consolidated level enhances overall profitability.

Cash Flow Advantage: MCPL operates on a model where it secures 90% advance payments from its clients, resulting in negative working capital. This ensures robust cash flow, supported by an average monthly order book of ₹7-10 crore.

Capacity Utilization and Revenue Growth: Currently, MCPL operates at only 30% of its capacity, generating sales of around ₹107 crore in FY24. Annapurna aims to significantly increase this capacity utilization, targeting a revenue peak of approximately ₹400 crore by FY27.

What is the catch?

Annapurna’s management previously missed its revenue target of ₹300 crore by FY24. This suggests a need for cautious optimism regarding future growth projections.

Let’s estimate the growth:

Assuming Annapurna’s current business grows conservatively at 10% annually, its revenue by FY27 would be around ₹350 crores. If MCPL achieves a revenue of ₹300 crores (instead of 400 crores guided by management) by FY27, the consolidated revenue for Annapurna would be approximately ₹650 crores, which is 2.45 times the current revenue.

Important point to note is that acquisition is expected to lower the consolidated PE ratio due to MCPL’s better unit economics, which should further improve with increased capacity utilization.

Also, don’t forget the significant potential for cross-selling between Annapurna’s existing distributors and those newly acquired from MCPL, enhancing market penetration and sales.

My view: Given that there is less downside for PE, and conservatively, sales will become 2.45 times the current revenue, you can calculate the value you want to assign now. I believe that if executed well, management can achieve sales of around ₹900 crores by FY27, which is 3.4 times the current sales.

Shared on Twitter by Ashish

InvestorAshishK

7 Likes

Didn’t Sebi had lock-ins for Preferential shares? I belive 1 year for non-promoters.

Zeal Global , and Leading Light fund might have exited or reduced below 1% as in September holdings data their names are missing

.

Nova Global and Bofa Securities are there.

Hi ,

Greetings .

I am trying to get user feedback for snack products of https://www.annapurnasnacks.in/

I am based in south india and these edible products are currently available in West bengal and some neighbouring states only , we dont have access to try out these products .

Any feedback from folks residing in these states will be helpful , Any star products ???

Note : this is listed company , i dont hold any shares at the moment , only researching at the moment.

Thanks

Akshay

Any comments on September results?.

.looks like business growth has slowed down since last 1 year…

EPS in Sept Quartet grew by 48% relative to last year Sept quarter. The stock is trading at 43 PE. In facts, it fits perfectly as a GARP pick.

No…actually out of 204 cr revenue reported, almost 55 cr belongs to madhur confectionaries…if u deduct that, annapurnas revenue comes to about 155 cr only which is a very moderate growth of 15% YoY…and if we consider management commentary earlier, then this growth looks very sluggish

2 Likes

Hi Bhavnesh

I think the numbers reported are for Annapurna Swadisht only and it does not include the revenue from Madhur Confectionaries.

Please see the below screenshot from the financial results page no. 7:-

The business rather has shown great growth and once the revenue from Madhur Confectionaries starts getting included the growth will be tremendous.

Please correct me if i am wrong.

Thanks

4 Likes

Hi…

You are right…my bad…

Results look great if Madhur numbers are not included…

But any idea why were they not consolidated yet during current results?

1 Like

Please check the filling on the acquisition of Madhur confectioners, the first closing was mentioned for 31st october only. They would be consolidated in H2FY 25 results.

The h1fy25 growth numbers have been great considering q1 was 90 crs and q2 being 110 crs.

1 Like

Annapurna has posted great numbers.

The company can see astronomical* growth in the next 5 years if their execution matches their strategy.

*T&C applied, of course.

2 Likes

That’s the reason of acquiring companies benefits the P&L statement.