Well executed https://nsearchives.nseindia.com/corporate/ANNAPURNA_26112024164019_Intimation_ASL.pdf

My gut feel is Annapurna Swadisht is a bogus company as is Madhur Confectioners (or Srivari Spices at the risk of digressing). Reminds me of Manpasand Beverages tbh. These are some of the reasons:

-

I have not found any offline presence of either Annapurna or Madhur’s products or listing of their products on trade channels.

-

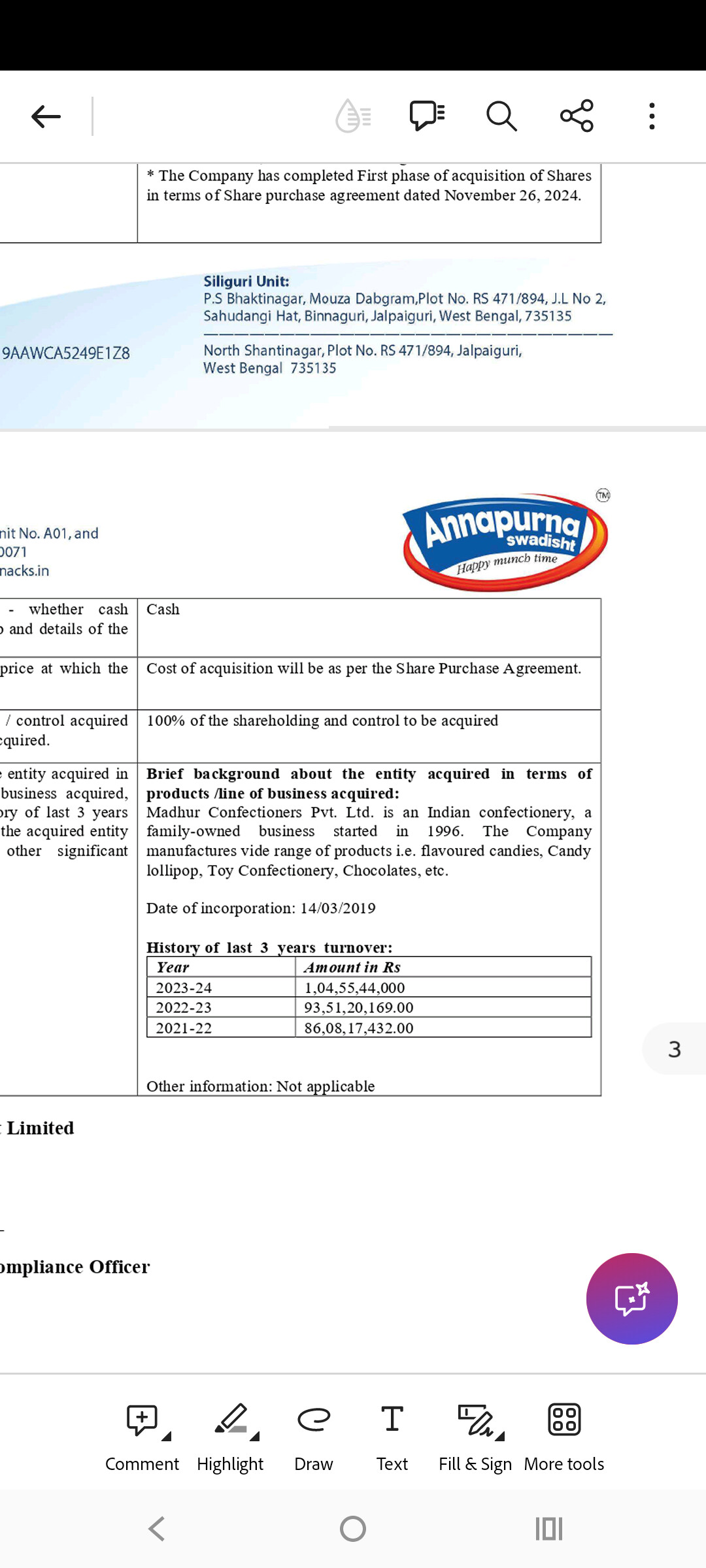

Cash acquisition at 30x PE Multiple is highly suspect. Especially when Madhur had a networth of 9 cr as on FY23 (as per ROC) giving 20X P/B. For context, Annapurna’s fixed assets are 60 cr. Don’t understand any reason why an FMCG company wouldn’t invest in capex and use cash to acquire a 4-year old business at such high multiples except of course to siphon cash.

-

I have seen their factory videos and Google maps photos of their plants and all look like an elaborate staging.

There is zero information available on the Internet in this company regarding its products except for its website. They have even misspelled a product on their website and social media as “Crispy Diet Chidwa” haha. Just to be clear this analysis is based on my limited research. Happy to get insights from someone who has done on ground diligence such as channel checks, factory visits etc.

4 Likes

I asked a friend about this company, but he had never heard of it. My friend works in the FMCG sector (snacks segment) in West Bengal as a sales manager across various markets, such as Kolkata, Durgapur, Siliguri, etc.

1 Like

Do we know if any big HNI has been invested in this company?

I found this online, not sure if we can trust it,

https://www.screener.in/people/679/ajay-upadhyaya/

Ajay Upadhyaya is a HNI investor in the same and recently 1-2 FII also entered. Assuming they have done basic diligence and should know more.

Motilal Oswal was a big investor in Manpasad Beverages and defended it vigorously. I wouldn’t give too much credit to diligence of an HNI investor who would have invested at peak of bull run in hopes of quick buck. The biggest red flag for me is Rs. 180 cr cash acquisition of 4-year old Madhur Confectioners (again a questionable company) which defies all logic and is clear cash siphoning. Even the Promoter’s shareholding has fallen from 51% to 39% in last 2 years. Unless there is contrary feedback from somebody who has confirmed doing on ground diligence, I would classify this company as a sham.

PS: You should check their YouTube channel. It’s hilarious!

9 Likes

I am not defending Annapurna Swadisht. But i dont see an organized campaign to promote this company like it happened in Manpasand. Just an observation.

Also can any Bengali confirm that Chivda is known as Chidwa in Bengali?

3 Likes

Thanks for sharing. @Moonrise

Do you have any idea for the expected asset turns of the current capex of ASL? I remember they had mentioned an asset turn of 8-10 in the Alpha Ideas video. Current Asset base +WIP is nearly 75 Cr, kind of translates to peak revenue potential of 600-750 Cr . This kind of ties up with the presentation shared earlier on Madhur acquisition.

On a consol basis, the current business is nearly at 500 Cr Topline with 63 Ebitda ( 400 Cr Annualised for ASL with 46 Cr ebitda + 100 Cr of Madhur with 17 Cr Ebitda).

ASL was valued at nearly 25X EV/EBITDA before the correction, so this consol business should be nearly 1500 Cr compared to ~800 Cr now.

1 Like

No idea.

I try and not overanalyse.

Keep it simple, just connect the dots, the story, and the potential.

Understand the DNA, the strategy, and watch the steps in execution.

Children & adults will not keep track, or count, of the quantity of chocolates & snacks they consume. No track of quantity, or amount spent either.

North East is a notorious and unstructured market. Capture the flag is accomplished.

Chocolate and snack consumption is a never-ending theme.

2 Likes

Hi Ankit,

I am curious to know the reason why you are saying Madhur is only a 4 year old company when both madhur (in their website ) and Annapurna (in their disclosures ) say it started in 1996.

Madhur’s reported turnover for last fy is 104 cr. Isnt p/b for an fmcg firm a bad metric for valuation?

Please share specific insights if you have about anything else you could find.

Resharing recent disclosure by annapurna for further discussions.

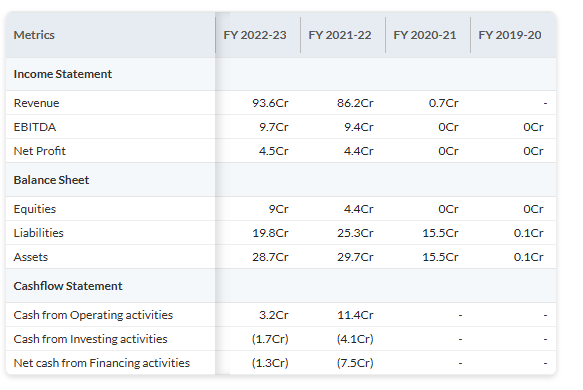

Of course Annapurna will only share numbers that suit the narrative. Please see below snapshot on Madhur Confectioners (Source: Tracxn)

Snapshot of their P&L and BS

For multiples, it’s better to check what companies of same size are trading at. I’m not here to vigorously defend my case but just lay out my observations and it’s upto the readers to make their own conclusions. I was an investor but have exited my positions.

3 Likes

Number of Employees for whom EPF amount is being credited is continously on rise:

For Kolkata establishment:

September-566

Oct-572

Nov- 776

For Durgapur establishment:

September-214

Oct- 215

November-276

Total employees as per EPFO in November- 1052

Payment Details (1).xlsx (16.0 KB)

Payment Details.xlsx (27.7 KB)

4 Likes

The law firm which advised Madhur Confectioners for the acquisition deal has tweeted.

1 Like

It’s called “Chire” in Bangla.

I have seen the products in small shacks and neighborhood shops in Kolkata. Low end price range. Taste wise we have better options available.

That snapshot from tracxn does not prove anything anyway . One may start a business in a small way in 1996 and then change names and grow and later change it again for various reasons. Company registration date need not be same as company incorporation date at all. One may start it as a single sole proprietorship( no registration needed) and then take on a partner and change to partnership or private limited company and then again think of listing someday and change to public limited .

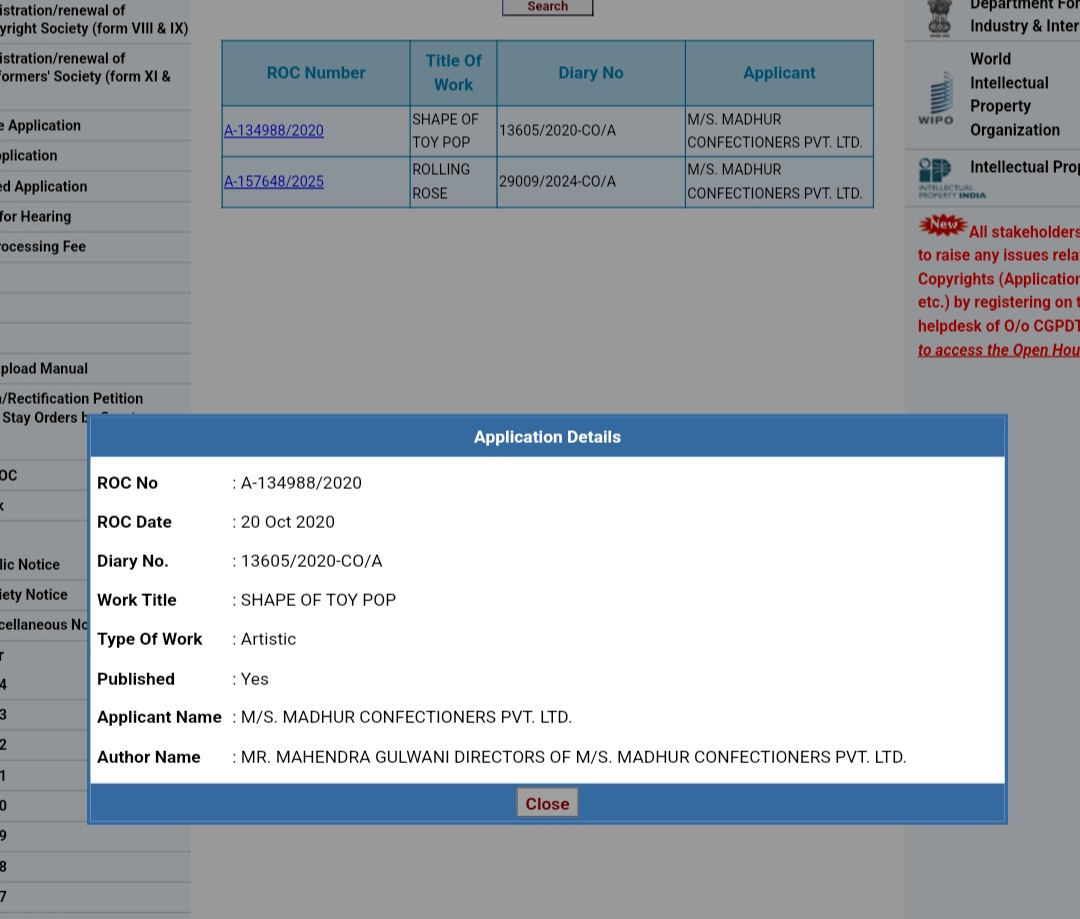

Check this screenshot and check the copyright date …

They must be visionaries to start planning this fraud in 2013 !

I live in kolkata and never saw Annapurna swadisht products before today …however, relatives brought these two today from a place in hooghly district . Nothing special in taste but not very bad either .The strategy seems to be colourful packets and toy freebies to attract kids in rural areas but do not think its something that would make kids ask for a specific packet .

Disc: not invested .

3 Likes

The screenshot of their website doesn’t prove anything lol. They can list the date as 10,000 BC. Have you searched the actual copyright website? Well I have.

2 Likes

Six year old video about Madhur confectioners, guessing the earlier name was Mahendra Industries, but we could all be wrong

1 Like