Great point. Thanks for sharing your perspective.

While Groww is valued at 3 times Angel, per recent updates Angel has 3rd spot ahead of Groww in active clients

This industry is bound to see heavy consolidation in near future and winner takes most will play out( top 3 to keep most mkt share), Angel management has iterated this point earlier as well.

Motilal Oswal’s Ramdev in recent interview was open about Angel transformation from traditional to digital and that traditional players are challenged by new incumbents.

Angel has delivered a successful transformation( easier said than done for a legacy biz), profitable growth, aggression in winning mkt share, seems to be holding ground well in recent correction.

They are aggressive in scaling talent pool ( sizable tech lateral talent hiring per LinkedIn openings)and this will require investments for some time to come in addition to marketing aggression spends.

Fight among top 5 is fierce and next few quarters crucial , market may also stay side ways/moderate growth bringing out some cyclical aspects.

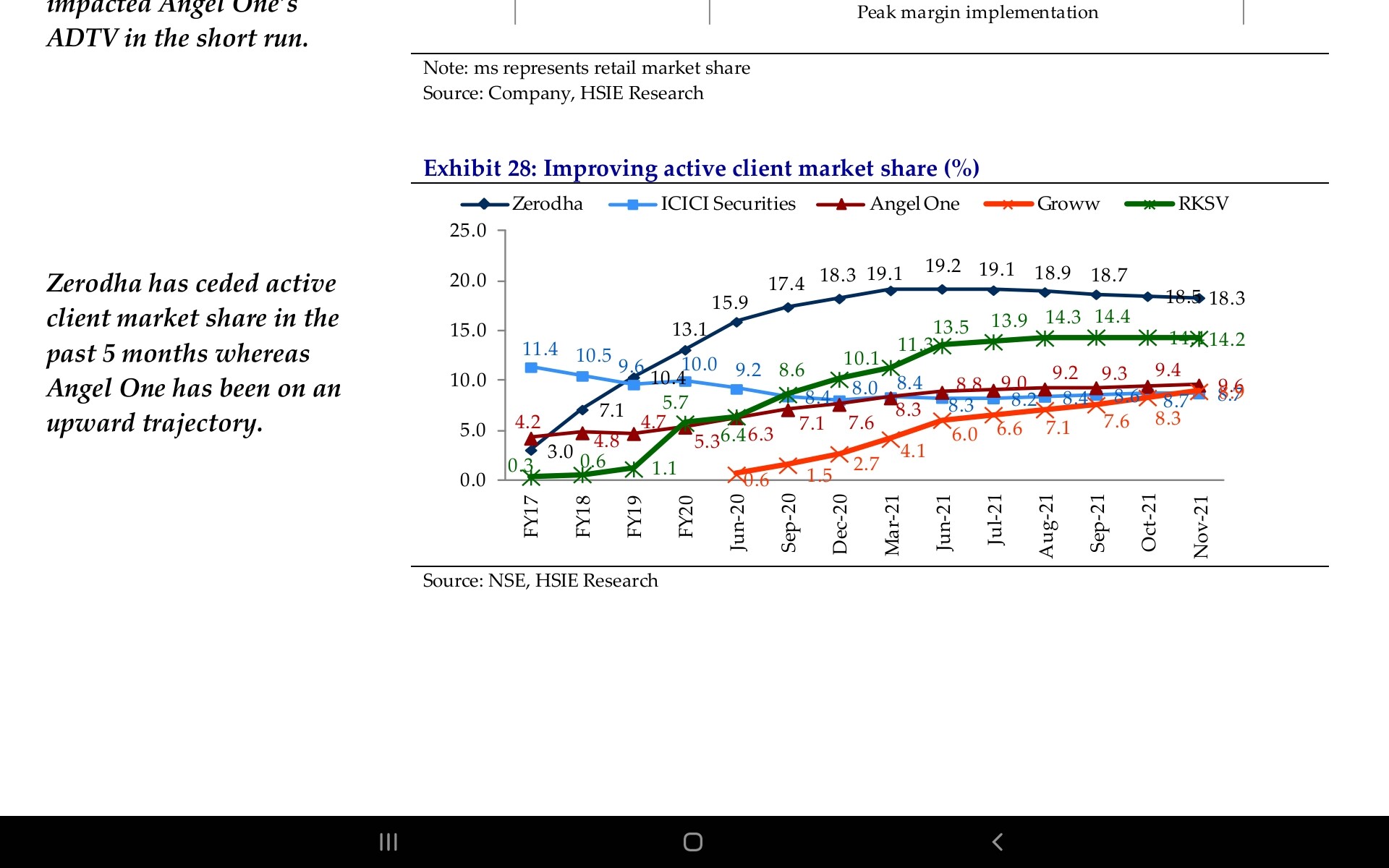

Edit - Very interesting mkt share trend per report shared by babuchit below

Invested

2 Likes

come across a good report on Agel one.

3 Likes

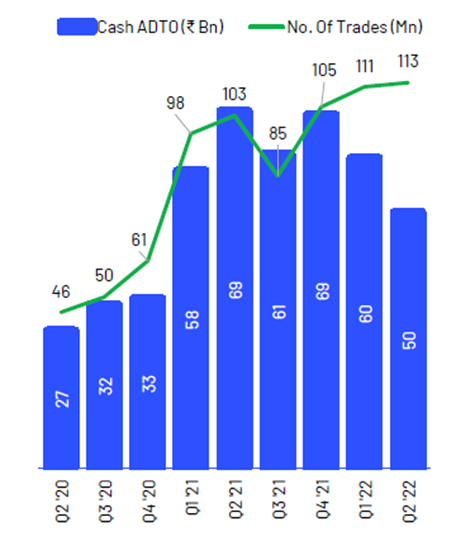

Pardon my ignorance, how does reduction in “average daily turn over”, directly coorelate to increase in business of cash segemt?

As i am a trader in F&O, speaking abt myself, if the peak marign comes down i wont bring cash to the play, i will reduce the number of bets and probably buy hedges which are closer the sold options, there by redcuing my margin requirement. instead of bringing extra cash to the game.

Let me clarify. Because of the peak margin requirements the average daily turnover in the cash segment came down as you can see but the number of trades kept increasing. So, even though the volume of money traded came down the volume of number of trades kept going up.

Now, brokers dont make money in the cash segment, but if this trend plays out in the F&O segment (which drives majority of the revenue) wherein tomorrow when the markets tank the ADTO (average daily turnover) shall also go down but the number of trades (all small in volume) will continue to remain or grow then we are looking at a stable discount broking business.

Traditional full service brokers charge a % commission of the volume of money traded and hence their revenue performance is highly linked to the market cycles. Discount broking business is expected to be more stable.

Ujjawal

Portfolio Manager: Green Portfolio ESG

5 Likes

Ujjwal there could be one more possibility to the above statement the peak margin rule definetly reduced the size of the trade but increased the number of trades, but alternatlievly this could also be due to the new entrants coming into the market.

As you are Portfolio manger probably you know more than i do . this theory can make or break the story of traditional as well as discount brokers.

Doesn’t Angel One publish / avg trades per user? This should be easily verifiable.

They publish cumulative monthly orders everyone in business updates. Vheck bse website.

1 Like

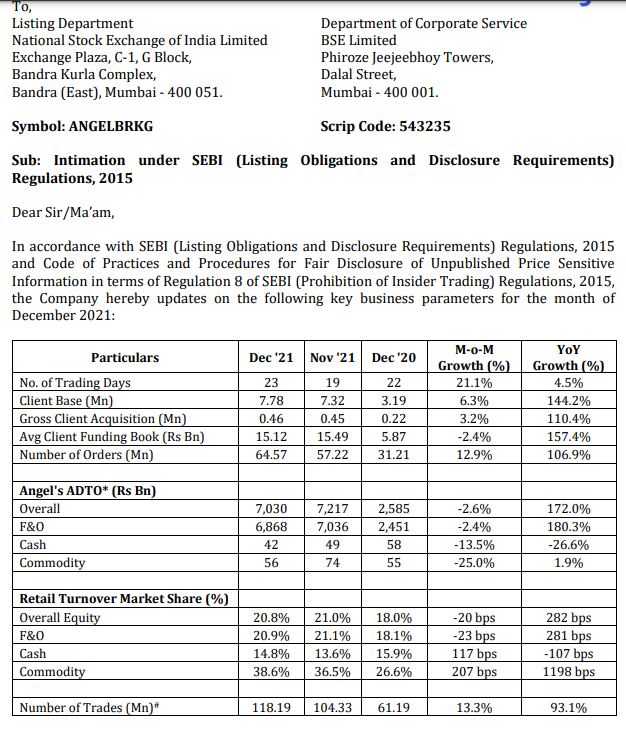

Monthly Business Updates shows very little impact of volatility (drawdown) during December Month. The report Mentions Angel’s strength of having more secular revenue profile and limited impact of any sharp market corrections. December Months updates kind of validates their Point. F&O ADTO are marginally lower compared to November(flattish and not a huge drawdown) and are higher compared to October.

IMHO, Currently Market is rating Angel only for their Broking revenues. Triggers like AMC license, SuperApp etc are lined up which will add optionally PE and contribute for Re-rating. With the kind of highly Qualified and professional team onboard, things are looking very good from the current levels.

Disc. Invested and doubled holdings after seeing Q3 Business updates.

8 Likes

Another one.

Initiating coverage report by Motilal Oswal (09.11.21)

2 Likes

Microsoft CEO Satya Nadella invests in Groww, will be adviser too

2 Likes

Attaching the Q3 results of HDFC securities. HDFC securities, as we know is not very innovative nor agile vs say the likes of Icici Sec or Angel. Still… the results are super good.

Angel is gonna report results on Monday. Fingers Crossed !!!

2 Likes

There is actually no need to cross fingers. Angel has been reporting monthly numbers. We already know they are going to be very good.

To my mind critical question is not about here & now (which is good) but rather the medium term -

- Progress on amc license

- Progress on super app

9 Likes

Great video on comparison of various discount brokers gives some insight into value proposition of angel broking :

8 Likes

Good results

ANGEL ONE Q3 : Cons Net Profit Up 125 % at Rs 164 cr (YOY) , Up 23 % (QOQ)

Revenue Up 95 % at Rs 597 cr (YOY),Up 13 % (QOQ)

Ebitda Up 121 % at Rs 234 cr (YOY),Up 23 % (QOQ)

7Rs Dividend declared

''Our Super-App is in the development phase. As a precursor to that, our fresh iOS and Android app, which is currently in the beta phase, is expected to be launched, over the next few months."

Presentation

efde7759-122b-439d-bb48-93acea736041.pdf (bseindia.com)

9 Likes

On Q3 annualized basis angle,is available at 18 PE - QoQ growth has consistently beaten hands down YoY growth for majority other industries and companies. Has RoE close to 50% and digital based model has clearly demonstrated operating leverage. Not even considering about scarcity premium yet being only listed play in top 5 digital brokers.

Few aspects that everyone talks about and market keeps worrying about

Cyclical aspects of business

-

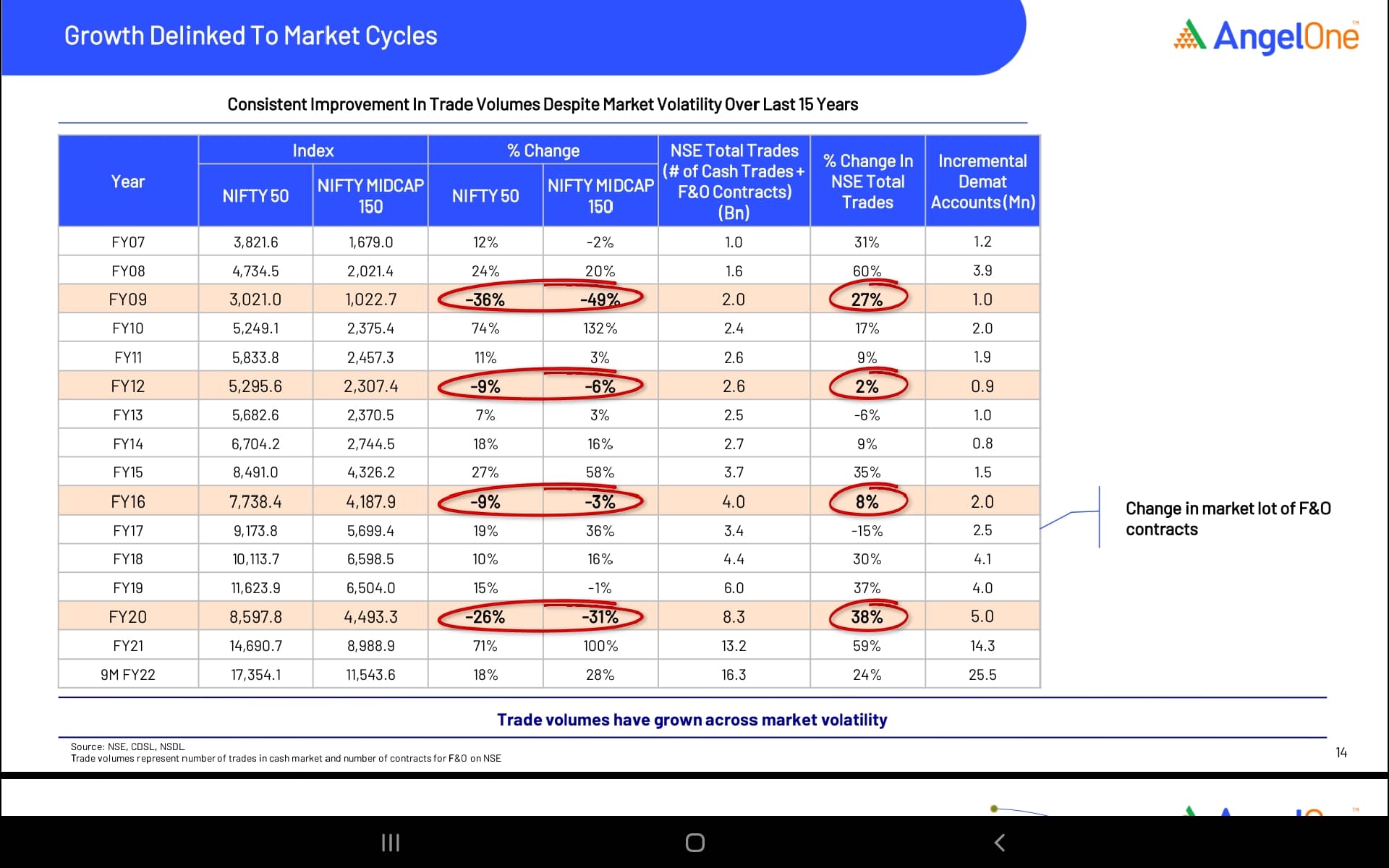

When market goes south Brokers will suffer - is that the case? Data from 2007 onwards at Industry level say it is not the case - would incline to agree with Angel growth being delinked to mkt cycles

-

Another short term view of same aspect on recent rally and in between draw downs- focus being on Angel( order no) - again agree with growth irrespective of Volatility

-

Operating leverage is visible across all periods- Another aspect on product mix is - key operating leverage component is Broking income - if that doesn’t grow - operating leverage doesn’t kick in - observe Q 22 to Q2 22. Funding book has a lower return ratios than core biz hence have to be managed accordingly. Once AMC business comes in, it is even higher EBDITA biz.

-

Competetion - Angel aspires to be No 1 at some point - they have come from 5 to 4 to 3, next two positions are not easy to dethrone as they are ahead in digital curve and Groww seems to be closing in with Angel. Irrespective of position in near term if eyes are on broadening active customers base+volume and breadth of offerings leading to higher engagement and Customer LTV would be apt step. Promoter is Smart and as long as overall pie is growing many can co-exist without crazy marketing burn.

-

Employee count is constant QoQ, jump in expenses from 65 cr to 73 cr - likely pinch of Attrition and senior tech hires done recently

Solid valuations disparity in same assets class Equity - Angel will do 700 cr profit on annualized basis, has mkt cap of 11K cr, will likely get AMC license soon. HDFC AMC has 55K cr mkt cap on 1300 cr profits, latter’s mind share with customers is also relatively nothing compared to Angel. Growth and runway is manifold for Angel or similar players compared to any AMC.

Market has its own wisdom and seems isn’t convinced yet on according higher valuations and re-rating.

look forward to hear updates on future plans from mgmt on concall.

Invested

25 Likes

Q2 call notes - numbers and narratives are known, will focus on biz model and go forward strategy

Super App

- Super App launch in Q1 23,brokerage first, followed by rollout of various offerings over 9 months from launch.

- First thing first what is Super App - today Angel and most industry focuses on a one journey fits all approach - I.e. digitization of onboarding, good user experience, online customer service, add on services like research, nudges, mtf, etf,ipo and so on. There is no differentiation or personalization from Customer A to Customer B / 28 year tier3 self employed vs 35 tier 2 salaried and so on…point is each customer segments has different profile and needs, some they know ( explicit like trading, delivery, f&or etc) and some they don’t know well or can’t get curated yet( cheapest insurance or personal loan, suitable learning content for new in mkt folks, risk profile based investment advisory and offerings and so on…)

- Right way would be to build segments of customers, their demographic profile, model the patterns which are explicit needs as well as implict, offer curated offerings based on what customer needs( what they know and what they don’t know yet), journey based experience delivery and so on - point being a highly personalized offerings and high engagement with broking at core and as platform learns user behavior, enhance product basket for cross sell - sums up, Super App without going into technical details.

- Benefits of Super App - Hyper personalization leads to better engagement, cross and up sell, if successful could lead to a Platform type model where Angel monetized customer base for not only increasing mkt share, customer LTV, own and partner offerings - all of this delivered via technology.(predictable growth & scale with substantial operating leverage)

Risks

- Core DNA of Angel is stock broking, shouldn’t take eyes off from goal of number 1 goal here, Dinesh Thakkar knows this well and balancing domain focus vs technology focus well - for e.g. he is clear on growth runway visibility of broking biz and not pushing hard on cross sell consciously, also clear that Super App has to stabilize first on broking biz before further roll outs.

Other highlights of call

- Per Dinesh pricing is no more a differentiating factor, experience is and growth runway is huge in terms of new customers and current base mining. They don’t see new customer acquisition slowing down.

- Emphasized decoupling with market drawdowns and cyclicality for their business model and having enough levers in hand to tackle same, infact in any serious slow down they might benefit from tail end consolidation.

- As expected despite no change in headcount, employee cost is higher given lateral tech and software investments- will continue for few quarters - imagine operating leverage few quarters out.

- Dinesh was categorical on saying that if a newly onboarded customer is not motivated and engaged to transact in first 15 days - it is as good as losing that customer. Hence very high focus on making that happen and increase active clients ratio. ( a contrast thinking from ICICI security is that all these new gen folks from Tier2 and 3 may not be engaged enough and even if we retain some over longer term it will pay off) - One wants to make it work and one hopes for it to work.

- Client acquisition cost breakeven is few months, demonstrates effectiveness of marketing spend. On A Question around acquisition strategy and source- key points stand out are social media, referral, content marketing, influencer etc. They were categorical about traditional media does not work( in contrast see heavy ad spend from Groww etc on massee TV/ Video etc)

- One key aspect of Angel IMO is successfully and balanced marriage of Brokerage domain knowledge with Digital native model - competetion is good at one but not another e.g. Motilal oswal has similar domain experience but not able to pivot to full digital model, ICICI security is attempting Neo plans half heartedly and focusing more on Non brokerage pie growth, Upstox and others are Digital first but not as domain savvy as Angel hence not a full service spectrum( content, research, mtf and so on), Zerodha team is too busy highlighting mkt froth, 99% traders fail, calling out FM on taxation issue - though deserves due credit for sector transformation to discount broking and many industry firsts.

- Another execution leadership capabilities has some advantage- Risk taking, optimist and visionary Dinesh thakkar as promoter, supported by Able tech and professional team they have built and are able to retain in current environment. Wonder what motivation HDFC sec and ICICI sec of world has to transform and disrupt themselves like Angel being salaried professionals running show( will continue to do well as long as industry grows ).

- AMC license may eventually come as well - an engaged customer wouldn’t care to give wallet share of MF investing to Angel vs traditional houses/agents. In era of ETF and innovative products, Digital savvy franchises are better positioned to continously provide exciting products. So is the case for other financial products. - again Angel target group is not affluent, tier1, high salary/ high worth folks. It’s Volume and scale based Digital savvy tier 2/3/4 folks.

Bit far fetched but Bajaj finance is what it is today because of their ability to have large customer databases, quick and convenient processing, prudent risk management and underwriting- all of this was built with data and analytics focus. Who is to say that Angel can’t produce similar success in Investment domain with focus on understanding customer context little better than others and provide personalization in experience and products. Ingredients of ambition + capabilities + market acceptance are here to make use of.

Invested

13 Likes

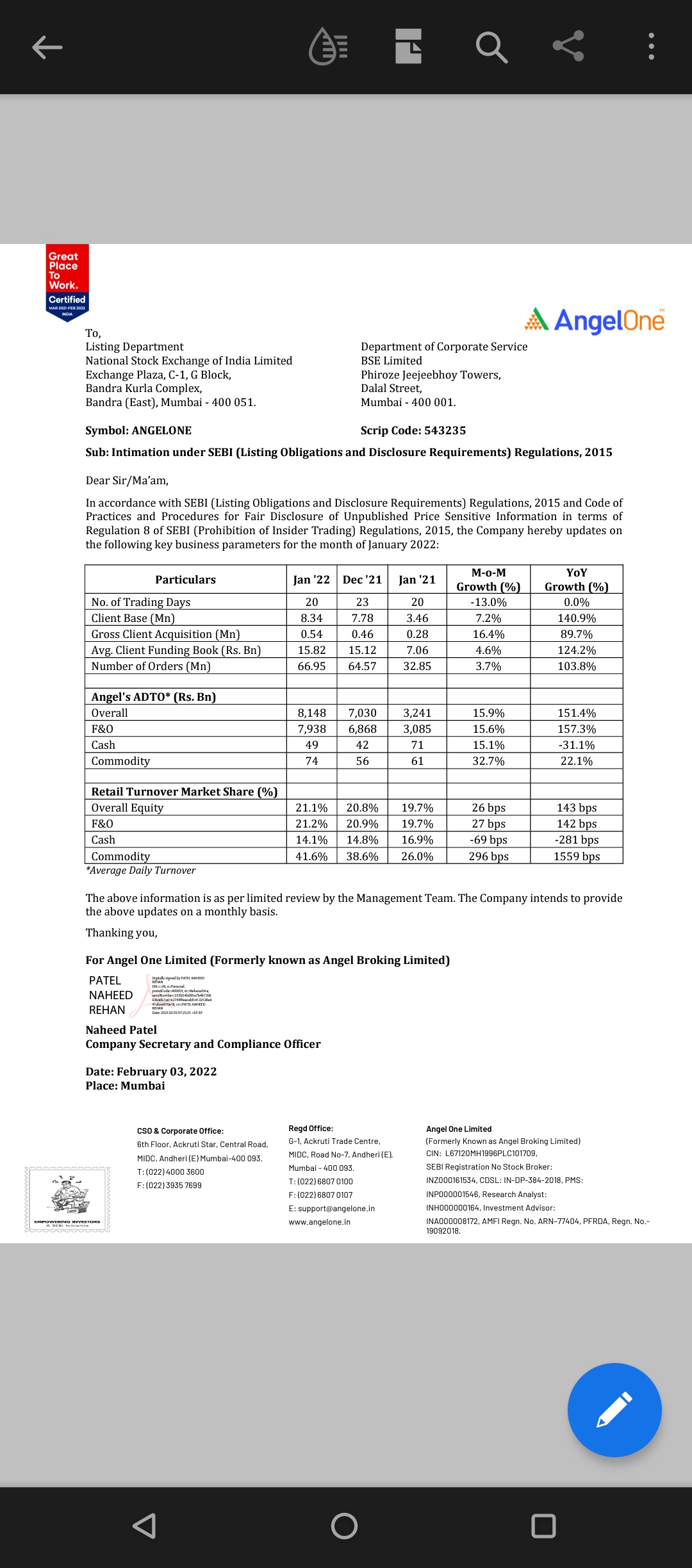

Pretty amazing numbers by angel

{kind=link}

Despite # of trading days being 13% lower, 4% higher # of trades in jan-21.

Client aquisition is also accelerating which is remarkable in & of itself. Half a million clients aquired in jan-22.

If we are at the cusp of an economic recovery , it stands to reason that the market would do well. Stands to also reason that trading volume would go up.

To my mind biggest risk to angels current revenue base is any faltering in economi recovery. Eventually such a faltering would reflect in earnings & thus stock prices & could depress trading volumes & brokerage revenues. While i would not give too much weightage to rerating in my investment thesis, the growth in earnings can surprise even the most optimistic imo. With LIC ipo coming up, lot of demat accounts would get opened. Even if some of them remain to trade, we could we a shift in the revenue & earning base.

This also creates an opportunity for angel to quickly develop their super app & diversify the revenue base & earnings base away from brokerage partially towards investments, credit & Such like.

Disc : invested & biased. This is not a reco. Do your own due diligence.

8 Likes

While faltering of economy could be a risk, the larger picture in the Indian context remains that equities still remain the preferred asset classes for compounding wealth. Given the Capital Gains/Indexation benefits for 3 years for debt funds, Crypto being dealt with huge tax/TDS, more streaming of Real Estate due to digitization of land records leaves equities as the preferred option. Brokerages that offer tech savvy platforms will gain the most. A look at Angel’s mgt team will reflect the focus and areas where Angel in transforming itself into