Hi @sahil_vi

Going forward do you think this numbers are sustainable as some day in future bull market should end.

And as we have taken taste of it in mid August when mid and small cap were down, angel also went down close to 10-15% in 2-3 days.

Hi @sahil_vi

Going forward do you think this numbers are sustainable as some day in future bull market should end.

And as we have taken taste of it in mid August when mid and small cap were down, angel also went down close to 10-15% in 2-3 days.

This is one of the most in depth interviews I have seen from Narayan Gangadhar:

Disc: Invested, biased.

On point no 5 (around 28 min in the video) he states something like angel being first of its kind to open it up as a platform. Based on my understanding Zerodha API-fied the platform much before Angel. Overall it is really hard to find what Angel provides (or can provide) that zerodha or other brokers cannot.

He is a technocrat which is great, but i think technology alone can’t be the hammer looking for nails. I really hope they have the same enthusiasm in other departments.

Disc: invested.

There is certainly some overselling. With zerodha being unlisted understanding it well is also difficult.

Having said that broking is a huge market. There is enough room for multiple big discount digital brokers. This isnt a winner takes all.

Right now imo zerodha is miles ahead of everyone else in terms of customer satisfaction & having the right product. But angel is fast closing the gap.

Yes he is lying through his teeth when he claims that they are the first to bring play-store kind of concepts, too much of overselling… What ever he is claiming is nothing close to path breaking which he is kind of makin viewers believe, every product based company worth its weight in salt follows all those best practice

Angel one is nowhere close to zerodha interns of UI user friendliness and ZeroDha cant match up to few offerings of Angel like pledging, margins, far away options trading… etc etc

I had two account with ZeroDha , I closed one of them because they wont allow you to buy faraway options for hedging which is ridiculous. Now i am getting used to Angel if all works well i will close the other account in ZeroDha…

For plain jane investing ZeroDa is good but not for options.

Zerodha is like Apple OS and Angel like Android.

Per previously indicated intent to get into MF business, application filed with SEBI

One thing worth noting in our valuation model is that as and when they get into MF biz - operating margins profile are very high for AMC (. Angel currently has 35%+ op margin, hdfc amc has North of 75%+).

There could be some visible benefits -

Assume SEBI approval comes in near future, market may reward it accordingly much earlier, execution is key but seeing Motilal as erstwhile broker getting into MF biz and doing alright gives a previous successful use case hence lowers risk - Angel execution will benefit from Digital backed scale and products. Hoping to see some MF industry hire coming on board as well.

Invested

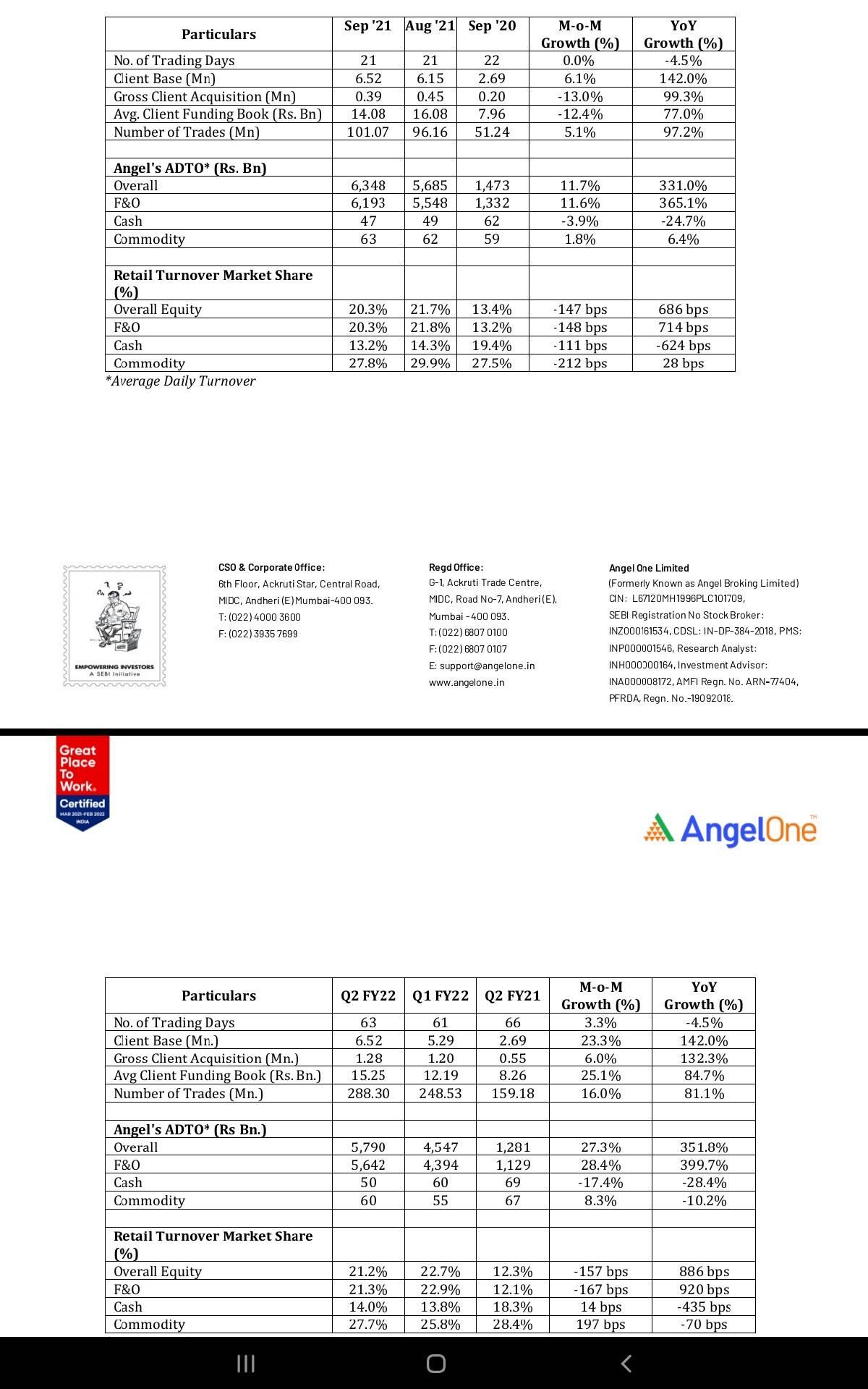

Monthly and Quarterly updated

For a change some market share loss in F&O and overall equity - reflects a possible fact that slowdown in client addition rate may have impacts in overall share – they may need to bump up mktg spends to catch up unless we are reaching a saturation point( growth is there but slowdown in rate). It’s good to have competitive intensity heat to keep them on toes.

Silver lining is no of trades trajectory is up both MoM and QoQ, This shows that Angel topline will likely have a good QoQ growth on similar lines.

YoY needless to say huge rise across the board.

Good numbers by HDFC securities, Angel will likely outperform hybrid peers. Monthly updates have already given glimpses and mkt factored of what to expect.

Key monitorable- MF biz plans, Operating leverage and margin trajectory, Cost of acquisition and activation quality, future commentary.

As of now going is good and everyone is growing in sector, opportunity size expansion seems to be surprising everyone and thus disbelief and shallow cyclical element linked to market performance keeping valuations in fair range.

Read in some WA forwards( can’t authenticate) that Crpto investors in India has exceeded Equity investor base in India - who knows opportunity size here in equity will keep surprising everyone in future as well.

Invested and believer that there is structural shift towards financialization of savings

Summary of Q2’21 Angel con-call: Long term prospects look promising. Some of the key points -

Within a year, it is likely to become an AMC. This would lead to significant change in valuations - it might get a PE similar to HDFC AMC. Also they are not planning to become a normal AMC, but a highly tech driven. e.g. Funds based on quant / algo trading strategies. This is a v successful model in the US.

Assuming that the current bull run will last for at least 4 more quarters, strong growth trajectory is likely to continue. They made the maximum no. of hires in last quarter, this indicates they are serious about the growth and they are investing heavily in to it.

They are close to launching a Super App, basically all in one app - this would lead to revenue expansion, as it would enable cross selling.

The focus is on improving customer experience – it seems they are trying to copy the silicon valley tech firms - where they try to generate “platform stickiness” by creating superior customer experience. For e.g. Air BnB despite its success has just started to work with John Ive (ex Apple) to reimagine the user experience.

Launching a new product which would make F&O trading easier. All of these products and features are taking Angel towards being a one-stop shop for investing.

My take: If this trajectory continues, it might be a good idea to hold this stock for next decade or so, as Indian equity market is still under-penetrated. The risk of market cyclicity is there and in next 10 years we may have to face two extended periods of slow-down. Also, this space is getting crowded, and it will be interesting to see how Angel creates a differentiated product and customer experience.

Disclosure – invested.

Will not be easy to match hdfc sec this time. Hdfc sec are giving Amazon vouchers. Currently getting ad of 500 voucher of Amazon.from hdfc sec to do one trade.

Disclosure: No holding.

As a longtime hdfcsec account holder, I have not seen such an offer to me. Now I’m curious and angry at hdfcsec.

If you are dormant like me then you are getting that offer.

Cheers

Can anyone explain the term Avergae daily turn over (ADTO) with respect to broking industry. What does it specifically mean in F&O, Cash, Commodity and currency segments.

Does Angel earn any revenue from Cash segment?

Groww is now valued at 3 billion $

Upstox is expected to be valued at 3-3.5 billion $

Angel is trading at 1.25 billion $.

Dont you think there is a big upside to angel one. This is the only profit making firm amongst the three.

Any views on this?

Is Angel also clutter free and equally mind space capturing as Groww or Upstox? Last I checked Angel’s UI, it was dreadful.

They have 21% market share in ADTO and 11.8% market share in incremental NSE active clients. The CEO is a formed head of technology at UBER. It is transforming into a fintech and the CEO in his interview says that he wants to provide the best UI to the customers.

I also believe that there will be consolidation in the sector and angel one being a profit making company can survive in the consolidation phase.

My only worry is that competitors are also raising insane amount money from PE players.

I’m still tracking this stock

checkout angel spark their new app, still in beta mode

The upcoming LIC IPO can be a huge trigger for Angel broking.

LIC has 29 crore policyholders, who’ve been asked to open Demat accounts since 10% of the issue is reserved for policyholders.

Assuming 5% of this universe open demat accounts, the number would be 1.5 crores.

As per Angel investor presentation, 1 out of every 7 new demat accounts is opened with Angel. This translates into 21 lakh new demat accounts.Assuming 1/3rd of these are active clients, the incremental revenues can be 7 lakh* Rs 8000 per active client = Rs. 560 crore annual revenues.This means more than 25% of projected FY’22 revenues from these incremental numbers. Thoughts?

Angel customer base median age is mid 20 to late 20, last year or so most of customers acquisition happened in this range and that is what they intend to focus on per mgmt. LIC existing Customer base is likely to be much higher age, legacy folks and conservative folks rather than new gen. Even if they use discount brokers to open accounts they might be dormant than active eventually unless Angel can nudge them but doubt it given totally different age and demographic profiles.

CDSL type entities might gain a spike IMO than Angel or Zerodha of world. CDSL ac trend does reflect upward trajectory.

However Angel has done well in recent correction per last month biz updates( Nov) when market were in correction mode in Nov, so is the case of Dec and a good test of business model of Angle if No of trades continue to do well in Dec as well. Q3 performance will be keenly watched both on ability to deliver on topline and protect margins during mkt down cycles - though 1 qtr is small period but business resilience will be visible.

Stock has corrected 25% plus from top and seems to be in consolidation mode below 50 DMAs.

Invested