In their annual report they talked about spark and smart store, spark was available in beta testing in play store since end of march which is great upgrade from their current app.

Now smart store is also available, it is a place where one can learn about new technologies in trading, buy third party products basically angel is integrating into a platform as management talked about.

1 Like

Angel broking’s chief growth officer Prabhakar tiwari interviewed by leadsquared

6 Likes

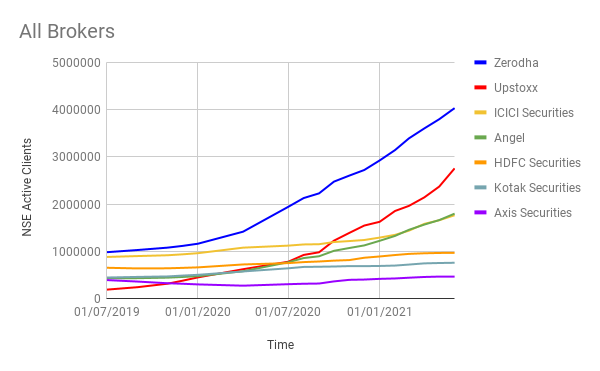

Here is an analysis of growth in NSE active clients over last 2 years or so.

Few observations:

- Bank backed brokers are losing marketshare of nse active clients. Only exception here is icici sec, which is a stand out among all bank backed brokers.

- Among the discount brokers, zerodha and upstoxx stand out. Both have been growing at a very nice clip.

- Angel is going well but is matched by icici sec in terms of growth. Having said that, angel’s growth curve started much eaelier than icici sec which is why angel was able to catch up with icici sec and now both are matched in terms of nse active clients as well as growth rates.

Some interesting scuttlebutt from Twitter in icici sec. If others can contribute about such underhanded means by which other brokers might be trying to influence this metric I’d be very grateful.

“ICICI played a trick. I had an old dormant account with them opened 10 yrs ago. Few days back they called me and asked me to trade 1 axis share and they told they would waive off maintenance fee. So I did it. Now I understand they wanted to influence this nse active users metric”

Disc: Invested, biased.

20 Likes

Active client numbers these days do not gives clear picture, what matters is number of trades on the platform, also icici securities is losing market share.

3 Likes

Investor Conference Call Highlights:

- The company appointed Mr. Narayan Gangadhar as the new CEO. Mr. Gangadhar has extensive

experience and has been part of global experience leading technology businesses like Google,

Microsoft, Amazon, and Uber. - Angel saw its highest ever overall ADTO of over Rs. 3.75 trillion in Q4 FY2021 which has grown

close to 15x between Q1 FY2020 to Q4 FY2021. - The company has endeavored is to share at least 35% of its profits in the form of dividends every

quarter. - Around 72% of broking revenue comes from direct clients.

- The management has highlighted that Angel is also looking to become a platform company where

it can offer lots of other financial services to its customers. - For the next 2-3 years, the focus will be to get maximum market share from the stockbroking

business, to get maximum market share in the mutual fund business, and to get some inroads in

the insurance business on the digital platform. - Angel is looking to make a multifunctional app where it will be selling mutual funds and insurance

on the same app platform. - The management also sees huge scope in passive investment and ETF business and smart beta

product through the digital app route. - It will be looking to introduce a mutual fund having backed by its Robo advisory passive strategy

where it can reduce costs of distribution as well as the cost of managing funds. - The company is not spending on mass media and is instead targeting social media and search

engines and the internet for acquiring customers with AI/ML-led acquisition plans. It is also

specifically targeting Tier 2 & 3 areas that remain underpenetrated. - The scope for expansion in the underpenetrated tier 2 & 3 regions is present for all digital players

due to the lack of physical branch accessibility here. - Angel boasts of an activation rate of 38% to 40%.

- The company is earning an OPM of 44% from the digital model and it is aiming to bring this up to

50%. The company is also looking to maintain a breakeven time of 3-4 months for every new

customer. - The company is aiming to become the largest player in the stockbroking space in the next 2 years.

- The vision for becoming a preferred fintech company through the all-in-one app should take 6-7

years according to the management. - Angel has not had to burn cash like other online brokers as it has a well-established customer base already and didn’t need to spend too much on expanding its scale. Given its size in broking space,it can easily put up the acquisition cost for new segments from cash flows from the established segment.

- In the AMC business, the company will be going the passive funds’ way with its ARQ engine and it

will not be doing any human stock selections as its model has proved to give good performance

over the past few years. - The new CEO states that a big part of his focus shall be to build large teams with the right skill set

on machine learning, data science, and AI sides. - The tech investment should be around 13-14% of total OPEX excluding fees & commissions for

Angel. - The increase in opex in Q4 was mainly due to higher customer acquisition as the acquisition costs

are always front-loaded. -

90% of customers added in Q4 were young people with an average age of 30.

- The main cost in setting up the AMC will be coming in year 3 which is the marketing cost.

- The management is looking to launch the new super app in the next 2 quarters.

- Easy access to stock markets through mobile apps, declining interest rates, and significant underpenetration of equity investment in India are expected to be the key factors driving growth for the industry.

- On average a customer takes around 4-4.5 months to break even for Angel and provides at least

5 years in terms of regular revenues. - The company is not looking to acquire any existing AMCs as it is looking to make its disruptive

model rather than pay a premium for an old model in the AMC business.

8 Likes

monthy updates

MoM negative in ADTO and mkt share( may vs june), however client base growth continues. Corona peak coincides with MoM drop ( mid may to mid june). Mkt share degrowth could imply competetion intensity or higher impact on Angel captive client base in value terms, July performance will be key to observe.

Q1 22 is good growth over Q4 21 across all parameters - considering this was peak of Corona wave 2, business resilience is visible.

Invested

4 Likes

Great numbers from Angel One.

EPS has increased to 14.8 for quarter.

Optically the stocks looks very cheap, however does P/E or EPS matter in the bull market for broking companies? The transformation to Fin Tech will take its own sweet time and hence ignoring it as of now.

Disc. Invested 8% of PF

4 Likes

Investor Presentation TakeAways

Investor presentation

- SmartStore is the joker in the pack. If Angel can build a successful engagement based platform for the users. We also see that they have initiated regulatory approval for AMC already

- Some Details on how they are developing the platform for educating traders. Discussion forums are the primary variable to track IMO. I am HOOKED to ValuePickr. I came for the knowledge, but stayed for the community.

- ARQ Prime, their proprietary smart beta strategy is steadily outperforming midcap index.

- Good to see expanding market share of NSE active clients. Would also love to get feedback on whether angel indulges in any petty practices to inflate this number (the way ICICI direct and groww do).

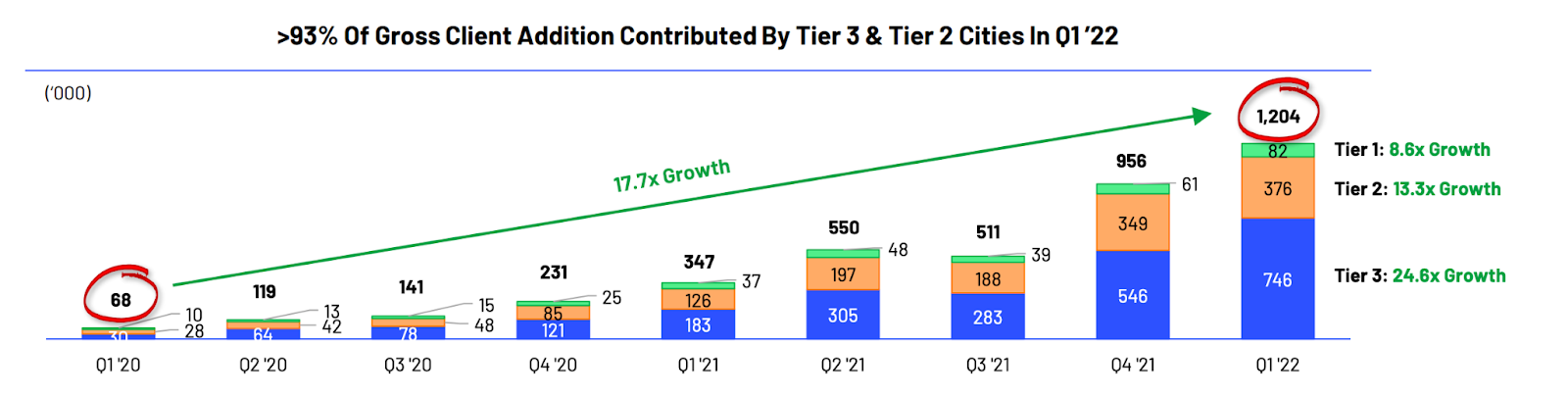

- As suspected, the bulk of the volume growth is coming from the tier 2 and 3 cities but interesting to see that there is an actual acceleration in growth as we go down the tiers.

- Since most of the revenue comes from flat fee structure. The # of trades metric is most important for revenue. Good to see ~15% QoQ growth in that. ADTO is also important in order to have an engaged client base. As suspected most of growth is coming from F&O segment with cash and commodity being flattish.

- The margin funding book is growing nicely. Remains to be seen how much of this is sticky growth. Remains to be seen how fast India margin (~1B$ now) funding becomes as large as China (100B$) & US (800B$)

- Interesting to see how their digital focussed talent pool has growth even though the overall talent pool hasnt. Shows the transformation in the thought process & focus on AI & ML enabled user experiences

- Look at the strength of the independent directors on the board. Max life insurance, World Bank, LIC, SBI life insurance

Disc: Invested, Biased

6 Likes

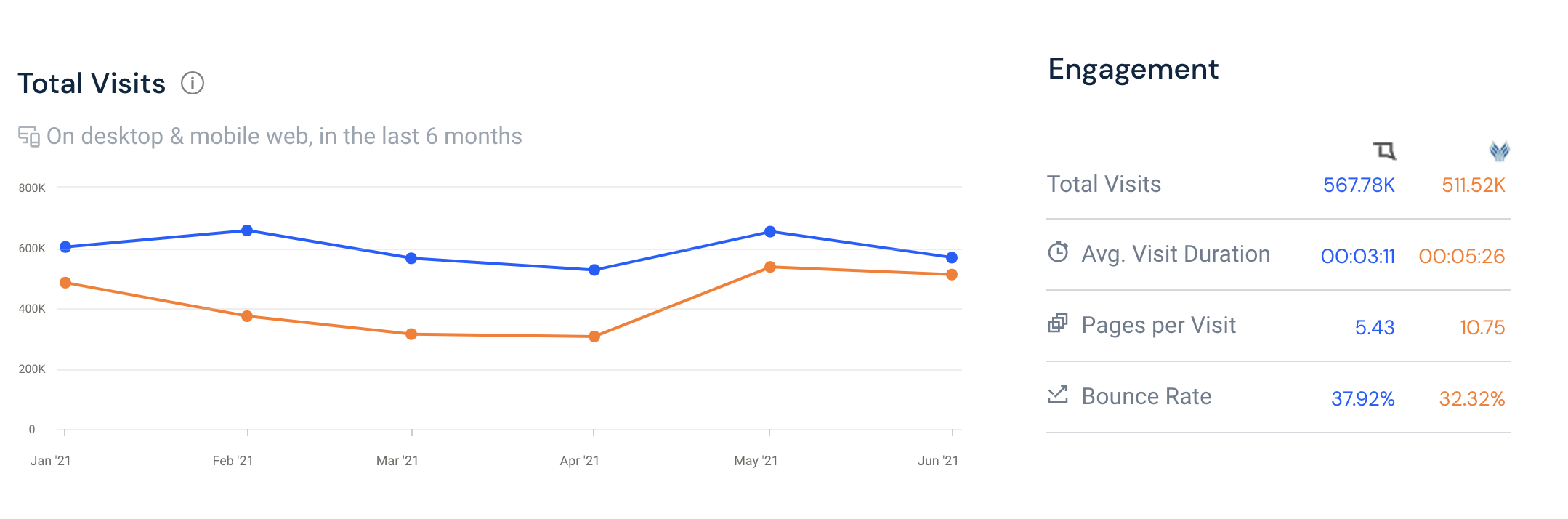

I am not able to understand how the angel will push the traffic on the smartstore. The current traffic on Forums – SmartStore is almost negligible and also doesn’t seem they are not pushing any content creators or engagement drivers or any other incentives on these forums to create initial traction for users.

Engagement on tradingqna.com (competitor platform from Zerodha) is currently very high and even comparable to valuepickr

The first column is tradingqna and second is valuepickr

Also there web UI/UX needs to be overhauled not sure about app UI/UX considering they are heavily hiring on digital front.

Disc- Invested, biased

2 Likes

Q1FY22 Concall Notes

- Will launch super app in next few quarters (later this year). Superapp will be 1 stop shop for all financial solutions. We will offer lending products from other banks. 2 years from now we will also offer our own products: ETF and smart beta. Expect 3P product distribution to increase post super app launch. Able to understand customer better. Future needs. Higher lifetime value. Straightaway comes to bottom line. Angel Spark is 1st leg of superapp.

- Massive growth opportunity in next 10-12 years due to fintechs.

- When market goes down, client turnover drops, but revenue does not drop that much due to flat fees model. Lifetime value of customers has improved (people who used to trade less after a year, are also trading more because they are on the app).

- Peak margin implementation led to more impact on turnover and not on revenue.

- We are far away from the 15% limit for F&O volume. Growing market share is not a problem.

- MTF book has grown 26% but interest income only grew 15%. Why so? Interest income comprises interest we own from FD as well as client funding. There has been a decline in interest we earn from fixed deposits.

- Margin requirement rules have led to reduction in the volumes/ADTO but not much on revenue. More than offset by new client addition.

- Smartstore launched in June21. Provides verified solutions to users to trade effectively. Can be huge optionality. Can monetize the platform itself. Revenue sharing model with niche fintechs. Wide range of trading applications. When developers sign up, many features are for free: profile of customer, analytical data of app in real time. Back testing. Angel will serve as an intermediary for the fintechs and the users. Can also serve to provide nudge to the relevant users. 100,000 users already for the platform.

- For acquiring new customer from some channel we look at unit economics, we dont look at ARPU. We dont have cost of acquisition for AP acquired clients but it has better unit economics so it can dent ARPU.

- Can creating a super app affect the focus of our app. Having more journeys can overload the user experience, but using ML enables us to build experiences which are tailor made for the client.

- We are not looking at size of customer today, we are looking at what their wealth will look like 10 years from now.

- Cash market marketshare reduced in Q1. 14% for last 4 months. Whenever there is a peak margin rule implementation there is a knee jerk reaction in terms of losing market share.

- Activation ratio will increase as we bring more journeys to the super app.

- Market opportunity is at least 10x compared to today.

THis is not even 2 months old. Only started in Jun 2021. Give it some time. ![]()

Edit 19 July 2021:

Major consolidation happening in broking industry:

Dinesh thakkar interview:

Disc: Invested, biased

13 Likes

@sahil_vi , you also mentioned about consolidation in the industry, which is good, weaker players moving out. But I also read the article on HDFC securities to enter broking business as discount broker. So, isn’t it like weaker is moving out but increased profits/increased participation is attracting companies with deep pockets ? And that will not be good as profit pool gets split.

And I really appreciate your fantastic write up on angel broking.

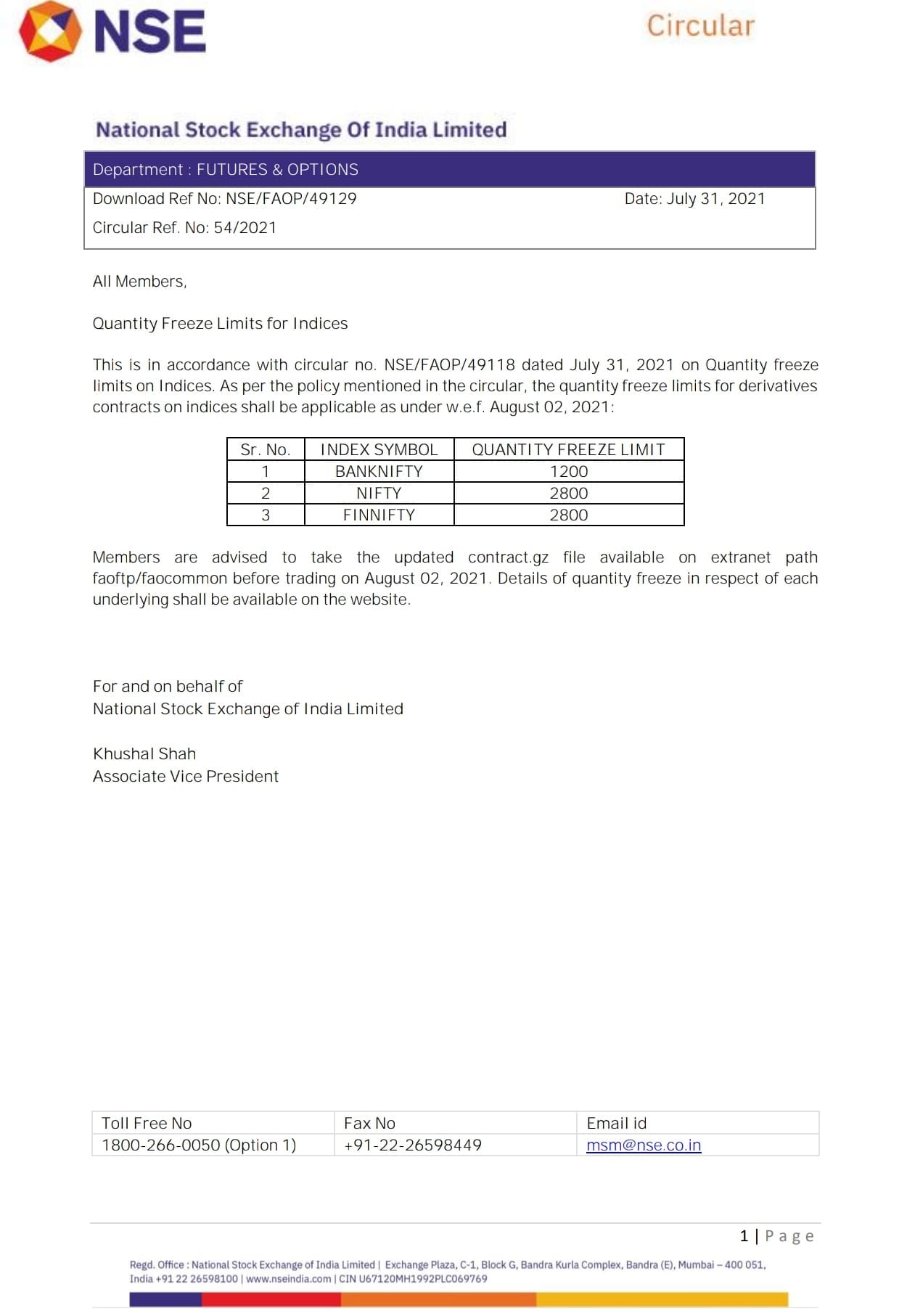

NSE quantity freeze = more number of orders = good for discount brokers like Angel who charge per order.

2 Likes

Can you elaborate on this please.

NSE has been reducing the threshold progressively from 10000 to 7500 to 5000 to now 2800…which means that more number of orders have to be placed if the quantity exceeds the thresholds set…

Just to add a little bit of context this was done to prevent the situation like the one that happened when there was a flash crash due to an erroneous trade.

For instance if someone wanted to sell 200 lots or 10000 NIFTY …one will have to place 4 orders,

2800*3 and another order of 1600 quantity to accomplish the same…so brokers make more money as more number of orders have to be placed compared to when the quantity freeze per order was set at 5000.

8 Likes

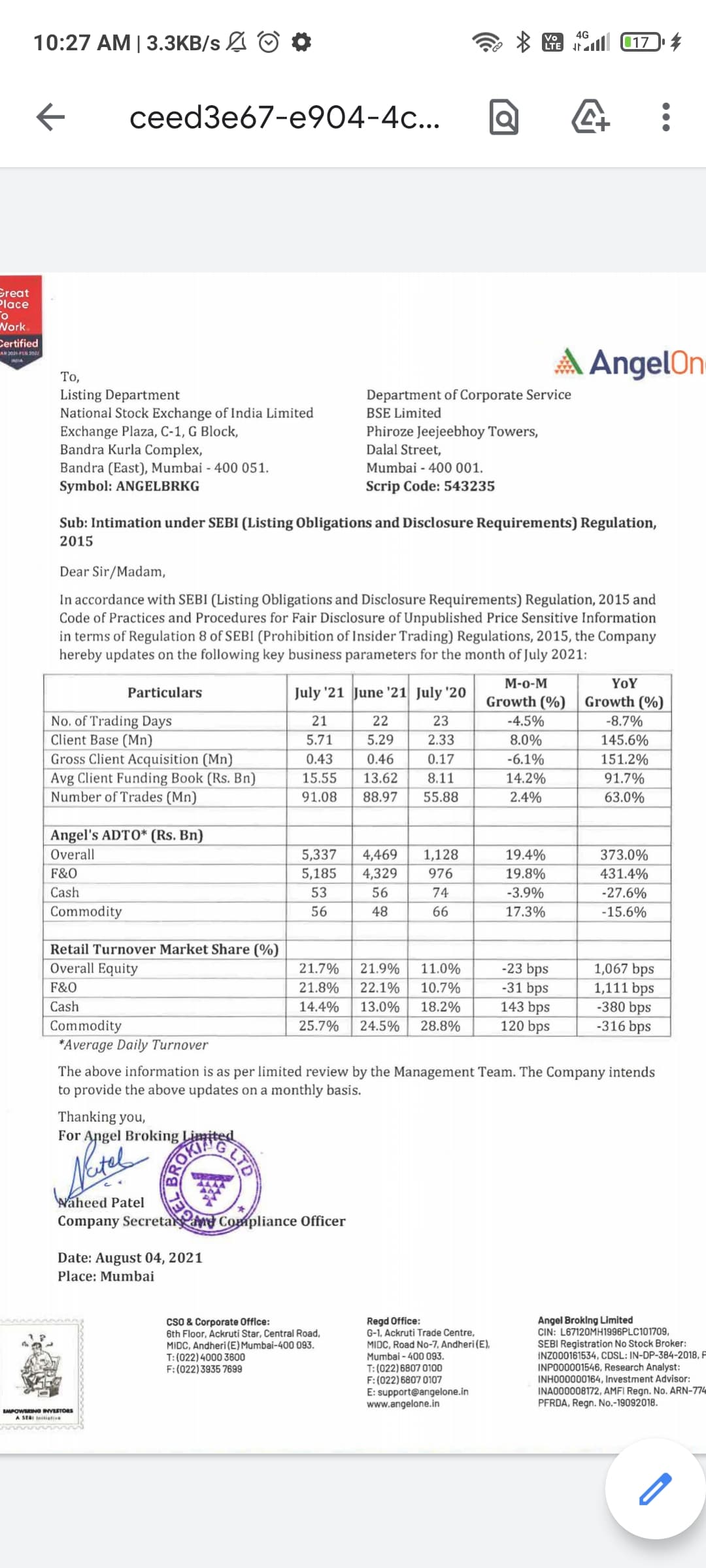

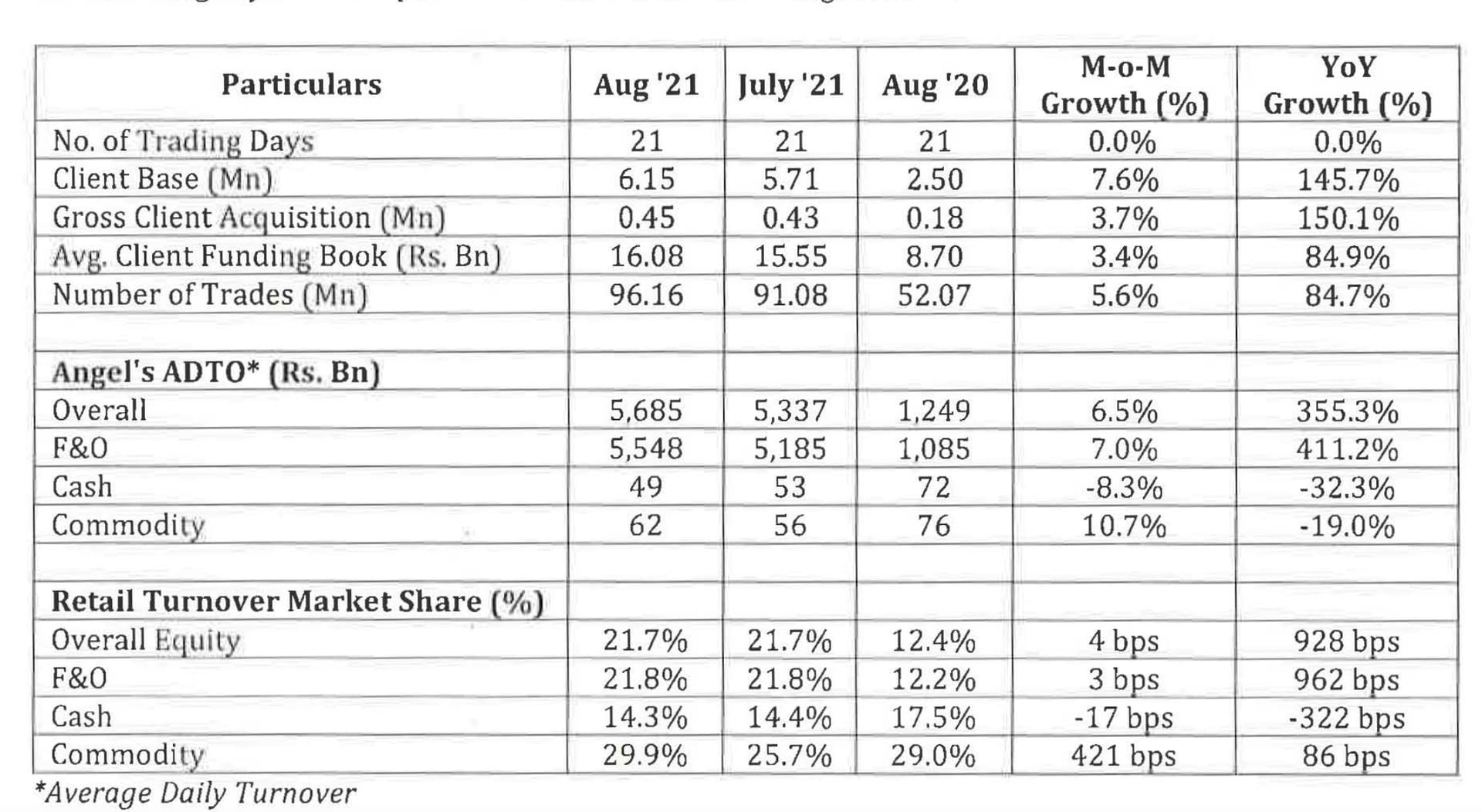

July’s bussines update, again firing on all cylinders.

One poin that i want to make is in June 20 angel’s total client were 2.15 million and in august 21 angel will have 6 million total customers so i.e 3.8 million new customers and starting from this month some of them will start contributing to the monthly mantinance charge of 20rs as you know angel doesn’t charge mantinance for 1 year so these 3.8 million will get added in paying mantinance charge customers till august 2022 so these 3.8 million alone can result in 7.6 crore of revenue every month and 23 crore quarterly and 92crore yearly and this revenue will go straight into bottom line so this alone is big massive bull case scenario for me, tell me if i am wrong and now add 4 lack customer for every month to these 3.8 million after july 2022 all this is if their bussiness remains at current levels but we know as customer grows thier revenue from their main bussiness will also grow i.e broking and they are bringing more products like mutual funds,insurance,loans etc and revenue from these will also be a addon to the OP margins.

5 Likes

I can totally relate to this. 5 years ago I would have never thought I d open an account with a full service broker but as my equity portfolio grew as a proportion of my total wealth, the little things mattered. You start thinking of “What Ifs” Today if I have an issue I know i can call an actual person who ll take care of it. Not some bot. When i sell shares the proceeds go straight to my bank account. These are things I knew 5 years ago as well but you dont think you need these EXTRA services until you get to a stage where u have enough to lose. Extra brokerage is a small price to pay for peace of mind. I still use Zerodha but mostly for Trading

2 Likes

Angel or ISec? For all those trying to figure out which one is a better.The answer is both or none Please consider this-Competition among firms is for customers and seeing how they serve different customer needs it’s not fair to think of them as direct competitors. Sure, in periods of supernormal industry growth like the current one there will be some overlap in the type of clients they onboard but as growth moderates (I am aware market penetration is just 3%  ) which it always does, the difference in the client profile will become more evident. Both these companies know that and to that effect they have a very different approach towards client boarding.

) which it always does, the difference in the client profile will become more evident. Both these companies know that and to that effect they have a very different approach towards client boarding.

Angel wants to gain market share in hopes that some of its clients might have enough income in the future for them to successfully cross sell other financial products. It hopes to do this via technological superiority to increase customer stickiness and customer experience. Isec is not behind when it comes to tech investments but it doesn’t need to race with Discount brokers to acquire customers at such a frantic pace. It cares more about the quality of clients. It cares more about revenue per customer than just marker share gains. Angel doesn’t have that luxury. It has to gain clients as fast as possible. Broking revenues after all are cyclical (even though the industry has moved to revenue per trade model) but with enough market share, it can possibly make a good ROI on its total CaC, if it can get some valuable lifelong customers.

So to sum it up- If you want to compare companies then look at their strategy and see what they are trying to achieve. If they are doing just that, then one needn’t worry. Both these companies are doing what they said they would and hence I remained invested in both

8 Likes

Angel will be coming out with its startup funding program named cosmos where they will be investing in emerging companies in investment field.

3 Likes

Great MoM growth in most segments. Special focus on Client funding book and Number of trades.

Disc: Invested, biased.

7 Likes

Thanks Sahil for posting the data.

Angel’s cash value has come down in August, though number of overall trades have gone up. I am not sure if all the trades are charged per lot. Also, are they trying to target just F&O traders ?