The company is one of great achievement of being continuously paying dividend despite operating in commodity sector (started with sugar and then diversified in chemical and power) since inception. It is a mean achievement given the volality and limited free cashflow from commodities and definitely talk about corporate governnance practice of the company.

While business is doing well and , in segment wise results, not able to get any understanding on power business profitability. It has been volatile and determine direction of profit growth for the company in past. Valuation is quite moderate in my opinion.

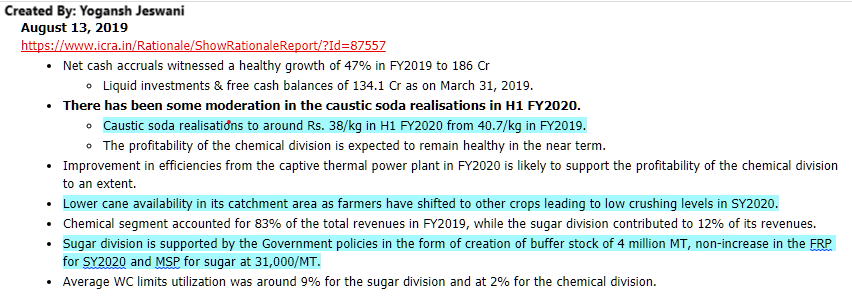

Came across an Environment Clearance report for a proposed CAPEX plan by Andhra Sugar.

You can access it by clicking here. Below are some of the key points:

With not much loans on balance sheet (reduction in loans in Sept 2018 balance sheet), high cash generation, brownfield capex expected to commercialize soon + good dividend yield of 3%+ (and might be higher dividend in FY19)…the stock trades at 5-6 PE multiple!

Margins on Caustic soda segment have been very strong for past many quarters and Industrial Chemicals is also posting strong numbers (Please see below table).

Last quarter results were decent and the stock price saw a good run up. It now is available at PE of around 7. Is the market considering Andhra sugar a Chemical commodity company with price cycle already peaking? The company is a good dividend payer and I have not come across any governance issues. Do cheap valuations for such a long period indicate a value trap. Requesting views.

Stable set of numbers from the company. Waiting for Annual Report for some cues on reasons for such huge margin fluctuation in industrial chemical business.

Is anyone aware of the dividend payout timelines. It was announced post last quarter results but there is no clear mention of the ex-dividend dates etc. The filings to BSE also dont have exact announcements on dividends.

The company has some issue with BSE and hence all exchange related information are available on NSE. Please check NSE website. The company would trade ex dividend from September 12 2019 as per NSE

Company came out with great set of numbers. I am surprised how they are able to maintain Chlor Alkali segment profits since competitor DCM Shriram had reduced realizations this quarter. Would love @ayushmit@dd1474 to comment on the numbers.

If someone has attended the AGM, can they post their observations?

Regards

Kanv

Disc. Invested from 410 levels and it forms 4% of my PF

Surprisingly pretty good results. I don’t think anyone would be expecting such numbers given the fall in caustic soda prices and beating in nos of other cos. There could be 2-3 possibilities - 1. Andhra (or cos in South) might be having better pricing 2. There might be lag effect 3. Maybe because of integration Andhra could do better.

Another thing is that they announced commercialization of another 100 tonnes of capacity from Nov.

JOCIL - A subsidiary of Andhra Sugar is on sprint… Meanwhile sales of the JOCIL kept on increasing + Corona effect added more demand to the industry by making no of soaps & chemicals…

Am not an expert but someone can have a look at JOCIL results…

PAT : DEC 2019 : 491.51 | SEP 2019 : 404.41 | JUL 2019 : 71.56

Can someone check and let me know your inputs if this would add strength to Andhra sugars?

if so? what number and percentage?