I have been tracking Andhra Sugar for some time now and would like to highlight the theme which I feel has potential to improve the numbers Company has been posting.

Intention is to play on the Sugar cycle with Caustic soda (Chemical Division) acting as a safety net.

Over the years Andhra Sugar has been generating around 70% of its standalone revenue through Chemical Division and remaining from Sugar. Since, sugar has been under performing for past few years (industry wide problem) the profitability of Andhra sugar was getting hit. Still, the numbers posted by Chemical division (Caustic soda and Industrial chemical) were able to digest the loss from sugar and came out to be in profits, overall. (Please see below image)

You can Click Here to go through the Standalone and Cons. segment numbers which I have plotted and get a feel of the theme I trying to share.

About Andhra Sugar:

The Andhra Sugars Limited was established on 11th of August , 1947.It has operations located at Tanuku, Kovvur, Guntur, Taduvai, Saggonda and Bhimadole in the state of Andhra Pradesh in Southern India producing 25 different products. It is 9th largest chlor-alkali producing capacity in the country and has one of the largest producing capacities in the southern India. Its products are as follows:

Sugars

Aspirin

Alcohol & Alco Chemicals

Chloro Alkali

Sulphuric Acid

Super Phosphate

You can get further product-specific details from here.

Sugar has posted profits after several years and has break-even in 9MonthsFY17.

Caustic soda has posted good numbers with an improved margin.

Industrial Chemicals 9 Month Margins have doubled from FY16 levels.

33 MW coal based power plant at Saggonda is near completion and will provide saving in power cost, which is a key expense in Chloro Alkali segment. Thus, possibility of further margin improvement.

Aspirin plant (US-FDA approved) achieved 75% capacity (PY 55%) and capacity expanded from 1000 TPA to 2000 TPA.

What are the threats?

Both the segments: Sugar & Chemical are cyclical and pure commodities.

Commencement of incremental caustic soda capacities in the southern market, coupled with caustic soda imports, could put pressure. (As per ICRA credit rating report. Click here to read the rationale.)

Questions in my mind:

Caustic Soda segment posted good numbers in Q3, as both sales and margins expanded. What were the drivers here? Did we see improved realization or cost efficiency? Also, is there any recent capacity expansion in this division?

With our own power generating capacity (33MW plant) what will be the future relationship with APGPCL, given the supply issues faced by us with them (61.59 cr invested)?

What is the expected cane availability in ASL’s catchment area? Any issues or concern that they are witnessing in sugar segment?

What is the update on 100 TPD Sodium Hypochlorite project (expected commencement was oct 2016)? What is the investment in it and potential revenue and margins from it? What will be the key market and customer for this segment?

How has been the performance of aspirin segment?

What is the installed capacity and utilization figures?

What is the target optimum product mix? Gradually are they moving towards value added products, and aiming to use their existing chemical division capacity as a RM source or backward integration?

The story is looking attractive to me as it is a professionally run company with a long history, a strong reach in market in its respective products and good dividend payout in the past.

Pleasingly, all this is still available to us at: PE of 6 CMP: 268 BV: 251

@yogansh Thanks for sharing it. Is there a risk of the company being at peak profits and hence the 6 P/E looks optically low and on a normalized basis it may look higher?

Few questions on the top of my mind- haven’t done any work yet

I saw the segmental numbers for their caustic soday division - in the five years they have never made a loss there- that is phenomenal, given caustic soday is a cylical sector? Any answers as to why is that the case ?

Sugar has been the big driver for profit growth - one needs to be sure where we are in the cycle. This will give us can the profit sustain for the next few quarters… One data point we know is that the production in this season has declined as per the official figures

Can we do an excercise of comparing the capacity/margins and valuations of peers in sugar & chlor alkali industry? That should give us some insights.

I have been following this company for sometime and it’s pretty interesting to see that the caustic soda segment has remained very very stable for them and it generates very high margins. What could be the reason for the same? Infact, in recent years, the margins had started tapering off but they have jumped back in the latest result. It would be great if we can understand the drivers for the recent growth and sustainable of the same.

Yes, industrial chemicals seems to be doing pretty well for them. They keep bringing new products or expansions in the same. The margins are also very healthy…may be its due to forward/backward intergrations.

Can you share the excel sheet of the above data. Thanks.

Ya, even I have the same question. I always thought that caustic soda is highly cyclical. I am trying to compare the numbers with some other Caustic soda players… Has anyone already done it?

I don’t think its at the peak as there are several moving pieces in terms of expansion and efficiency drivers being put into play.

Co is setting up a 33MW power plant for captive consumption and as Chlor alkali is a power intensive industry, this plant will play an essential role in improving margins. Also, for past few years due to gas issues faced by APGPCL (Andhra has invested 61 Cr in it) they were impacted by high cost of power.

Another thing that I came across is that power tariff cost has also softened in past Qtr. If this is true, it will prove to be a real good news as the overall power cost across division will witness substantial reduction.

Aspirin plant is getting its capacity doubled. As of now, it contributes just 4.4Cr to profits. But, with the plant having US-FDA approval and international inquiries (as per AR16) this is another section which might offer some growth.

Another addition to business is 100 TPD Sodium Hypochlorite project (expected commencement was oct 2016, as per AR16). I don’t have any quantitative details about this project. But, its worth understanding -What is the investment in it and potential revenue and margins from it? What will be the key market and customer for this segment?

After several years sugar has again turned back into profits. I agree with your point that we need to understand the sustainability of these numbers.

In the sheet that I shared in my previous post, have put in some initial data about capacity under Peers tab. We can surely work in more depth and try to dig out a better view from it.

Thanks for sharing your datasheet, these numbers gave me a much better picture than what I had so far

Since Caustic Soda is very energy intensive sector, it may make sense to include power+caustic soda figure to get true picture of Caustic soda business. ROCE for power is around 7% from FY02 to FY16.

Yes, I think above is the correct way! Its a good way to look at the data. At the same time as they are reporting it as a separate segment, may be they sell some power back to the grid. But anyways this is a better way to look at data. Interestingly the margins and ROCE are still very good.

ICRA has upgraded the long-term and short-term rating for Andhra Sugar Ltd. However, the outlook on the long-term rating and the medium-term rating is revised to Stable from Positive.

You can read the rationale from here. (Dated:January 25,2017)

The Power Plant is not yet commissioned. They are expecting to commission it by March 31st.

Aspirin business is really doing well. they did double the revenue this year. The work on it is going on.

100 TTD sodium Hypochlorite project may take more time.

Overall, business is doing well and we can expect the quarter to be similar to the last quarter.

It may just be a proposal and may take quite sometime before it gets commercialized. However, it does make a lot of sense as they would have already done the expansion for power plant and they already have huge land bank. This all may result in material benefits as seen in several brownfield expansions.

I have taken and compiled all the data from publicly available free sources like: annual reports, exchange announcements, credit rating reports etc.

You can find all of it over the net.

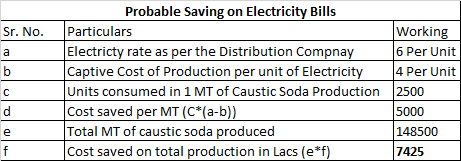

Good analysis. However, in my opinion, the actual benefit from the 33 MW power plant may be lower, as the maximum possible generation from the plant is 289 million units (i.e. 33 MW * 100024365) assuming 100% PLF and plant availability for full 365 days. Taking a more realistic 85% PLF, the generation possible is ~246 million kwh, and assuming a price differential of Rs. 2/kwh as per your estimate, the annual savings work out to ~Rs. 49-50 cr., which, in my opinion, is still substantial