Trying to revive this thread. At at PE of 10, is this a good buy. Also, less of a sugar company than the name suggests

1 Like

@varaganesh

It would be better if you add some insight with message to revive thread. Just writing message without any input would not lead to any meaningful discussion.

1 Like

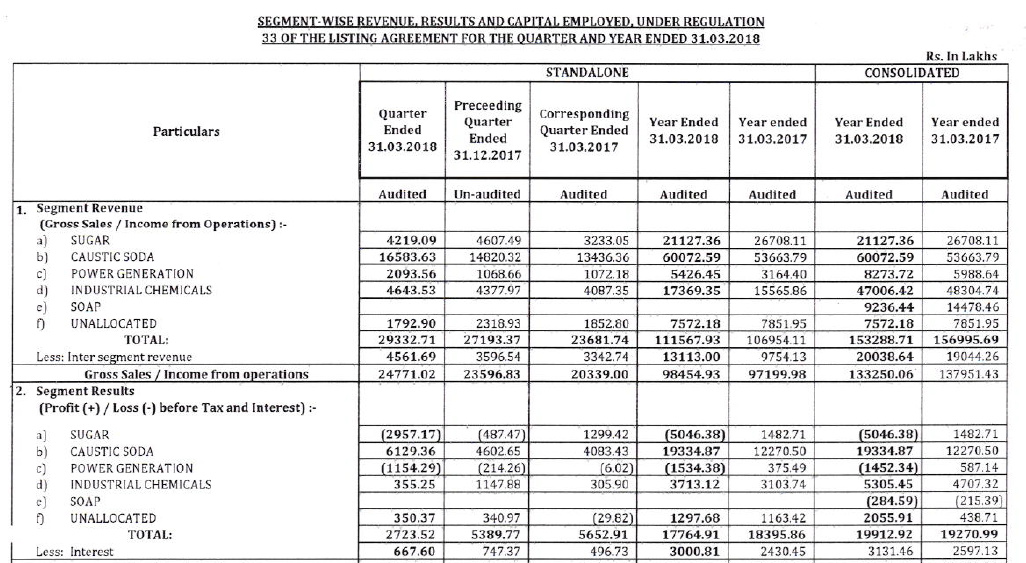

It seems like casutic soda prices have moved from 500$/tonne level to 600- 630$/tonne levels ( source - Grasim and DCM sriram reports). DCM sriram, Grasim , Gujarat alkalies and Gujarat Flurochemicals have shown better margins. There is no new capaicty adding in FY19 . But small companies like DCW, TGV Sraac and Andhra sugar lacks any margin expansion in Q4FY18.

1)Anyone has any knowledge about pricing of caustic soda and why south india based companies are not performing well? One of the reason can be power costs as mentioned above

2) Are we at peak earning cycle? Domestic alumunium and paper demand is intact.

Before you invest in the company please visit the website BSE India

https://www.bseindia.com/stock-share-price/andhra-sugars-ltd/andhrsugar/590062/ and further I tried to browse to the " Corp Announcements" section which leads to below link

https://www.bseindia.com/corporates/ann.aspx?scrip=590062&dur=A&expandable=0

The company is not submitting its financial results regularly and I tried to visit their website from there I got the results

https://theandhrasugars.com/quarterly/

Although the caustic soda prices may be high just like DCM Shriram - Andhra sugars also has other verticals which comprise of Sugar amongst others. Since sugar sector is going through a limbo which is affecting the profitability of the group as a whole.

Also Sugar and Caustic soda are both cyclical in nature and how can we justify giving higher PE multiple when there is turmoil in sugar sector since 2018 also will have good monsoon which will lead to higher sugarcane harvest.

And please don’t invest by calculating the PE multiple of current year EPS (which might distort our decision making capabilities especially for cyclical companies) instead we should consider the EPS over an entire cycle.

Kindly revert if an anomaly is noticed in my rationale.

The company is regularly providing information on NSE. As per the company, the shares are listed on NSE. There are some issue with BSE due to which the company is like to listed on BSE.

You can get information about the company related news on following NSE Link

https://www.nseindia.com/live_market/dynaContent/live_watch/get_quote/GetQuote.jsp?symbol=ANDHRSUGAR&illiquid=0&smeFlag=0&itpFlag=0

On performance of the company, it would be call of individual investors. Segment wise results does provide some idea about Sugar and Power business adversely affecting the performance. The future growth and valuation is the call investor shall take.

Discl: I have invested in company for more than year and my view may be biased due to my investment.

2 Likes

Andhra Sugars is not listed on BSE but trades. A few years back when I asked to company officials why the corporate announcements are not updated on BSE, they stated they do not submit their filings. BSE allows trading,eventhough AS do not pay any listing fees., which is strange.

Disc … invested since 2009… 3 % of portfolio

1 Like

While they have been submitting results to the exchange, the shareholding pattern does not show anything beyond 2012. That is strange.

Disc - Invested since 2003, added more in 2014.

All the details and listings are available on NSE.

Finally some benefit of higher caustic soda prices got reflected in the Q4FY18 results of Andhra Sugar. Though the overall results got hit due to the big loss from the sugar segment and power segment (which they have scaled down from last few years…yet it gave a 30 Cr loss on 42 Cr turnover! )

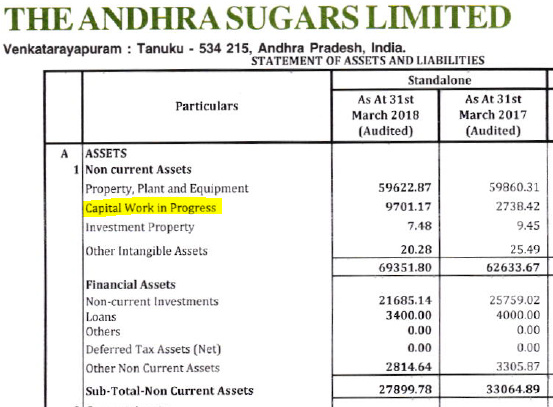

As per the balance sheet there is a CWIP of close to 100 Cr…is it towards the expansion in caustic soda planned earlier? Will this expansion come through while the going is good for the sector?

2 Likes

In notes they have mentioned that close to 76 crs. Is capital work in progress for expansion

Any idea why they post such losses in power segment ?

Latest credit rating report of the company. It’s good to see that the prices of sugar have recovered from Rs. 29 per kg to Rs. 33 per kg and also the prices of caustic soda are in upward trend as per the report. Outlook revised from stable to positive, a good sign for all caustic soda companies.

https://www.icra.in/Rationale/ShowRationaleReport/?Id=71759

2 Likes

This credit report has some good insights:

Key Points:

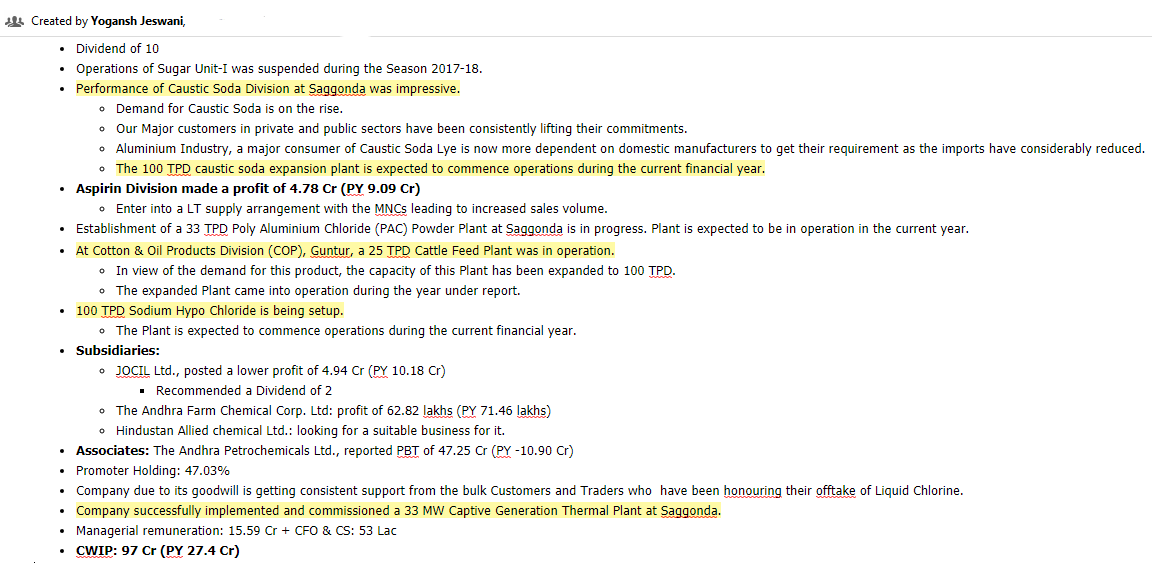

Outlook is positive as chemical division performance is expected to further improve in 2019 due to better realisations in caustic soda along with likely decline in power costs.

Losses from Sugar division are expected to significantly reduce (51 Cr loss in 2018). Co has inventory at 26,650 per MT but due to Govt support and price improvement the co should report inventory gains

Co is financially robust. They have undertaken expansion of Caustic Soda capacity by 100 TPD at a cost of 80 Cr from internal accruals.

ASL has significant integration of operations and hence the efficiency

Prepaid term loan of 93 Cr

3 Likes

Caustic Soda prices have actually moved down a little, whereas chlorine prices have moved up from Negative realisations to positive.

1 Like

Was listening to the concall of Transformer and rectifier india limited where it was mentioned that the caustic soda industry in China is currently in complete shutdown hence the demand by the chemical companies in India for the transformers is rising as they increase production due to demand. Good sign for all caustic soda companies.

Disc:Invested

1 Like

HI…the stock has corrected substantially since your update… Are there any headwinds due to present economic situation like rupee depreciation and / or threat of imports…

In my viewe the present situation should be a good tailwind for AS … or any threats ?

Dear Yogansh,

How is the present market conditions for Andhra sugars products. To the best of my knowledge most product prices especially caustic soda , sulphuric acid etc have better realisations YOY. Also Andhra Petro ( 33% stake) is going great and may report best ever results…

Any insights why the stock has corrected so much and is near 52 week lows ?

Hi @vskr63

Caustic soda is performing well currently but is a cyclical commodity and the current cycle has been going on for a long period now, it would be tough to call its peak. On the sugar front company has reported huge losses in the past but with some improvement in pricing the losses should get arrested and the segment might not cause a drag on the overall profitability. Also, as you rightly pointed out Andhra Petro has been doing well in recent past and let’s hope it continues to do so. Finally, w.r.t to your query on share price correction, overall mid-cap stocks have seen similar extent of fall and I personally don’t have any specific comments/insights on the issue.

Regards,

Yogansh Jeswani

Disclosure: Invested

Thanks Yogansh for sharing your views.

I am invested in this company since many years and off late i see certain metrics pointing towards more consistent performance than before. Over the past 4 / 5 years the through consistent efforts the management directed the company to become more or less self sufficient in power, invested most cash flows back to increase capacities, stopped unviable operations, added new products and these steps are significant to mitigate the cyclical nature of the commodity business.

I feel that Andhra Sugars is in line to achieve consistent cash flows in excess of 200 crores in FY 19 and beyond.

The next quarter results may provide a good hint of what is in store for future.

1 Like

any insights… The Q2 has been consistent with Q1 and this year EBIDTA is on course to be 20 % above last year.barring unforeseen circumstances…