where can i check the caustic soda price in indian market on daily/weekly basis trends ?

Q1 results are out. Results are good keeping in mind covid impact and lockdown.

Gross margins are down due to higher contribution from sugar and lower caustic prices.However OPM has improved from 16.5 in Q4 to 19.3 in Q1 due to better cost control.

Segment wise, Sugar losses has increased.

EBIT Margins in caustic soda have dropped to 17% from 27 % in last quarter. this is mainly due to fall in caustic prices.landed cost of caustic soda has dropped to 250-280 $ FOB.Domestic prices have fallen even more due to excess capacity.

Power segment has nearly doubled and industrial chemicals has tripled margins as compared to last quarter.

Negatives:

next 1-2 quarters may be weak for the company as caustic soda prices are on a downtend. Overcapacity and less demand from end user like paper and textile industry is likely to weigh in on caustic soda prices.

Positives:

no fresh capex in caustic soda by any big player.Both DCM sriram and grasim have put a hold on capex for a time being.

Hold of operation at tanuka sugar plant to aid margins.

Disc: invested at an average price of 279.

4 Likes

Came across andhra sugars via a filter in screener. Their financials for a company in a cyclical commodity industry are sound. Their low dependance on sugar and high priority on chemicals is good. Dividend payout is fantastic. PE is currently just under 5 PE. however, was looking for a growth driver to help break its previous ceiling of 10 PE and found this in their latest annual report:

-

“Your company is setting up a project at J.N.Pharmacity, Parawada, Visakhapatnam in non-sez area to manufacture

100 TPD Sodium Hypochlorite. The estimated project cost is about Rs.10 crores. The important raw materials

required are Sodium Hydroxide and Chlorine gas, which can be supplied from our Chemicals Division, Saggonda.

Sodium Hypochlorite has its applications in Bulk drugs / Pharmaceuticals, Fine chemicals, Water treatment and

Sea food industries. Most of the civil construction works are completed. All the bought-out components required

for this project have already been procured. Fabrication of all the process equipments and main storage tanks

are completed. Fabrication and erection of pipe racks / bridges are also completed. Erection of process equipment

is in progress. It is expected to complete the project by the end of December, 20” -

Theyve also expanded caustic soda capacity to 500 TPD

-

“Keeping in view the need for your Company to expand the base of its Chlor-Alkali operations an application to

the concerned authorities has been made for establishment of Plants at J.N.Pharmacity, Parawada, Visakhapatnam

for 245 TPD Caustic Soda, 50 TPD Caustic Potash, 600 TPD Hydrochloric Acid, 300 TPD Sulphuric Acid and

200 TPD Chlorine.

To meet the International customers’ requirement, capacity of Aspirin Plant has been expanded to 2000 TPA

from 1000 TPA.”

Almost all of the above look like they follow some backward integration and use their own power so operating margins look like they’ll be pretty high. however considering demand is cyclical I’m not sure how to interpret the above and where in the curve we are currently. Considering the price, low valuations, high dividend payout and these potential growth drivers I can’t see much downside. However, I am new to the company and so am still in the process of discovery. Hoping this post renews discussion from the esteemed members here since I don’t really understand the growth drivers too well since most of the products are alien to me so I can’t tell if the above warrants a re rating in the future

Disc: Studying. Not invested

7 Likes

The more time I spend researching andhra sugar the more it reminds me of one of my favorite companies : Deepak Nitrite. Slave to commodities and cycles so it’s a company on the lookout for diversification and secularity of income. Backward integration allows increase in operating margins. They use byproducts of their products to create new products which shows nimble management and great chemistry skills. Addition of products like sodium hypochlorite shows that management isn’t averse to jumping on trends smartly(using their own products and byproducts to create it). Deepak did the same thing… and slowly managed to counter cyclicality by just continuously adding huge volume of cyclical products they produced and by maintaining good margins and look where we are now with deepak. This looks like it’s happening here too but with better margins and infact they have higher profits than deepak last year and look at where deepak is this year. I dunno if I have recency bias but I can see a similar inflection point happening here as I saw there especially with sugar, caustic soda etc forming and explosive cylical base aspirin offering stability and now bleach/other chemicals providing growth. I dunno if I’m imagining this. But I can’t get it out of my head and wanted to run it by the previous owners and members in this thread to check if I’ve got my thesis correct? I am not saying this is another deepak nitrite. They just have very similar stories. After pouring through thr AR I’m honestly shocked that it’s valued at just 4 times earnings and I’m sure there’s something huge I am missing @ayushmit . I could really use your help here. Sorry for disturbing you

6 Likes

Hi @Malkd - yes, Andhra Sugar seems to be a very well managed company and pretty well integrated. Despite the big fall in end product prices of caustic soda by almost 40-50%, the recent quarters haven’t been that bad. I have been positively surprised to see the margins in recent quarters. The positive surprise was the liberal dividend of Rs 20 per share given by the company in around March 20.

Have been invested for last few years but sadly the stock has seen de-rating in valuations. Few possible reasons - 1. it has 2-3 segments and sugar has been a big drag for them 2.its been a dull company zero interaction with investors/analysts (and growth too).

8 Likes

And also not listed on BSE. Getting any informatjon from NSE big task. Even disclosure are difficult to get. While BSE may not have volume but website is quite good in my opinion. Further, the company long track record of dividend payment. The consolidated results also include part of Jocil which had good Q1 due to soap and detergent segment where is operate.

6 Likes

Thanks ayush and dd1474… think il just leave it on the watchlist then. Lack of concalls/commentary and difficulty in getting information makes it too difficult to track and considering I’d only be putting a small amount of capital it doesn’t seem worth the trouble. May look again if there’s a technical breakout (52 week/all time highs etc). Cheers.

1 Like

Only very few companies are conducting AGM through physical mode without providing additional facility of VC. Andhra Sugars is one among that. Really disappointed to see from the notice that the AGM is scheduled today at 3 pm through physical mode at Tanuku (Registered Office) without VC facility. In this pandemic situation, considering the size of the company and the area of business they operate, they should have provided the facility of VC also so that all the members can participate in corporate democracy. I feel management is not valueing shareholders. This is one classic example. Also many times it is observed that the company is not giving timely disclosures to BSE. They give disclosures to NSE only. As far as Q1 2021 results are concerned, they have published it on NSE only. Still it is not published in BSE. This is not acceptable.Request all value pickr forum members who are tracking this company to write a mail to CS of Andhra Sugars expressing the strong disappointment.

4 Likes

Andhra Sugars is actually a chemicals co. It has in 2020 closed 2 of 3 sugar units. Third unit does breakeven. If i eliminate sugar losses of the past then chemicals business is very profitable and surprising more stable than what one expects from a caustic soda/chlorine derivatives play. Reasons are approx 50% chlorine is used in captive. Also we may at be a new dawn for this sector as this is the third year that chlorine prices are positive, so possible that new profitability metric is higher than historical median (though lower than fy18 and fy19 which were a caustic soda cycle). Vals and b/s reassuring. There are growth plans too. And ADD investigation on caustic soda offers additional comfort.

4 Likes

Hi All,

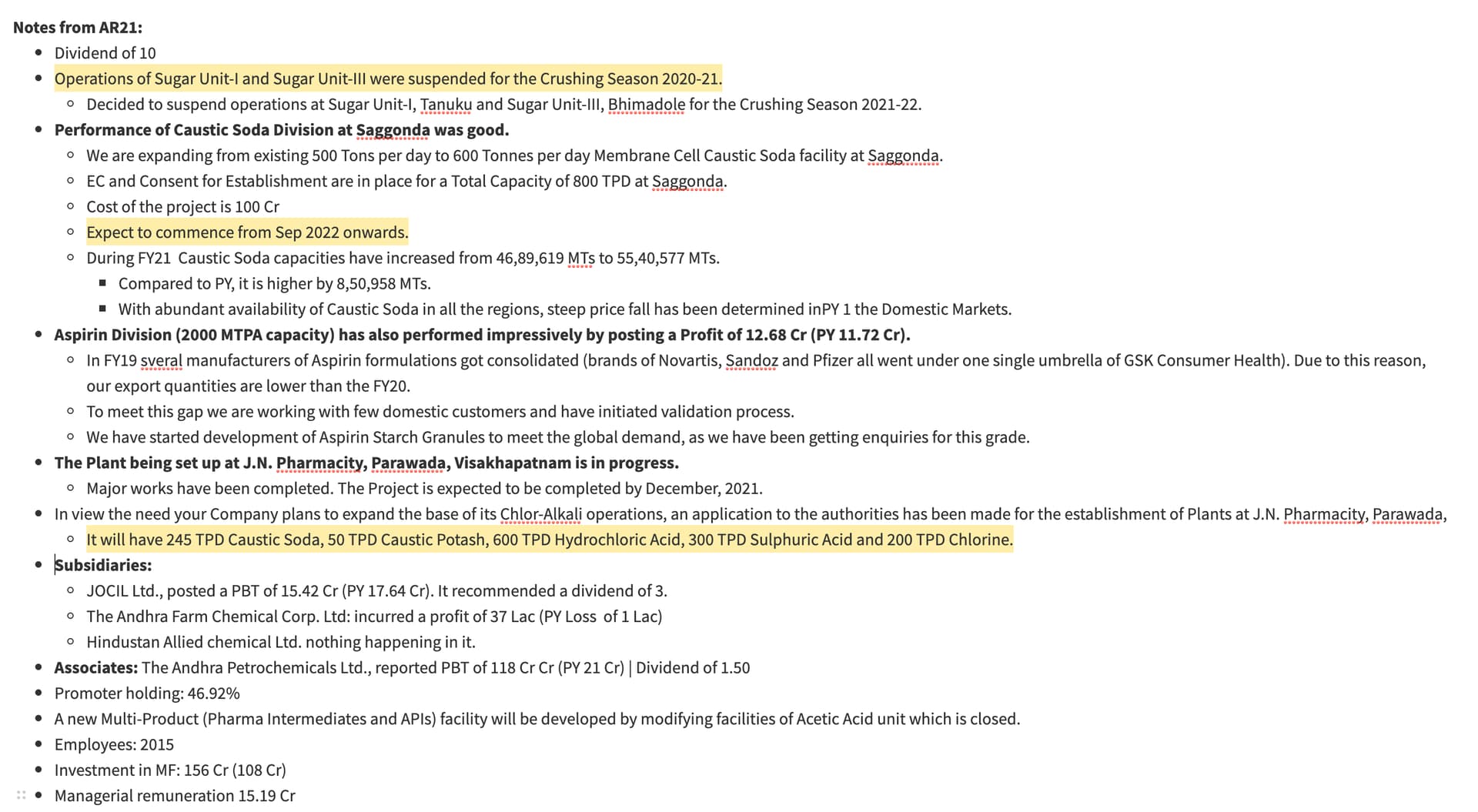

Sharing my notes from AR21. Key takeaway is that company has been able to increase its Caustic soda capacity by 100 TPD in FY20 and has further plans to add 100 TPD at Saggonda unit by mid of FY22 and the long term plan is to build an integrated complex at JN Pharmacity with 245 TPD cautic soda and several other products & by-products.

Though the prices of caustic soda were under pressure for last year…things have improved considerably now and prices are much higher and have even gone beyond their previous highs of 2017 (This is not part of Andhra’s AR but is my understanding by tracking other industry players).

Hope this helps!

Regards,

Yogansh Jeswani

Disclosure: Invested

2 Likes

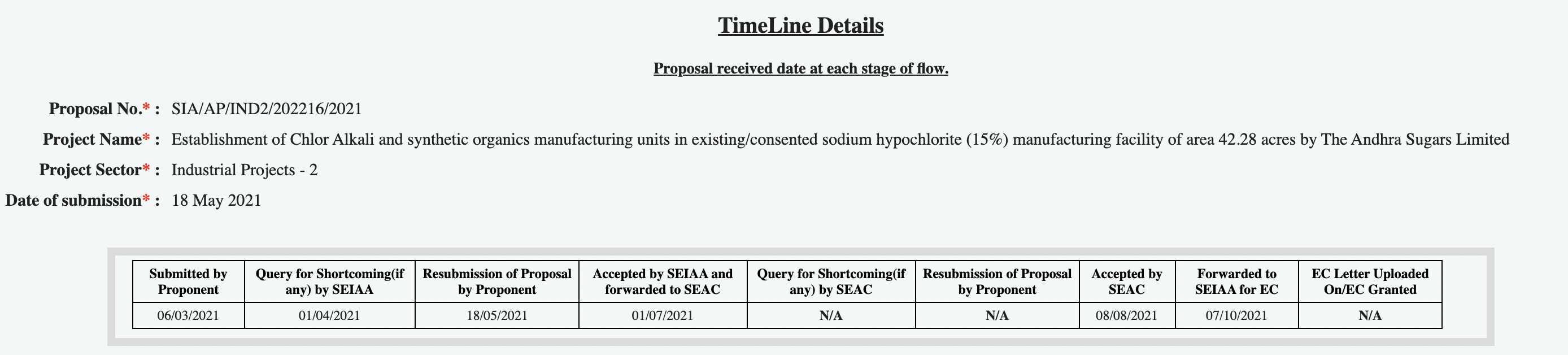

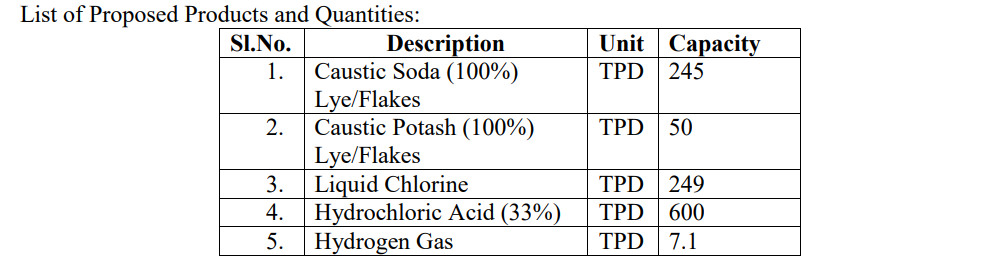

Sharing a quick update on the progress of the EC filing for the Chlor-Alkali operations planned by the company at JN Pharmacity.

As highlighted in the AR21 as well, this unit will have 245 TPD Caustic Soda, 50 TPD Caustic Potash, 600 TPD Hydrochloric Acid, 300 TPD Sulphuric Acid and 200 TPD Chlorine.

The cost of this project is 300 Cr

Company’s file for this project has progressed further and in Oct 2021 was forwarded to SEIAA for EC approval (please see below image)

However, additional details have been sought from the company and grant of EC will be dependent on the response/action needed for the same (please see below image).

These things may or may not take time…so one will have to wait and watch the developments.

Regards,

Yogansh Jeswani

Disclosure: Invested

6 Likes

Stock split 5:1

Sugar division posts profit on inventory gain and export incentive. Chemicals business should ideally reflect caustic buoyancy from Q3 (like grasim). 33% Andhra Petro continues to add cash in super-cycle.

Andhra Sugars 10 year roe is 12% and 5 year roe is 14%. Like most manufacturing cos outlook might be brighter. Risk-reward favourable.

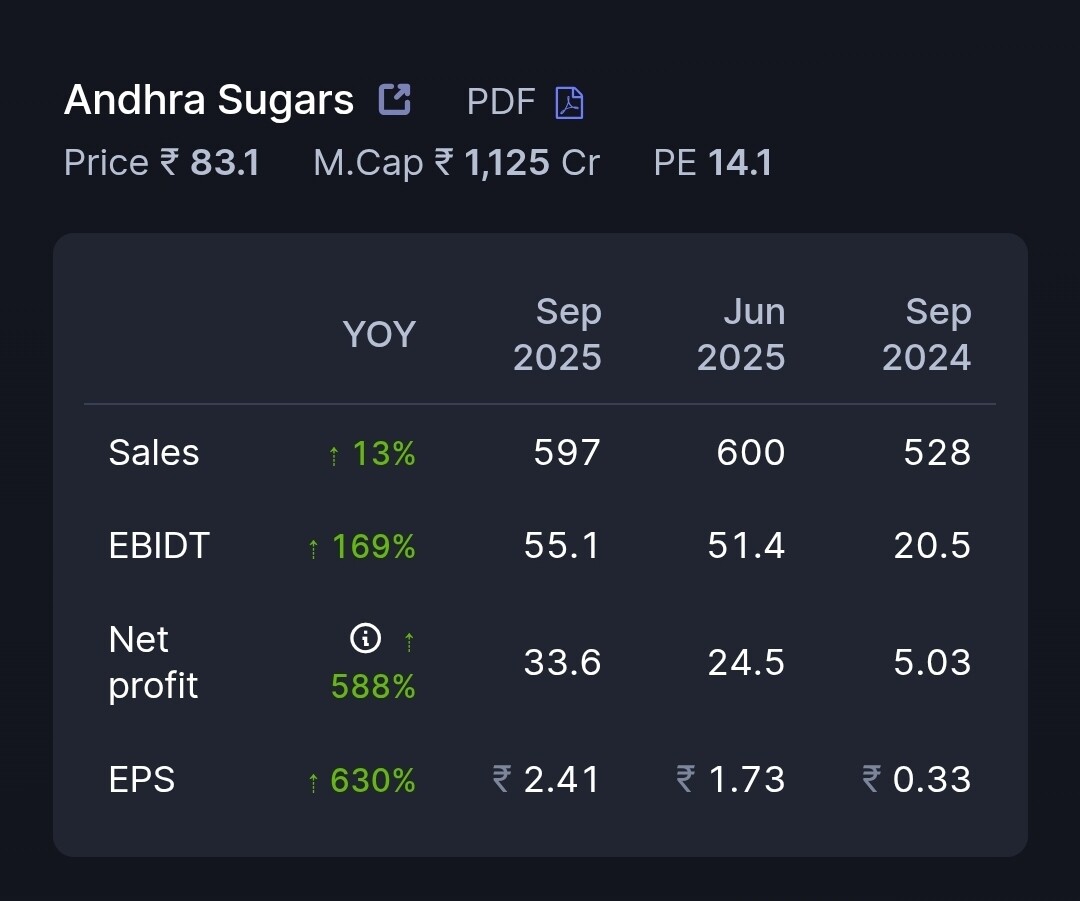

Andhra Sugar Q2 results

3 Likes

Yesterday on 27th May, 2022 Andhra Sugars got EC Approval for Establishment of Chlor Alkali and synthetic organics manufacturing units in existing/consented sodium hypochlorite (15%) manufacturing facility of area 42.28 acres.

The total cost of the project is Rs.300.0 Crores.

3 Likes

Feedback about Andhra sugars from my father who use to supply them lime stone related stuff few decades back: Many of the sugar mills employees use to take money and let low quality material get into their factory. But Andhra sugars employees was always stringent with quality parameters and didnt allow bad quality material into their factory. He has no idea about current situation though…A company paying dividend consistently since decades definitely should be doing something right consistently.

Disclosure : Have not studied the company in detail barring the information from this thread.

2 Likes

this is not a Sugar company. Sugar revenue is not even in double digit as a percentage.

This is essentially a chemical company.

6 Likes