Recent errection and commissioning of 33MW power plant was done by thyssenkrupp which met andhra sugar management commitment for Mar’31

Thanks @yogansh for starting the thread. The thread elicited my interest to do some work on the company.

Thanks @rohitbalakrish_ for working on getting segment wise result. That was a big effort and very helpful in understanding the story.

Some notes -

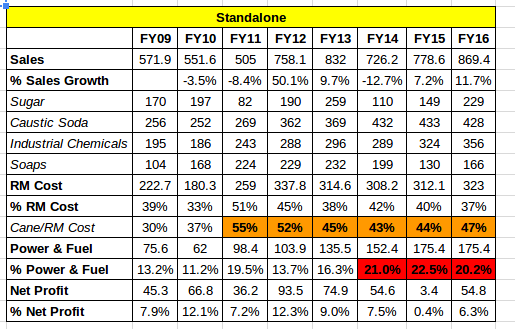

On Standalone basis, the power cost had become 20%+ of the total cost and 33MW plant shall definitely improve their margins for the long term.

There is structural problem in the sugar industry where cane prices are procured at fixed price which is revised upwards every year whereas sugar price is market linked.

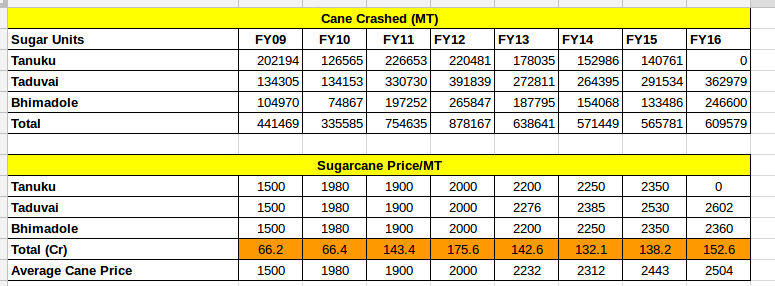

As can be seen above cane now account for almost 50% of RM costs. The tables below show that cane price has increased every single year since FY10 and their cost.

Another obvious observation is - company does well when sales increases and when sugar business does well. But every few years sugar business takes the byte out of profit. For long term valuation, shall we consider bad sugar year business as base to have margin of safety?

Some other data points -

I am not fully convinced that wind power business shall be seen together caustic soda business. The in-houser power generated from Taduvai + 33MW power business can be clubbed with caustic soda business.

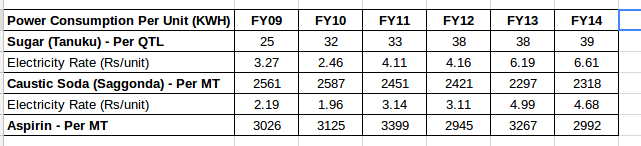

Till FY14, company used to 1) number of electricity units per unit of products and 2) per unit cost of electricity for various products. For sugar and caustic soda, electricity rate were indeed inching up high. Would be very interested to calculate electricity rate after 33MW plant.

In FY16 AR, company flagged that power cost is low in China and Gulf and caustic soda is dumped in India. It seems like there is very little entry barrier for these products and it is intriguing that company has a very stable Caustic soda business. What is the secret there?

In summary, there are three short term triggers for the company namely -

- 33MW power plant leading to margin expansion

- Caustic soda capacity expansion to 600 TPD and expansions in industrial chemical business

- Low institutional holdings

There is a long term possibility that - the business might move to higher orbit (niche products, products with high entry barriers etc.) if management can demonstrate some resourcefulness and skills. I would be watching for any signs of this transformation.

The negatives are usual suspects - structural problem in sugar industry, government regulation, run-of-the-mill chemical products etc.

Regards,

Rupesh

Disc - No investments yet.

Hi @rupeshtatiya,

Good work. It’s good that you have put the power cost in excel. While reading the annual reports it was clear that the margins of their core business of caustic soda is getting affected and the margins were falling gradually (from 25% to 20%). There was a huge power problem in the south over the last few years and hence the new power plant should really help the company. I also think that with the improving power situation and coming down of tariffs, the co can benefit in coming times and plan expansions.

Their sugar operations may continue to face problem due to falling sugar acreage in South. It seems they are not operating one of their sugar Mills.

Since Caustic Soda business is so important in investment thesis, I decided to spend some time trying to get industry picture and status of competition. Following are some notes →

As per AMAI, total installed Caustic Soda capacity on 31 Mar 2016 was 33.7L MTPA and production was at 28.71L MTPA. Imports were at 5.67L MT - an increase of 12%, exports were at 1.1L MT.

Source: http://ama-india.org/industry-data/caustic-soda/

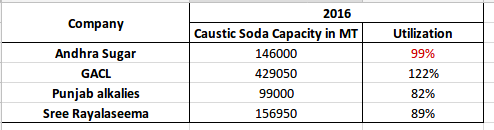

@yogansh has done some good work to list out capacity of peers in is excel sheet. Just pasting the data here →

For the company to do well, two or three things will have to happen.

First, the end usage industry for Caustic Soda has to increase.

Second, the domestic industry has to be competitive so that products are not imported.

Third, since the cost of transportation can be high - there either has to be large demand not very far away from company or some economical mode of transport has to be worked out.

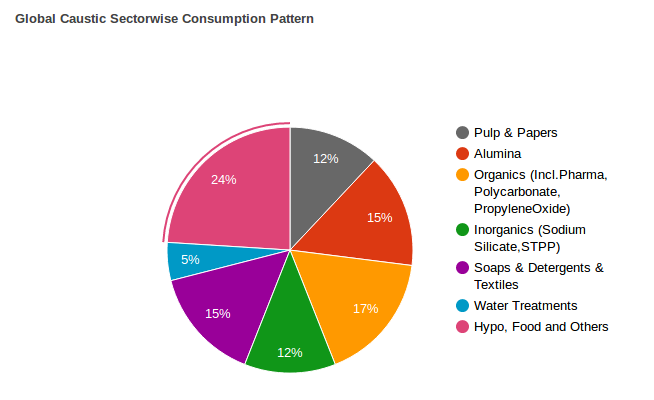

The sector wise consumption pattern of caustic soda as per AMAI is as follows →

Please note that these are Global patterns.

The competitiveness of Caustic Soda players remain on several factors - the most important of them are optimum usage of by-products and cost of power.

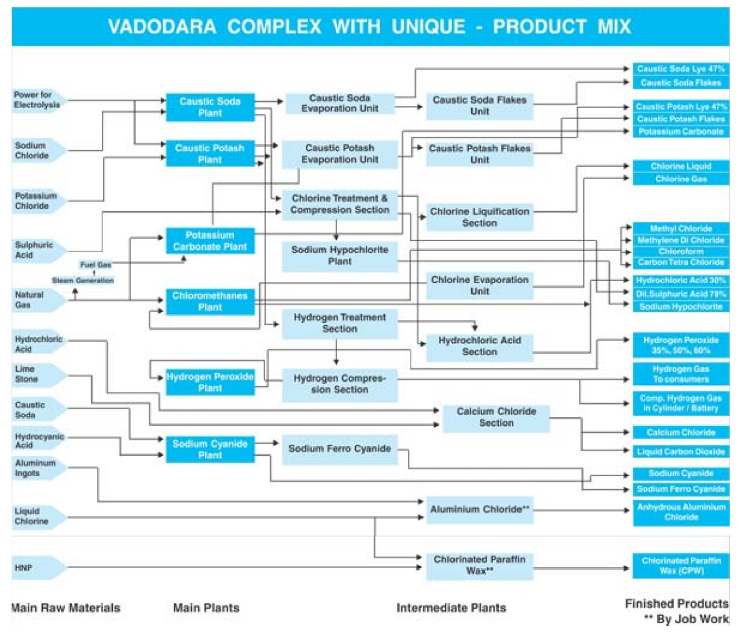

GACL seems to be biggest player in India and following diagram from GACL AR gives some idea about how by-products can be used.

I see that Andhra Sugars do not have any Choloromethanes plant and GACL and Sree Rayalseema seem to be having them. This might be one avenue to further increase usage of Chlorine.

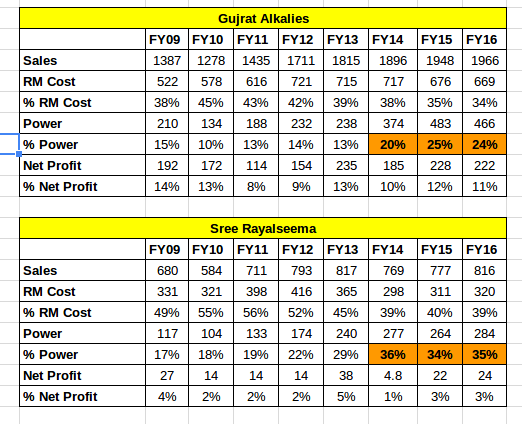

The power cost seem to be the issue across the industry and all of them are looking for cheaper power by installing captive power plants. Following are numbers for GACL and Sree Rayalseema.

Following are some notes on cursory reading of AR of GACL and Sree Rayalseema.

Gujarat Alkalies

AR FY16

Industry leader in Caustic Soda, Stable outlook

14% share of domestic Chlor-Alkali market

POWER SCENARIO

- 90MW gas based Captive co-generation power plant

- Participation in 145MW Joint Captive Gas Based power plant of GIPCL

- 31 MW Wind Farm commissioned - Rajkot, Gujarat

- Total installed Wind Energy Generation Capacity - 156MW

- Plan to setup another 15MW Wind Farm.

- Plan to setup 15MW Solar Power Plant to fulfill statutory requirement of Renewable Purchase Obligation

CAUSTIC SODA CAPACITY

- Caustic Soda - installed capacity - 429050 MT

- Plan to setup 800 TPD Caustic Soda Plant & 100-120 MW coal based power plant at Dahej in JV with NALCO

- Plan to increase production of caustic soda from 785 TPD to 1000 TPD at Dahej

Import/Dumping Threat

- The price of caustic soda remained under pressure due to huge imports during most part of FY16.

- Industry faces competition from cheaper imports with reduction in customs duty. Anti-dumping duty imposed on imports of Caustic Soda Lye/Flakes & Potassium Carbonate.

- Imported 8750MT of Caustic Soda Lye and traded

Eastern Market

- Supplied 11000 MT to NALCO, Orissa

- Transportation remains a major cost in distant markets - Used Rail/Sea for bulk movement

- Plan to stock products at some strategic locations. 1100 MT Caustic Soda Lye supplied to Nagpur branch.

Sree Rayalseema

AR FY16

- Company commissioned chloromethanes project where chlorine is captively used. This is also one product option for Andhra Sugars.

- Due to reforms of government, electricity availability is not an issue but cost is still an worrying factor.

AR FY14

- Unseasonal rains have affected salt availability resulting in increase in RM costs

Regards,

Rupesh

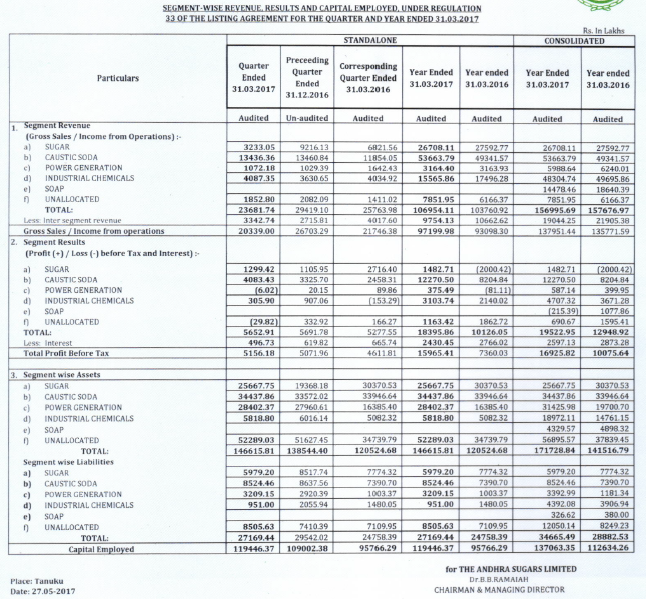

March 2017 Results fromm NSE

Andhra Sugar March 31 2017 Results.pdf (2.4 MB)

Thank you Dhiraj bhai. These look to be very interesting set of results.

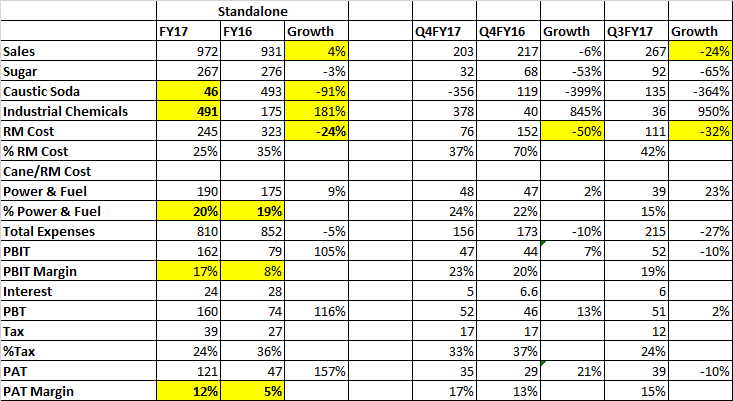

SOME OBSERVATIONS

-

For FY17, RM cost went down from 35% of sales to 25% sales. This cost reduction has resulted in massive margin expansion as PBIT and PAT margins have more than doubled.

-

The top line growth has been tepid for full year at 4% and there is de-growth on QoQ and YoY basis for Q4FY17. Maybe reduction is RM cost has resulted in reduction in the price of final product as well.

-

There seems to be some re-classification of revenue between Caustic Soda (CS) and Industrial Chemicals (IC) as can be seen from above results. The important thing to notice is revenue of CS+IC together has reduced to 537Cr in FY17 from 668Cr in FY16. What happened here?

-

The power and fuel cost remained constant at 20%. This might be expected as 33MW plant got synchronized to grid in Apr as per company’s notice to BSE. Another angle here is - if volume of products has grown but selling price has reduced, then constant cost of power is actually efficiency improvement.

-

LT Debt of the company increased from 154Cr to 232Cr. I hope these will be brought down in coming quarters due to such good results in FY17.

Regards,

Rupesh

Find enclosed revised financials from the website of the company.

I am more curious to understand major drop in EBIT margin of Industrial chemical in Q4FY17 as compared with Q3FY17. All other aspects, particularly, performance of Caustic Soda, continues to remain encouraging.

Hello @rupeshtatiya

need your help in analyzing the current prices of caustic soda. Can you please advise where can i find month wise price of caustic soda from April 2016.

Please anyone else if you have any idea kindly share

I wanted to understand its impact on coming results of andra sugar. Kindly share some insights

What is positive is the dividend payout of the company is consistently very high. For FY 17, they have proposed of dividend of Rs. 10 (equal to FV), roughly 3% dividend yield at current price . P/E of 7-8 looks attractive but we would need to monitor the performance of chemical division and sugar prices. Looks interesting. Just added a tracking position.

Disc: Invested

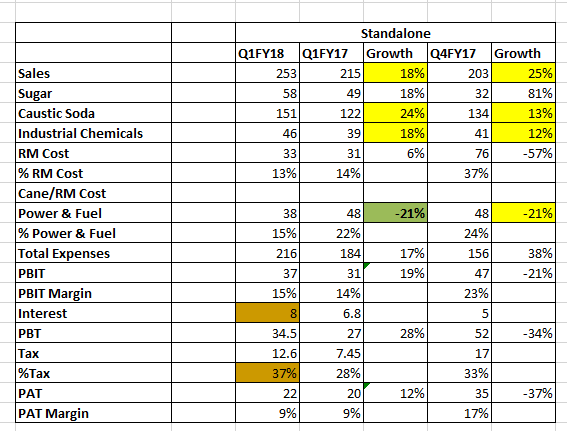

Andhra Sugars Q1 FY18 Results →

Segment PBIT →

- Sales and PBIT growth in caustic soda and industrial chemicals remains encouraging.

- Sugar dragged the results of the company down in Q1 FY18

- Higher tax and interest outgo suppressed the PAT.

- Good to see savings of ~10 Cr per quarter in power numbers in both QoQ and YoY numbers, hope to see similar saving on annualized basis

- Change in inventory in Q1 FY18 is at 72Cr. Would be interesting to understand this number.

Disc - Invested

Found some interesting industry data while going through another company’s AR. It is useful for forum members who are looking to understand the Chlor-Alkali industry.

Sharing the key points below (emphasis mine):

The Asia-Pacific region was the world’s largest market for ChlorAlkali products in 2013 and is expected to be till 2019. China is the key consumer of Chlorine, Caustic Soda and Soda Ash in Asia-Pacific whereas India is expected to be the fastest growing market of ChlorAlkali in Asia-Pacific as well as the World.(Source:MarketsandMarkets)

The market for Chlor Alkali in India is projected to grow at a CAGR of ~7% during 2014-19. The market is broadly categorized into three segments, namely:

-Caustic Soda

-Chlorine

-Soda Ash

Caustic Soda and Chlorine are the basic building blocks of economy. Caustic demand relates to manufacturing activities and chlorine relates to infrastructure / construction activities. (Source:TechSci Research)

Caustic Soda finds major application in diverse industries, such as soap & detergents, pulp & paper and textile processing CPW (Chloro Paraffin Waxin). Chlorine is produced as a co-product during Caustic Soda production and is widely used during PVC manufacturing, Alumining, Dyes & Dyes intermediates, various Oraganic and Inorganic Chemicals. drinking water disinfection and pharmaceutical production. Soda Ash is used mainly during glass, soap & detergent and silicate production.

Caustic Soda and Chlorine are produced together in the ratio of 1:0.88 through electrolysis of salt, whereas, Soda Ash is produced using a different process.

On account of their co-production, the market dynamics for Caustic Soda and Chlorine are heavily influenced by each other. In India, it is influenced by Caustic Soda. The major input cost in Chlor Alkali industry is power and salt. In case of Caustic Soda, power constitutes more than 60% of the cost of production.

In India, there are 35 manufacturers of Caustic Soda with Gujarat being the largest Caustic Soda producing state.However, the installed capacity in India is much lower than China. Currently, the world production of Caustic Soda is 80 million MTPA while India’s capacity is merely 3.5 million tonnes i.e. ~4% of the world capacity, while china has a capacity of 28 mn tonnes i.e 35% of the world capacity. Similarly, Soda Ash capacity of the world is 55 million tonnes. China and US are the biggest producing countries accounting for 40% and 20.5% of total global Soda Ash capacity respectively, while India’s capacity is only 3.2 million tonnes. (Source: AMAI)

Regards,

Yogansh Jeswani

Disclosure: Invested

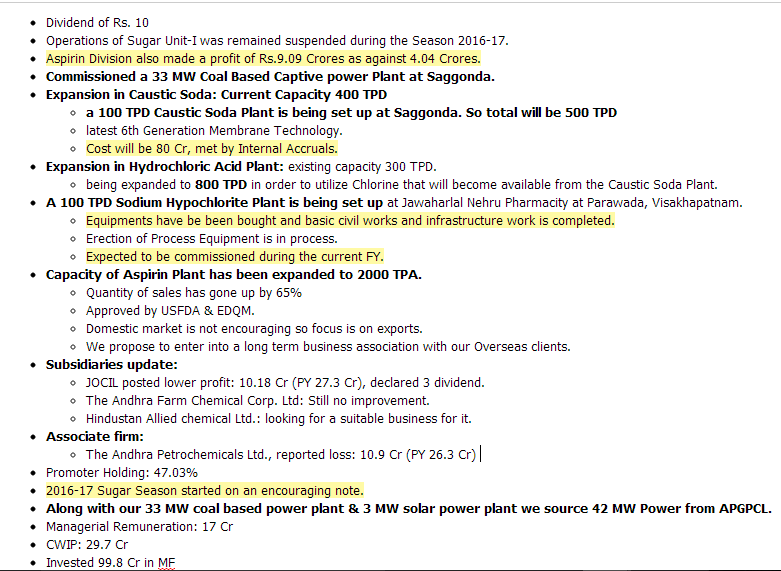

Sharing my notes from AR17. There were several developments in FY17.

Regards,

Yogansh Jeswani

Disclosure: Invested

The most interesting thing to look out for will be increase in earnings due to less power and fuel expense in current year 2017-18

Caustic soda prices have surged in past few months if we go by the below price chart. However, this chart looks to be depicting local Chinese market price. It would be far greater helpful if we can affirm that a similar price trend is prevalent in India too.

My sense is Caustic soda being a commodity should mirror the global price trend and given the higher power cost in India + ADD, the realization can be even higher in domestic market.

Views Invited.

Regards,

Yogansh Jeswani

Another link below, says Asia prices have surged 18-22% in CY17. But I have seen similar data for US/EU as well, will find and share.

DCM Shriram Ltd is another major player in Caustic Soda. I own it for many years now. They are excellent capital allocators, amazing turnaround in last five years.

Has anyone done work comparing Caustic Soda businesses of Andhra Sugar vs DCM Shriram? Would be interesting…

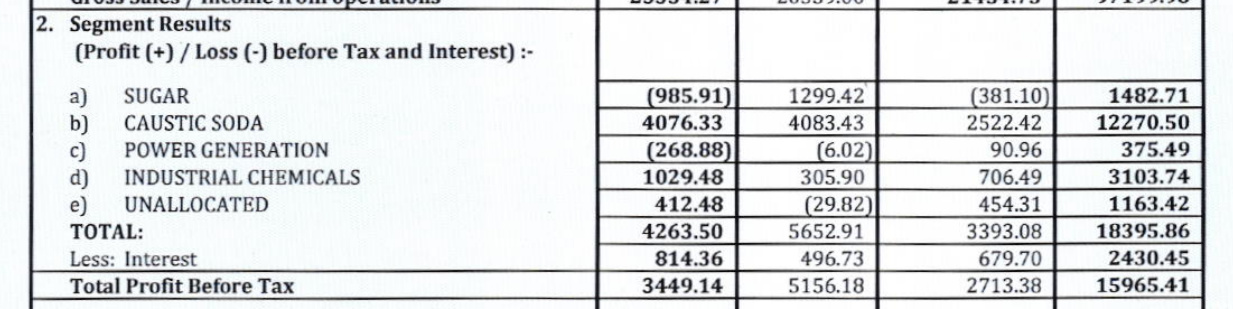

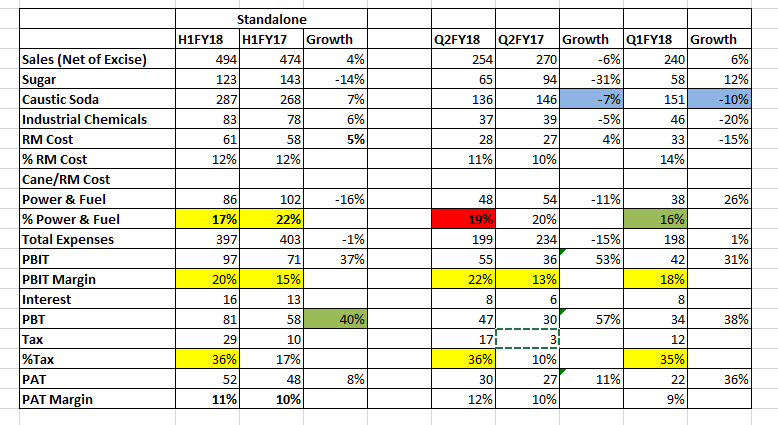

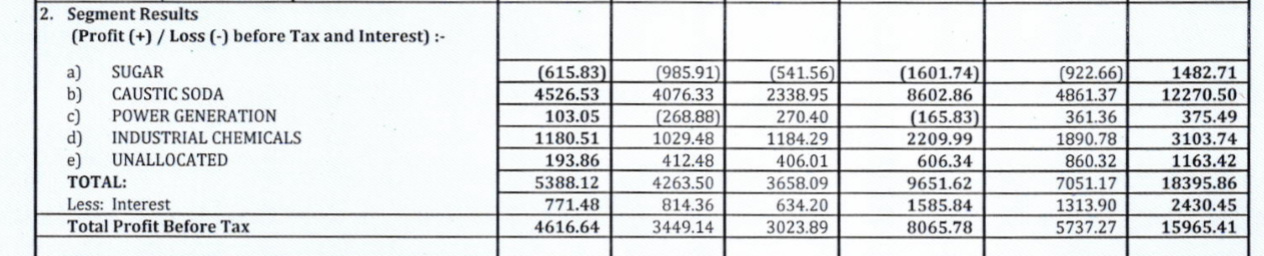

Andhra Sugar Q2FY18 Results →

Source → https://nseindia.com/corporate/stockexchange_28102017125408.zip

Segment Results →

Few Observations →

- On half year basis, there was 5% improvement in power & fuel cost which directly flew into the PBIT.

- In Q2FY18, power costs have gone up to 19% compared to 16% in Q1 FY18. This might be due to rising coal costs.

- On half year basis, there was 40% increase in PBT but it did not flow into PAT as tax rate went up from 17% to 36%.

- Although numbers tell that there was a degrowth in Q2FY18 on QoQ and YoY basis in Caustic Soda revenue, but the number are not strictly comparable. Q2FY18 numbers might be net of excise duty due to GST where as Q1FY18 and Q2FY17 numbers are not.

- Sugar business continues to make losses due to sugarcane scarcity in southern states. The company has shut down one unit an Tanuku due to nonviable operations.

Source - https://nseindia.com/corporate/crushing_28102017125910_827.zip

Disc - Invested

@rupeshtatiya @ayushmit @yogansh @rohitbalakrish_

I came accorss one article from web about Tata Motor launch fuel cell bus based on ISRO technology.

The first link talk about MOU and functioning of new technology between Tata Motor and ISRO. While I am not technical person, reading from this article, I understand that technology provided by ISRO used liquid hyderogen handling in which ISRO has expertise.

https://economictimes.indiatimes.com/slideshows/auto/isro-tata-motors-develop-indias-first-fuel-cell-bus/slideshow/21545957.cms

In Jan 2017, the vehicle is launched.

I also understand from enclosed link that Andhra Suagar is major supplier of Liquid hydrogen used by ISRO as Fuel for Rocket.

Being layman, do not understand whether the technology used by Andhra Suagar has any role in Liquid Hydrogen based Fuel Cell/Bus developed by ISRO. Hence, would appreciate if any expert can provide some insight into same.

Thanks in advance.

Discl: I hold shares of Andhra Sugar and my view may be biased. Investors are advised to do their own due diligence before taking any decision.

The company is launching a new product ‘Poly Aluminium Chloride’ from Feb 2018 as per their website. However, they haven’t guide on quantity and price. But, definitely a good sign as ASL is looking at value added products. Yet to study the demand/supply of the new launch.

Poly Aluminium Chloride is used in deodorants and in water purification process. Aditya Birla Chemicals, and GACL etc are few other manufactures of the same.

https://theandhrasugars.com/new-product-launch-poly-aluminium-chloride/