While much of the discussions on this forum is focused on bottom up analysis of individual stocks we all agree that if the overall market has a good influence on price of a stock. In fact, after company’s own earnings, overall earnings growth of corporate India is IMO the most important indicator that drives the stock prices. We all keep hearing about Nifty earnings growth, earnings recovery etc but there is no definitive source of finding out aggregate earnings growth.

Calculating earning growth for a group of companies is not that difficult as we anyway track individual companies so we we just have to add up earnings of companies in a group to get earnings of the group.

I have made an attempt to calculate earnings growth for 3 broad group viz Large Cap, Mid Cap and Small Cap. I have used BSE Large Cap Index, BSE Mid Cap Index and BSE Small Cap Select Index to get a list of companies. Each index has about 60-75 companies with no overlap.

I have excluded very few companies from this list mainly if the reported earnings do not represent the underlying economics of the business (e.g. oil marketing companies like IOCL, MRPL, HPCL etc).

Here are the results

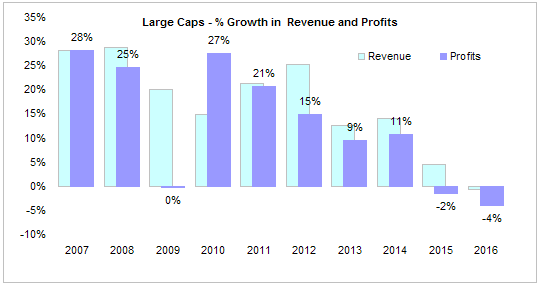

Large Cap - Annual Earnings and Revenue Growth

Source: Capitaline

During the boom years of 2004-2008, earnings grew at a phenomenal 25-30% per year. Financial crisis of 2008 put a break on the earnings growth and earnings did not grow in FY 2009. Govt responded with a stimulus package which boosted the earnings back to 27%. But it also unleashed high inflation of 2011-14 and earnings growth slowly dropped to -4% in FY2016. Part of the de-growth a result of huge losses reported by banks beginning Q3 of FY2015-16.

While the market started rallying in 2014-15 after election of the new government, earnings growth was actually rapidly slowing down. This could be the reason market gave up most of the gains of 2014-15 in 2015-16.

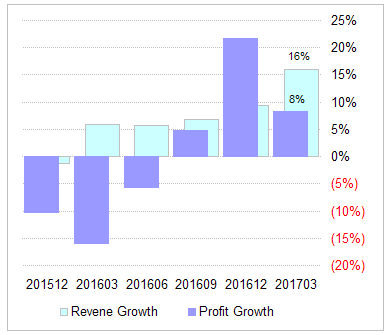

Large Caps - Quarterly Earnings and Revenue Growth

Source: Capitaline

As seen from this quarterly chart, earnings growth bottomed out in Q4 FY2015 and a patchy recovery began in 2015-16. As the earning recovery was gathering pace, RBI asked banks to perform stress tests of their portfolios and make additional provisions beginning Q3 FY16. This move resulted in earnings growth again going down to -5% in Q3 FY16. Over the next 4-6 quarters as banks made catch-up provisions, earnings growth resumed its upward move. Market however, largely ignored the bank earnings and instead focused on revenue growth and earnings growth excluding banks. Even the demonetization in Q3 FY17 does not appear to have any impact on the ongoing earnings recovery.

As we head into Q4 FY17 earnings season, we should see some better numbers even from banks as banks are largely done with their provisions. Recent rally in Nifty is largely on expectations of good earnings.

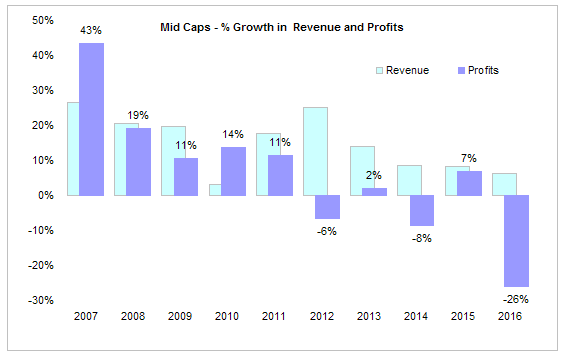

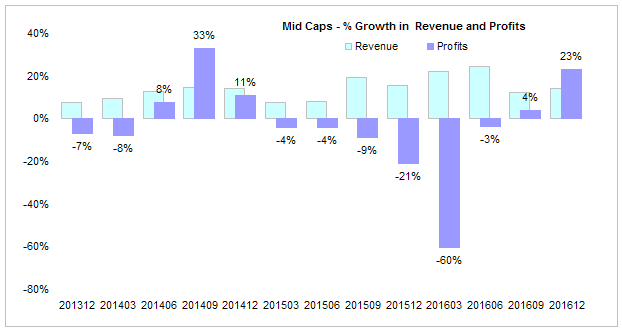

Mid Cap - Annual Earnings and Revenue Growth

Source: Capitaline

Mid caps did well along with large cap during the 2007-2011 period but could not sustain the earnings growth during the high inflation period of 2012-14.Although they were able to pass on higher input costs to customers, they had to absorb some of the costs resulting in lower earnings. Although Mid caps began earnings recovery sooner than large cap, many PSU banks in Mid Cap index reported huge losses in FY16 hence midcap index as a whole reported huge losses in FY16. Excluding these banks, Midcaps have done well in since FY15 and that can partly explain out performance of midcaps over last 2-3 years.

Mid Cap - Quarterly Earnings and Revenue Growth

Source: Capitaline

Quarterly earnings chart revel the huge losses reported by banks in Q3 & Q4 of FY16. Since then earnings have began to recover and Q4 of FY17 should see some good numbers.

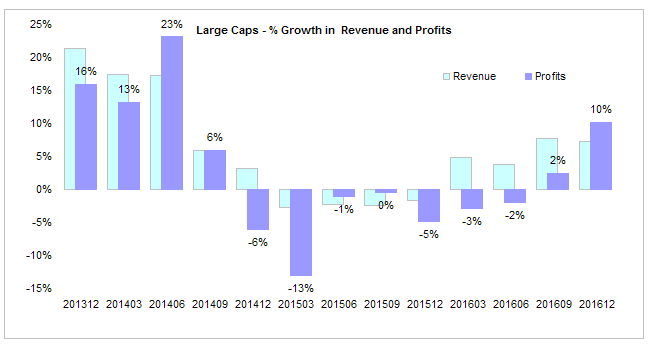

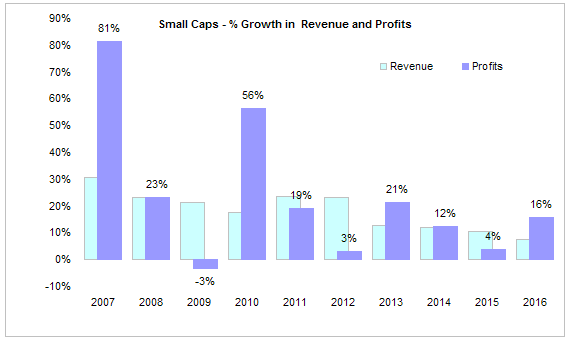

Small Cap - Annual Earnings and Revenue Growth

Source: Capitaline

Small caps have performed much better than mid large caps although the data set does have a survivorship bias. Since I took current members of BSE Small Cap Index and aggregated their earnings going back 10 years, only the good small caps have remained in this list. This kind of bias is most prominent in small caps than large and mid caps as current members of large cap index have been members of large cap index for much of the last 10 years.

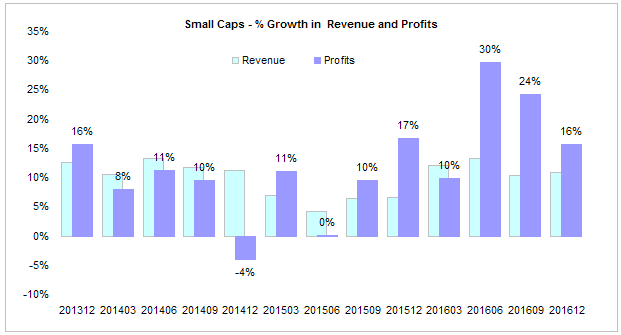

Small Cap - Quarterly Earnings and Revenue Growth

Source: Capitaline

Quarterly results also show that small caps have seen much better earnings recovery than mid and large caps. This is mainly because banks and commodity stocks are missing from this index. These stocks tend to be much larger in size so they are represented in mid and large cap indexes.

Overall I think earning recovery is well underway and we should see some good numbers in Q4 FY17. Its also the time of the year companies come up with annual forecasts (which analysts pick up and relay in their reports). If the commentary is good, it will add fuel to the fire.