I started reading up on this company in recent months and it seems to be an interesting case given the frenzy in the small/mid cap space. Few things which interested me are:

Reasonable valuations. When most of the things are trading at 25-30 PE, I was surprised to see a large branded consumer facing company available at about 12-15 PE

It seems the de-rating could have been due to risk of EV on the core business. However, few months back, Amara raja announced aggressive plans to foray into this segment. Though it needs to be seen if what will they do and what will be their edge.

Interestingly they already have created this new energy segment and are growing rapidly on a small base

They do intend to keep growing the lead battery business too and are targeting exports etc. They are also looking at data centres etc.

Risks - 1. EV foray - don’t know what will be their value proposition 2. Political risks

View on ARBL’s Lithium Play

My only problem with Amara Raja’s Lithium ion optionality is that they are not aggressive in building relationship with the OEMs / TIER-1s. The difference between a Lead acid battery and Lithium ion battery is that Lead acid batteries can be bought from anyone and fitted in your car. Lithium ion batteries cannot be treated that way. The vehicle level controller ( VCU - think of the brain of an EV ) needs to know details about the battery - State of charge, state of health , resistance buildup etc. The VCU is mostly designed and owned by the OEMs and they ultimately will build the system with 2-3 suppliers.

Using a non OEM authorized battery can cause hazard and this is where ARBL’s relationship with the OEM deteriorates.

Knowledge of making lead acid battery at scale is not transferrable to making Lithium ion battery.

Lead acid battery is very simple and can be done in cottage industries ( un-organized sector ) The VRLA batteries are a bit more complex. But since lead acid batteries rarely pose a fire risk OEMs and Customers will not be too worried about the batteries. The Lithium ion battery is completely opposite and not knowing the characteristics of the cells and the chemistry in it can cause fire hazard. The process of producing Lithium ion is complicated with heavy upfront capex and wafer thin margins. The requirement of clean rooms are also crucial. The manufacturer will also be impacted with the commodity price fluctuation of Lithium which has become geopolitical in nature

Large Chinese, Korean OEMs will partner with Indian business houses India a part of the global supply chain

My experience says that if the volumes of an OEM is large, they will design the battery around the vehicle. E.g. OLA would provide requirements to their battery supplier to make them a custom battery. If the volumes are low, the vehicle is designed around the battery. Many Indian startups who had imported the batteries from China had to also import compatible, BMS, Motor with them ( this is why they were not able to keep the proportion of the indigenous components level to less than 40% ). My question is what stops a CATL, Panasonic to form JV with a non automotive business house flush with cash to set up a shop to serve the fragmented market.

Jindal for example will partner with LG. Tata, Mahindra’s might have similar partnership. Globally Mercedes has partnered with CATL

Silver Lining

What might act as a good trigger for me is that if ARBL is able to absorb LOG 9 within itself as I see LOG9 aggressively partnering with 3W and 2W startups. Maybe LOG9 will be able to supply a 2W and 3W powertrain on which EV startups can build their vehicles.

Yes, what you are saying is correct and the concern. EV battery is expensive and a large part of the vehicle and hence OEMs would like to keep it in-house or have strong control. So don’t know how Amara Raja will be able to grow in this but perhaps at these valuations, I would like to have some exposure and watch…I’m not paying for growth…and a company like this with investments to be made from internal/past cash flows, they are usually sane about the investments they make…they won’t make a large investment just for the sake of it. If one observes, they have created a large R&D setup and team to work on these areas and decide how they want to go ahead.

So let’s see how it evolves.

Also there is a large difference in valuations of Exide vs Amara Raja while story is similar

We need to differentiate between cells and battery packs. While some OEMs may keep battery packs in-house, very few OEMs go backward to make their own cells. The value proposition of Amara/Exide is that they will manufacture cells at scale. Battery packs are anyway very low value addition.

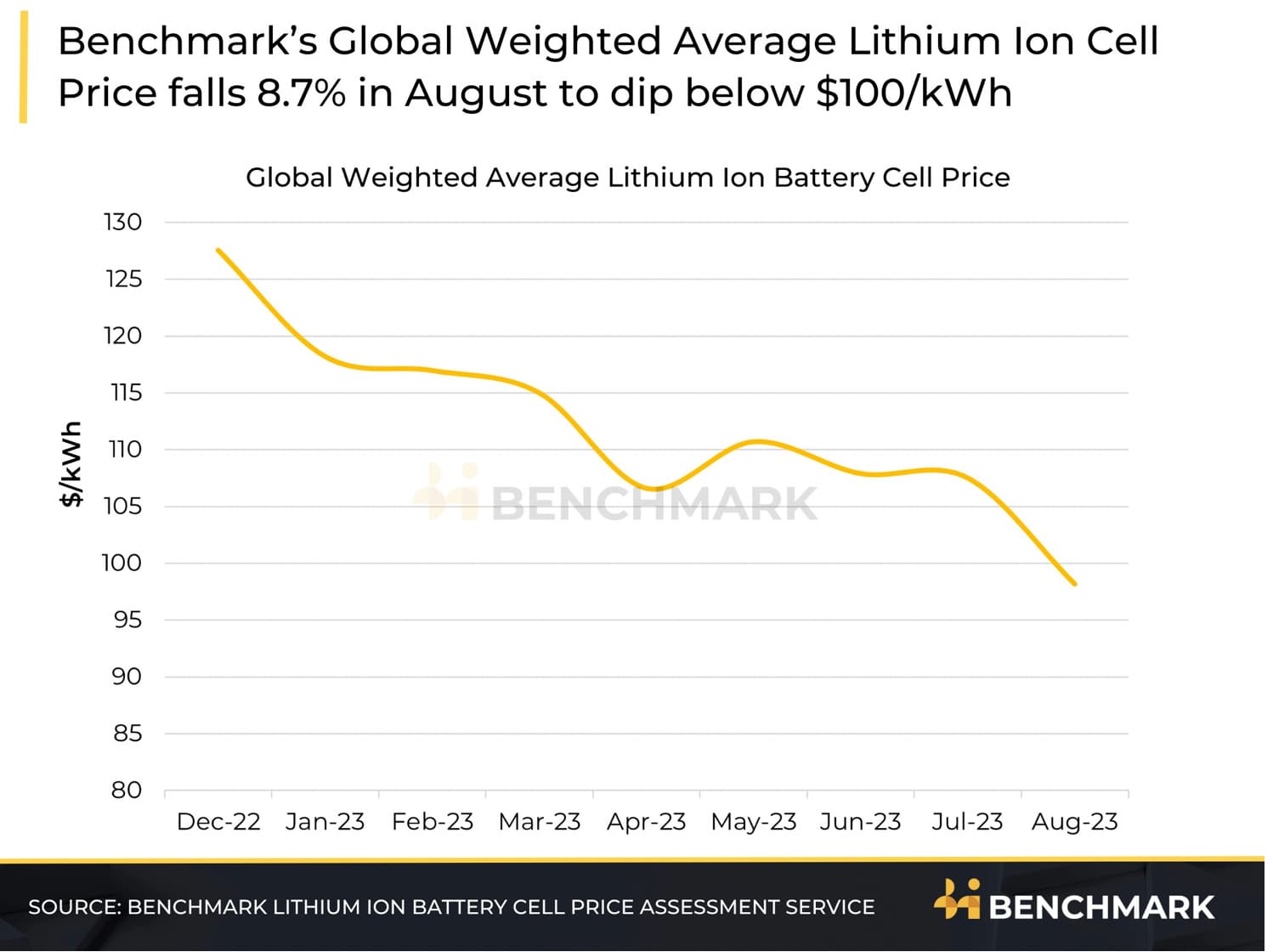

The larger risk for cos like Amara/Exide is that they may not be the lowest cost manufacturers of cells, as the Chinese have already built economies of scale. At a cell price of $100/GWh and 2GWh capacity, Amara expects fixed asset turns of 1.4-1.5x and gross margins of 25-30%. If for some reason, cell prices come down (as have been coming down in recent months), the entire value proposition goes for a toss.

They are not putting up any investments for this, as manufacturing will be outsourced. They are simply leveraging their existing dealer network to try and grow sales. This is akin to FMCG cos introducing new products at minimal costs, if it works out they can manufacture in-house at some point, if not it was atleast worth a try.

They will be manufacturing cells, which can then go into battery packs for EVs/storage centers/telecom tower/etc. Amara is anyway the leader in storage batteries used in telecom sector with a 60% market share.

Shouldn’t have any impact, Johnson control divested their battery division to private equity and haven’t been investing much in lithium ion batteries. It doesn’t have any impact on Amara’s business.

Related party issues used to a pain point in 2012-15, but of late Amara has been trying to rectify these. All these mergers are being done at very reasonable valuations (7x EV/EBITDA for Mangal, 6.5x for Amara Power systems). Also, the way its been done allows promoters to increase their shareholding in the co., which is quite low.

Disclosure: Invested in Amara (position size here, bought shares in last-30 days)

Exide has been through EV learning curve since 2019 .

First with different battery packs targeted at varied use cases - It already has 600 crore pipeline of orders in battery packs

Now it is moving to cell MFG with Chinese Battery player support for setting up Mfg and RM support .

Amara Raja has been slow … but still it can negate it if ties up player like LG or CATL … That will bring access to in global clients supply chain …

As you said, < 100$/kwh, investment can go for a toss. Toss in the sense of asset payback - Asset turnover i think.

I have not studied Spread between raw materials for cells and final cell price $/KWH, but it seems OPM will maintain a range over a longer period of time. Any comment on this?

Any idea on how cost incurred to set up plant AND manufacturing cost (besides materials) go down with fall in cell price? These factors will determine asset payback and desire to add more capacities. Usually longer than 7 years asset payback slows down new capex.

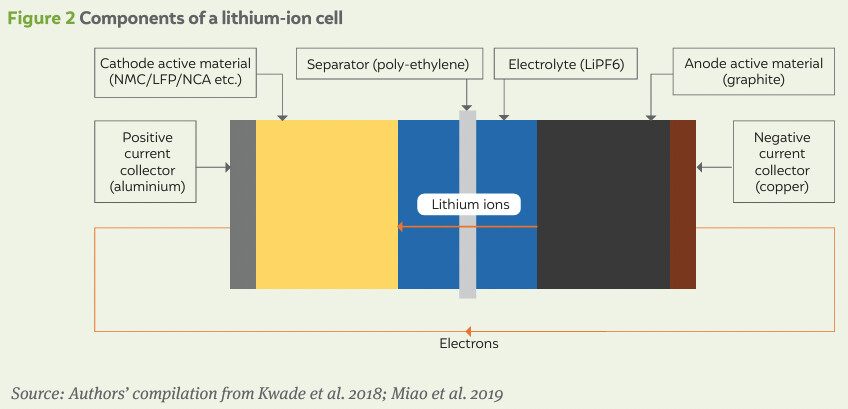

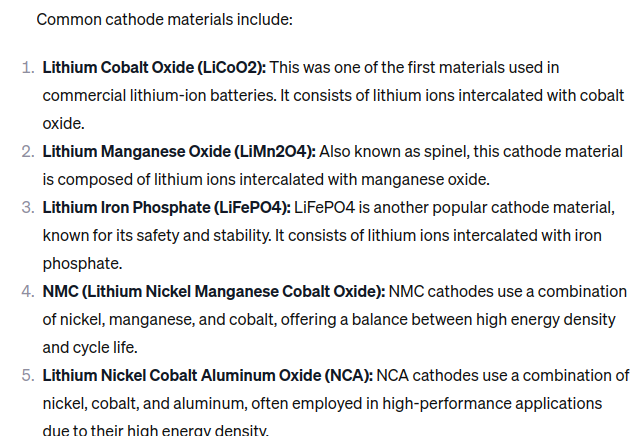

Is plant fungible to other technologies like metal air, sodium based OR even different Li based compounds (likes of LiCoO2, LiMn2O4, LiFePO4, LiNiMnCoO2 etc) cathods ?

Amara came out with decent results, sales grew by 9.6% and EPS by 12%. Its interesting to see that they are already decently profitable in their new energy business which is scaling quite fast, having reached last year revenue in H1FY24. They are seeing higher growth in telecom segment with rollout of 5G. Additionally, they are now guiding for 15-16% EBITDA margin even at lead prices of 180/kg, previously they used to do these margins when lead prices were around 150-160/kg, so they have been able to build in operational efficiencies to improve margins. The smelter plant commissioning in Q1FY25 will lead to 1-2% further improvement in RM costs. Concall notes below

FY24Q2

Lead acid battery: 6.4% YOY growth

o 4-W volumes: growth of 7%. OEM: 3-4%, after-market: 8%

o 2-W volumes: growth of 9%. OEM: 2-3%, after-market: 12-13%

o After-market 4-W demand has softened due to lower car sales 3 years back, there is a 2-3 year lag which they generally see. Expect 6-7% growth in 4W and 12-13% growth in 2W after market in FY24

o Industrial volumes: growth of 8-9% (telecom: 9-10%, UPS: 7-8%). Operating at 85-90% utilization in telecom. It is possible at a given lithium price (@$100/kwh) that lithium ion batteries gain adoption in telecom

o Home inverter volumes: decline of (-11%)

o Exports: Witnessed some shipment delays due to name changes, sales of which will come in Q3. Should see double digit growth in FY24

o Did not see any market share loss in OEM business, quarterly growth depends on production schedule of OEMs and on the models

New energy business:

o 150 cr. (vs 108 cr. in Q1 and 62 cr. in Q2FY23). Reported EBIT of 11.6 cr. (vs 4.2 cr. in Q1)

o Witnessed volume growth in chargers + 3-W battery packs

o Approved investment of 500 cr. in Amara Raja Advanced Cell Technologies, for lithium ion battery manufacturing.

o NMC and LFP cell manufacturing will be reasonably fungible

15-16% EBITDA margin is now possible even if lead prices stays at 175-180/kg

One time consultancy fees of 10 cr. incurred for enhancing throughput

Capex for lead: 200-300 cr. growth, 100-150 cr. maintenance

Got 93 cr. from tubular plant scrap sale in H1FY24

Amara Power Systems acquisition completed in September 2023, expected to strengthen charging solution offerings (2-W, 3-W and storage applications)

Amalgamation of Mangal Industries plastic division will result in 7.15% equity dilution and increase promoter shareholding to 32.86% (vs 28.06% now)

Recycling plant will be commercialized in 2 stages (total capacity: 1.5 lakh MT, 1 lakh MT will commercialize in Q1FY25). 1 lakh MT smelter plant will account for 25-30% of their lead requirements. Expect 1-2% gross margin benefit

Disclosure: Invested (position size here, bought shares in last-30 days)

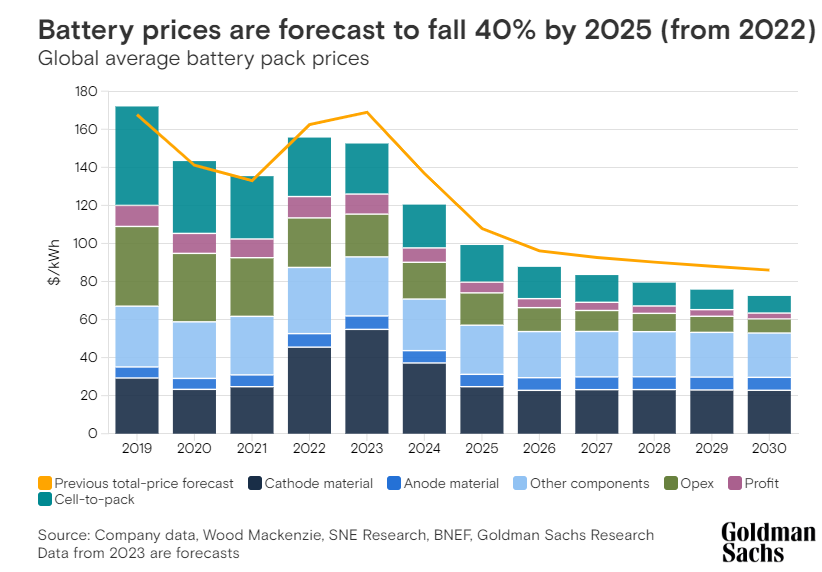

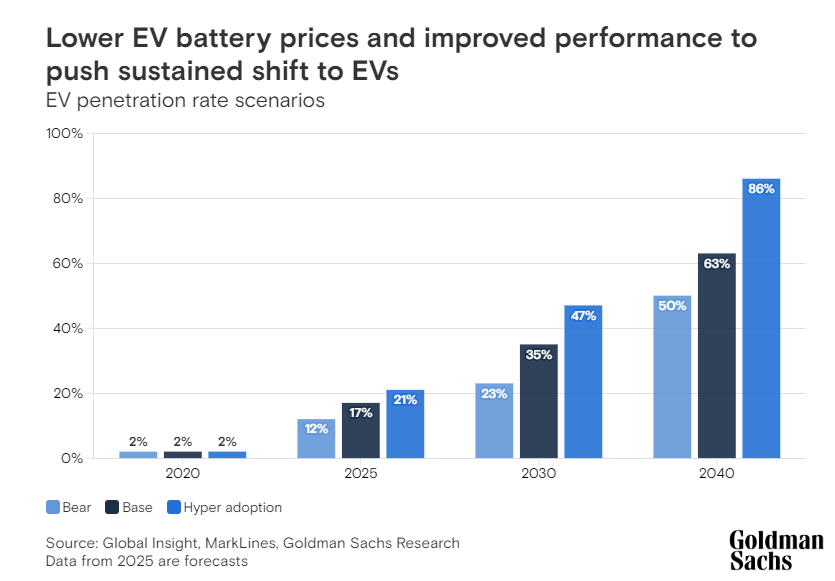

Goldman Sachs Research has revised its outlook on electric vehicle (EV) battery prices and the EV market. They anticipate significant changes that could make EVs more competitive with traditional internal combustion engine (ICE) vehicles:

Battery prices are expected to decline to $99 per kilowatt hour (kWh) of storage capacity by 2025, a 40% decrease from the 2022 levels.

A substantial portion of this price drop, almost half, is attributed to the falling prices of essential EV raw materials, including lithium, nickel, and cobalt.

Battery pack prices are projected to decrease by an average of 11% per year from 2023 to 2030.

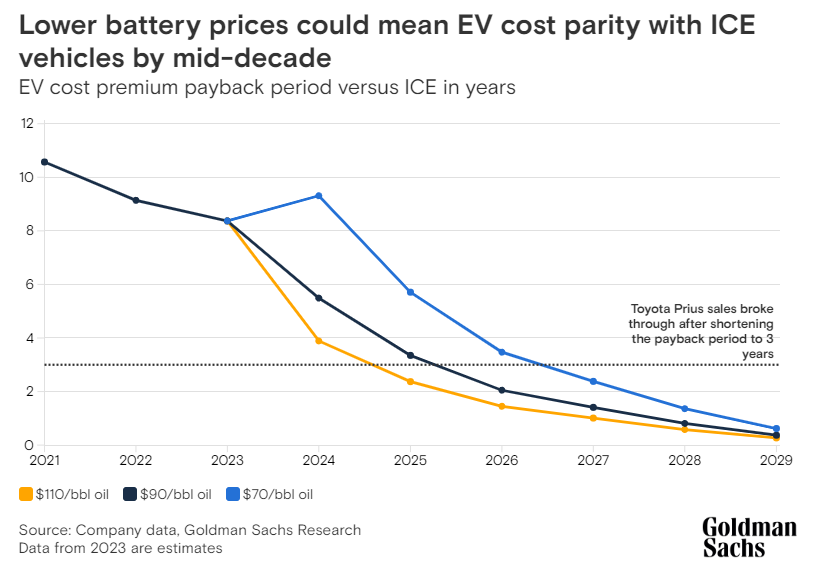

With the expected drop in battery prices, the EV market could achieve cost parity with ICE vehicles on a total-cost-of-ownership basis without the need for subsidies, potentially around the middle of this decade.

This reduction in battery costs may lead to more competitive EV pricing, which, in turn, could drive increased consumer adoption and expand the total addressable markets for EVs and batteries.

The EV market, which was initially driven by regulatory support, is transitioning to a new phase influenced more by consumer adoption than government incentives, thanks to declining battery prices.

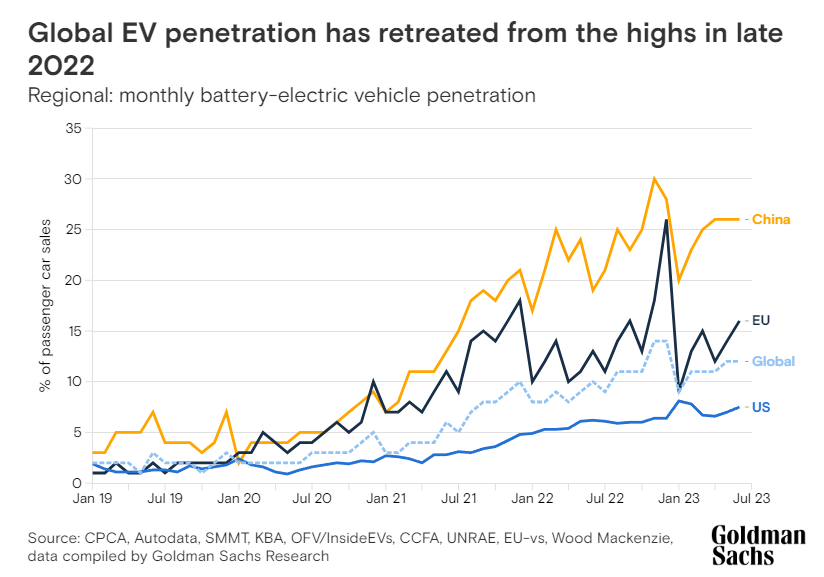

Goldman Sachs Research’s base-case estimate for global EV penetration sees it jumping to 17% in 2025 from just 2% in 2020. Projections increase to 35% and 63% by 2030 and 2040, respectively.

In a “hyper adoption” scenario, EVs could account for 21% of total global vehicle sales by 2025, 47% by 2030, and 86% by 2040.

China is at the forefront of this shift, with its EVs competitively priced compared to ICE vehicles, especially in its local market.

While Chinese EV sales have been subsidized by manufacturers selling at a loss, this trend is expected to change in the mid-2020s, coinciding with battery price declines and increased EV sales volumes.

Global Perspective:

In contrast, carmakers in the US and Europe have predominantly focused on larger and more luxurious EV models.

Goldman Sachs Research believes that the EV market in China is the closest to a consumer-led EV adoption phase.

Battery Innovations:

New battery technologies are expected to play a significant role in the rapid decline of battery prices.

Innovations include novel anode materials that incorporate silicon, enhancing energy density, and new battery structures, like larger cylindrical batteries, streamlining pack manufacturing processes, leading to savings in labor and machine time.

These changes in battery prices and market dynamics are predicted to have a profound impact on the EV industry and could accelerate the adoption of electric vehicles, making them more accessible and competitive in the coming years.

Happy to announce that our persistent efforts to connect with domain experts/folks tracking EV/Storage/Charging Infra space is bearing fruits.

Someone from the Industry @BCell_Tracker well-conversant with Li-On Cell/Battery player space will make a few posts to help bring more clarity in this emerging and rapidly evolving space.

Let’s try and take things forward with his/other domain experts help

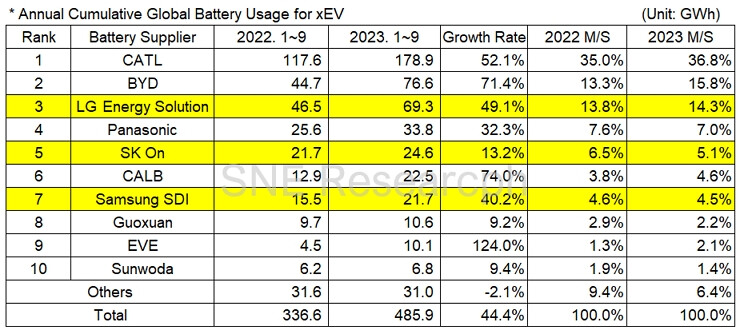

CATL (China); BYD (China); LG Energy Solutions (South Korea); Panasonic (Japan); SK Innovation (SK On) (South Korea); CALB (China); Samsung SDI (South Korea); Gotion (Guoxuan) (China); EVE Energy (China); Sunwoda (China)

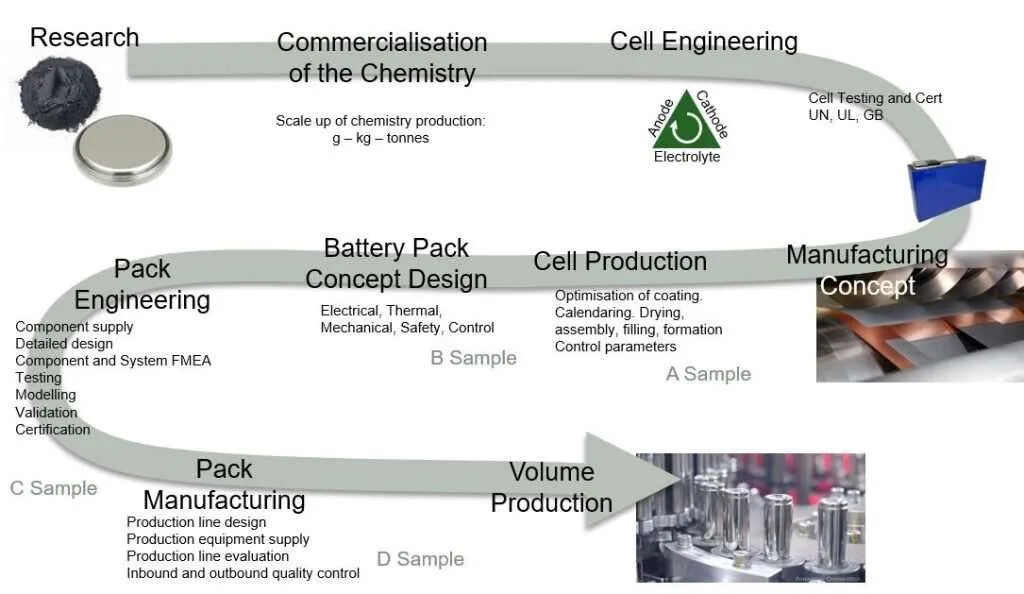

Cell/Battery Development process - A sample to D Sample

A Sample and B Sample can be produced from Manufacturer’s Pilot Plant facility

C and D samples have to be produced from the actual production line

The timeline is typically 6-12 months to move from one Sample to next before being qualified by the Auto OEM.

Lithium-Ion Cell GigaFactories are very tough to scale up

Even Panasonic with several decades of experience in batteries space, including in lithium-ion batteries struggled to scale up their first large scale gigafactory in Nevada US

Panasonic Started Construction for the factory in January 2015, with Production starting in January 2017.

Panasonic first achieved profitability from their Nevada plant in 2021.

Basically, it took them 4 years to reach the desired scale and yield from the Plant. Note that this is the plant that supplies Tesla.

There are more such examples. SK Innovation’s Battery business is yet to break even. They are operating since 2017. Again this is mainly due to plant yield issues.

Scaling/Ramping up the plant to optimum level of capacity is tough.

The Batteries have to go through stringent quality checks as there are safety issues to monitor. A small defect can lead to fires and huge provisions. (for example look at LG Energy Solutions and GM’s Bolt recall issue)

Also, there have not been many new entrants/Start-ups in the Cell space. There are so few that we can list them out:

New Entrants in Europe – Northvolt, Verkor, Freyr, Morrow (None of them have started production yet)

New Entrants in North America – Our Next Energy, Quantumscape, Solid Power (Again none of them have started production)

China has huge edge with them being highly capital efficient (wth Government Incentives)

The Chinese companies are most efficient helped by Government incentives. Capital Intensity for Chinese companies especially leaders like CATL is $35-$50m/GWh of capacity in China. In US, Europe Capital intensity is more the 2x. US plants >100m/GWh (for examples look at any of the recent announcements by LG Energy Solutions/ SK Innovation in US). For Amara Raja too Capital Intensity is around $71m/GWh using current exchange rates.

What this does is Chinese companies keep building capacity even without firm contracts in place. They operate at much lower plant utilisations. Being cost competitive with Chinese players globally is tough.

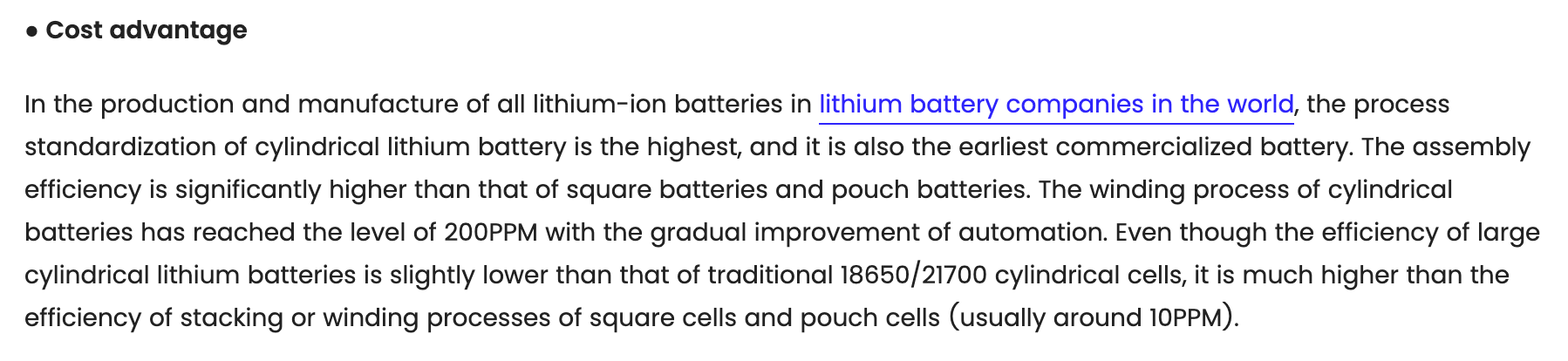

Why ARE&M’s Decision to go for Cylindrical Batteries 21700 format is good

Basically Cylindrical Cells/Batteries are easier to mass produce compared to other forms (pouch and Prismatic) See below

Stellantis – JV plants with Samsung SDI and LGES (so partially in-house)

BMW – No in house manufacturing – Long Term contacts with – CATL, EVE Energy, AESC, Northvolt (confirmed), SVOLT (Rumoured)

GM – JV with LGES (Ultium) and Samsung SDI (so partially in-house)

Ford – JV with SK Innovation (so partially in-house)

Hyundai – JV with LGES and SK Innovation (so partially in-house)

Toyota – Are building their own plants and have JV with Panasonic called Prime Planet Energy Solutions (partially in-house). Has contracts with LGES too

For India

Tata – Has plans for in-house manufacturing, currently key partner is China’s Gotion

Mahindra – Not aware of in-house manufacturing plans. Currently key partner is LGES

Hyundai – Key partners are SK Innovation and LGES

Challenges for ARE&M

Scaling up is a challenge

Technology challenge – Already companies are moving to 46-Series cylindrical cells (Tesla, BMW) Also the space is very fluid in terms of new technology coming up. Things like new Cathode chemistry (Manganese based – LMFP) or silicon anode. They need to move with the market or their product might not remain relevant. Lot of focus on Fast charging now with CATL’s Shenxing battery launch.

Getting contracts from OEM’s to ensure plants are utilized.

Also, need to note that the batteries are unique for every OEM. So they cannot be interchanged. Losing a contract/non renewal of a contract is a big dent as new contracts again need to go through the qualification process.

Thank you @Nishant_Sampat for a good Report - gives us more granular understanding - to explore ARE&M New Energy/Mobility segment plans/viability

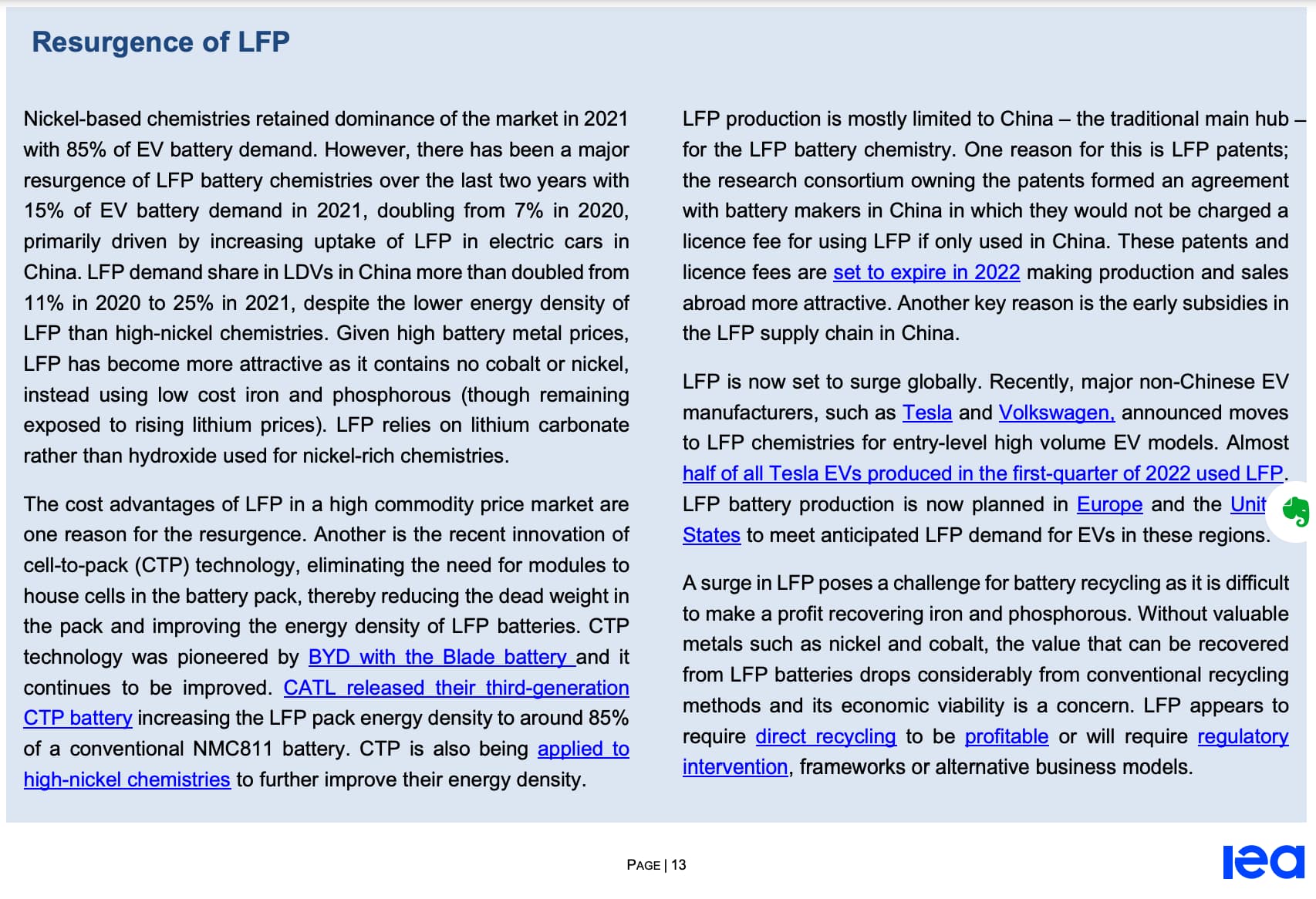

Another slightly dated report (2022) highlights a crucial aspect: Re-emergence of LFP tech, and why Tesla and VW have reposed full faith in LFP now (Chinese Patents expiry in 2022 - my have been a big contributing factor, even for ARE&M?

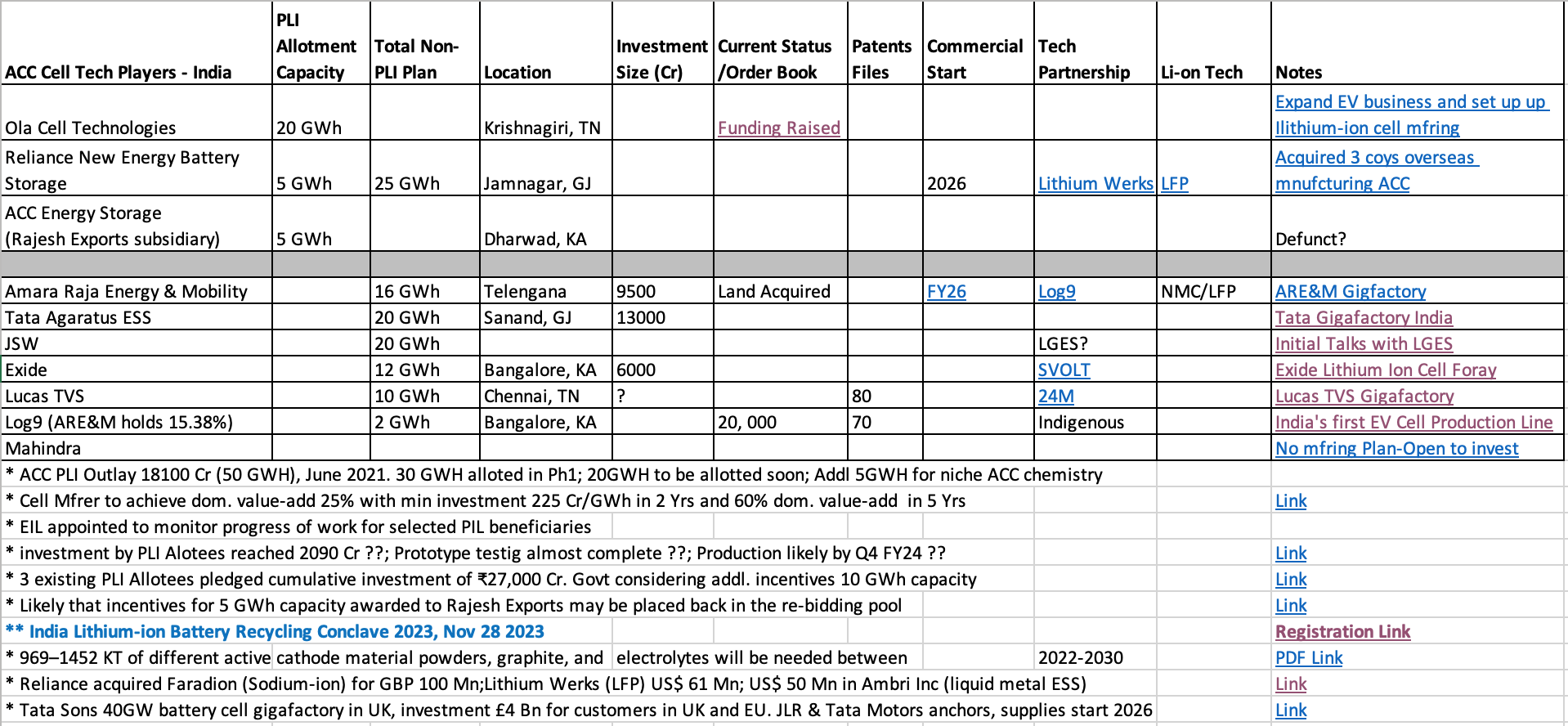

Compiled Notes on the India Cell Tech Players space.

Hope this is useful to bring everyone on the same page quickly.

Invite Domain Experts to help us take this forward /establish the on-ground reality.

Among these Lucas TVS’s partnership with 24M is not very helpful. Freyr a Norway based cell start-up has been working on 24M technology for 2 years now. Their Pilot plant keeps getting delayed. 24M’s technology is different from conventional technology.

Exide may have one of the strongest technology partner in Svolt with proven cell manufacturing capabilities and expertise in LFP, as well as Nickel based technology