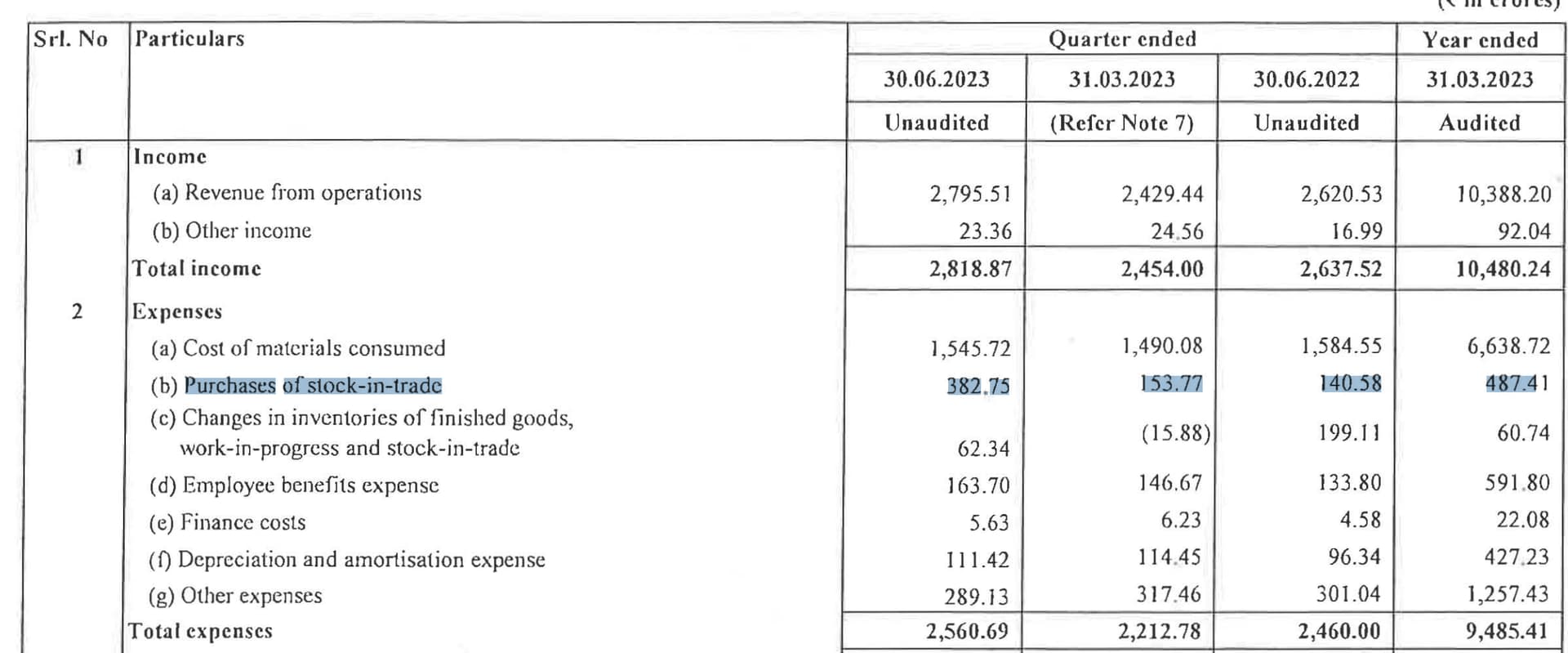

Yes there were discussions around it, but not much beyond whats already in the public domain. They have currently outsourced manufacturing of 3-W tubular batteries and will build their new plant with insurance proceeds. Until then, their gross margins will be lower as their tubular batteries will not be manufactured by them. You can see this in purchases of stock-in-trade which showed a large jump in this quarter. I think this will continue being the case until their plant is rebuilt.

8 Likes

Upon checking the case status and the orders so far one finds that it hasn’t moved since January 2023 and a few days after that last date one of its factories which the APPCB had targetted for closure got completely gutted in a fire, talk about coincidences!

In my view Clarios cashing out was just that, liquidating a non core non material investment for the PE Firm that acquired the battery div of Johnson Controls … I am not looking at it as my oh my a Big FII has exited the company…

As a minority shareholder I would look forward to the day when this existential crisis on the companys future by the APPCB is removed by the Judiciary… the management being content with letting the writ sleep since January 2023 and happy with interim stay does not bode well for me… As the petitioner in the two writs filed by them, they should persue the case aggressively until final orders stage…

I attended the conference call post Q1 and no question was asked of the case progress although my internal queries w.r.t. problems due to factory fire were taken care of … tubular batteries (ups?) division has been affected and the company is not expecting growth there…as Harsh righty pointed out, they are replenishing stocks at the dealer level through third party manufacturing… minimum 18 to 20 months until they can restart manufacturing in that plant and the other insurance money is tied to machinery and factory rebuilding

5 Likes

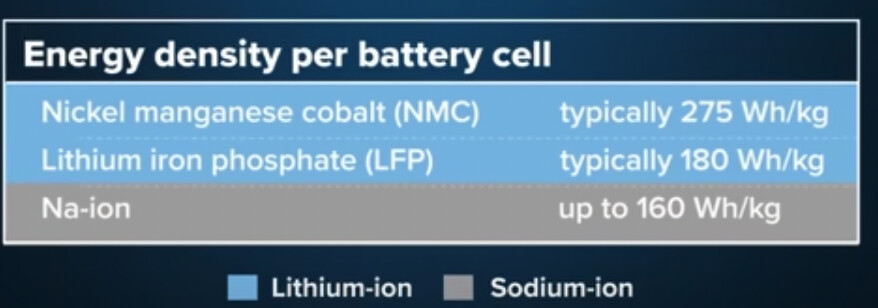

Energy densities covert to range in electric vehicles. If you are centered ur business towards EV OEMs. Then LFP NMC make sense. Na-ion need to be bigger and heavier to hold the same amount of electrical charge. EV Cars where space is a luxury Na-ion doesn’t make huge sense. Cost effectiveness Vs Range debate.

Na-ion can be stored at zero volt charge and Li-ion has to be transported at a finite charge state usually 30%.

Sodium Ion batteries are less energy dense Vs Li-ion

Faradion’s latest offering (note: reliance bought faradian recently) are at 160Watt hours per Kg

Whereas, Li-ion on shelf today for sale offer 250 watt hours per Kg going up to 400 by advanced chemistry.

IPLTech electric + Faradian developed heavy electric vehicles launched rhino first electric truck in 2018 using Na-ion tech but had mixed success and eventually Li-ion was used.

faradions real spot was in stationary energy storage which I also think Na-ion should go.

1 Like

Does anybody have access to their investor concall recording from 14th August? Couldn’t find it on their website or YouTube.

2 Likes

Amara Raja came with flattish results, with margins reviving YOY but being impacted QoQ due to higher traded sales of tubular batteries. They are confident of doing 750 cr. sales in new energy business this year, which will be a 3x scaleup over last year. Lithium ion validation plant will come onstream at end of FY25, and the 2GWh capacity in Fy26. Interestingly, at $100/GWh cell costs, they can do revenues of upto 3000 cr. which translates into asset turns of ~2x (investment of 1500 cr.). Given this space is evolving, its hard to estimate IRRs on the project, but directionally it seems to be going the right way. Concall notes below.

FY24Q1

-

Lead acid battery: 4% YOY growth

o 70% contribution from 2-W, 4-W and inverters; 30% from industrial segment

o 4-W grew by 5%; after-market grew at 7-8%

o 2-W grew by 9%; both OEM and after-market grew at low double digit. Have seen significant market share gain in after market

o Inverter and other applications declined by (-20%) due to poor season and fire in tubular factory. This business was replaced by trading revenue (15-16%) and has impacted margins. Have maintained market share, but has failed to gain market share due to absence of self-manufacturing

o Export was muted partly due anti-dumping duty in Middle East markets. Expect export growth to recover in coming quarters from Western markets

o Industrial segment grew 15% YOY, telecom even higher - Capacity utilization

o Automotive: 74-75% (2-W: 80%)

o Industrial: 95-97% - New energy business: 107 cr. Supplying battery packs to 3-W (Piaggio is main customer) and battery chargers to 3-W OEMs and other stationary applications (Piaggio and M&M are main customers). Getting ready to launch battery packs for 2-W and certain high voltage applications. Also supplying lithium battery packs to telecom customers

-

Lithium ion plant:

o Customer qualification plant will start in end of FY25 and GWh NMC line will deliver production in FY26. R&D lab + customer qualification plant + GWh line will cost 1500 cr. (200-300 cr. to be incurred in FY24)

o Depending on cell price (@$100/GWh) and 2GWh, fixed asset turns come between 1.4-1.5x

o Revenue contribution from 2GHh plant can be around 3000 cr. at full utilization (with 10-12% EBITDA margin) - Insurance cost increase (6-7 cr.) has also impacted margins

- Reduced power costs (10-15 cr.) due to solar plant coming onstream. Currently catering to 20% of power requirements. Total investment behind the solar power plant and rooftop facility will be 300 cr. (59.1MW currently + 7.5MW to be done in FY24)

- For any greenfield expansion, optimum size of plant will be 7-7.5mn batteries. If they put up a facility, it will be at a different location and the capacity will be added in phases

- Tubular plant will be reinstated in 18-20 months

- At lead prices of 150-170/kg, can do 15% EBITDA margin

Disclosure: Invested (position size here, bought shares in last-30 days)

15 Likes

6 Likes

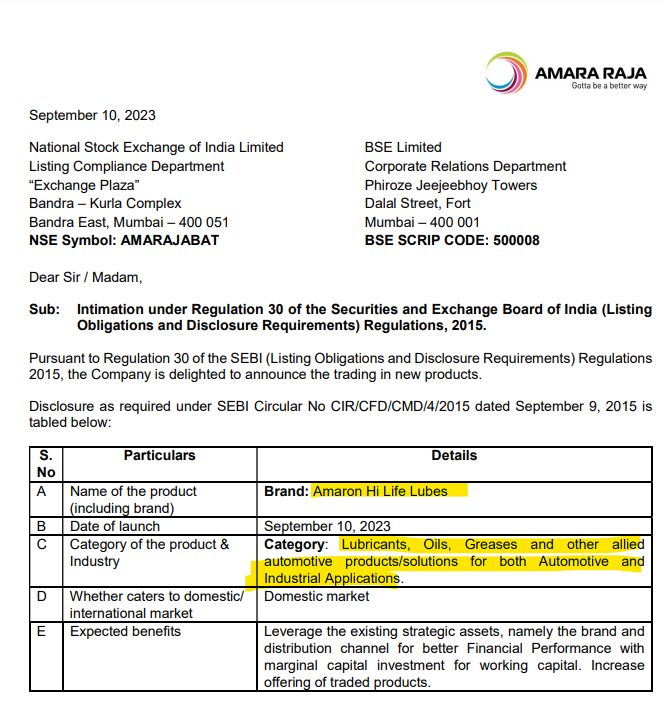

is it a good diversification? … if EV is coming, would oil and lubricants also not be in less demand??Would’nt it have been better if they rather invest capital and time in scaling the EV battery space?

1 Like

If you read through the notice, you may appreciate the fact that lubricants, oils and greases have use in industrial applications as well, which is a big market by itself

Again, EVs are much hyped, and the evidence lies in the sales quantity compared to general ICE engine 2-wheelers. India still lacks the infrastructure and reliability in terms of offering EVs that can disrupt the market like it did in China. So, at least for the next 2 decades, ICE engines will co-exist and this may be one of the reason for this diversification

Disc: not invested

4 Likes

Those of you following up Amar Raja Battery, do you have any info on Li ion battery start of production at the company.

I know they are putting up a Li ion batteries on their own ( they did not get PLI scheme from Govt for their brown field project )

What I wanted to know do they have plans for lithium ion batteries for EV only or they would be manufacturing Li ion batteries for BESS ( Battery Energy storage systems). There is a huge requirement/ opportunity coming up for storage of renewable solar energy / wind energy since hydrolyser capacities are lagging behind in our country. And at a later date , even if hydrolyser capacities come up, BESS -Li ion will have its own demand all through out this renewable energy boom.

If not Amar Raja, is there any other battery manufacturer who makes / plan to make Li ion batteries for BESS.

If you are following Green hydrogen thread , may be you would be understanding what I am talking about.

BESS batteries are supposed to be larger in size and comes as a large pack.

3 Likes

check log9 materials. They have a lot of good things that they keep sharing

Amara raja has strategic stake here.

Am a little wary of just having strategic stake unless the company itself does something in the area.

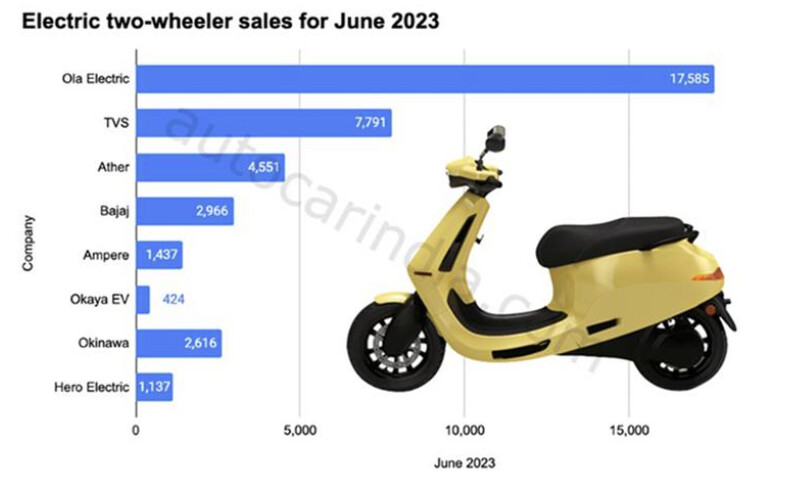

Case in point is Hero’s strategic stake in Ather Energy which was amongst the 1st to gain success. However the below stat paints a not so rosy picture for Hero-Ather. And TVS and Ola which built technology inhouse are leading. Specially look at TVS’s growth MoM from July to August 2023

To be fair, they have announced 10K Cr investment in creating Lithium Ion cells at their Gigafactory. Would be interesting to read if there is any update on the same… India's Largest Li-Ion Cell Manufacturing Facility: Amara Raja Lays Foundation Stone For Rs 9,500 Crore Gigafactory In Telangana

1 Like

They already have access to the distribution network in this area. The retailers selling aftermarket Amaron batteries for 2-wheelers are the same people selling engine oil, gear oil and lubricants. Maybe just capitalising on this advantage.

1 Like

Agree, and maybe its good thing from short term profitability standpoint, i was just wondering if its worth the distraction and distribution of resources in the long run…

Btw they do realize and are anyways investing in building the future, rebranding of the firm is also a good step in creating the future vision.

“Officially rebranded itself as Amara Raja Energy and Mobility Limited (ARE&M). This move marks the culmination of a two-year journey aimed at transitioning from a battery manufacturer to a comprehensive solutions provider in the Energy and mobility sector.”

1 Like

Complete exit of Clarios ARBL (Johnson Control) - Is the hangover or selling pressure over. How would market perceive going forward. Personally, I am sensing a strong break out in near future

2 Likes

Hi everyone, how does one make sense of the related party transaction the promotors have?

I am talking more specifically about fixed assets purchased from related party, & then eventual outright buying of the company/ division.

Like Purchase of FA of 242Crs from Amara Raja Power systems in FY22, followed by 40Crs in FY23 & now buying the stake at seemingly reasonable valuations.

Same with Mangal Industries buying FA worth 57Crs & 45 Crs in FY22&23 respectively followed by now buying of the plastics division of Mangal Industries

3 Likes

good quries. if any one follwoing this closely pls share your input.

1 Like

With Deloitte being their statutory auditor, personally I dont see related party transactions as much of a concern. The promoters / company are here for longer run and looking at much larger picture rather than impacting their goodwill with smaller gains by unethical means.

Buying of plastic division with almost 65 cr PAT at Rs 800 cr is 12x PE multiple - which is not unreasonable. This deal is also a mechanism to increase promoter stake - as ARBL is not paying cash for this acquisition. Promoter increasing their stake inspires more confidence.

Nalanda Capital (repuited Private equity) holding almost 10% stake gives strong comfort and clears checklist in terms of corporate governance and management.

Disclaimer : I am invested hence maybe biased.

13 Likes