I would love to invest too. Thats why amara raja investment stands good chance as log9 does need a niche distributor and Amara raja dearly needs the tech.

2 Likes

Interesting management interview

09.05.2023 ET

- Phase I (Commercial pilot plant with 2GW manufacturing + R&D center): 2000 cr. (via internal accruals) in 24 months

- For rest of 9500 cr. capex, capital structure is being planned

- In terms of localization, 25% value addition will be done in India with 75% being imported in the beginning. In 5-years, want to increase localization to 60%

- Battery prices have increased in past 2-years, this is an aberration and it should follow longer term trajectory of price deflation

- A lot of new battery chemistries are coming up to replace lithium ion batteries

- Revenue growth will be much faster in lithium ion batteries as each lithium battery pack is much higher priced than current lead acid batteries

- Before large scaleup happens in lithium batteries, after market lead acid batteries will be higher margin business

Disclosure: Invested (position size here, no transactions in last-30 days)

19 Likes

Why is the company reporting PBT (Profit before Tax) and not PAT (Profit After tax), which is what translates to EPS? Any specific reason??

1 Like

Amara Raja Q4FY23 Concall Summary

1 Like

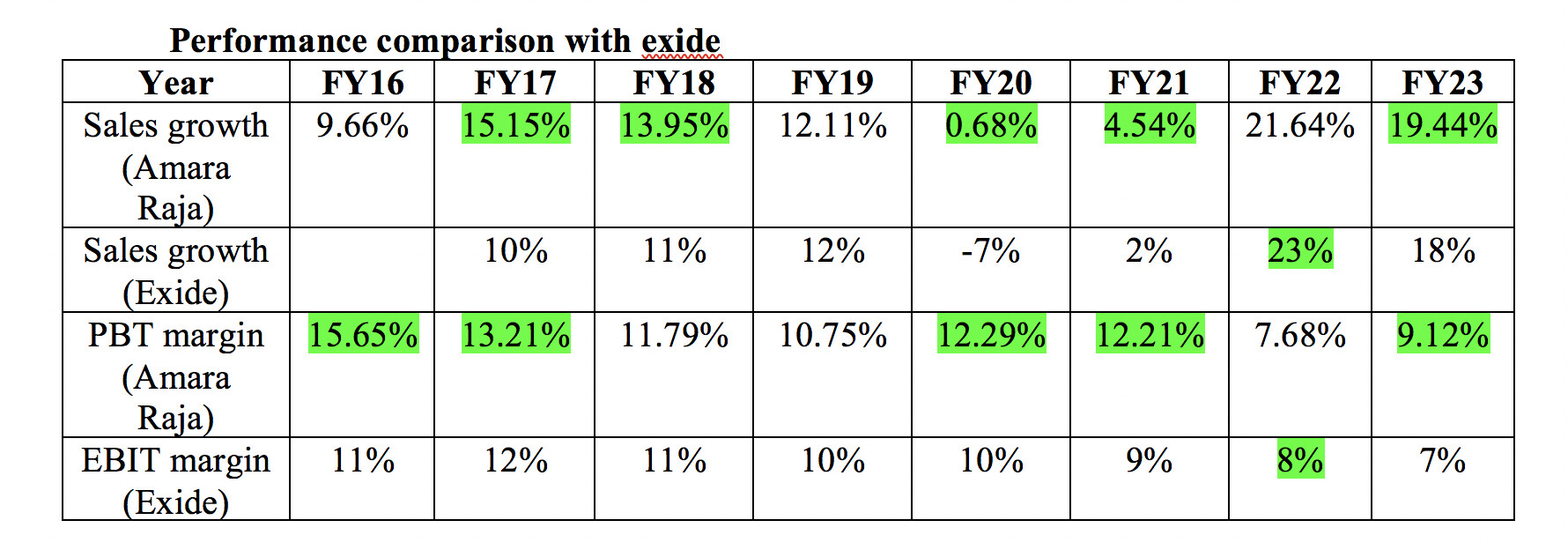

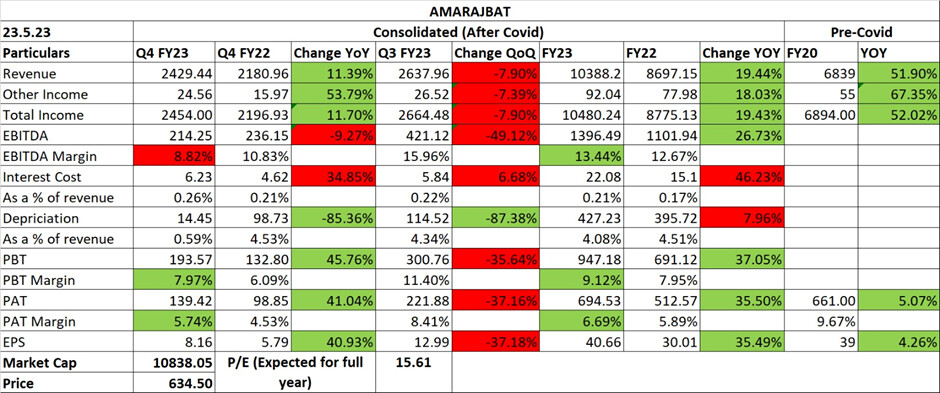

Mixed set of results from the co, the fire at their 3-W tubular battery led to muted growth. If we compare them vs Exide, they have done better in FY23 (both in margin and sales growth front).

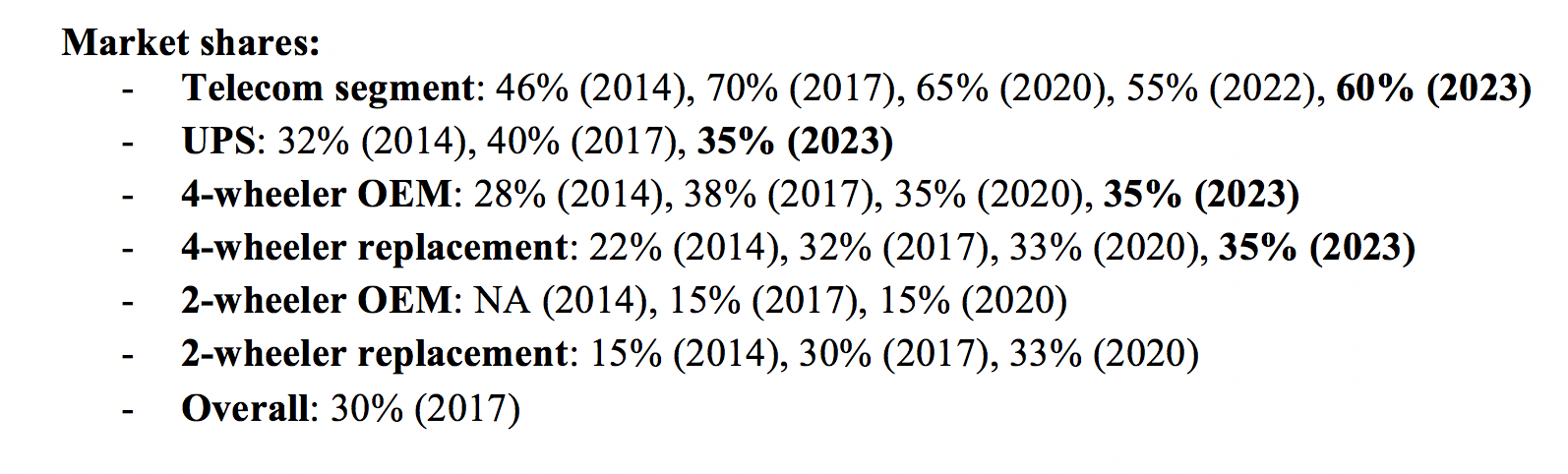

In the past few years, Amara Raja has made serious in-roads in 4-W battery (both OEM and after market) and has reached 35% market share. As the 2-W market has been largely flat in past few years, Amara Raja has done well in making in-roads with 4-W batteries. Additionally, they have maintained very high market share in telecom segment.

Most interestingly, Amara Raja has been very calibrated in spends in their lithium battery investments and can now completely fund the expansion from their own cashflows. They are generating close to 1000 cr. of cashflows each year, and plan to spend 400 cr. on both lead acid and lithium batteries each year for the next 3 years. This gives them 200-300 cr. of freecashflow which can be shared back as dividends or used for further expansion (like acquisition of Amara Raja Power systems or Mangal Industries).

On the negative side, lithium battery investments are really low ROCE as lithium battery packs generate 25% gross margins and work at asset turns of 1-1.2x currently. As lithium is largely imported, creditor terms will be unfavorable for the co and require higher inventory requirement. Even assuming a 120 day working capital cycle, ROIC comes in single digits. This has to change in the future, or Indian battery cos cannot be competitive.

Notes from concall below.

FY23Q4

- Margins: Gross margins have started reviving. Power costs were higher and should reduce due to commissioning of new power plant. Had higher employee costs as employees that were working in tubular factory (which caught fire) were kept on payroll. Hoping to get back to 14-16% EBITDA margin in lead acid division, but overall margins will be lower due to investments in lithium ion (13-15%)

- Will take 2.5 years in commencement of CQP and 2GW lithium plant and require 1300 cr. of investments (will use NMC technology). Investments will be spread over 2.5 years. Focus will be first on EV 2-W. Based on current prices, asset turns will be 1-1.2x

- Capex: 300-400 cr. for lead acid in FY24 and FY25. 300 cr. for new energy business in FY24 and 500 cr. in FY25

- Lead recycling plant will cater to 30% of lead requirements

- Have not taken price hikes in after market in Q4 due to recent lead price increase (it was not very high)

- R&D spends are 2-2.5% of sales

- Current capacity utilization is 90-93%

Disclosure: Invested (position size here, no transactions in last-30 days)

23 Likes

- Focus on Lead Acid Batteries value maximization and transition to new age technologies. Working on Li Cell & Pack Manufacturing, EV Charging Solutions, Energy Storage Solutions.

- Lead Acid Batteries: 7 battery Manufacturing plants in 2 locations. Capacity of 4W batteries is 19 Million Nos. Capacity of 2W batteries is 30 million nos. Industrial Batteries Capacity is 2.3 Bn AH.

- Demand for fuel efficient vehicles, meeting stringent regulatory norms, is increasing. Increased use of ISS, EFB, AGM technologies will result in increased share of organized brands. Auxiliary batteries for electric vehicle to enhance demand.

- Trends: 4W volumes have surpassed pre-covid levels. 2W volumes also saw an uptick in FY23.

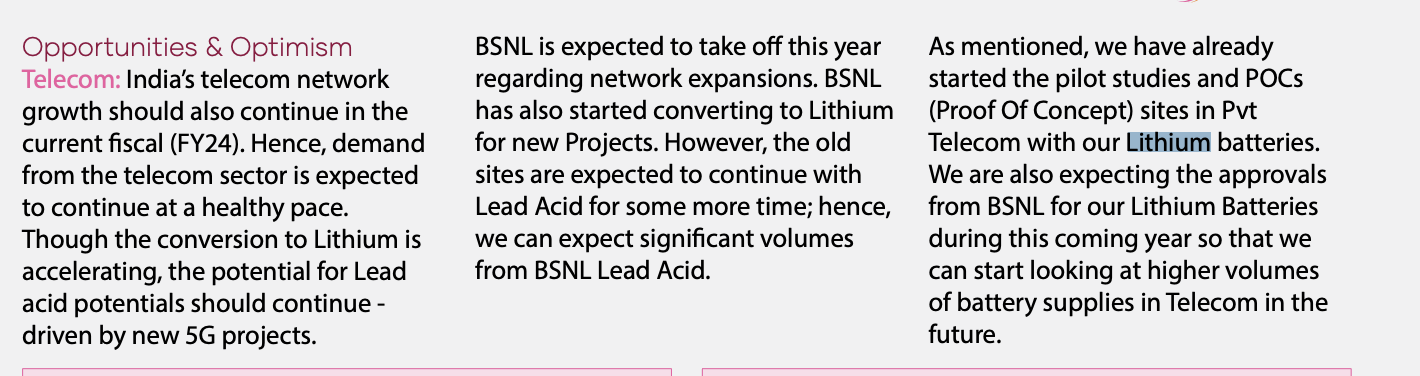

- Industrial Batteries saw double digit growth in FY23. Demand for UBS Batteries is robust. 5G rollout has seen a strong growth.

- Margin improvement due to lower input costs and higher realization.

8 Likes

Amara Raja Batt. trades

From Screener. It gives the information on who is procuring it. I don’t know much of the track record of the buyer or seller. In many cases, I noticed they also have wins and losses. Only those tracking the funds very well tell if buyer is right or seller is right.

Arbitrage funds - are these for long term holding ?

Bulk Deals/Block Deals

| Person | Quantity | Price | |

|---|---|---|---|

| 18 Jul 2023 | |||

| Tata Aia Life Insurance Company Limited | BUY | 20,00,000 | 652 |

| Societe Generale | BUY | 42,00,000 | 652 |

| Pinebridge Inv Asia Limited A/C Pb Global Funds - Pinebridge India Eqfund | BUY | 10,00,000 | 652 |

| Nippon India Mutual Fund | BUY | 14,59,854 | 652 |

| Kotak Mahindra Mutual Fund | BUY | 9,20,245 | 652 |

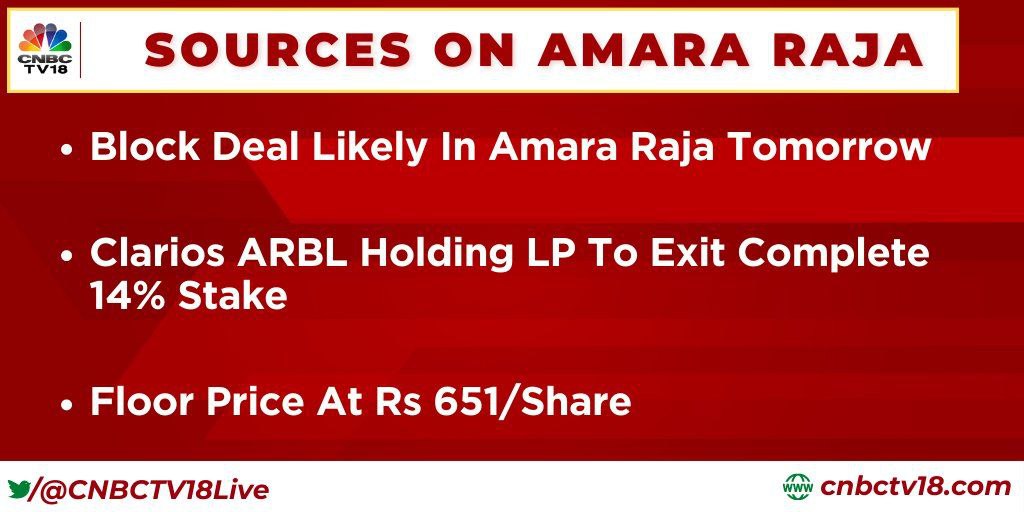

| Clarios Arbl Holding Lp | SELL | 2,39,13,750 | 653 |

| Bonanza Commodity Brokers Private Limited | SELL | 9,30,403 | 648 |

| Bonanza Commodity Brokers Private Limited | BUY | 8,40,403 | 656 |

| Bnp Paribas Arbitrage | BUY | 24,96,920 | 652 |

Any expert views are welcome.

Disc: a small position just based on recent breakout above 52 weeks. Now it went below 50 DMA and observing how it moves today. 14% exit will have impact for sure.

3 Likes

Clarios has sold 10% stake before as well around May 2021

They held 24% in total of which 14% has been sold this week.

Overhang of selling should ideally be zero now. New investors buying that 14% stake ideally won’t exit for at least medium term. And log9 strategic investment and mangal industries merger augers really well in terms of things investor community kept complaining about when it came to Amara Raja.

8 Likes

https://www.bseindia.com/xml-data/corpfiling/AttachLive//89384598-d717-4b42-ba46-a9b260ad2434.pdf

Annual Report - Amara Raja. batteries

Li Ion approvals this year in near future probably

The Company is one of the first players to achieve IATF 16949:2016& ISO 9001:2015 Certification for Li-Ion battery pack assembly and manufacturing operations

8 Likes

Interesting interview with Vikramadithya. Very detail oriented, honest and self-critical guy. I think the companys future will be in safe hands.

4 Likes

2 Likes

I participated at their AGM, it was quite a long event where management took out a lot of time to answer a variety of questions that were raised. I am sharing my notes.

Q. We used to do EBITDA margins of 16% until FY21. Since then, lead and power costs have seen a sharp increase. When do we see ourselves getting back to our earlier margin trajectory?

- Have been unable to pass on full lead price hike to customers. Expect to recover to 14-16% EBITDA margin

- Have installed in solar plants (roof and ground based). Currently using 20% of renewable energy for meeting captive power requirements

Q. Over a longer period of time, our fixed asset turns have decreased, from peaks of 8x achieved way back in FY13 to now being 3-3.5x. Effect of this is also visible in the form of higher depreciation costs in our P&L statement, which has reduced our EPS growth rates over time, despite us growing sales at a decent clip. What has changed in the industry landscape that has affected the return metrics of the company over a long period of time?

- Have been adding capacities faster than demand growth which has impacted asset turns. Expect fixed asset turns to ramp up to 4.5-5x at full utilization which should be achieved in next 1-2 years

Q. And, can we get back to doing 25-30% ROCEs like we used to until FY18?

- With increased asset turns and margins, ROCEs should go up from current levels

Q. Our foray into lithium ion batteries is again very capital intensive, with us guiding for asset turns of 1x and margins in-line or lower than lead acid batteries. In this scenario, how do we navigate from the increasing commoditization of our business?

- Now expect to reach 1.4x fixed asset turns in lithium ion. As technology becomes more evolved and they have more experience with commercialization, asset turns are likely to increase further

- Currently have 70 scientists and engineers working in lithium ion vertical

Q. In recent times, a number of parent entities are getting merged with the company at reasonable valuations, and I applaud the management intent. Can you give a 5-year road map, as to how many group entities (and which ones) might get merged with the listed co? More importantly, how does management decide which entity to merge?

- Not answered

Q. With increasing capital requirement for lithium ion business, how do we see dividend payouts going forward? Will it further reduced below 15%?

- Dividend payout has reduced from 30% to 15% in light of increased capex requirements for the business. Will maintain 15% payout

Miscellaneous

- Have digitized supply chain for better monitoring

- Business breakup: 30% industrial + 70% home and auto

- In auto division, 65% revenues come from aftermarket with rest coming from OEM

- Mangal Industries: Plastic component plant running at 85-90% utilization

- Geographical de-risking: Will announce 7.2mn battery greenfield expansion across the country

- EV: Have products for auxiliary battery that goes into EVs, will introduce them as their OEM customers introduce these vehicles in the market

- Will commercialize both NMC & LFP platforms for lithium ion batteries

Disclosure: Invested (position size here, no transactions in last-30 days)

27 Likes

Just putting it out there as NMC vs LFP debates have been center of couple of posts here in this Amara raja thread. Did read this back in may to get what is the latest debate around.

3 Likes

Hi Harsh,

Thank you for sharing the notes on the AGM, answered many queries in my head… I was going to take a position in this company, could still ignore the pollution case as vendetta politics but the Jan 2023 fire completely gutting one of their manufacturing units in Andhra Pradesh stopped me from taking a position here…

Did they not talk/no one questioned them about that incident, how it impacts them, the responsibility factor, or is it something very minor…they claimed losses of 450 odd crores with the insurance co.

I was wondering if you could share any information on that, or how you read it …

2 Likes

On January 30,2023, a fire broke out at one of the manufacturing facilities of the Company at Chilloor, Andhra Pradesh which caused damage to the Company’s property, plant and equipment and inventories, There was no loss of lives. The Company recognized a loss of ~ 438 56 crores arising from such incidents during the quarter and year ended March 31, 2023 . The loss is based on an evaluation of physical condition of property, plant and equipment and inventories and technical inspection by equipment manufacturers or chartered engineers and an assessment of recovery / salvage value by the designated vendors.

The Company has a valid mega all risk insurance policy covering the fire accident and has lodged a claim with the Insurance Company for losses suffered on account of the property, plant and equipment, inventories and loss of profits. The Insurance Company has admitted the claim based on an interim survey carried out by the surveyor appointed by it and the extent of final loss admissible under the policy is being evaluated by the surveyor. The Company estimated and recognised an insurance claim receivable as at March 3 I, 2023 in respect of the claim in accordance with its acco

unting policy. The aforementioned losses and the corresponding credit arising from the insurance claim receivable were presented on a net basis under Exceptional items tor the quarter and year ended March 3 1,2023.

During the quarter ended June 30, 2023, the Company has received an adhoc payment of ~ 100 crores from the Insurance Company and the Company is confident of realizing the balance amount on final determination of the loss and completion of the related activities

^^ Insurance money will come in.

And what is the vendetta wrt politics here ? can u please explain if possible.

Hi Gaurav,

I was referring to the pollution case as vendetta politics possibility…( The promoter is a politician and part of the opposition in the state of Andhra Pradesh) …

With respect to the fire incident, getting claim is one thing, there is also production loss, time loss in rebuilding the lost capacity, government enquiry into the safety aspect which may not renew factory licence and most of all doubts on management credibility as well at times, if this repeats like a loop every few years…

As some Institutions holding large positions also exiting the company and these circumstances prevailing I was weighing the pros and cons before taking a position in this company…

As @harsh.beria93 had attended the AGM my query was directed towards getting a first hand account of whether the management spoke about it, did a shareholder question the management on the same…

2 Likes

I might be splitting hairs here, but here is what I can see from the monthly chart of the company. From the lows of 470 in 2014 June, after AP was divided into 2 states, and the new government is formed in the residual AP, price made the ATH of 1128 in 2015 August, 2.4 times in 15 months. Then the price went into difference consolidation phases. Price did not fall any further, despite the change of power in 2019 June, and then came the 2020 March fall, and the subsequent rise, and then again the fall from the highs of 1025 to 438, with the PCB issue, company wanting to move out of AP and go to Tamil Nadu, and the rise in last 1 year.

I don’t know how much of the price movements are related to the business of the company, EV theme, or any other tailwinds or headwinds. I have not the slightest idea. And I don’t know if the MP is active w.r.t politics or things that pertain to his company, or if he wants to contest the next term from the same party or another party. And of course, all of this has been and will be very well known to the participants.

Just providing an observation, had a position long back, not invested now.