Listened to the entire concall. Notes below(I may have misheard some parts. Not a sebi advisor)

Risn pharma did a milestone payment of 26 crores.

ROW(regulated markets in Canada, Europe, Australia) and Api growth will continue next quarter. Chinese supply is back in the market for api but since alembic caters to premium no pricing pressure for alembic yet. Under invested in api right now… 400 to 500 crores capex in api and injectables next 2 years and approx 300 crores in maintenance capex. 6 products to be launched in Q4.

Domestic branded growth in specialty was good and will continue. Cough and cold should slowly get back to normalising in Q4 due to the vaccine. Growth in India was due to older brands. New brands will take a few years to pick up. Trade practices set pre pandemic helped. Post covid we ll now see even more growth in India since covid was a hindrance to it.

Regards USA, last 8 quarters provided loads of opportunities which are now slowing down. Sartans slowing down is the main factor and won’t reach previous quarter highs for some time. Launches from last quarter only contributed for few weeks end of December. No short term guidance but did mention usa should be similar to Q3 but very bullish on Us market over 2 to 3 years(400 to 500 million USD by FY 24)

Debt of 600 crores will be paid off by FY 23(ncds) ie 100 crores in FY 22 and rest in FY 23

R&D to come down to 9 percent or so over the next few years

Also, via interview MD Shaunak Amin doubled down on 60 eps for this year and 50 eps for next year so expect 250 crores+ for Q4. Mentioned that specialty growth in India will continue too and cough cold/antibiotics will improve with the market trend. USA growth had been continuous for 10 quarters and now slowed down but new base is set and they’ll move on from here(in concall mentioned that will move from current 280usd million to 400/500 over the next 3 years). Usfda still not visiting sites but approvals will continue… Approx 8 approvals expected this quarter. Recent qip helped bring debt down from 1700 to 300 crores. Link to the interview is below.

My thoughts based on all the info I’ve gathered via results/concall/interview/general pharma cycle is that:

FY 23/24 looks like it’s going to be an inflection point for alembic pharma and market is being very short sighted/over reacting right now.

By then Capex will start firing, loads of patents are ending and all alembics approvals will be completed by then and they’ll be ready to capitalise, debt will reduce, usa market will have grown by 50+ percent, domestic/api/ex USA growth will reduce dependancy on USA (post 500 million USD management has mentioned that usa will be difficult to grow quickly earlier), r&d spend will have reduced… all of the above leading to improved and sustainable margins and free cash flows.

Theoretically we could have a long period of consolidation while the market waits for capex spends and debt to clear in FY22 so there could be short to mid term pain(which depending on the type of investor you are could be a bad thing/could be a good thing for accumulation purposes) but markets are forward looking so you never know.

In a bear case scenario there is an argument all of the above mentioned factors may not happen but the pharma cycle overall looks like it’s on an uptrend and Alembic has a lot of factors that could keep it immune even if it slows down(and its not like it’s valuations are through the roof either)

Isn’t exposed to currency issues with emerging markets

Undeterred by china coming back into the conversation (as per concall) due to premium APIs

Spending more than their peers on R&D and have a clean history of approvals… which bodes well for their pending approvals and a move to complex generics which will help when the inevitable pricing pressures comes in.

Disc: invested. Not a sebi advisor. Not a buy/sell recommendation

Thanks @barathmukhi

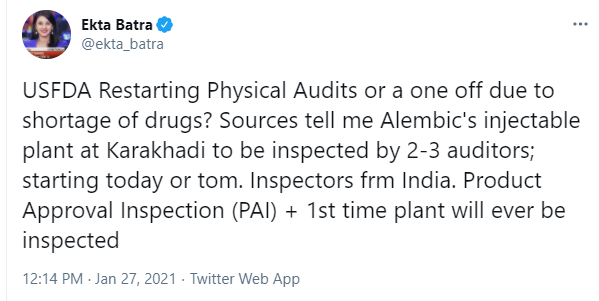

Looks like it’s been confirmed.

Here’s the video from CNBC regards the Pre Approval audit

Here’s info about pre approval inspections in general for those interested:

Surprising news that this has happened so early and the tension attached to physical audits is officially back in pharma … Hopefully everything goes through without issue. Could be huge if passed since getting a sterile unit approved is no mean feat and the wait for this has been a while now(and I wonder if contribution from here and the drug shortage that has led to this inspection has been factored in current Eps guidance by management or not)

US FDA inspection of Alembic new factory as per CNBC is being carried out by scientists employed by USFDA in India. This suggests that USFDA representatives need not take up the risk of traveling during pandemic to carry out inspection work. This has far reaching implication for entire industry.

Alembic of course stands to gain a lot if it gets approval #learning .

“… the first NCE discovered by Indian scientists to secure a US FDA approval…”

A milestone day for Rhizen, Alembic and India. This approval is for Marginal Zone Lymphoma/MZL and Follicular Lymphoma/FL.

The approval for Chronic Lymphocytic Leukemia/CLL (expected in Cy21) will be a lot bigger. The CLL phase 3 success has changed TG Therapeutics stock price from $11 to $52 in 7-8 months.

TG Therapeutics - Annual Report 2015 // same is repeated in 2019 AR

In September 2014, we exercised our option to license the global rights to TGR-1202, thereby entering into an exclusive licensing agreement (the “TGR-1202 License”) with Rhizen Pharmaceuticals, S A (“Rhizen”) for the development and commercialization of TGR-1202. Prior to this, we had been jointly developing TGR-1202 in a 50:50 joint venture with Rhizen.

Under the terms of the TGR-1202 License, Rhizen received a $4.0 million cash payment and 371,530 shares of our common stock as an upfront license fee. With respect to TGR-1202, Rhizen will be eligible to receive regulatory filing, approval and sales based milestone payments in the aggregate of approximately $175 million, a small portion of which will be payable on the first New Drug Application (NDA) filing and the remainder on approval in multiple jurisdictions for up to two oncology indications and one non-oncology indication and attaining certain sales milestones. In addition, if TGR-1202 is co-formulated with another drug to create a new product (a “New Product”), Rhizen will be eligible to receive similar regulatory approval and sales based milestone payments for such New Product. Additionally, Rhizen will be entitled to tiered royalties that escalate from high single digits to low double digits on our future net sales of TGR-1202 and any New Product. In lieu of sales milestones and royalties on net sales, Rhizen shall also be eligible to participate in sub licensing revenue, if any, based on a percentage that decreases as a function of the number of patients treated in clinical trials following the exercise of the license option. Rhizen will retain global manufacturing rights to TGR-1202, provided that they are price competitive with alternative manufacturers. The license will terminate on a country by country basis upon the expiration of the last licensed patent right or any other exclusivity right in such country, unless the agreement is earlier terminated (i) by us for any reason, (ii) by either party due to a breach of the agreement.

Pursuant to our license for TGR-1202 with Rhizen, we have the exclusive commercial rights to a series of patent applications in the U.S. and abroad. Thepatent applications include composition of matter patents relating to the structure, mechanism of action, and formulation for TGR-1202 as well as method of use patents which cover use of TGR-1202 in combination with various agents and for various therapeutic indications. Our composition of matter patent for TGR-1202 has been issued in the United States, which affords patent protection until 2033, exclusive of patent term extensions. All other patent applications currently filed for TG-1202 are currently pending. Because the dates for any potential regulatory approval are currently unknown we cannot predict the expected expiration date, and it is possible that the life of these patents following regulatory approval could be minimal.

371,530 Share (worth ~20 Million in Feb 2021 @55$ per share )

First New Drug Application (NDA) filing - What date this correspond to?

Is it safe to assume 20 Million annual benefits to Rhizen for next 10 years on lower side?

Umbralisib is indicated for treatment of adult patients with relapsed or refractory marginal zone lymphoma (a type of cancer)

First new chemical entity discovered by Indian scientists to secure a US FDA approval.

To be launched by early-next month in the US market, Umbralisib was discovered by Rhizen Pharma and subsequently licensed to Nasdaq-listed TG Therapeutics at an investigational new drug (IND) stage in 2012.

Rhizen Pharmaceuticals is co-owned by Alembic Pharmaceuticals with 50 per cent stake while the rest is held by by Dr Swaroop Vakkalanka, the President & CEO of the company.

In 2014, Rhizen Pharmaceuticals and TG Therapeutics entered into a licensing agreement as a part of which TG Therapeutics obtained worldwide rights while Rhizen retained commercialization rights for India. Also Rhizen remains the manufacturing and supply partner for Umbralisib.

TG Therapeutics has now bagged the regulator’s nod for the US market and will now market the novel drug under the brand name ‘Ukonig’.

Rhizen would get high single digit royalty on net sales of the product globally

Vakkalanka stated that the estimated market size for the drug is $7-8 billion per annum. "At peak sales, Ukoniq is expected to reach between $1-1.5 billion.

Alembic Pharma expects another 9-12 months for data to be ready for working towards a launch in India.

The company is awaiting USFDA inspection for F2, F3 and F4 plants that will manufacture oncology injectables and oral solid dosage (OSD), general injectables as well as OSDs

The drug took around eight years since inception of phase one development in early 2013 to getting USFDA nod now.

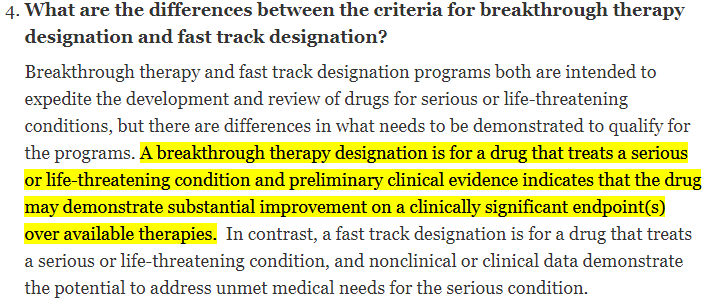

Umbralisib was earlier granted Breakthrough Therapy Designation (BTD) for the treatment of MZL and orphan drug designation (ODD) for the treatment of MZL and FL. More on Breakthrough therapies here

12th February, 2021

Alembic Pharmaceuticals announces its wholly-owned subsidiary, Alembic Global Holding SA receives USFDA Final Approval for Treprostinil Injection, 20 mg/20 ml (1 mg/ml), 50 mg/20 ml (2.5 mg/ml), 100 mg/20 ml (5 mg/ml), and 200 mg/20 ml (10 mg/ml), Multiple-Dose Vials.

Alembic’s maiden injectable ANDA approval. Indicates Karkhadi injectable facility (F-3) has green signal from the US FDA. The F-3 EIR announcement is a formality now.

Edit done on Feb 22, 2021 (07.11am)

Incorrect conclusion above. This ANDA approval is no green signal for F-3 Karkhadi facility. This is Corden Pharma S.p.A. manufacturing as per source here. No mention of Alembic Karkhadi plant in there. My apologies for reaching wrong conclusion. Thanks to Amit Rajan and Manprit for writing.

I think the point here is whatever royalty that Rhizen will get will not be flown to Alembic unless Rhizen declares dividend to the extent significant enough for the royalty to flow to Alembic (or there any agreement to share the royalty with Alembic that I am not aware - pls. let me know if i am missing this).

On the other side, when the Rhizen value addition takes place via this way, the Alembic value increases by means of holding share. But market has always undervalued the holding chunk of a holding company as we know many many cases.

Does anyone know is they are serious observations or anything to be concerned about?e.g. one of the comment - equipment is not of appropriate design might not be a small observation if it is made for all the equipments

As per Alembic these are not related to data integrity but procedural in nature. It remains to be seen how Alembic would respond to these FDA observations with corrective actions. If there are no WL issues post the response, should not be a matter of concern

… Hopefully everything goes through without issue. Could be huge if passed since getting a sterile unit approved is no mean feat and the wait for this has been a while now(and I wonder if contribution from here and the drug shortage that has led to this inspection has been factored in current Eps guidance by management or not)

… Hopefully everything goes through without issue. Could be huge if passed since getting a sterile unit approved is no mean feat and the wait for this has been a while now(and I wonder if contribution from here and the drug shortage that has led to this inspection has been factored in current Eps guidance by management or not)