https://www.screener.in/insiders/details/48061/

Acquisition of 18,064 equity shares worth Rs 173.97 lacs by promoter & director

https://www.screener.in/insiders/details/48061/

Acquisition of 18,064 equity shares worth Rs 173.97 lacs by promoter & director

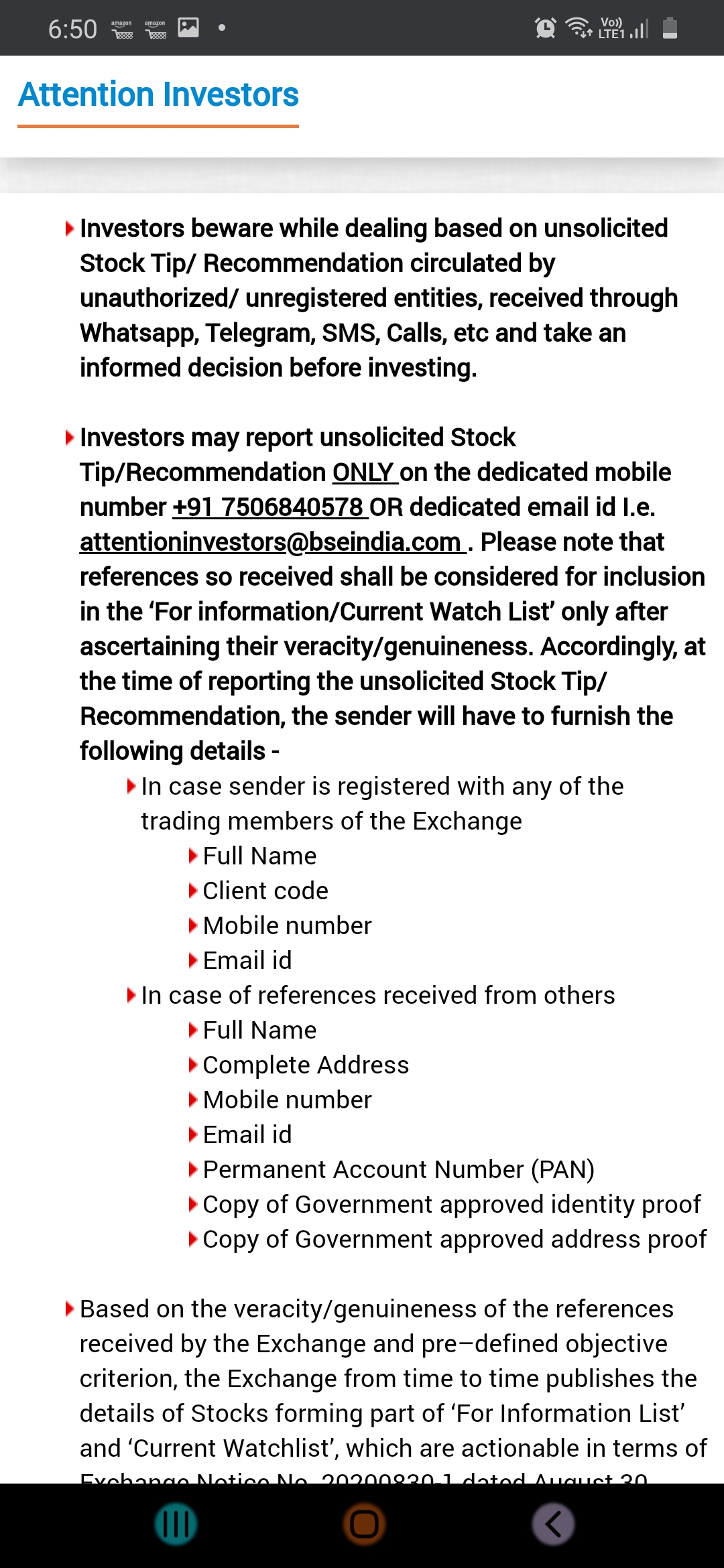

Alembic pharma has been under ‘watchlist for unsolicited messages’ for sometime…

Can anyone throw light on the exit criteria from this list?

Regards,

Abhijit

I wondered regards this too. Turns out it’s just a warning to potential investors tha a non sebi advisor is sending SMS/tips in some other fashion without the permission of the receiver. Someone must have complained regards the spamming and the warning has been put up. Not a list with any ramifications for alembic I think… just the spammer who sent the tips

It seems Alembic Pharma is no longer in this watchlist

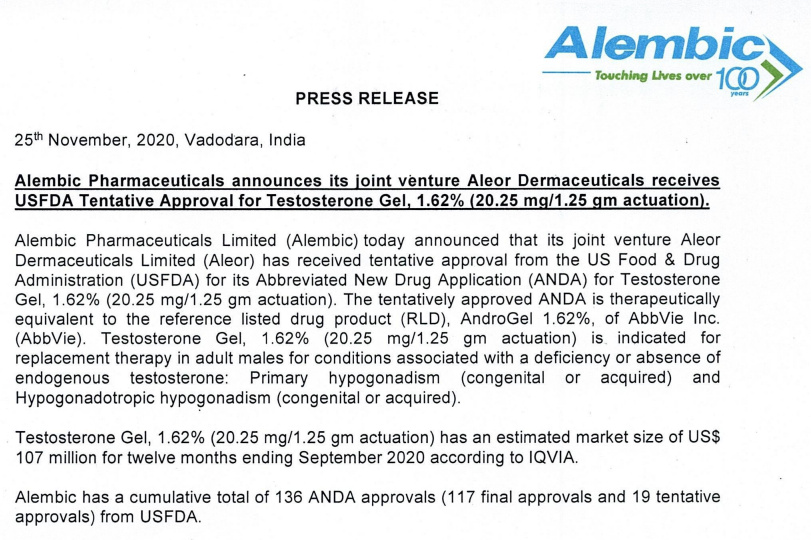

Regarding the press release which accompanies every ANDA approval, the estimated market size (for instance 600 million $ for Palbociclib) is always outlined.

On what basis should one estimate the probable market share for Alembic Pharma ? ( I know for this one, there is litigation ongoing with PFizer).

TG Therapeutics laid out post-approval launch plans which indicate that Umbralisib’s combo U2 is on track for an early 2021 filing ( Positive for Alembic as per a note published today by Jeffries) .

Alembic Pharma Q2 concall highlights -

Intl formulations sales at 779 cr, up 21 pc. US generics at 582 cr, up 8 pc. Last years base was high. Ex- US sales at 197 cr, up 84 pc.

API sales at 263 cr, up 30 pc.

Above guidance provided to allay fears and to assert that the current business is sustainable.

Disc : invested.

Last figure I am aware of regarding Alembic Pharma’s Management Compensation as a % of Sales was 1.40%. As far as I am aware, this is the highest in pharma sector, have there been any changes to this ?

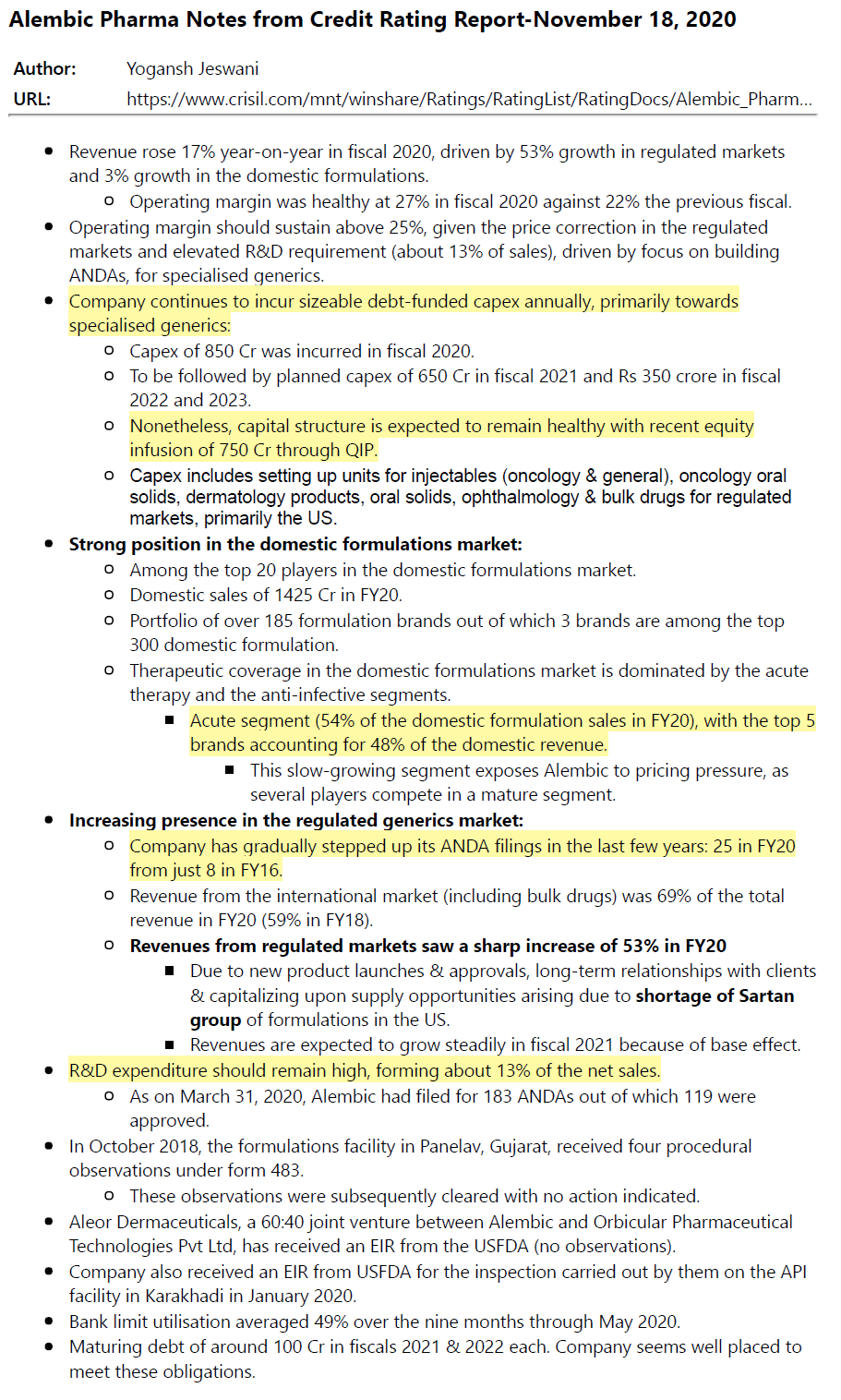

Hi All,

Sharing my notes from company’s latest credit rating report.

Regards,

Yogansh Jeswani

Disclosure: Invested

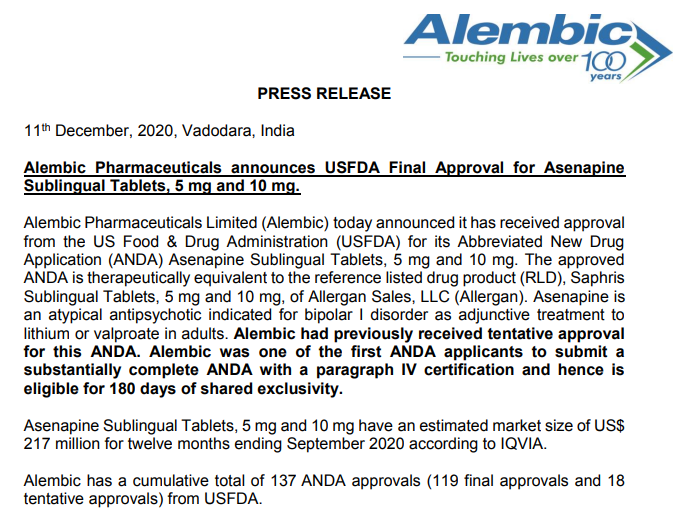

Another USFDA approval today:

Alembic Pharmaceuticals announces USFDA Final Approval for Metolazone

Tablets USP 2.5 mg, 5 mg, and 10 mg.

Alembic Pharmaceuticals Limited (Alembic) today announced it · has received

approval from the US Food & Drug Administration (USFDA) for its Abbreviated New

Drug Application (ANDA) Metolazone Tablets USP 2.5 mg, 5 mg, and 10 mg. The

approved ANDA is therapeutically equivalent to the reference listed drug product

(RLD), Zaroxolyn Tablets 2.5 mg, 5 mg, and 10 mg, of Lan nett Company, Inc.

Metolazone Tablets are indicated for the treatment of salt and water retention

including: a) edema accompanying congestive heart failure; b) edema accompanying

renal diseases, including the nephrotic syndrome and states of diminished renal

function. Metolazone Tablets are also indicated for the treatment of hypertension,

alone or in combination with other antihypertensive drugs of a different class.

Metolazone Tablets USP 2.5 mg, 5 mg, and 10 mg have an estimated market size of

US$ 33 million for twelve months ending September 2020 according to IQVIA.

Alembic has a cumulative total of 137 ANDA approvals (118 final approvals and 19

tentative approvals) from USFDA.

Hi @topdog,

Stock recommendations are not given in valuPickr.

There is enough information on the history of the company,it’s future plans and opinions by many stalwarts of this forum

You are requested to go through these posts and conclude yourself.

Regards,

Abhijit.

The first part of the comment is for Dr Reddy’s.

In the second part of his tweet, he talks about inspection of Alembic’s new sterile unit.

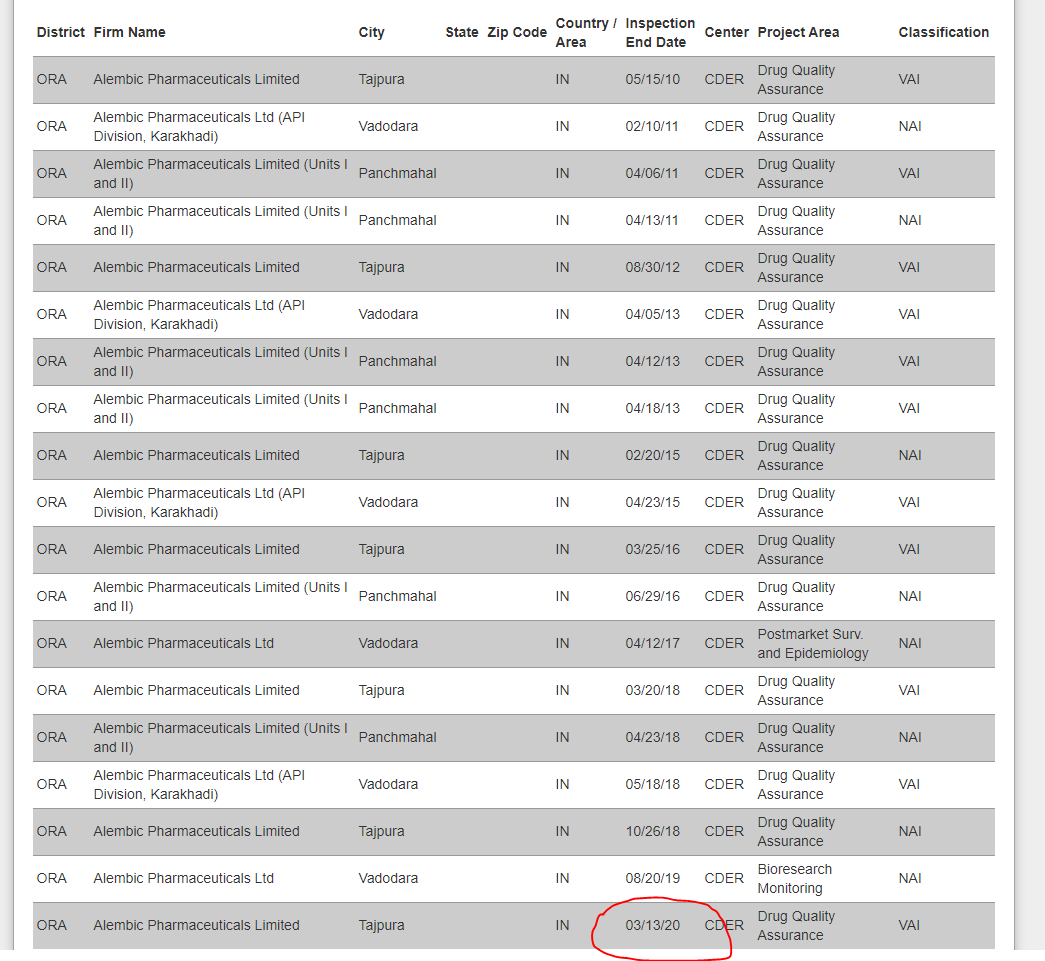

As per FDA site, their Tajpura site got inspected in March 2020.

https://www.accessdata.fda.gov/scripts/inspsearch/index.cfm

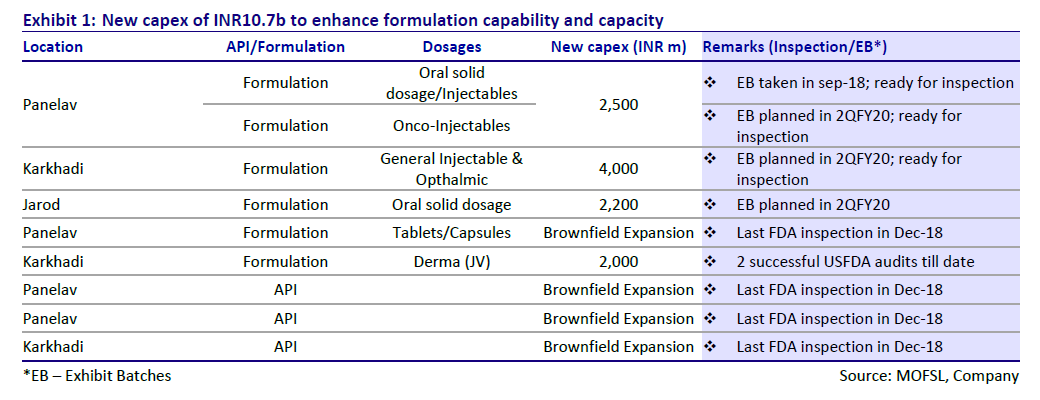

Any idea which one of these sites is the one for sterile?

https://www.alembicpharmaceuticals.com/manufacturing/

I am assuming it is their Panelav and Karkhadi plants.

I tried looking up but couldn’t find anything other than this comment from their May 2017 concall.

Also, my understanding is facilities don’t get inspected by the FDA for years, at a stretch, due to FDA’s internal reasons (logistical & political).

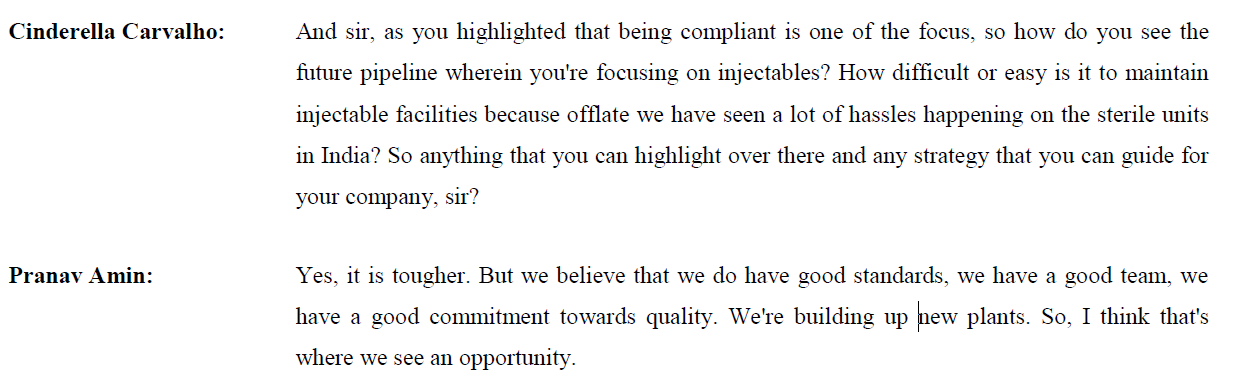

Wondering what implications an audit on one of their sterile facilities have, whenever it does happen?

Basically Sterile plant has stringent inspection criteria and passing inspection confirm that you have arrived on compliance front.

As per shareholding pattern for Dec’20 Qtr, LIC of India has entered Alembic Pharma with 1.01% stake:

CFO Interview on Dec 15, 2020:

Q3 Results

• Net Sales for the quarter up 9% to Rs 1314 crores from Rs. 1209 crores.

• Net Profit for the quarter up 25% to Rs 293 crores from Rs 234 crores.

• Net sales for 9M FY21 up 21 % to Rs 4113 crores against Rs 3399 crores.

• Net profit for 9M FY21 up 53% to Rs 927 crores from Rs 604 crores.