Fantastic material on the Sartans shortage causes. ![]()

![]()

Thanks a lot man!!

2 Likes

Dear @barathmukhi

Three vital data points are missing for us.

-

Total Market Volume of Azithromycin Tablets (No. of Million Tablets) in USA - base market size and potential COVID upside.

-

Market share of existing companies and the extent of drug shortage in market share terms that Alembic can capture

-

Net Selling Price realized by existing companies. Retail prices can differ from NSP realized by manufacturers by a huge range. Also the extent of drug shortage will determine the new NSP sustainable in market.

While, as you pointed out, Alembic may have the capacity to manufacture 10 Crore Azithromycin tablets per month; USA demand might be far lower. Assuming that 20 Mil. US population takes one time Azithromycin course of 6-12 tablets, the COVID specific upside may be 120 to 250 Mil. Tablets.

This is a broad assumption. Also, whats the base market volume of Azithromycin and what’s the share the other competitors have?

Lets see what the current info. on FDA Drug Shortage page says:

[Ignoring 600 MG strength as the major vol. is 250 and 500]

- Alembic - Available / June 2020 launch for 250 MG and 500 MG

- Aurobindo - Additional supply to be available in May 2020 - 250 MG 6x3 Blister SKU only

- Bionpharma - Currently unavailable; Expected to become available early June 2020 - 250 MG and 500 MG

- CSPC Ouyi - Limited supply in the second quarter of 2020 - Both strengths

- HEC Pharma - Available - 500 MG 3x1 Blister SKU only

- Lupin - Continuous production. More products are in transit and will be available for distribution within next few weeks - 250 MG - 3x6 Blister SKU only

- Pfizer - Available, Next delivery: June 2020 Estimated recovery: TBD, Next delivery: June 2020 Estimated recovery: TBD - 250 MG and 500 MG SKUs

- Sandoz - Available - 250 MG and 500 MG - 30 count Bottle SKUs only

- Teva - Available - A backorder is anticipated. The estimated duration is unknown at this time. Product allocations being made based on customer Rx Trends. 250 MG and 500 MG - All SKUs

- Wockhardt - Unavailable.

So, including Alembic, there are 9 companies who are supplying the drug in some SKU form. Out of these 9, around 6-7 seem to be holding DMF as well. [Aurobindo, Pfizer and Bion are the ones for which I couldnt see a DMF.]

So while there is definitely an upside opportunity for Alembic, the size CANNOT be quantified. And based on the existing shortage info. supplied by manufacturers, the upside seems quite limited.

This is my reading of the situation today.

11 Likes

Hello… Those are some really thoughtful questions. Market volume / market size is a huge unknown in this situation, given that it is too premature to say what combination of drugs will really turn out to be the ultimate cure. What volumes of Azithromycin will get sold this year? Nobody knows.

On the flip side, I think it would still be reasonable to assume, Alembic might be able to sell every unit of Azithromycin it produces this year to other countries, if not the US. This is based on the fact that shortage for the drug continues, at least in America, as of now. This is also based on the assumption that Hydroxychloroquine & Azithromycin will continue to be used until a viable solution is found.

Volume growth / market share is an unknown given that the situation is a rapidly evolving one and has no precedents. As investors, the best we can do is to stay on top of the situation, by evaluating whether or not it is going in the direction we anticipated, as and when more data points become available.

So based on what we already know, Alembic is the largest player in selling active pharmaceutical ingredients (APIs) of azithromycin to the world. This means other players are likely to be dependent on this company for their supplies. I equate this situation to Peter Lynch’s quote -

When there’s a war going on, don’t buy the companies that are doing the fighting; buy the companies that sell the bullets. Effectively, Alembic is doing both - Fighting the war (by selling the branded drug) as well as making the bullets (by selling APIs to companies like Pfizer).

So while volume growth is an unknown, the company might still benefit from realization growth / margin expansion, given that API prices have doubled too.

Having said this, I understand the risks involved and beleive the downside is capped while the upside looks decent and could change quickly as and when the situation evolves.

6 Likes

alembic in more news

5 Likes

Stumbled upon a few more links, this morning.

One of the many articles which show doctors are prescribing other medications over hydroxychloroquine & azithromycin

Other therapies now favored over hydroxychloroquine at area hospitals in Hudson County

2 Likes

Number of openings for Alembic- mostly recent days and most of them direct sales.

https://www.naukri.com/alembic-pharmaceuticals-limited-jobs-careers-47

2 Likes

Alembic Pharmaceuticals on Thursday said it has received final approval from US health regulator for its generic doxycycline hyclate tablets used for the treatment of adult periodontitis. The approved ANDA is therapeutically equivalent to the reference listed drug product Periostat Tablets, 20 mg of Galderma Laboratories, LP.

Citing IQVIA data, Alembic said doxycycline hyclate tablets 20 mg have an estimated market size of USD 53million for the 12-month period ending December 2019.

1 Like

PRESS RELEASE

15th May, 2020, Vadodara, India

Alembic Pharmaceuticals announces USFDA Final Approval for Doxycycline

Hyclate Tablets USP, 100 mg.

Alembic Pharmaceuticals Limited (Alembic) today announced it has received

approval from the US Food & Drug Administration (USFDA) for its Abbreviated New

Drug Application (ANDA) Doxycycline Hyclate Tablets USP 100mg. The approved

ANDA is therapeutically equivalent to the reference listed drug product (RLD)

Vibra-Tabs, 100mg of Pfizer, Inc. Doxycycline Hyclate Tablets USP 100mg should

be used only to treat or prevent infections that are proven or strongly suspected to

be caused by susceptible bacteria. When culture and susceptibility information are

available, they should be considered in selecting or modifying antibacterial therapy.

In the absence of such data, local epidemiology and susceptibility patterns may

contribute to the empiric selection of therapy. In acute intestinal amebiasis,

doxycycline may be a useful adjunct to amebicides. In severe acne, doxycycline may

be useful adjunctive therapy. It is also indicated for the prophylaxis of malaria due to

Plasmodium falciparum in short-term travelers (<4 months) to areas with chloroquine

and/or pyrimethamine-sulfadoxine resistant strains.

Doxycycline Hyclate Tablets 100mg have an estimated market size of US$ 53 million

for twelve months ending December 2019 according to IQVIA.

Alembic has a cumulative total of 121 ANDA approvals (108 final approvals and 13

tentative approvals) from USFDA.

1 Like

While both the stocks and company have been doing good in recent times I could not find update on 3yr old PANAMA case and drinking party case that was charged against promoters

One more thing I was curious about was of [Archana Hingorani] who is independent director though it is not criminal but still good to know what kind of people past record/behaviour of people company associates itself with.

The most high-profile among these exits was possibly that of Archana Hingorani who was executive director and CEO of IL&FS Investment Managers till she stepped down in April 2017, after a stint of eight years at the group.

Disclosure: Very small allocation and trying to find above answers before making any further decision.

2 Likes

Dear All,

Please find attached stock story brief on Alembic Pharma.

Cheers

Alembic pharma_VP Stock Story Version 1.1.docx (62.2 KB)

35 Likes

Alembic Pharmaceuticals announces its joint venture, Aleor Dermaceuticals receives

USFDA Approval for Clobetasol Propionate Shampoo, 0.05%.

The approved AN DA is therapeutically equivalent to the reference listed drug product (RLD), Clobex Shampoo, 0.05%, of Galderma Laboratories, L.P. (Galderma). Clobetasol Propionate Shampoo, 0.05% is indicated for the treatment of moderate to severe forms of scalp psoriasis in subjects 18 years of age and older.

Clobetasol Propionate Shampoo, 0.05%, has an estimated market size of US$ 28 million for

twelve months ending December 2019 according to IQVIA.

Alembic has a cumulative total of 122 ANDA approvals (109 final approvals and 13 tentative

approvals) from USFDA.

HI Yachna,

Good job so far on capturing what is to be known, can be known about the business.

It’s very good - as a more-or-less commentary on the business.

Some observations/pointers for improvement

- Improvements will come in - when we have better perspective on this show put up by Alembic over last 10 years. And how will better perspective come in?

a) Peer Comparison - seems to be completely missing in this attempt - (prompts to that from Management Q&A?). Read the Q&A carefully - note our line of questioning too.

b) Pondering on “Opportunity Shortage” - Could this be the new game in town? Have they designed and orchestrated the US Generics game differently than others? IF so - what are those differences?

c) Is it a high-risk high-growth being pursued, or is it a No-brainer - given their execution planks - what are the pillars of that execution track record; Relationships - what are the pillars of those relationships; Longevity and Sustainability - What are the pillars of that?

d) Risks - Needs much better thinking through - its only an enumeration right now. What are the Risk MItigation processes/strategies employed by the business. And how do these stand out? - Thinking through deeper - 2nd order thinking - may provide better insights.

Now how do we enable us to think through deeper?

Simple - Now that you have done all the hard work - know all that is to be known/can be known on the business including Competition/Industry perspective - Just attempt a “Deep Dive” using the Processor Deep Dive Template. Think that the Processor-Template will be enough to do justice - and will force you to think on new lines/lines that may have been missed - your attention may be forced to - what are the most important things that move the needle - for both US Generics/Domestic Markets.

Alert me if the Template lacks something. We can talk, and I will offer a Pharma specific Deep Dive Template if needed.

Thanks for your sustained effort and perseverance. This is a high-quality effort again. All newbies and learners (must download) can take inspiration from this sincere complete effort. The sincerity (of the quest) shines through and through, and thus energised me to respond quickly on prompting by Hitesh.

10 Likes

Hi @Donald how you see current QIP of 1200 cr announce by company. ?

@hiteshchauhanca If you are referring to this announcement, I read it as announced.

In my view, this seems to be an enabling resolution (should premium valuations be available down the line) - so they would be ready to utilise opportunities. One can take a more nuanced call when we cross the bridge - when further announcements/details are provided. The timelines need NOT be tomorrow.

Having been interacting with Alembic Management since 2012, my views can certainly be biased. They had just finished an aggressive capex program. Ideally they would have been looking to consolidate for a couple of years. That is the clear indiction we got form Concalls and VP Alembic Mgmt Q&A, that 300 Cr Maintenance Capex was what was being seen as the annual capex spend run rate in the medium term. Internal accruals could take care of that.

However, if we read the fine-print closely, some of the “significant” developments mentioned in March Concall were a) seeing big opportunity in scaling up on API front b) “large interest and a large stake” in Azythromycin trials.

This announcement tells me that there is good visibility and traction/progress on probably both fronts (Azythromycin traction is perhaps known?). They might be considering it necessary and prudent to raise capital sooner than later to harness the opportunities before it. We know by now, that they are inherently “aggressive” on their strong areas (refer Alembic Pharma Management Q&A). Utilisation of funds could be for a) paring down current debt levels b) new capex program planned

My views are inherently biased - invested from earlier levels.

I am in favour of Managements that show the confidence of diluting at “premium” valuations. Having said that Alembic valuations currently are NOT premium ![]()

I would think Alembic Management is pretty savvy to know when to dilute, and get that roughly right!

This view could be proven totally wrong. It’s just a view. As I said before, better to cross the bridge when we actually come to it.

13 Likes

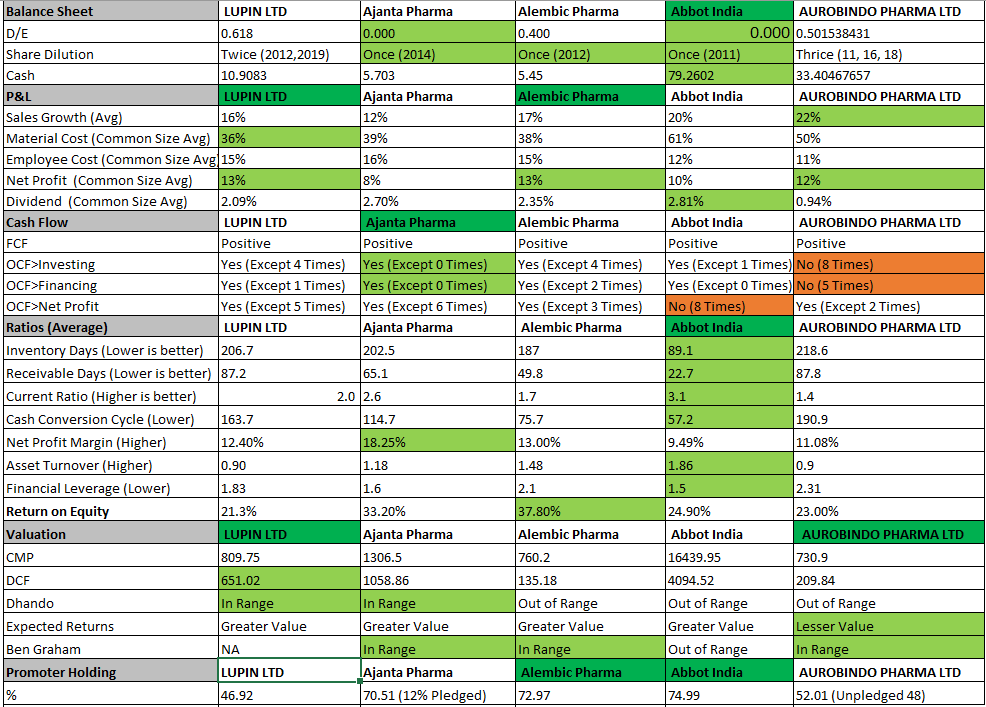

I did a Quantative Peer Comparision on the some of the Pharma names and below is my analysis. Please suggest if any improvements on the Comparision

Technically i see the trend is up in the Guppy.

Disclosure: I am invested in Alembic, Ajanta and Lupin

12 Likes

Excellent report, thanks for sharing. Will companies like Cipla get a higher advantage for their partnership with with Gilead ?

Interesting article on how pharma companies are ferrying their employees to work during lockdown and what measures are being taken to avoid infections at plants.

The Gujarat-based Alembic Pharmaceuticals deployed 120 buses with only 23 employees travelling in each bus to ensure social distancing.

4 Likes

Have added some more ground work on Alembic-:

ANDA Approval database

Listed below all the ANDA approvals received by Alembic / Aleor over the last 1 year, along with

- the estimated market size of the drug for previous 12 months, and

- Other companies which have received approval for the same (I could not find some data (shown as ? in table below); Pharma experts: pls help here )

| Approval Date | Drug Name | Drug size $ mn | Other players |

|---|---|---|---|

| May-20 | FAMOTIDINEANDA #078916 | 28 | Apotex, Aurobindo, Dr Reddys, Perrigo, Carlsbad etc |

| May-20 | DOXYCYCLINE HYCLATEANDA #210536 (100mg) | 53 | Actavis, Cadila, Emcure, Mylan, Novel Sun Pharma etc |

| Apr-20 | ALCAFTADINEANDA #209290 | 7 | ?? |

| Mar-20 | DOXYCYCLINE HYCLATEANDA #210537 (20mg) | 7 | Asun pharma, Heritage, Larken Labs, Epic etc |

| Jan-20 | CLOBETASOL PROPIONATEANDA #213291 | 57 | Mylan, Lupin, Glenmark, Torrent, Zydus , Taro, Rising |

| Jan-20 | VILAZODONE HYDROCHLORIDEANDA #208202 | 469 | Allergan, Alembic pharma, 180 days of shared exclusivity with Allergan on signing of settlement agreement with Allergan – This seems big with no other player. How do we get more details here? |

| Jan-20 | TIZANIDINE HYDROCHLORIDEANDA #213223/Emapgliflozin Tablets | 3400 | Alkem, Casi Pharma Inc, Dr Reddy Labs, Mylan, Sun Pharma, Unichem, Zydus |

| Jan-20 | FENOFIBRATEANDA #213252 | 100 | Aurobindo, cipla, lupin, mylan, sun pharma etc |

| Jan-20 | BIMATOPROSTANDA #210515 | 57 | Apotex, allergan, sandoz, hi tech, |

| Jan-20 | BOSENTANANDA #211461 | 68 | cipla, sun, natco, zydus, par pharm etc |

| Jan-20 | AZITHROMYCINANDA #211793/91/92 | 131 | Sandoz, lupin, bionpharma, wockhardt etc |

| Dec-19 | ASENAPINEANDA #206098 | ?? | No other player looks like |

| Dec-19 | TRAVOPROSTANDA #210458 | ?? | Alembic, Par pharm |

| Dec-19 | DICLOFENAC SODIUM ANDA #212506 | 974 | Hitech, cipla, aurolife etc |

| Nov-19 | DEFERASIROXANDA #210060 (90 and 360 mg) | 415 | Alkem, cipla, MSN, Zydus, sun, etc |

| Nov-19 | DEFERASIROXANDA #211824 (125, 250 and 500mg) | 135 | MSN, Sun, Zydus, Novartis, alkem etc |

| Nov-19 | DEFERASIROXANDA #211824 (180 mg) | 59 | MSN, Sun, Zydus, Novartis, alkem etc |

| Nov-19 | SILODOSINANDA #211731 | 114 | Aurobindo, ajanto, hetero, lupin ,acleods etc |

| Oct-19 | DESONIDE ANDA #212473 | 13 | glenmark, taro, hi tech pharma etc |

| Oct-19 | CLOBETASOL PROPIONATE ANDA #211191, 212881 | 55 | glenmark, macleods, taro, wockhardt, hi tech pharma etc |

| Aug-19 | DORZOLAMIDE HYDROCHLORIDEANDA #212639 | 35 | alembic, FDC, hitech pharm, micro labs, sandoz |

| Jul-19 | FEBUXOSTATANDA #205421 | 578 | Mylan, sun , MSN, indoco etc |

| Jul-19 | ACYCLOVIRANDA #209000 | ?? | Apotex, cadila, cipla, torrent, mylan etc |

| Jul-19 | PREGABALINANDA #203459 | 5470 | alembic, alkem, cipla, dr reddys, hetero, msn, hikal, sun pharma etc. |

| Jul-19 | DAPAGLIFLOZINANDA #211560 | 1700 | alkem, glenmark, teva, ajanta, biocon, micro etc |

| Jun-19 | CARBIDOPA AND LEVODOPAANDA #210341 | ?? | apotex, mylan, impax, sun pharma |

| Jun-19 | BROMFENAC SODIUMANDA #210560 | ?? | Gland, hitech, mylan |

| Jun-19 | OSELTAMIVIR PHOSPHATEANDA #211823 | 647 | hetero, lupin, natco, macleods, roche etc |

| Jun-19 | CLONAZEPAMANDA #211033 | 20 | Par pharm, sun pharma, Barr |

| May-19 | SOLIFENACIN SUCCINATEANDA #205575 | 967 | ajanta, alkem, cipla, glenmark, msn, strides, unichem etc |

The summary of the above is that there is competition, in each and every molecule (barring two highlighted in bold). Competition is even larger in the bigger size molecules and therefore the product approval here doesn’t seem to be the differentiator for Alembic’s performance thus far.

So, what has contributed to the differentiated performance?

- Drug shortages - They definitely have been lucky with the Sartans where the shoratges have continued for fairly long and the mgmt. indicated that this is likely for to continue for another 3-6 months.

I looked at the latest drug shortages on US FDA to verify this and surprizingly, there are no sartans showing in shortage currently. Should this be a concern from short term perspective? Is there any way to find the trend in sartan prices? If anybody can help here.

Also, another important to note, that from Alembic’s perspective, following drugs are in shortage in the US currently –

- Azithromycin Tablets – Expected - While 8-10 companies have received the approval, it is in shortage and currently available for supply with less than 5 companies, including Alembic. They have a very large capacity here and could be a key beneficiary.

- Famotidine Tablets – This also has approvals from 5+ companies but currently Alembic seems to be the only supplier. Aurobindo expected to supply from 15th June and the rest of them by Q4 FY 20.

Separately, Aurobindo seems to be in a good position with drug shortages in many of their products.

- They have a very nimble supply chain which enables them to meet the above drug shortages at a short notice – this is a result of various factors like

- Compliant plants with strong regulatory focus on a continuous basis

- Adherence to manufacturing schedule with flexibility to modify it depending on opportunities

- Product selection

- Strong relationship with buyers with track record of consistent supplies

- US FDA policy of fast track approvals have also helped them cover up their delayed entry in the US markets as compared to their peers (though in longer run it reduces the IRR).

Will add more as I work. Meanwhile request pharma experts to help fill up the gaps.

29 Likes

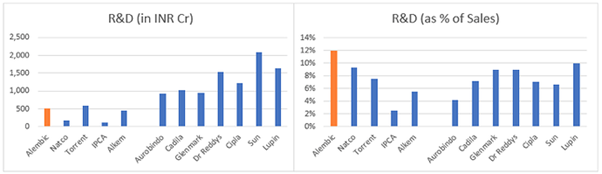

R&D expenses

One of the concerns was the high R&D expenses as % of sales c. 13-14% of sales vs 4-8% for most other pharma companies (see chart below). The plausible explanation was the accelerated investment program of Alembic as compared to other players, on account of their late entry into US markets. (Pic source mgmt q&a).

To verify the above, I compared the total R&D expenses across few pharma companies over last 10 years divided by the incremental ANDA filings done by them in this period – to get an average R&D cost per filing over the years (see attached excel for details).

| Name | Avg R&D Cost per ANDA in Rs crs |

|---|---|

| Ajanta Pharma | 19.0 |

| Alembic Pharma | 18.8 |

| Torrent Pharma | 27.6 |

| Lupin | 44.7 |

| Cipla | 26.9 |

| Aurobindo Pharma | 18.2 |

The above methodology is only an approximation as it does not consider non-US sales of the company, sample set for comparison is small, does not consider time lag between R&D expense and ANDA filing, complexity of pipeline etc. But overall, over 10 years it averages out some of these elements. And this data broadly tells us that Alembic’s R&D costs are in line with competition and seem high as % of sales only due to the accelerated R&D program.

The same thing is also evident in the table below – which shows that Alembic has higher ANDA filings and higher pending approval ANDAs relative to the sales of the company:

| Name | Last 1-year turnover (annualized) | ANDA Filings | ANDAs pending approval |

|---|---|---|---|

| Ajanta Pharma | 2,588 | 55 | 23 |

| Alembic Pharma | 4,612 | 183 | 64 |

| Torrent Pharma | 7,939 | 145 | 45 |

| Lupin | 16,092 | 424 | 152 |

| Cipla | 17,132 | 259 | 62 |

| Aurobindo Pharma | 22,587 | 572 | 154 |

For instance, Cipla’s topline is 4x that of Alembic but number of pending approvals is similar and total filings is only c. 1.5x. This also reaffirms that as Alembic’s topline catches up, this aberration of high R&D expense % should correct, thereby aiding margins

alembic_R&D.xlsx (19.6 KB) .

29 Likes