One thing to consider while looking at the ANDA - Filing alone may not give the complete picture. Money is made when company files ANDA for niche drug with limited competition.Ex: Look at NATCO pharma. So its not the quantity of the ANDA that matter but how well company select molecule that matters a lot. Also, despite getting approval a molecule may not commercially viable when company actually start commercial production.

2 Likes

Nice work @YachnaBhatia, thank you - I had been wanting to do something similar and check if the R&D expenses being done are not too high as compared to peers. The R&D expenses/investments are being expensed out to P/L each year and are almost equivalent to yearly profits (almost like Ajanta 5-7 years back). As @Sanjay_Bakshi used to say - other way of looking at this is - as these are expenses which are of long term benefit in nature, in a way, the current earnings could be understated. But this holds true only if these R&D expenses are efficient and the company has a good pipeline.

If these expenses are efficient then a lot of value creation will happen in coming times.

20 Likes

No of ANDA fillings and approval is less meaningful data by itself .

What is Market size opportunity and competition in each of ANDA approvals it gets is key …

Some Pharma companies are very focussed and target few imp molecules with limited competition and high complexity … so while overall approvals may seem small for them - The ROI on each ANDA is very high .

Also many Pharma companies don’t launch products even after getting ANDA approvals becos of size and competition .

2 Likes

The purpose of this exercise was to just check why is Alembic’s R&D expenditure % to sales so high as compared to peers. Individual ANDA level analysis is important and has been elaborated in post # 521 above.

12 Likes

They found that between March 15 and 21 prescriptions for azithromycin, amoxicillin and the painkillers hydrocodone/acetaminophen declined, and rates for heart medicines remained stable.

In contrast, there was a dramatic surge in prescriptions for hydroxychloroquine/chloroquine: from 2,208 prescriptions in 2019 to 45,858 prescriptions in 2020 – an increase of more than 2,000%.

2 Likes

https://www.bseindia.com/corporates/anndet_new.aspx?newsid=5f8656b7-4c62-40ec-9e8e-1c1917226ece

ANNUAL REPORT FY 20 ALEMBIC PHARMA WITH VIRTUAL AGM THIS TIME

1 Like

Annual report for Alembic Pharma has been released.

Overall a good read. Have appended few interesting snippets below:

• We have accomplished some of the industry-leading return ratios, margins and have among the lowest receivables in the industry. Our debt levels are also contained below 1x and we are planning to deleverage our balance sheet in future. Our EBITDA margin has increased for the past four years in a row from 20% in 2016-17 to 26% in 2019-20. We enjoy attractive return ratios and with a significant portion of the capital expenditure behind us, these metrics are expected to improve further.

• US Business - Our agile and nimble supply chain clubbed with proactive front-end marketing helped us to lead growth in the US market. Our ability to deliver high-quality products in the required quantities, in a timely manner as per the customers’ convenience differentiated us from our peers. Consequently, we gained market share, solidified our bond with existing customers and added new customers during the year. With an accelerated pace of new product launches as well as ANDA filing, we are confident of sustaining this momentum in the future. We launched 22 new products in US as against nine products in 2018-19 and will be ramping up new product launches in the future.

• 90% of our R&D spends are directed towards the high growth US market. We continued to invest in R&D against the run of play with several generic players downsizing their US investments. This contrarian approach has paid rich dividend.

• Sartans - Another instance of how we do more with less is to identify niche product opportunities such as Sartans to achieve a healthy balance between growth and profitability. During 2019-20, we again demonstrated our ability to maximise opportunities in a short period, more efficiently than our peers. We believe, sartans opportunity will remain strong over the next three to six months and with 15 ANDAs across different combinations, we are well equipped to maximise its potential.

• US products - Yet, we have put in concentrated efforts on select products such as anti-depressant drug, Venlafaxine to mark our presence globally and generate sustainable returns with a diversified portfolio. Another product offering significant growth opportunities is Azithromycin, an antibiotic for bacterial infections. In India, we are one of the largest manufacturers of Azithromycin, with a 30% market share in India. Amid rising demand for the product, we have ramped up our production capacity for Azithromycin. This ramp-up is both for the domestic as well as international markets. The demand for Azithromycin has shot up significantly as it is being tried to treat coronavirus in combination with hydroxychloroquine in the US and several parts of Europe. We have secured final approval from the USFDA to launch Azithromycin in the US in January 2020 and have recently launched the product in the US. Azithromycin tablets have an estimated market size of $129 million for 12 months ended September 2019 according to IQVIA.

• In the non-US market, growth is likely to rebound in 2020-21.

• India business - Most of you would be aware of our strategic decision to focus on high potential, high-margin products (focus products) in the domestic market. We completed this transition in 2019-20 and started witnessing an uptick in performance in the last quarter of 2019-20. Our aim is to grow our presence in the specialty and chronic therapies segments. In 2020-21, we expect this business to grow in double digits in sync with the growth in the domestic market. Strong brand recall, an efficient sales force, a growing network of supportive doctors and timely product launches are the key catalysts for this business. Benefits of the portfolio and incentive rationalisation exercise expected to be visible starting 2020-21.

• API business - We believe there are immense opportunities in our current APIs including Azithromycin. The API business witnessed softness in 2019-20 due to lack of orders from a large manufacturing deal with an MNC. The rest of the business witnessed growth upwards of 20%+in the year. We believe this business is on a solid turf and expect it to grow by atleast 15-20% in 2020-21.

• Quality focus - The result is that we are among the few companies in the Indian pharmaceutical industry to have clean status for our USFDA plants.

• Operational efficiencies - For us, at Alembic, improvement in operational efficiencies is an on-going process. One example of this can be found in the way we manage our R&D function. We proactively scan our R&D grid to realign our product portfolio by mapping it with critical factors such as potential to garner desired market share and generate profits. Products that don’t fit the criteria are dropped from the grid. Thus, we ensure that our R&D efforts are moving in the right direction.

• US Front end - The US front-end is a credible example to demonstrate how we are optimising both short-term and long-term opportunities. With our unwavering focus on quality and customer-service, we have managed to build a loyal customer base in a short span of time. Close customer relationships have helped us to ensure we were key beneficiary of supply disruptions, despite having less than five years of US front-end experience.

• Auditor change – from KS Aiyar & Co to KC Mehta & Co for 5 years subject to shareholder approval – Still not a Big 4

• Promoter remuneration – c. Rs 65 crs (including commission linked to profits c. Rs 37 crs) – This is c. 7.9% of profits (vs 9% in FY 19)

• Three key products – Azithromycin, Venlafaxine, Valsartan

• Large increase in receivables has led to lower CFO – to be watched out- funded through incremental working capital loans

25 Likes

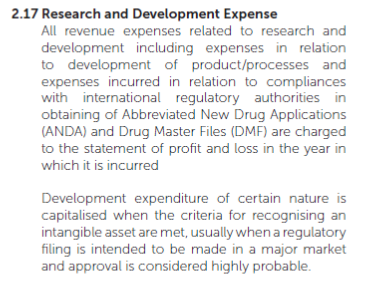

This extract is from the latest Annual Report - Accounting policies:

What’s the difference between the two? Can someone tell me exactly what expenses are charged to P & L and what are capitalized? An example will be useful to understand.

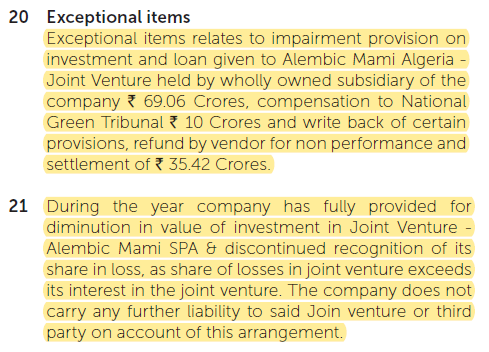

I want to highlight couple of items in FY20 AR that caught my eyes. FY2020 would had been even more bumper year from PAT standpoint had the company not taken below mentioned two hits in the P&L totaling 97.36cr:

1) Exceptional Loss of 43.65cr

2) Impairment of Goodwill of 53.71cr

Company did a good job to to explain the exceptional loss of 43.65cr, i.e. fully provided for diminution in value of investment in JV - Alembic Mami SPA discontinued recognition. Below is the screenshot from AR (page 161). This was shared with Q1FY20 results.

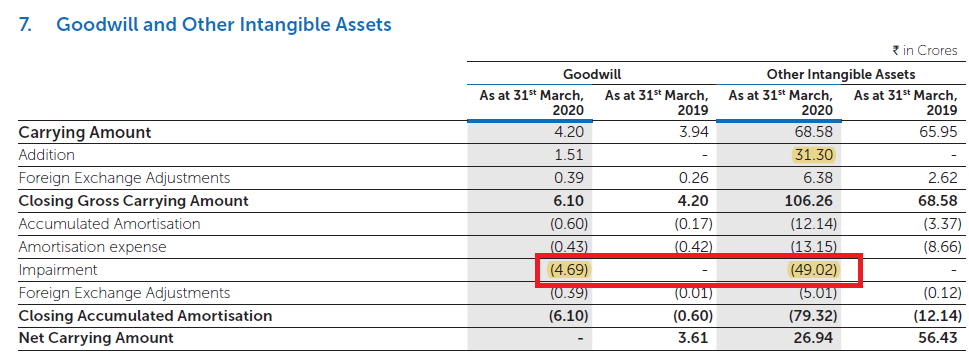

But I wasn’t able to find any details in the FY20 AR of 53.71cr hit that company took by reducing Goodwill. Screenshot below:

Major reduction coming from intangible assets. I wasn’t able to find any details that management has shared in the AR. If anyone finds anything that I missed, please share here.

Since its a goodwill item, its good to be vigilant and be top of the movement within Goodwill calculation.

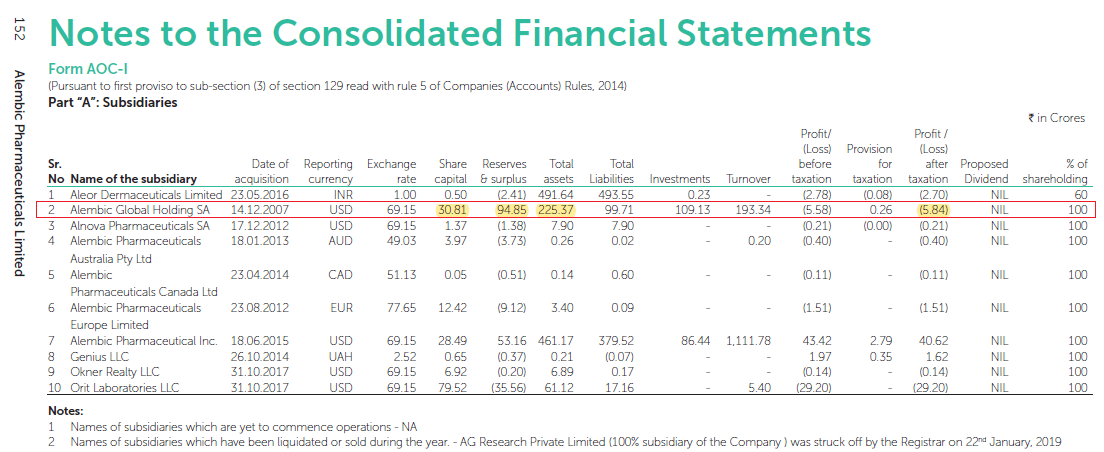

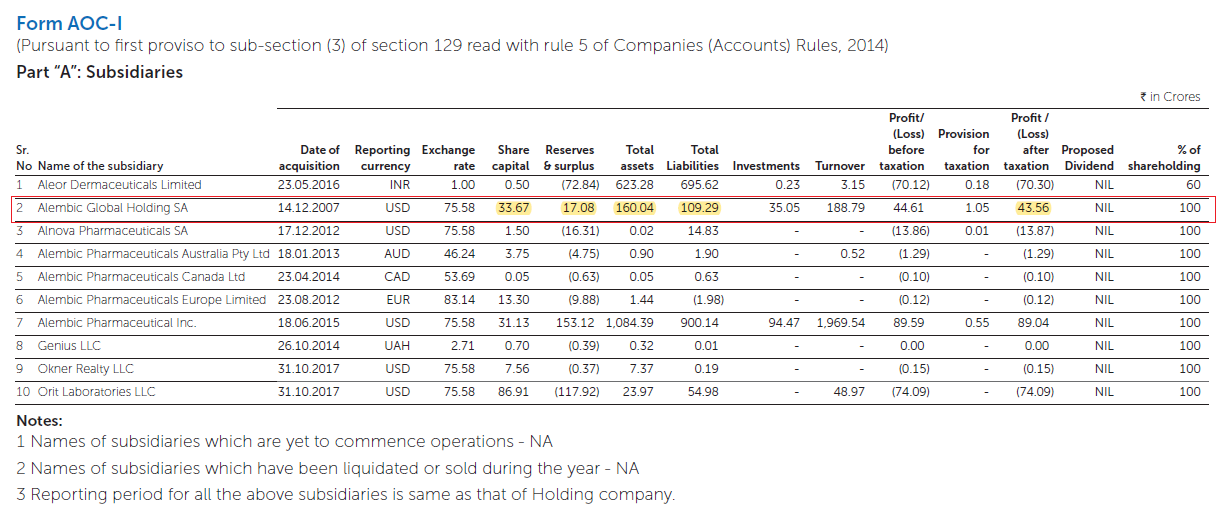

I feel they have possibly taken this GW hit against Alembic Global Holding SA. Below is possibly why I feel so:

Screenshot from FY19AR:

Alembic Global Holding SA had Total assets worth 225cr.

Screenshot from FY20AR:

There is reduction of total assets of about 65.33cr. And if you notice this subsidiary made profit of 43.56cr for FY20. And this was the only subsidiary which had less total assets compared to FY19. Hence, there is a good chance that GW was charged against this subsidiary.

It would had been good if management had provided few lines somewhere in AR explaining this hit in Goodwill.

If this has already been covered in any of the existing con-calls, please let me know. I have not read any transcripts so far. But if it hasn’t been, then I will try to jump on the next earnings con-call and will try to find out the details.

Disc: initiated a starting position in last 30 days

13 Likes

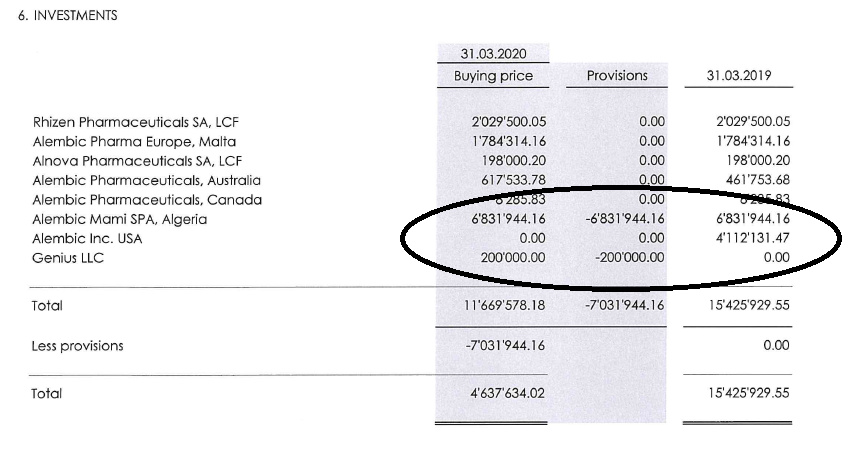

The financials of Alembic Global Holdings SA are available on the website.

They show that the total impairment taken is 6,832,286.50 USD (around Rs.53 crores), of which Alembic Miami Spa Algeria is USD 6,831,944.16 (around Rs.51 crore) and Genius LLC USD 200,000 (Rs.1.5 crore). Thus, the Rs. 43 crore impairment is included in the Rs.53 crore write-off, these two are not independent items.

4 Likes

Thank you for digging further, @Chandragupta!

I ran out of time y’day while going through Alembic’s FY20 AR and didn’t get a chance to look at Alembic Global Holding SA’s financials.

So it looks like investments in Algeria project was through this Swiss subsidiary holding co. This somewhat explains the exceptional loss of Rs. 43.65cr (#1 item per my above post).

But the puzzle of impairment of goodwill of 53.71cr still remains.

1 Like

Alembic Pharmaceuticals receives USFDA Final Approval for Deferasirox

Tablets, 180 mg.

Alembic Pharmaceuticals Limited today announced that the Company has received

final approval from the US Food & Drug Administration (USFDA) for its Abbreviated

New Drug Application (ANDA) Deferasirox Tablets, 180 mg. The approved ANDA is

therapeutically equivalent to the reference listed drug product (RLD), Jadenu

Tablets, 180 mg, of Novartis Pharmaceuticals Corporation (Novartis). Deferasirox

tablets are indicated for treatment of Chronic Iron Overload Due to Blood

Transfusions (Transfusional Iron Overload) and for treatment of Chronic Iron

Overload in Non-Transfusion-Dependent Thalassemia Syndromes. Alembic had

previously received final approval for Deferasirox Tablets, 90 mg and 360 mg and

tentative approval for Deferasirox Tablets, for 180 mg.

Deferasirox Tablets, 180 mg have an estimated market size of US$ 53 million for

twelve months ending March 2020 according to IQVIA.

Alembic now has a total of 122 ANDA approvals (109 final approvals and 13

tentative approvals) from USFDA.

Many companies have this approval - Alem Labs, Cipla, MSN, Sun Pharma, Zydus etc.

4 Likes

Thread on Alembic Pharma

Full report download link:

https://drive.google.com/file/d/1ncI4U7L5jKZVZNUk-ehkMsjKTlvle7kI/view?usp=sharing

2 Likes

Adding my notes and some interpretation and open questions on released

AR

Hand written notes might be difficult to read (some issue with app to do text conversion), finished typing it and hence adding the same in typed text format:

Key notes from Alembic Pharma AR 2020

Key business updates:

- 3 R&D 3 API and 3 formulation facilities

- 3 more facilities to be added

- R&D expense up from 6% to 15% in last 5 years, despite of this EBITDA margin is up from 20% to 26%

- Growth was primarily driven by US markets whereas non-US and domestic market had flat growth

- Appraisal cycle implementation done in April as usual despite of Covid

Business Segment:

International Generic (54% of revenue):

- Scaled up in last 5 years

- 66% ANDA approval rate with 119 approvals and 1/4th of this has come in last financial year

- 69 products launched so far and 33% of these launches came in last financial year. 10 new launches have been done this year so far

- All facilities have regulatory clearance

- In business of oral solids and adding dermatology, oncology and injectables to product pipeline

- Compared to 9 new launches in FY 19, FY 20 saw 22 new launches

Domestic Branded (31% of revenue):

- 185 brands with 1.5% market share in India

- 93% of new launches are in specialty category

- 14% of revenue is exposed to NLEM

- 5500 field executives. Per MR productivity has scope to improve

- 30% market share in Azythromycine in India from covid perspective

API (15% of revenue):

- 109 DMFs files so far

Financial Performance:

- International Generic: 54% of revenue, grew at 39%, US grew at 53% and 43% of overall revenue

- Domestic at 31% of sales and grew at 3%

- Non-US and domestic growth was flat

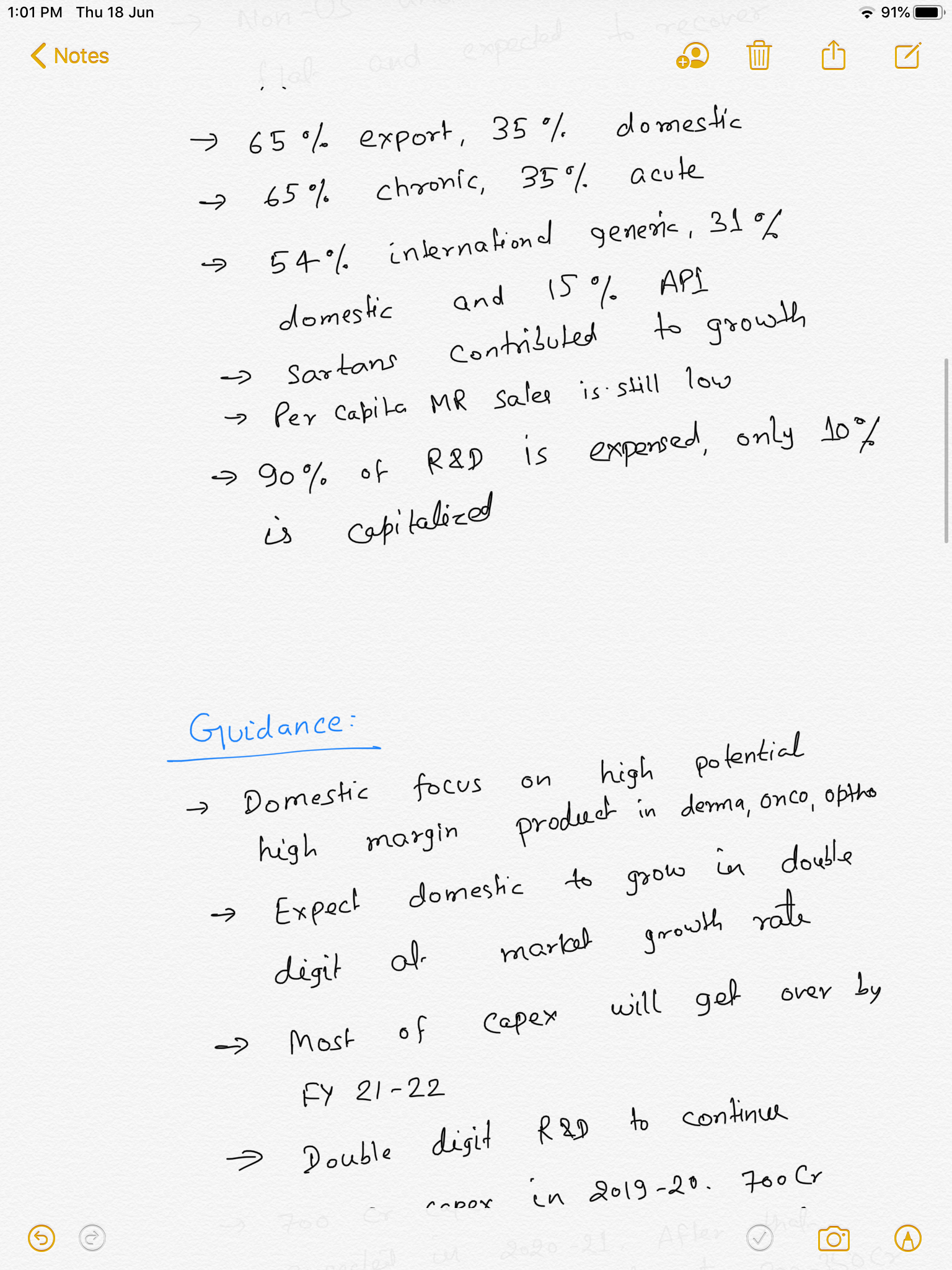

- Export to domestic share is 65:35

- Chronic to acute share is 65:35

- Sartans contributed to growth

- 90% of R&D is expensed and only 10% is capitalized (for last 2 years)

Guidance:

- Domestic focus on high potential high margin product in derma, onco and opthal

- Expect domestic to grow at double digit market growth rates

- Most of capex will get over in FY21-22

- Double digit R&D expense to continue

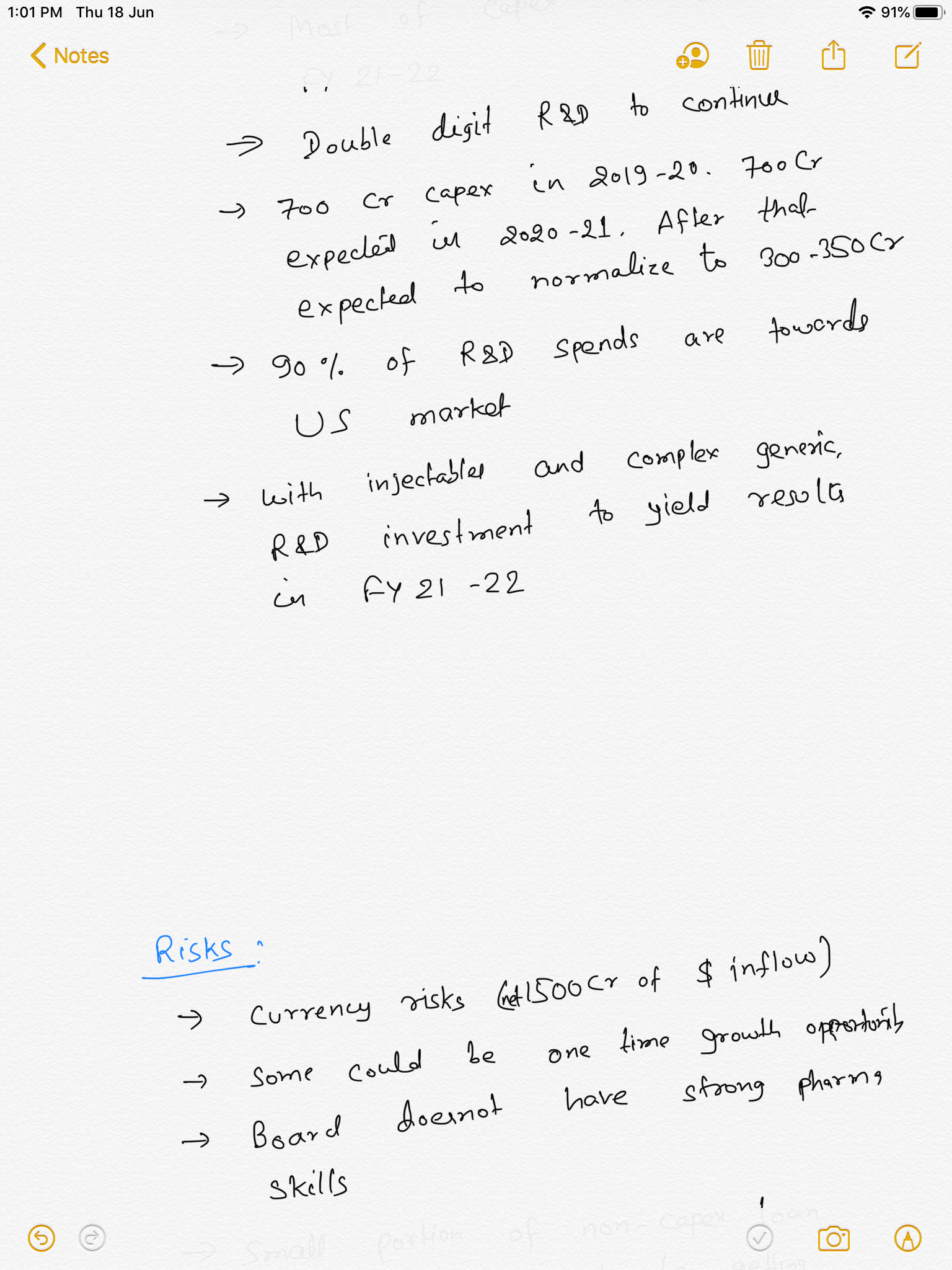

- 700 Crore capex happened in FY 20 and 700 Crore to be done in FY21. After that, it will normalize around 300-350 crore

- 90% OF R&D expense is towards US market

- With injectables and complex generics, expect R&D to yield results in FY21-22

Risks:

- Currency risk (net net 1500 crore of inflows)

- Some growth opportunities like Sartans could be onetime

- Board does not have strong pharma skills

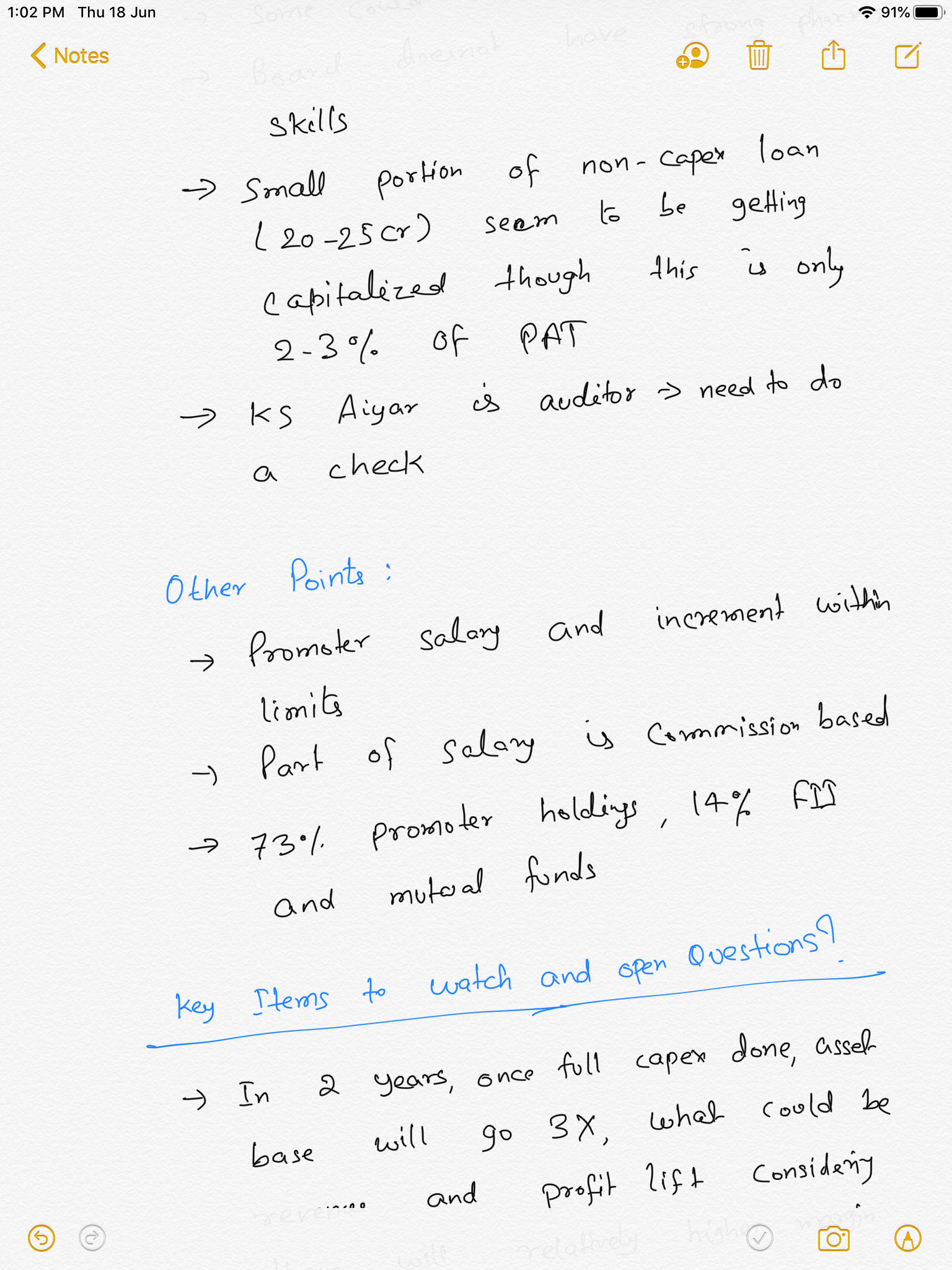

- Small portion of non capex loan seem to be getting capitalized (20-25 cr is rough calculation). However, this amount is very small compared to PAT

- Need to do a check on auditor reputation

Other Points:

- Promoter salary and increment within limits with part of salary in form of commissions

- 73% promoter holding, 14% if FII+ MFs

Key Items to tracks:

Would like to know groups perspective on below questions. Also, in case someone attending call/AGM, would be good to get clarity on some of below questions:

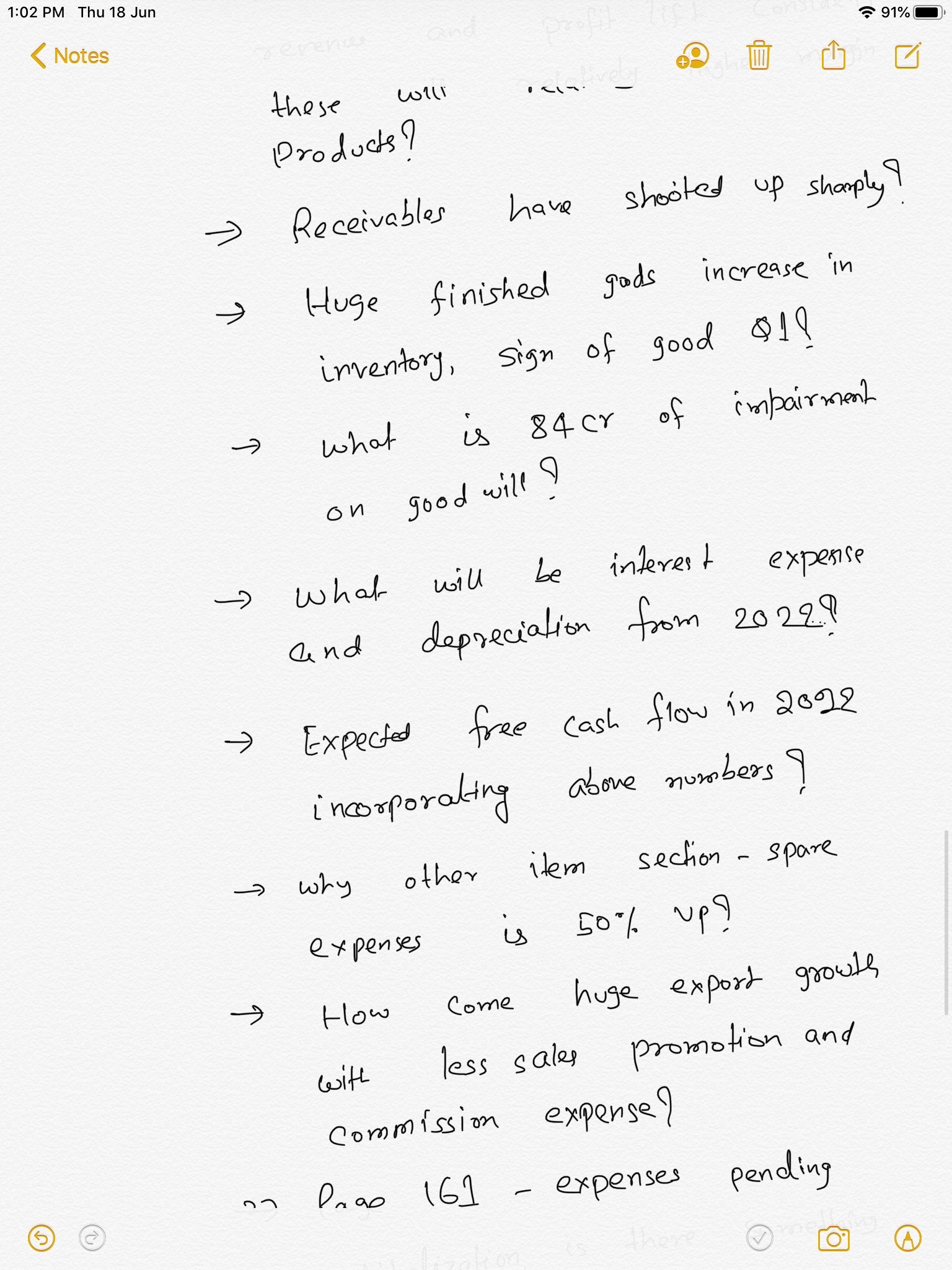

- In 2 years once full capex is realized, asset will be 3X, what could be revenue and profit opportunity out of this assuming regulatory clearance will not be an issue? Also, what expected free cash flow considering capex plan?

- Why receivables are up significantly?

- Major increase in finished goods inventory. Will it lead to good Q1?

- Why is 84 cr of goodwill impairment?

- What will be interest expense and depreciation from 2022 onwards?

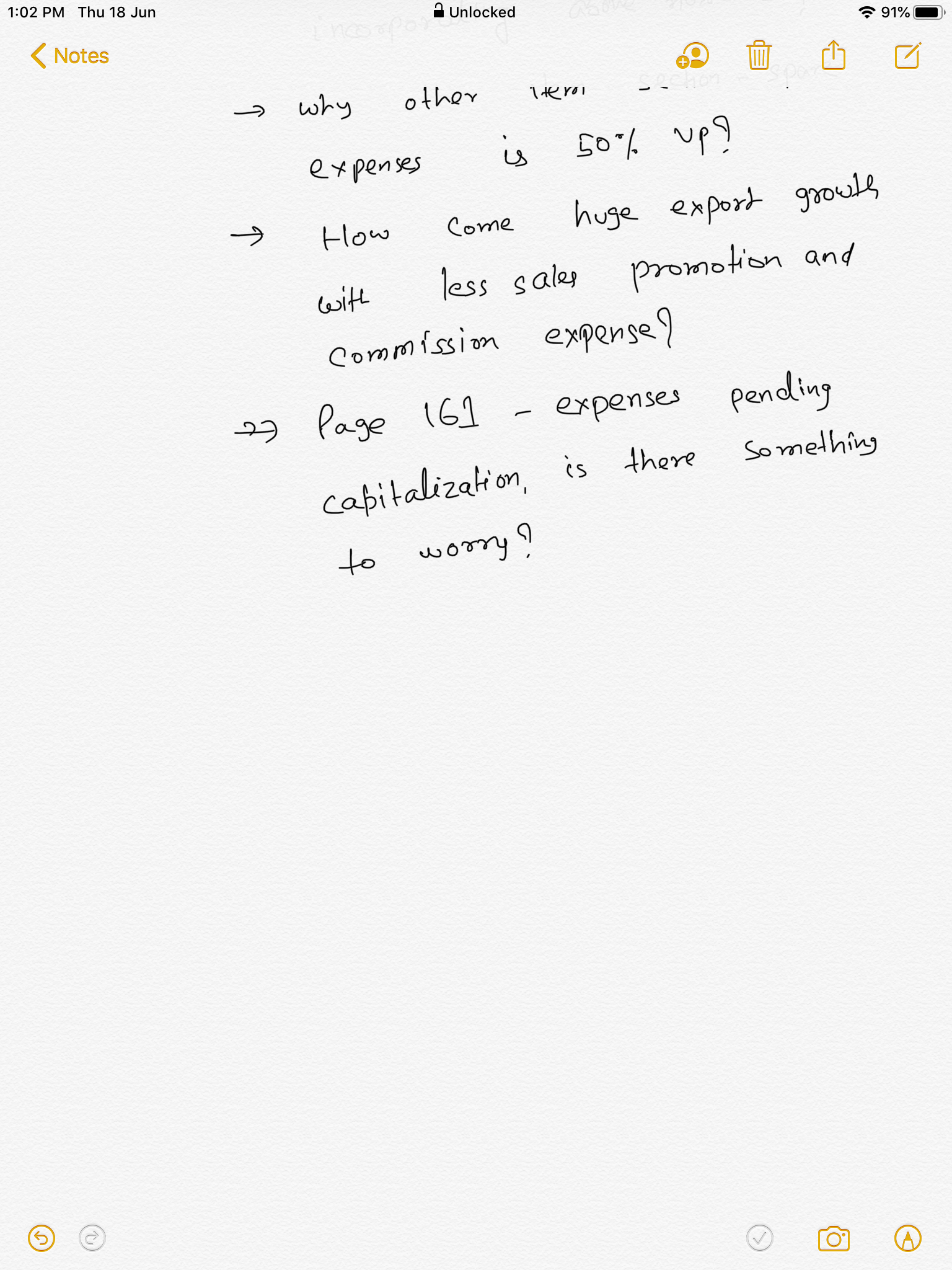

- Why in other expense section, spare expenses are 50% up?

- How come huge export growth was achieved at lesser sales promotion and commission expenses?

- On Page 161, expenses pending for capitalization – what are salary items?

Note: Thanks to @phreakv6 and Ravi Jain for help on some of open item analysis

35 Likes

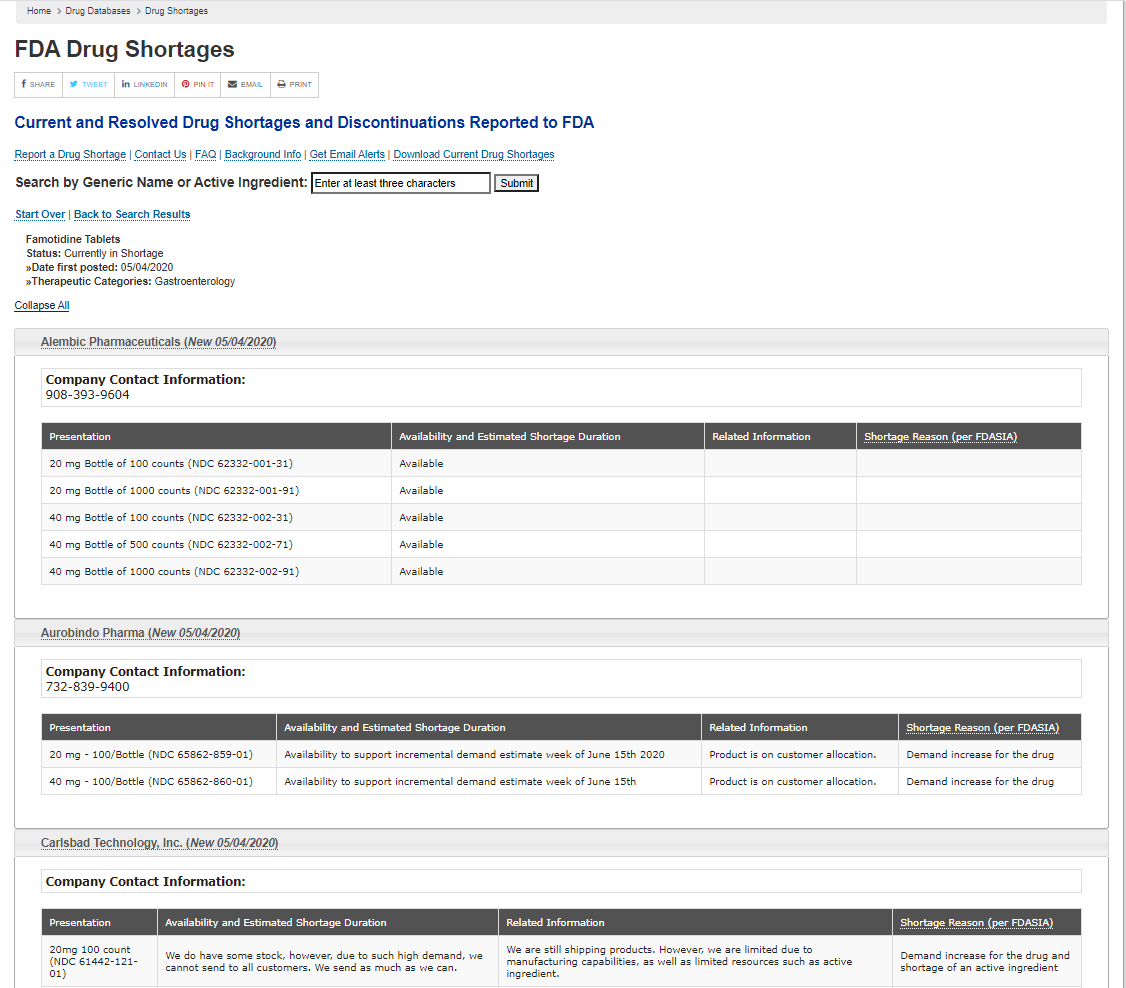

Ongoing shortage for Famotidine tablets and Alembic is the only one with enough supplies

Not sure if data is a bit outdated. Only, Teva Pharmaceuticals’ shortage data had been updated yesterday and for other 3 co. in May.

What I couldn’t figure out was whether the API for Famotidine is also made by Alembic.

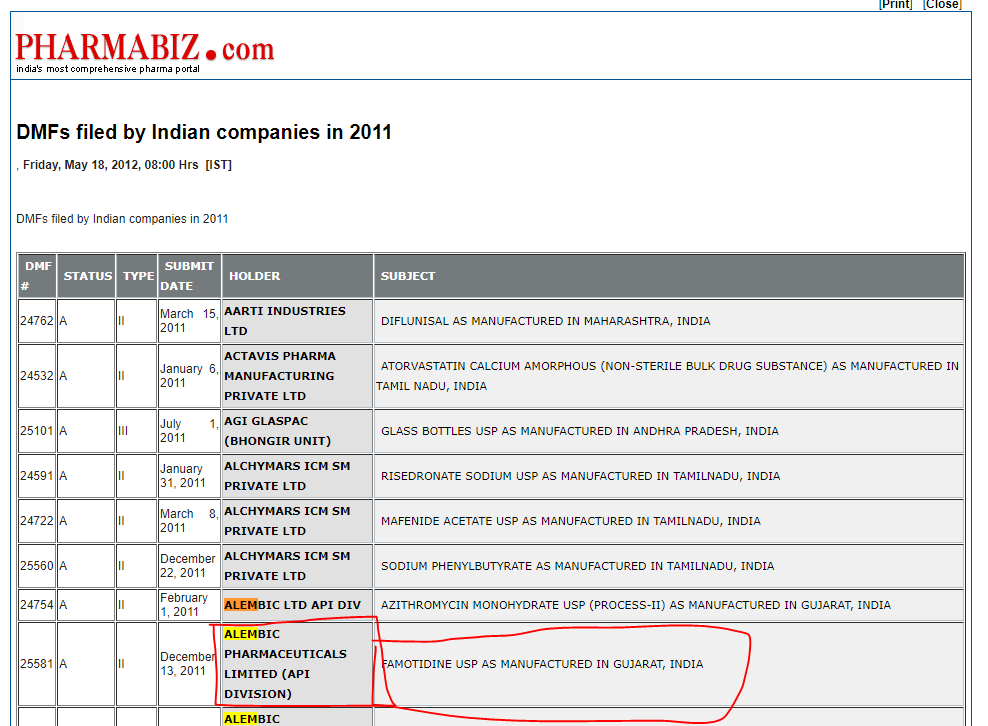

This website does show Famotidine API is made by the co. though

7 Likes

Another ANDA Approved by USFDA. Not sure which other companies hold this approval.

4 Likes

Certainly the impairments & write-offs have not been very clearly explained. Total impairments and write-offs taken during the year are as follows:

| Particulars | Rs. (crores) |

|---|---|

| Impairment in JV in Algeria | 33.65 |

| Goodwill | 4.69 |

| Other intangible assets | 49.02 |

| Total | 87.36 |

My previous post stated that of the Rs.53 crores (Goodwill & Intangible Assets), Rs.51 crores pertain to Algeria JV, which adds up to Rs.84 crore for the Algeria JV. On the other hand, Note 20 mentions Rs.69 crore pertained to Algeria JV. Somehow the numbers don’t tally, though it is clear the major chunk of write-off pertains to Algeria JV.

The Algeria JV was entered into in FY14-15. It commenced operation in Q1 of FY17-18. Immediately in Q2 of the same year, it reported a fire which destroyed the entire facility. Since then, the plant has been reportedly shut and now the company has written off the entire investment. It is not clear if any insurance claim was filed and anything received.

I think these kind of risks are something Alembic investors need to be cognizant of. Returns from investments made in subsidiaries, associates and JVs get less closely monitored, with analysts having a tendency to treat such losses as “one-offs”.

So far Alembic has had a clean record on this count. But in recent years, company has expanded its Balance Sheet aggressively (that too, funded by debt). And a lot of this money has gone into group companies (mainly Aleor, but some in others also). This was not the case in the past.

| Rs. Crores | Debt raised | Investments in Group Cos |

|---|---|---|

| FY17-18 | 619.05 | 200.00 |

| FY18-19 | 220.66 | 207.50 |

| FY19-20 | 609.39 | 326.86 |

| Total | 1,449.10 | 734.36 |

So going ahead, this point will have to be closely watched. It will be great if you ask the management in more detail about the Algeria JV in next concall.

(Disc.: Have a tracking position)

19 Likes

Alembic Pharmaceuticals receives USFDA Tentative Approval for Rivaroxaban

Tablets, 10 mg, 15 mg, and 20 mg.

Alembic Pharmaceuticals Limited today announced that the Company has received

tentative approval from the US Food & Drug Administration (USFDA) for its

Abbreviated New Drug Application (ANDA) Rivaroxaban Tablets, 10 mg, 15 mg, and

20 mg. The approved ANDA is therapeutically equivalent to the reference listed drug

product (RLD), Xarelto Tablets, 10 mg, 15 mg, and 20 mg, of Janssen

Pharmaceuticals, Inc. (Janssen). Rivaroxaban Tablets are indicated for i) the

reduction of the risk of stroke and systemic embolism in patients with nonvalvular

atrial fibrillation. ii) the treatment of deep vein thrombosis (DVT). iii) the treatment of

pulmonary embolism (PE). iv) the reduction in the risk of recurrence of deep vein

thrombosis and of pulmonary embolism following initial 6 months treatment for DVT

and/or PE. and v) the prophylaxis of DVT, which may lead to PE in patients

undergoing knee or hip replacement surgery.

Rivaroxaban Tablets, 1 O mg, 15 mg, and 20 mg have an estimated market size of

US$ 6.1 billion for twelve months ending March 2020 according to IQVIA.

Alembic now has a total of 124 ANDA approvals (110 final approvals and 14

tentative approvals) from USFDA.

As of now looks like two other cos have the tentative approval - Aurobindo Pharma and Prinston Inc.

5 Likes

As per their 2019 AR, Chronic contributes to 68% of their overall revenues.

Does anybody know the break up of Chronic vs Acute segments, as of March 2020?

Asking this because this could be a potential key factor in determining whether or not the company does well over the next few years,

A good article on drugs shortage including Sartans in Germany

1 Like