My logic behind investing in Alembic

Assuming, demand for Azithral continues for at least a year, retail sales in India could potentially be 2784 Crs (10 Cr tablets * INR 23 per tablet * 12 months). Out of this 2784 Crs of sales we need to deduct distributor & retailer margins, etc. One can compare this to compare this Alembic’s TTM sales of 4326 Crs (Although not strictly comparable, it does provide some insight anyway).

And this is just domestic sales. International sales could be higher or could be significant.

What are the things that could go wrong?

Alembic might as well turn out to be an undertaker in a plague, in which case, the upside could be significant.

Valuation - Before the markets started tanking, the market was pricing each share at INR 674. The price at the current time is 631, which is slightly below the “pre-crash” price. I believe the market may not be factoring the potential upside from Azithral sales this year. In effect, there is a significant option value embedded in the stock’s current valutaion.

Request other valuepickr members to point out anything else that I might have overlooked or might not have given enough weight to.

4 Likes

Audited financials firstly are released much later, possibly July after 1st qtr results of following year

Audited financials are for main purposes a stamp of auditors that internal financials are accurate and systems are followed even then lot of audited financials miss system weaknesses

Data is available now that probably is 90-95pc accurate, why would you not discuss it now ?

Alembic, which also claims to be the largest player in selling active pharmaceutical ingredients (APIs) of azithromycin to the world, holds 30 per cent market share in selling the finished tablets of the antibiotic in India.

3 Likes

Result is good

but dependency of raw material on china could affect the company result in near future??

Excellent results

| Rs crs |

Q4 FY 20 |

Q3 FY 20 |

Q2 FY 20 |

Q1 FY 20 |

FY 19 |

FY 18 |

FY 17 |

FY 16 |

| Topline |

1,208 |

1,209 |

1,246 |

949 |

3,935 |

3,131 |

3,134 |

3,162 |

| EBITDA |

329 |

332 |

342 |

233 |

875 |

642 |

615 |

1007 |

| EBITDA Margin |

27% |

27% |

27% |

25% |

22% |

21% |

20% |

32% |

| Net Profits |

225 |

234 |

246 |

124 |

584 |

413 |

403 |

720 |

| Net profit margin |

19% |

19% |

20% |

13% |

15% |

13% |

13% |

23% |

| R&D spends |

185 |

146 |

174 |

140 |

500 |

410 |

430 |

320 |

| As % of sales |

15.3% |

12.1% |

14.0% |

14.8% |

12.7% |

13.1% |

13.7% |

10.1% |

Q4 FY 20 numbers include a net exceptional item of c. -Rs 10 crs

Growth was led by US generics growing 84% YoY. India formulation grew 13% YoY and RoW grew 63% YoY. APIs degrew -33% YoY.

10 ANDA filings for the quarter and 25 ANDA filings for FY 20

There is a investor call at 4 pm today.

9 Likes

Q4 Alembic Concall Notes

Didn’t connect for first few mins might have missed a few points, others please add.

US Business:

- Base US Business - 70 Mn $ per Quarter since the last 3 quarters. Expects it to continue for the next 3-4 years

- Bulk of the competition is among the Indian companies in the US Market

- 15 ANDAs in the US. Don’t foresee any demand changes for next 3-6 Months

- Price erosion in the US Market is in lower single digits

- Significant gross margins improvements – Product Mix, Deprecation of Rupee

- 60% (air) shipping ratio maintained. Will add a bit to the cost

Domestic Market:

- Business Turnaround is sustainable in the domestic market for the next 3-4 Quarters

- Product Launches in FY 20 – Haven’t been any large launches in domestic business

- No price increase is expected of Azithromycin with govt capping

- 60% (air) shipping ratio maintained. Will add a bit to the cost

Lockdown:

- No impact from the Lockdown foreseen as of now – Marketwise no changes

- Women’s Healthcare, Orthopedic might see lower demand but it is expected to recover after the lockdown

- 70-80% capacity utilization currently

Market Share:

- No loss of market share in Focused Brands in the last 4 years

- Generic Portfolio we are defocusing hence lost Market share

- De-growth on API business – API contract with 1 particular MNC has become Zero

China:

- 15% overall raw material dependency from China

- 70% normalcy of supply chain from China since March

- Raw materials level should be ideally of 3 months, but that’s never the case

Others

- Debtor Days – 68 Inventory Days – 93 vs 88 YoY

- Capex 700 Crs for next year with an increase of Debt not more than 200 Crs

- Guidance of R&D – 700 Crs vs 650 Crs (PY)

18 Likes

ALEMBIC

ANTIQUE

Upgrade to BUY from HOLD

Revised TP of Rs 830 vs 640

Top Notch US performance

Recovery in domestic biz

AXIS CAP

Upgrade to BUY from ADD

Revised TP of Rs 840 vs 585 earlier

Raise FY21E EPS by 39% and FY22E EPS by 29%

Well positioned to generate Free Cash Flow

1 Like

IIFL on Alembic Pharma

We increased our US sales estimate for FY21 by 24% that, along with higher margin assumptions of 100-150pa and INR/USD rate of 76 (vs. 71 earlier), leads to an EPS upgrade of 23/10% for FY21/22ii

Maintain BUY, TP Rs 800

@CNBCTV18News @ekta_batra

Alembic Pharma Monthly, Weekly & Daily Chart. [PriceAction] BULLISH on all time frame. [EMA] ADX_DMI also confirmed last week BREAKOUT. Looking good for long term investment after price cool down a little bit.

Note: View is biased as already invested.

1 Like

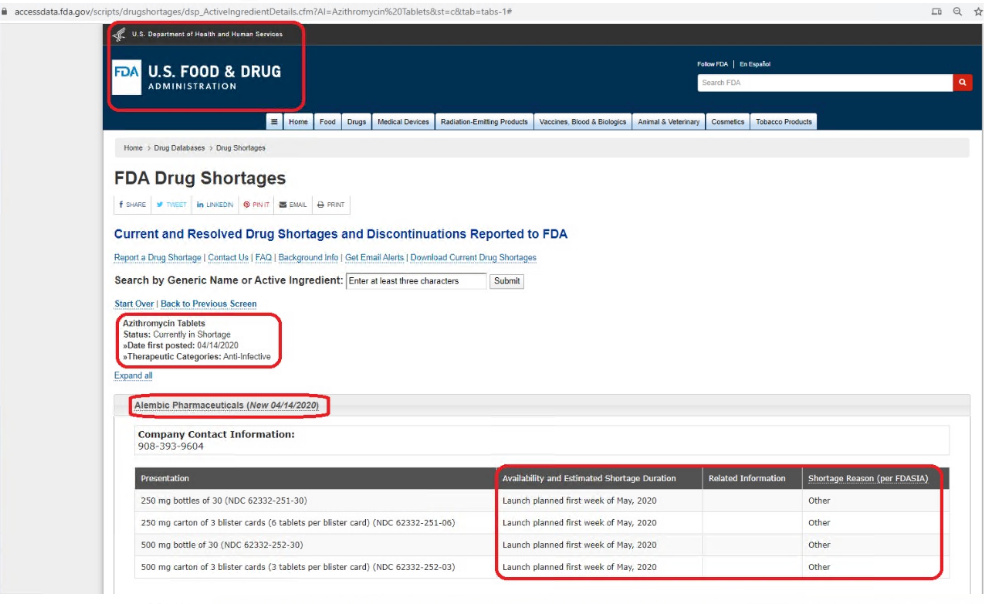

Have been researching this co. over the last few days and found something interesting.

Shortage for Azithromycin continues, as per the US Food and Drug Administration site. The site also states - launch (I am guessing in the US) of is planned for the first week of May.

As per management, this is a big opportunity for the company.

Disclosure: Invested

8 Likes

I have updated my thesis based on various news reports

Sales estimates for Azithromycin for FY21

Alembic can manufacture 10 Crore tablets a month / 120 Cr tablets a year

Retail price in America ranges between INR 120 & 174 per tablet

At INR 120, retail sales for Azithromycin could reach 14400 Crs / $2 Billion, in the US alone.(10 Cr tabs * 12 months * INR 120 per tab) (This is assuming that this situation lasts, at least a year)

Alembic’s FY20 sales - 4600 Crs

How much of a market share, Alembic can manage to capture remains to be seen

What can go wrong / right

FDA site mentions Hydroxychloroquine has not been shown to be safe and effective for treating or preventing COVID-19.

However, there are some reports that Hydroxychloroquine, which is used in combination with Azithromycin, is showing some positive results.

API Business

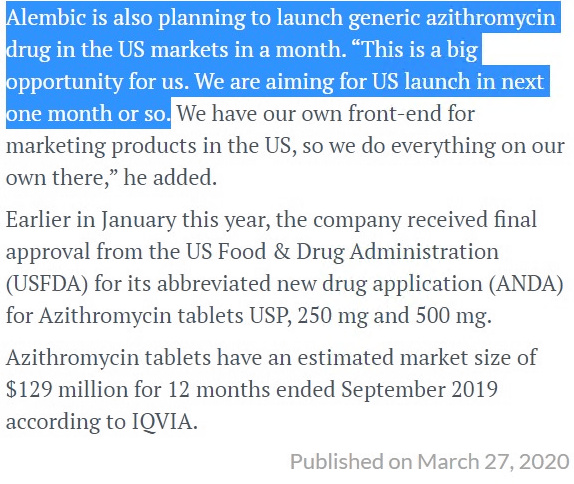

Alembic is also the largest player in selling active pharmaceutical ingredients (APIs) of azithromycin to the world

The company has been supplying azithromycin active pharmaceutical ingredients to patent provider Pfizer for over 10 years.

API prices prices have doubled to 16,000 a kg

The cost of azithromycin, an antibiotic used for treating a variety of bacterial infections, has risen 70 per cent.

15 Likes

Good stuff! Going into FY21,one big headwind for APL was the end of the Sartan opportunity but it seems Azithromycin shortage will more than make-up for it. APL had mentioned in the Q4 call that they are in the process of launching.I am guessing Azithromycin sales would’ve started already. Thus,assuming that Sartans run out of steam in H2,the tailwind from Azithromycin should help a lot. H1 should be strong with both Sartans & Azithromycin leading the charge and the base business chugging along at decent rates. For me,the domestic business also offers very good opportunity for APL. The management mentioned that their work-force is only at 70% of their competitors. Thus,on ramp up of this factor alone APL can pull up their sales quiet a lot(should occur over next 3-4-5 years)

Given the overall economic conditions,most companies across industries will find it tough to report a positive rate of growth in FY21. This situation makes companies like Alembic an island of sorts. If they can continue to control the instances of Covid at their facilities,APL should do very well.

Disc.: Invested. Views are biased.

7 Likes

I was trying to understand what caused the Sartan shortage and the reason why it has lasted this long. The problem first surfaced back in 2018 and its now 5-6 quarters old and the company has guided for Sartans “one-off” lasting another 6 months at least.

It looks like unlike the usual causes of shortage like plant closures of a large player or impurities in certain batches of products, in this case, the “impurity” NDMA/NDEA (carcinogenic equivalent of 20 cigs in a day, apparently) in losartan, irbesartan and valsartan is more structural in nature, as it is due to the process used for manufacture itself. This article too explains this simply.

So this has affected not just one batch, label, re-packager, distributor, API manufacturer or company but a messy combination of all, leading to severe recalls and consequently, the shortages. What’s interesting too is that this process has been around since about 2013 but the issue surfaced only in 2018, so stopping something that has worked for so long suddenly is probably not easy. This is the reason why supply hasn’t come back soon as this means changing the process used in the manufacture, and that also means lower yield and a less competitive end-product in terms of margins, not to mention fresh approvals for the new API/process and the fact that some of these players have been placed on import alert.

To give you an idea of how much of supply is probably affected - Here is a list of all Sartan supply that has nitrosamine impurities and this is the list of approved Sartans that don’t have nitrosamine impurities. (Alembic features with 28 Sartans in the second list)

Azithromycin definitely is a fantastic opportunity, and the ability to sell to US at a time of shortages, means that it could play out the way Sartans have played out, perhaps in an even larger scale if HCQ + AZM is proven beyond doubt in clinical studies to be effective. Selling it through the capable US front-end of Alembic could result in higher margins (80-90%) as well if it happens. We should know in a couple of weeks how it plays out.

32 Likes

During my last meeting with Alembic guys I had asked a question related to competitive strength in Sartans. I asked if a previously affected company somehow resolves its problem of manufacturing sartans and manages to get a proper source and finally manages to manufacture NDMA free sartan, how much time would be needed for it to re launch these sartans in the US markets. The answer was anywhere between 8-18 months.

So in effect a company has to first figure out a way to establish a supply chain that ensures NDMA free manufacturing of sartans and then re apply to USFDA for approval and then if all goes well it could take 8-18 months for it to start delivering to the US markets. As of now there are only a few (4-5) players who address the sartans market and Alembic is present with all possible combinations and all possible strengths. It has close to 15-17 products in the sartans basket and shortages keep cropping up in one or the other molecule/combination and hence Alembic seems to be sitting well as of now.

Azithromycin is a product wherein Alembic is vertically integrated. Even API prices of Azithromycin have gone up a lot recently. This can be of benefit to Alembic.

I came to know that Venlafaxine (psychiatry drug) group sales in Europe has been very strong and consistent for Alembic.

Domestic sales for Alembic and most pharma players will in all probability remain weak for most pharma players atleast in q1 fy 21 barring only those who have established brands in the chronic portfolio.

40 Likes

Had read this old article earlier, however even today its a good read to get some good insights on what helped transforming Alembic Pharma from a mere API-driven business to one of the fastest growing generic drug maker with young generations of Amin family at the helm.

6 Likes

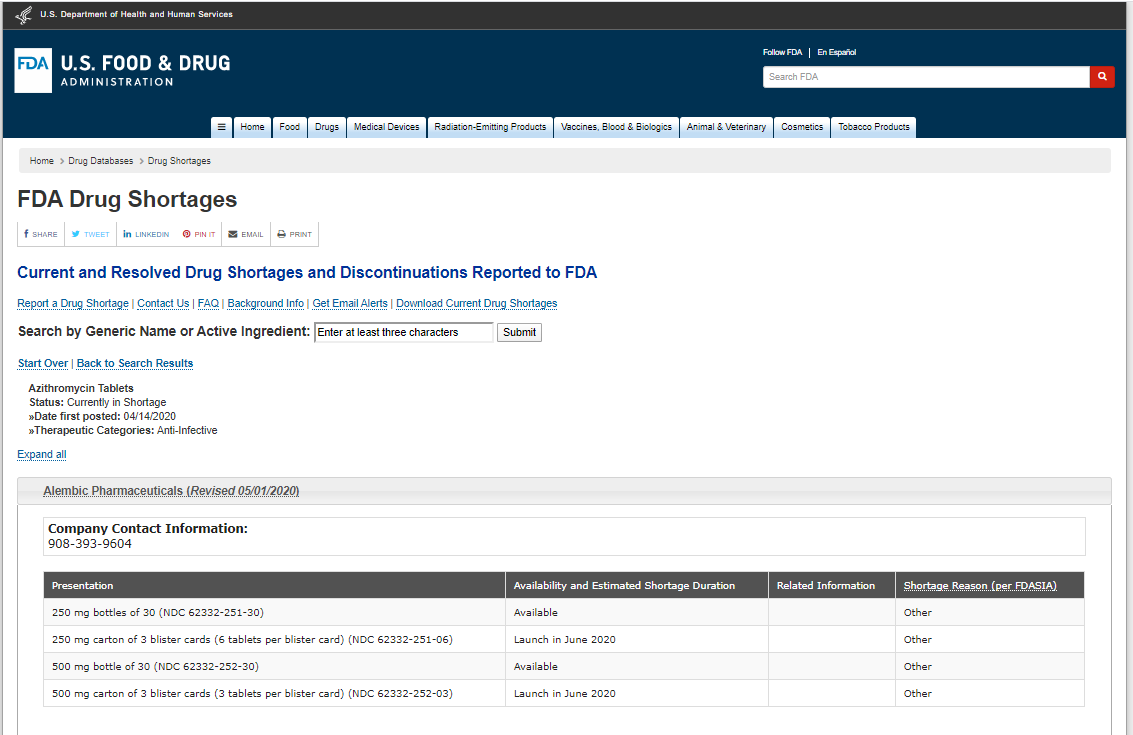

US FDA website updated on 1st May - FDA Drug Shortages

Shows 250 mg & 500 mg bottles of 30 now available in the USA, while shortage for Azithromycin Tablets, continues.

2 Likes

USFDA accepted the Company’s response to its observations with regard to General Oral Solid Formulation Facility located at Panelav .

Inspection at the said Facility was conducted by

USFDA from 9th March, 2020 to 13th March, 2020.