No Sir,

International Sugar did bid.

They quoted lesser price then AGI. (AGI was 2100 cr while madhvani (international sugar) was 1850 cr)

AGI bid was higher and recovery to banks was better and hence COC selected AGI.

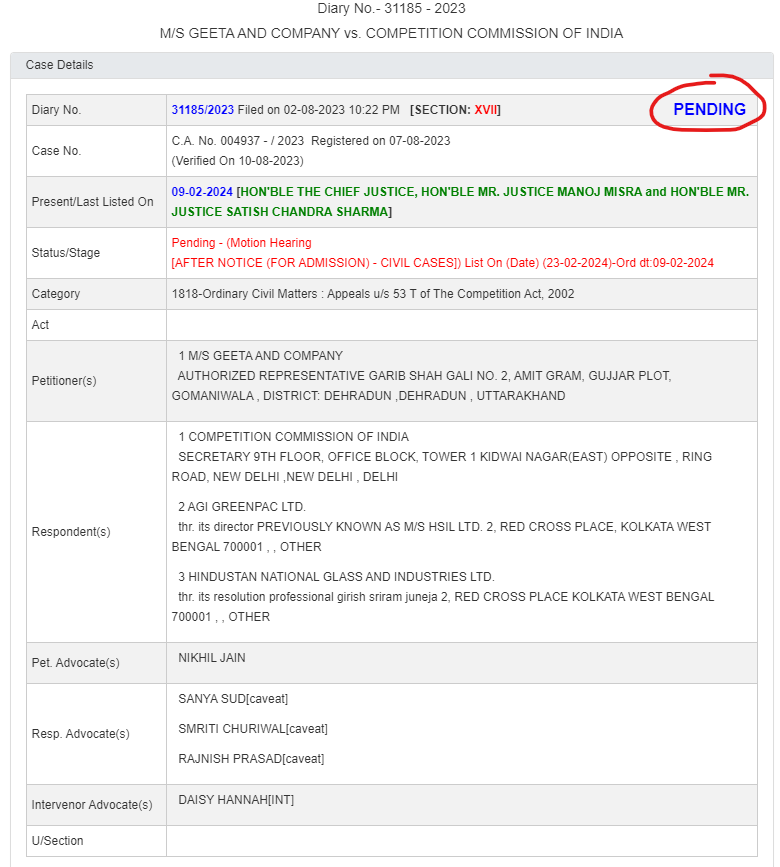

International sugar (despite being loser) are now fighting on thin technical grounds that AGI did not had CCI approval before getting selected by COC. Their appeal was dismissed in NCLT and subsequently in NCLAT and both approved AGI as successful bidder for HNG.

As of now, both AGI and International sugar have CCI approval and AGI is offering much more then international sugar.

Well in that case you are late. SC heard the case for the first and the only time around 16 oct (don’t remember the exact date) and admitted it for further hearings…

Stock corrected from around 1000 Rs.

Two quarterly results are declared after that.

I believe that Even without HNG the stock has still to realise it’s true potential…(individual call)

We need to see in broader perspective, AGI is expanding capacity by 120 ton which is close to 13%. Delay in HNG or even scrapping of HNG will increase prices and margins will rise further. I still believe paying 2200 cr for defunct furnaces is not a good option, delay in HNG aquisition and HNG dying its own death is only beneficial to AGI. No merit in aquisition at this price now. Any decision will trigger stock upside. In case AGI further bids agressive and raise bid price than that is a clear trigger for an exit.

Piramal glass again on the block. Blackstone wants $1.8B to 2B. Company doing 1162 EBITDA.

AGI green does 400 and if it gets HNG, it will be close to pirmala EBITDA. Going by the valuation which Piramal is commanding, we can see a 2x-3x outcome here.

Piramal has historically had better margins and has a specialty business that is more prominent than AGI. Hence, I would assume that there will be some sort of discount. However, your point on valuation catch-up could be valid to some extent.

News article published on 20th March. Market was already down. 21st March AGI share was 1.1% up when the rest of the market was mostly all guns blazing.

Is this the end of the AGI + HNG saga and will AGI have to go it all alone with a question mark on corporate governance?

Sir, These are usually planted articles. Under IBC there is no restriction on Member of COC to fund bidders. At the end of the day there are handful of scheduled banks and large NBFCs in India. Banks/large NBFCs are in coc in most cases in IBC and corporate bidders have running credit lines from them.

Issue here is simple.

HNG is bankrupt.

Open bids were invited.

One who quoted maximum should win the deal.

Maximising lenders returns and minimising their haircut is fundamental bedrock of IBC.

No one stopped the Kenyan chap from quoting higher…now he is sulking.

I agree with you for the most part. In all fairness, even after discounting an investor bias, it seems quite straightforward. But the real world is much more murkier.

The core point of worry is that the delay may result in deterioration of the HNG assets and workforce that are non operational and that’s what seems to be the core motive now of the losing bidder.

Another thought is that at current valuations, does AGI seem a worthy investment even without HNG given that their growth will be stemmed unless the acquisition is completed soon or they plan greenfield capex? This is a thought for a two year horizon.