Tentatively case may be listed on (likely to be listed on) 03-05-2024 (Computer Generated)

Tarik pe tarik ![]()

![]()

Tentatively case may be listed on (likely to be listed on) 03-05-2024 (Computer Generated)

Tarik pe tarik ![]()

![]()

Just sent a mail to investor relations seeking the reason behind multiple postponements, will update the group once I get a reply.

So from the con-call it appears that Management doesn’t anticipate a scenario where the ruling is not in their favor (as in there doesn’t seem to be a plan B with regard to future growth). So let’s hope their confidence holds good. One point that I couldn’t quite grasp was the condition subsequent to acquisition of HNG to sell their Rishikesh unit (400 TPD capacity) which is a voluntary modification action from AGI. Anyone can shed more light on this?

“AGI’s resolution plan got “conditional” approval from the CCI in March 2023. There were complaints that AGI’s acquisition of HNG would create a monopoly in the segment it operates yet the CCI gave its go-ahead on the “condition” that AGI had agreed to divest HNG’s Rishikesh plant”

So looks like it was voluntary in order to ensure CCI doesn’t raise concerns on monopoly.

Best case assuming positive SC verdict it will take 6 - 9 months before AGI would get hand on HNG assets. This is turning out to be long drawn battle.

SEBI fined AGI for failure to disclose to shareholders key details of the modifications to the HNG deal required by CCI. The order is discussed in detail in this article -

https://businessworld.in/article/sebi-fines-agi-greenpac-for-inadequate-disclosures-to-shareholders-519391

A week back, following the SEBI imposed penalty, AGI has made a voluntary disclosure of all litigations pending with Supreme Court and NCLT regarding the HNG deal. Total 12 challenges, 7 with Supreme Court and 5 with NCLT. Of these 4 have been filed by Independent Sugar, 2 by UP Glass Manufacturers’ Syndicate and the rest by various labour Unions of HNG.

UP Glass Manufacturers’ Syndicate has 4 Directors, all of whom own glass making companies. One of the directors is Mr. Sanjay Agarwal of Kwality Glass Works. There is a Sanjay Agarwal who is the sitting President of the All India Glass Manufacturers’ Association - The All India Glass Manufacturers' Federation. Not sure if its the same person. The Sr. Vice President of AIGMA belongs to AGI Glasspac.

Disc: Not invested. Tracking the HNG acquisition.

Arihant Capital analysis of the HNG acquisition and buy recommendation issued.

thx Sid_Mathew for the update That is why the stock is up around 8% today i think by the end of August the court decision will come in favor of AGI

@Sid_Mathew The link doesn’t open.

I just checked. Seems to be working fine.

Yes working now. Had been trying since last 2 days. Opened only now. Thanks.

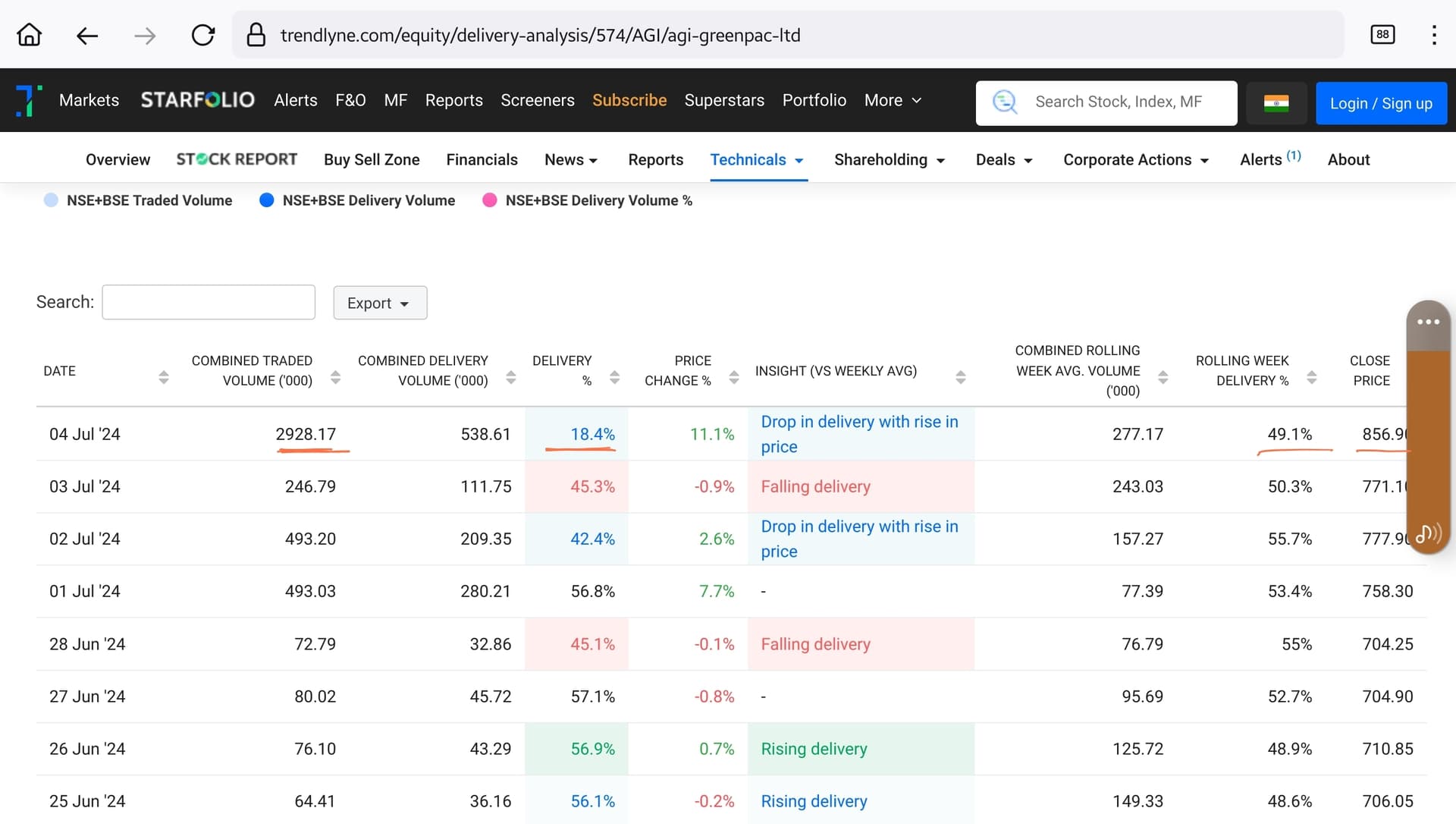

Caution for retail investors - Huge volumes yesterday but comparatively low delivery percentage.

Looks good in absolute numbers but this jump may still be speculative based on the Arihant Capital analysis report. Company will definitely do good in the mid to long term but the immediate huge jump is something to be cautious about.

Disc: Invested.

Dont find any issue here as 230 cr capex to further optimize capacity and its trading cheap

AGI (established in 1960) is engaged in manufacturing and distribution of packing products comprising three diverse segment namely glass containers, PET bottles and security caps and closure. Co has 20% market share in organised glass packing industry. The co is projected to give returns of 12% next year

| Date of report: | 11-08-2024 | Industry PE | 29.91 | Sector | Packing Industry |

|---|---|---|---|---|---|

| CMP: | 760 | Current PE | 19.58 | No of Years | 44 |

| Market Cap: | 4916Cr | Highest PE | 28 (2023) | Key Products | Glass Packing |

| ROCE / ROE | 18% / 15% | Lowest PE | 2.5 (2011) | Key Competitor | Haldyn Glass |

Business Model and Industry Analysis

Overview:

The company is in packing industry where majority of revenue comes from glass container. The company has grown itself by debottlenecking and relining of existing furnace to increase the capacity utilisation. Further it has also filed for acquisition of HNG a bankrupt co which is pending since long. Below in its three business segments-

Industry Growth:

The glass packing industry is expected to grow at 7% CAGR. Alco bev industry being co’s major customer is experiencing rapid growth. Further the glass packing gives aesthetic appeal to its consumers and is also a way now to provide a distinguish and captivating glass packing to create a brand image. It also facilitates to enhance shelf appeal of customers

Capacity Utilisation:

The company has 7 plants with glass packing factories (3) in Hyderabad and others in Uttarakhand and Karnataka. Co operates at 90% capacity utilisation and keeps on increasing its furnace capacity continuously by relining and debottlenecking. The company’s capacity stands at 1,754 TPD (tonnes per day) for its glass packaging division (including specialty glass capacity of 154 TPD), 11,892 TPA for its plastic packaging division, 780 million of small cap pieces and 132 million of large cap pieces

Opportunities:

Risk:

Future Expansion:

The co has planned capex of Rs 250 cr which will be funded by internal accruals. This funds will be utilised for relining of furnace and to expand capacity to meet increasing demand

Management:

Management is very money wise as it prefers to debottle than to setup a plant. Further they are strategic by foraying in cap closure segments as well as speciality glass segment. They have maintained their profit margins by switching to alternate fuels during rising fuel prices. Management draws around 7% on net profit as salary. Promoters has 60% unpledged shareholding

Institutional Investor:

FII and DII continue to hold around 9% in the company

Historical Data and Financials

Profit N Loss Account:

* Sales have grown at CAGR of 24% for last 3 years

* Margins have continuously improved and stands at around **10%** currently

Balance Sheet:

* Interest coverage ratio is **6 times**

* Co is continuously reducing its borrowings every year

* Debtor days and Inventory days have improved

* Working Cycle and Cash conversion cycle have improved YoY

* Current ratio stands at 2 times.

Cash Flow:

* Co has a very healthy CFO/PAT of 1.83 times

* Co is generating enough accruals from operations to fund its capacity expansion and reduce debt

Valuation and future potential:

| Particular | Current | 52W High | 52W Low | Historical High | Historical Low | Industry Median |

|---|---|---|---|---|---|---|

| Price | 760 | 1067 | 643 | 1067 | 8 | - |

| PE Ratio | 19.58 | 28 | 16.2 | 28 | 2.5 | 29.91 |

| EPS | 38.81 | 43.68 | 38.1 | 43.68 | 5.28 | - |

| Price/Book | 2.7 | 4.1 | 2.3 | 4.1 | 0.2 | 2.23 |

| EV/EBITDA | 8.7 | 13.9 | 7.5 | 13.9 | 2.4 | 13.06 |

Valuation:

| Particular | 23/24 | 24/25 | Comments |

|---|---|---|---|

| Sales | 2421 | 2663 | Management Conservative guidance |

| Profit | 251 | 276 | Management Conservative guidance |

| No of Share | 6.46 | 6.46 | - |

| EPS | 38.85 | 42.72 | - |

| PE Ratio | 19.58 | 20 | Average PE traded in past year |

| Share price | 760 | 854 | |

| Return | 12% |

Should wait for price to come at 660 (38.81*17)

Disclaimer: This is a study report, not for any decision making or investment advisory.

Made by: Nidhi Devidan

Date:11th August 2024

Hi!

Anyone who may have attended the AGM today, could you please provide any important insights from the QA session?

Any update on the legal front also?

Thanks.

Nothing worth of significance. Two speakers usual “thankyou sir” types…

I think, Once this HNG overhang is cleared, either way, company will embark on capex plan organically or via HNG depending on the outcome of the case…

It’s been over a year that case is lying in SC and over three years since the company won the bid in cirp process… capacities have almost exhausted…

Btw: it’s one of the most efficient glass company globally…

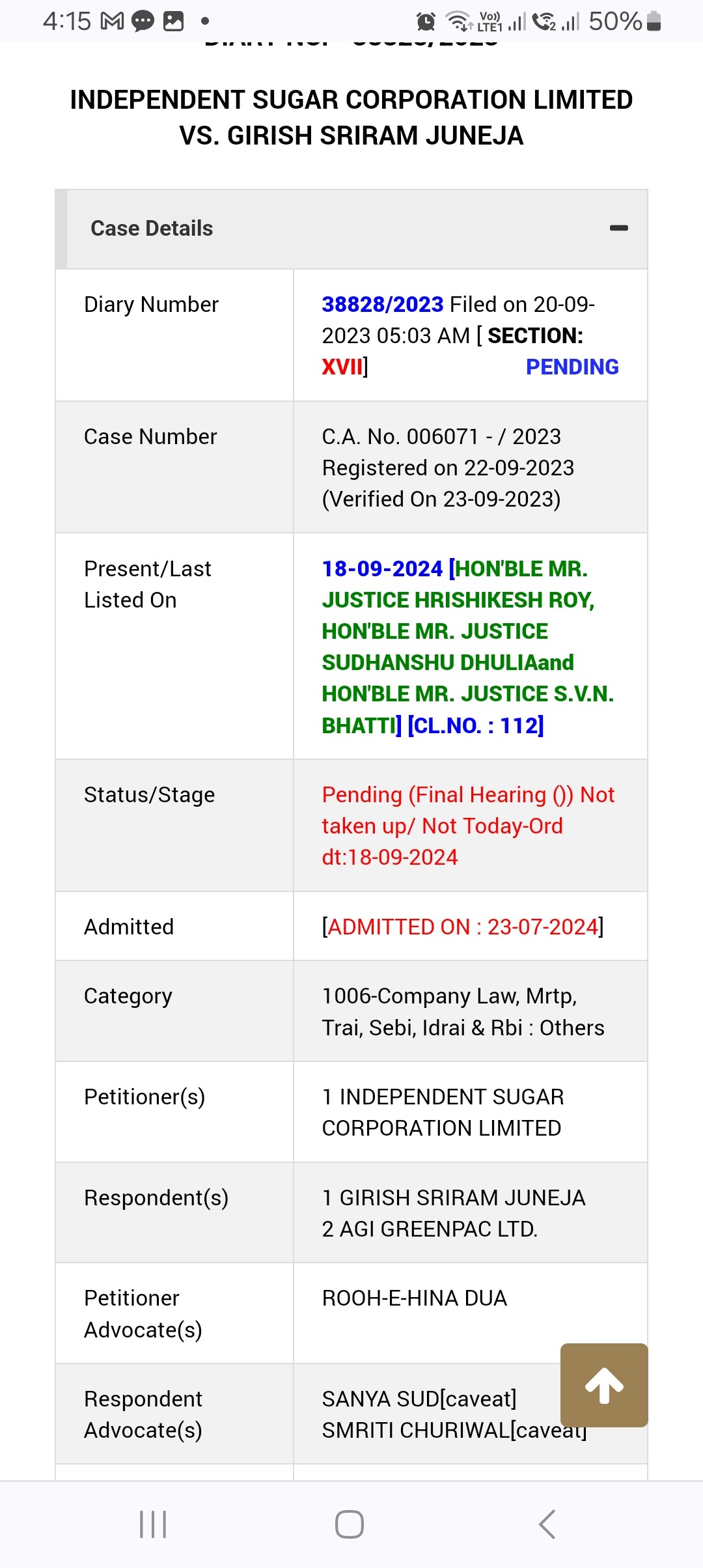

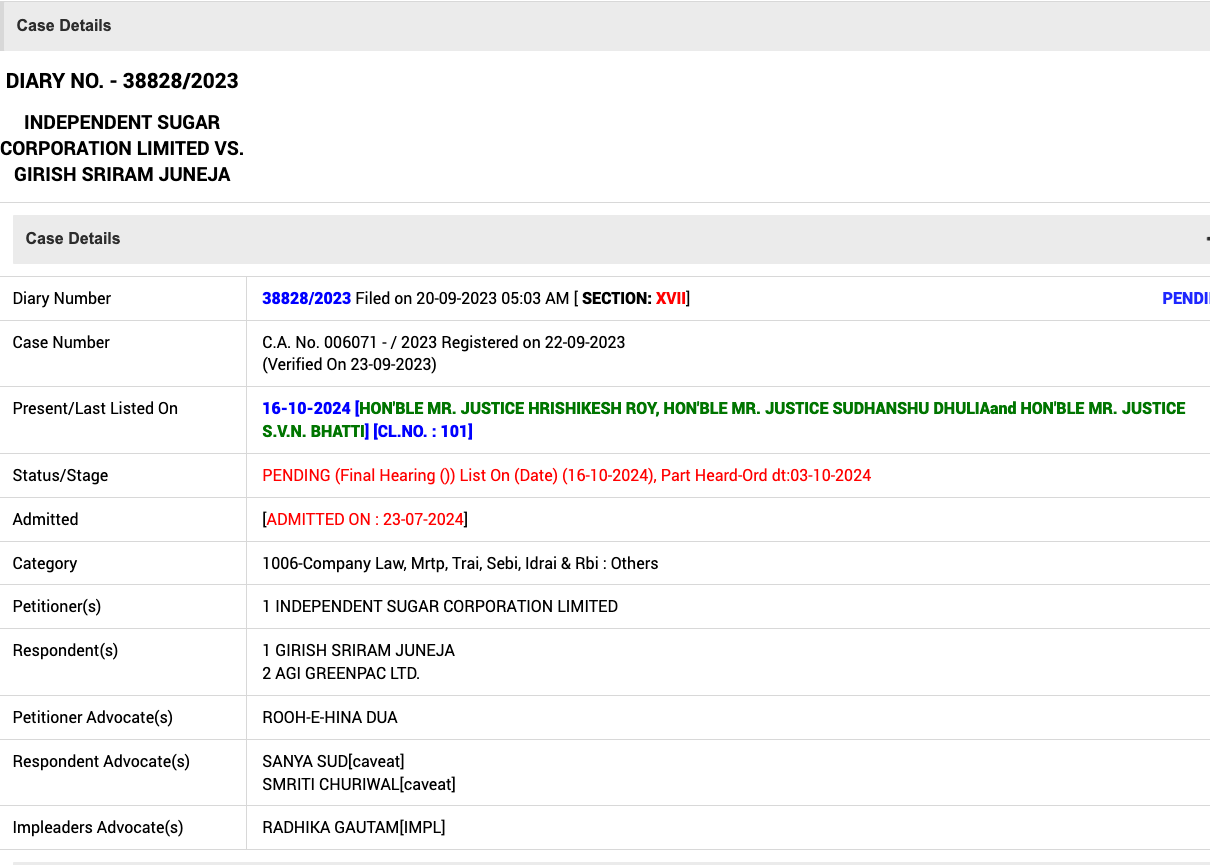

Diary number 31185 and 38828 year 2023, both next hearing on 06/11/2024.

Tareek pe tareek. ![]()