1.What is the typical realisations per tonne of glass manufacturing?

2.How many Bear Bottles can be carved out on a per tonne glass-Can the Revenue be increased if they manufacture >1Liter bottles or Bigger Bottles?

1 Like

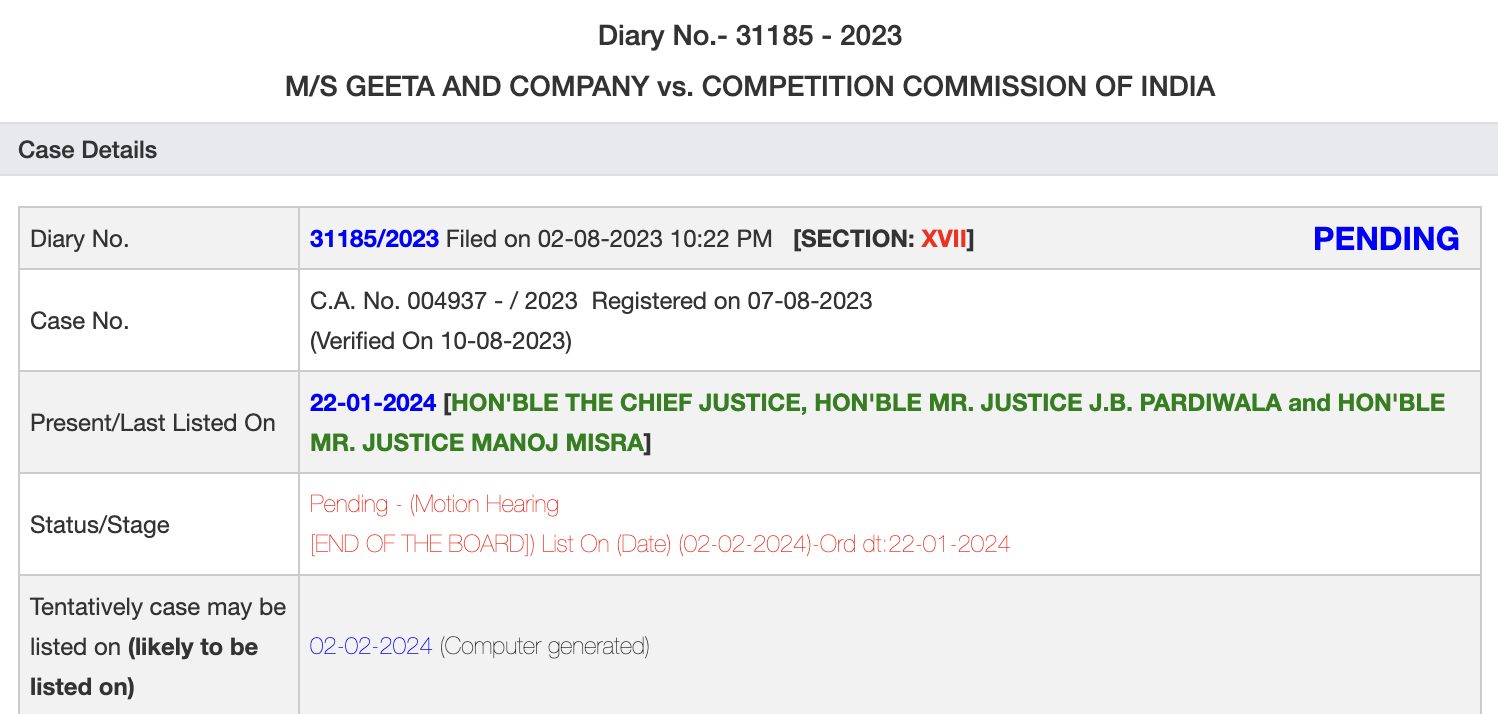

Bro, did this tentative case hearing heard on 22 Jan?

Average realization is around INR 37000 to 38000 per tone. EBITDA is around INR 10000 per tone. For speciality glass average realization per tone is 1.7 to 1.8 times more than normal product segment. For AGI , Speciality Glass division capacity of 154 mtpd is running at 65% to 70% utilization.

For second question I dont have any straight forward answer. Smaller pacakge used in Cosmetic and Perfumery(C&P) has better realization. Speciality Glass also used in bevrage packaging also has better realization.

8 Likes

Looks like this SC case is not tilted in favour of AGI . And many be market is skeptical about HNG acquisition plan.

2 Likes

The basic tenet of IBC is to minimize the haircut of creditors. Once COC has approved the plan there should be lightening speed in the implementation of the plan to save the bankrupt company and its stakeholders.

On broad basis, it appears that the CCI approval condition for a bankrupt company is a joke. For a bankrupt company best suitors will come from the same industry only. They have the understanding of the economics and ecosystem and best geared to turnaround the sick company!

AGI has quoted maximum price. The loser (international sugar) is playing the delay tactics.

5 Likes

And banks cannot keep NPAs in their books for years and years…and how can someone prevent banks from selling their NPA loans to ARCs?

Infact banks will be doing injustice to their shareholders if they continue to keep rotten NPAs in their books.

If AGI’s plan is not approved by SC (after due bidding and AGI quoting maximum and their plan approved by COC. Further L2 bidder’s appeal quashed by NCLT and NCLAT) it will be sad day and HNG may die slow death.

5 Likes

Date moved to 9 Feb. Taarik pe Taarik!

2 Likes

Same SC bench heard jet airways case (link below).

These foreign bidders only interested in puting spanner in IBC resolution.

Same thing happened in amtek auto resolution when Britain based Liberty group just backed out after all clearances destroying the company and stakeholders (including employees).

I hope same is not repeated here .

2 Likes

Beer Season on the way - 1 more reason to enjoy the beer season now. ![]()

HNG is hogging the limelight. But earnings will remain the trigger most of the times.

3 Likes

Any update on court roceedings? Friday wad supposed to be the latest hearing

2 Likes

Again Postponed to 22 feb

4 Likes

How can we track the court proceedings, can you please share the source to track it ?

6 Likes

Hi, can someone please share the implications of the following order? Thank you

1 Like

Basically the bid for insco was not considered despite being compliant with the CCI approval

And AGIs was considered by coc despite not getting a greenlight from CCI.

The court order has asked that insco Bbid allowed to be considered and AGIs opposition to it be dismissed

This means INSCO will push lenders and the RP to go back to bidding and the bids will go higher.

Lenders will make more money but who gets the asset is unknown.

So even if AGI rebids and wins

A) it will cost more money

B) It will take more time

Both are bad for AGI

6 Likes

There is no court order.

This is just CCI order reaffirming international sugar approval. (Since AGI had filed objection 9

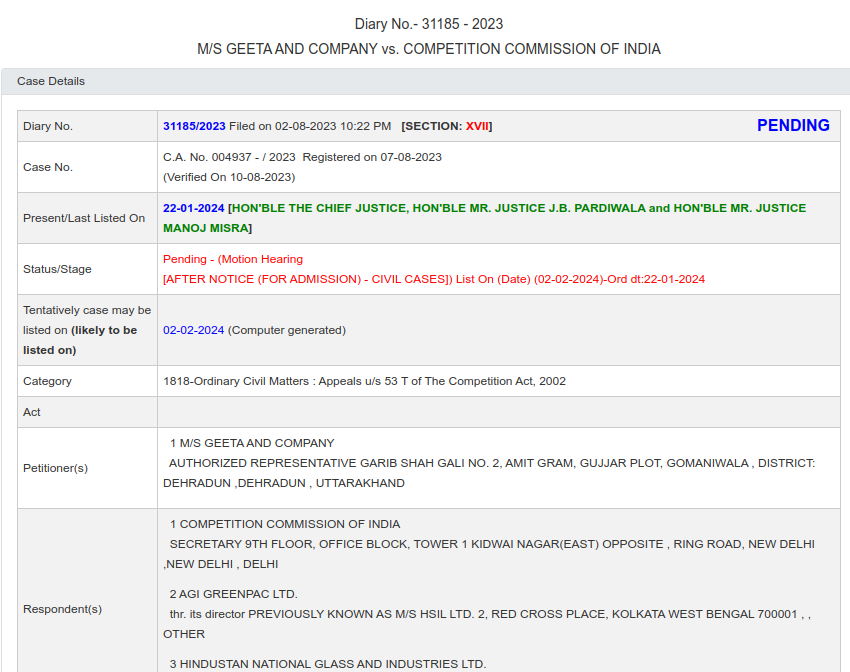

Case is tentatively listed for hearing on 23 Feb in supreme court.

With passage of time, HNG’s furnaces have become inefficient and dangerous without any repairs and maintenance.

If one or two years further pass on this IBC , HNG would have died slow death.

4 Likes

next date is on 27th feb

The entire case in the supreme court was by international sugar that they were not given a chance to bid inspite of greenlight approval

So if the CCI has now allowed it isn’t the case redundant ?

Regardless, this will mean a rebid for the asset with the COC. And the RP.

so AGI winning this is not certain at all

1 Like