Customer data is such a arcane concept in digital marketing and exploited and spun off in different ways. For example, no one has more granular customer data than the walled gardens like google, facebook, twitter and Tiktok. Many digital marketing co’s claim to have granular customer data but they are mostly probabilistic data points not deterministic ones that walled gardens possess. Unless you have owned data where users actually register or sign in/opt in like in the case of facebook and google very few can claim to have opted in customer data .

1 Like

Affiliate space. Can’t compare with 1st party data that these behomoths have.

Despite posting consistent good numbers, Affle is still under pressure. Does anyone know why?

They lost real money gaming clients due to government ban and stock also not cheap though.

If I remember correctly they mentioned they could have some impact this quarter due to RMG client ban but it was mitigated by early indian festivals and it will be interesting to see how next couple quarters they will perform.

7 Likes

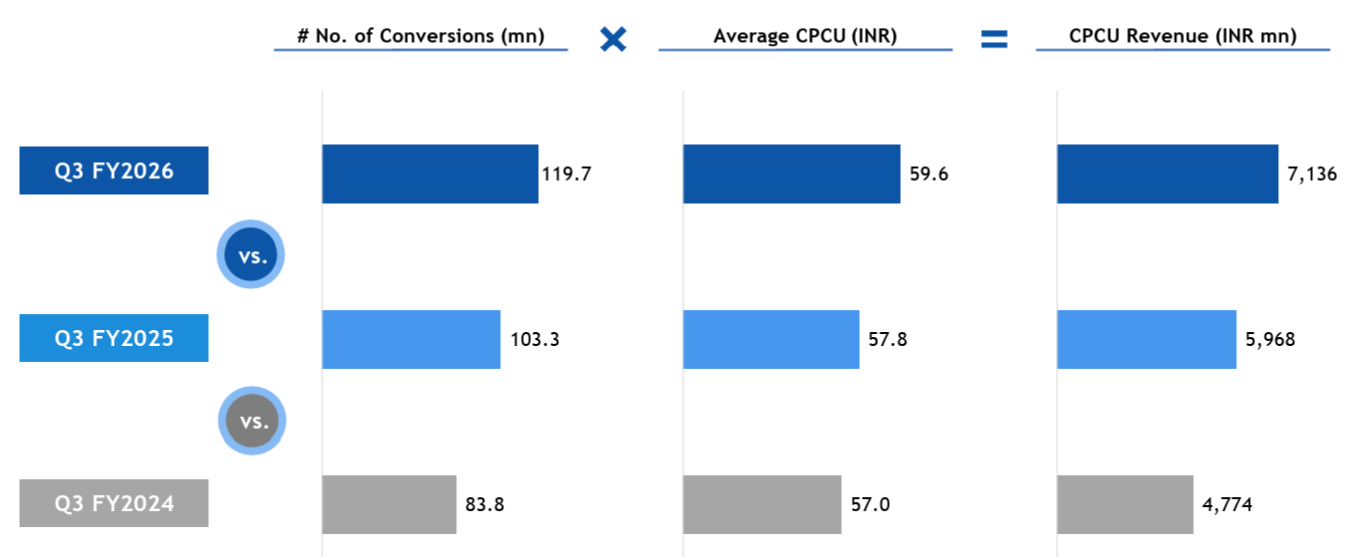

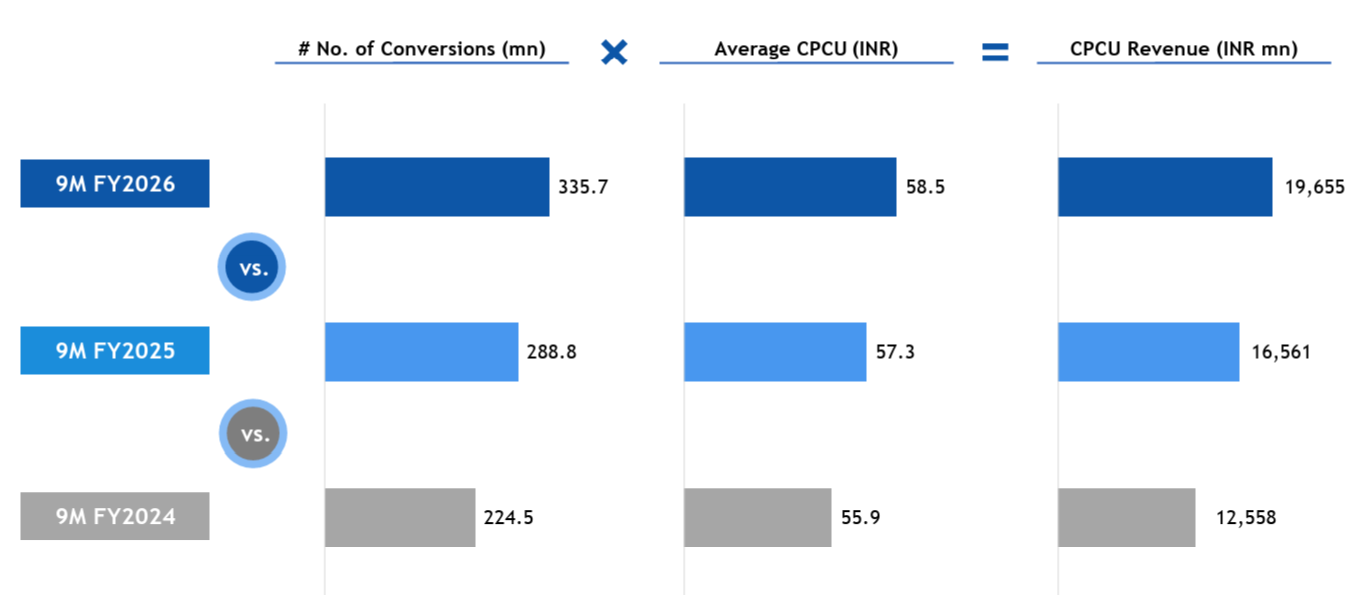

Most Interesting Slide on CPCU. Record Conversions and Revenue

Go Through the Investor Presentation Once

1 Like

Agree good numbers and I like there examples they give in investor presentation ppt like every quarter they give different real buisness use case examples how they helped in terms of advertising and increased there sales,roas etc

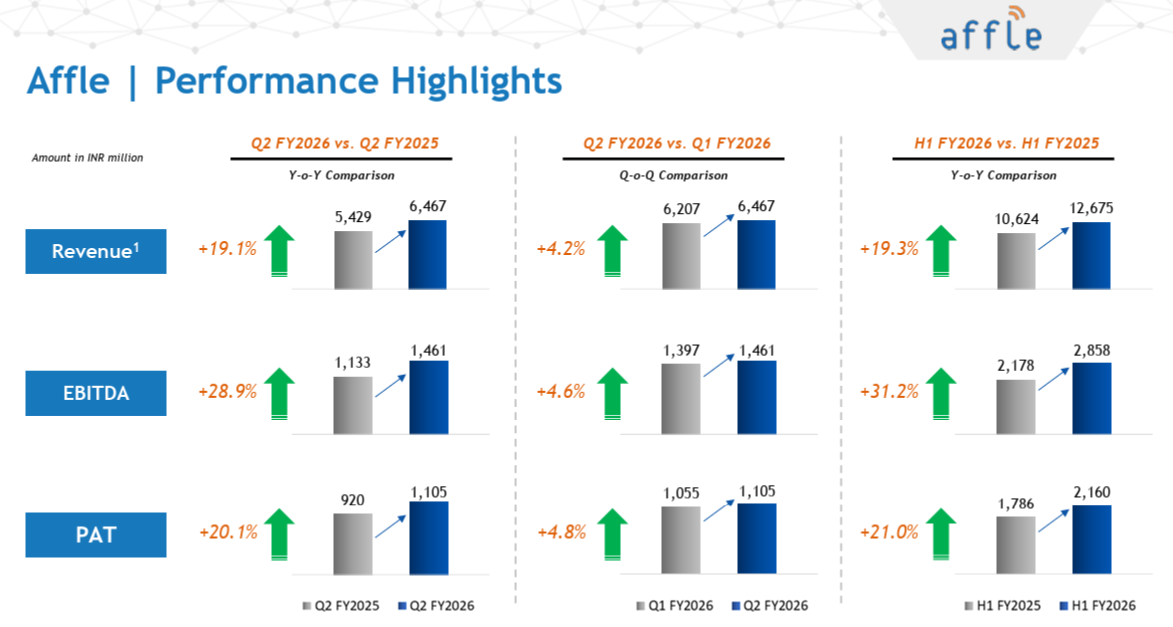

Only concern there revenue growth not growing 25% instead it is growing 20% which is also good maybe beacause they lost real gaming clients due to government ban but will get some clarity in the concall.

1 Like

Yes, I agree, but despite the gaming hit, their CPCU model still delivered 12 crore conversions this quarter. Even if they aren’t growing at 25%, the business they do have is very high-quality and sticky.

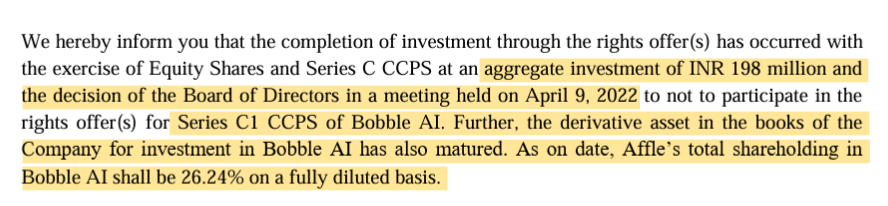

Have to see a few things first, whether the RMG impact has finally bottomed out. Secondly, the contribution of recent acquisitions (like YouAppi or Bobble AI) to the organic growth mix. and of course guidance for the full year FY27.

3 Likes

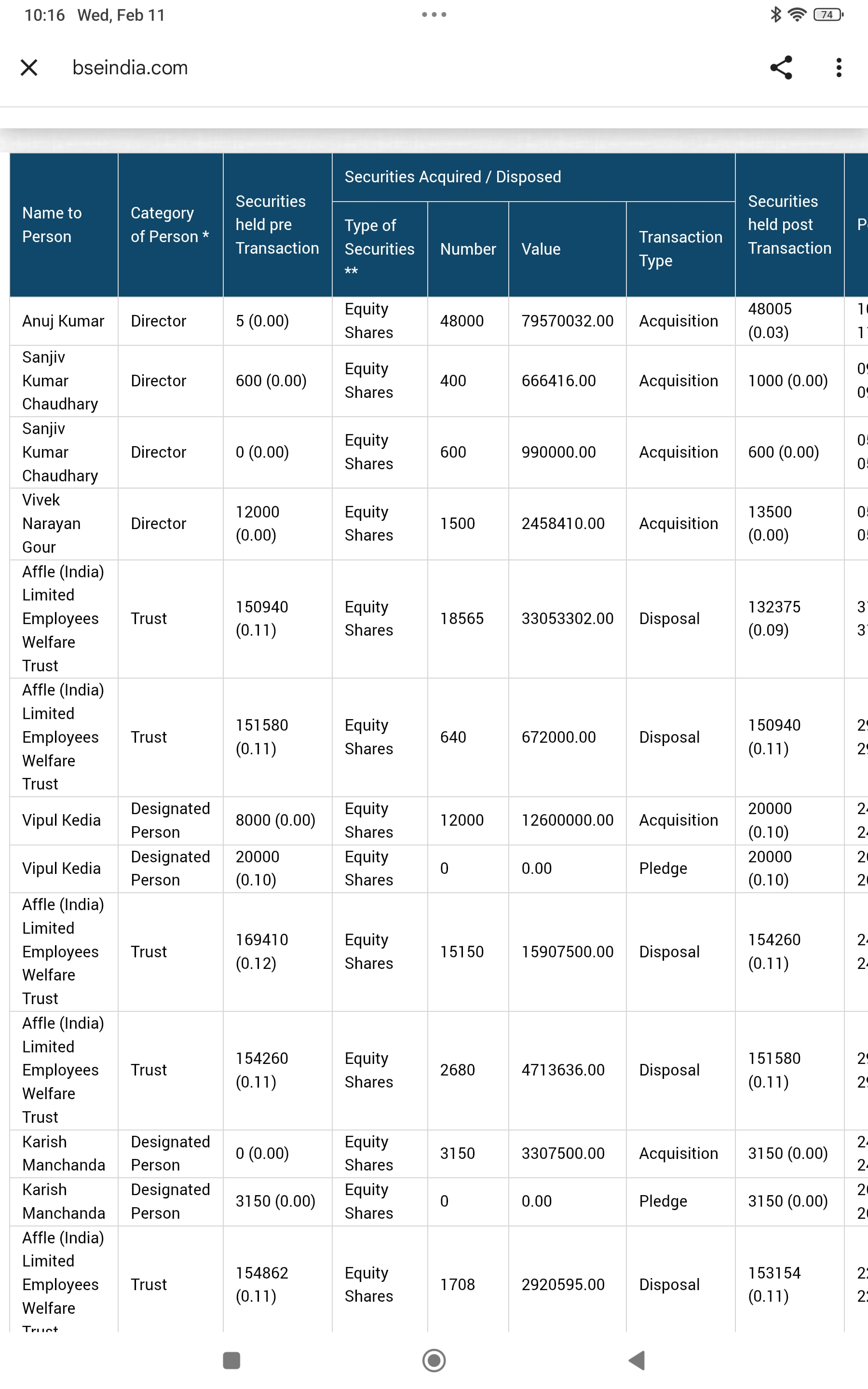

3 Independent directors of affle buying from open market and today it caught my attention because Anuj Kumar who is independent director as well as co-founder of affle and chief revenue & operating officer bought stake around 7.95 crores.

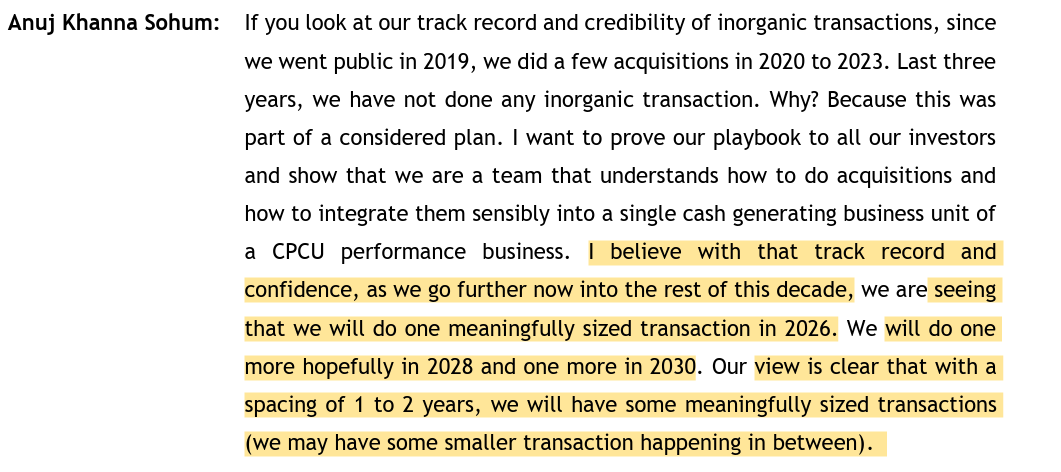

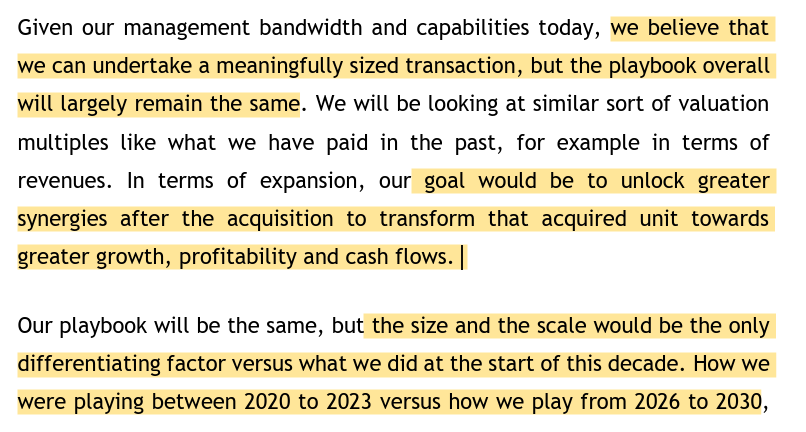

Anuj khanna ceo in Q3FY26 concall hinted some acquisitions are going to happen and maybe it will happen very soon.

3 Likes

i dont think any tranasction (acquisition) of bobble has happened over last few months by Affle

Anuj continuously bought shares, after 48K again bought 25+13k = 38K.

1 Like

Page 26: I am looking forward to our company turning 21 years old on 5th of April 2026. There will be exciting news to follow. We have laid a great foundation for Affle 3i in its first year already.

1 Like

Inspite of admirable revenue and EBITDA growth, stock price growth of Affle is very poor: A mere 7% CAGR over 5 years

I do not think so. At the time of Covid, it was 400/- and now 1600/-

Yeah, a classic case of earnings catching up with valuation. It’s Dmart of IT sector. ![]()

In early 2021, Affle was trading at a trailing P/E of 160x. Investors were pricing in decades of perfect growth. Even though the company delivered 30%–40% growth, it wasn’t enough to justify a 160x multiple.

Over five years, the market de-rated Affle from 160x to roughly 40-50x. When a stock’s valuation multiple drops by two-thirds, the earnings must triple just for the stock price to stay flat. And that’s what happened in this case. just like Dmart.

The good news for a long-term investor is that the risk-reward profile is now much healthier.

The froth has been wiped out. If Affle continues its 20%–25% earnings growth from this 50x P/E base, the stock price is far more likely to track earnings growth moving forward than it was in 2021.

3 Likes