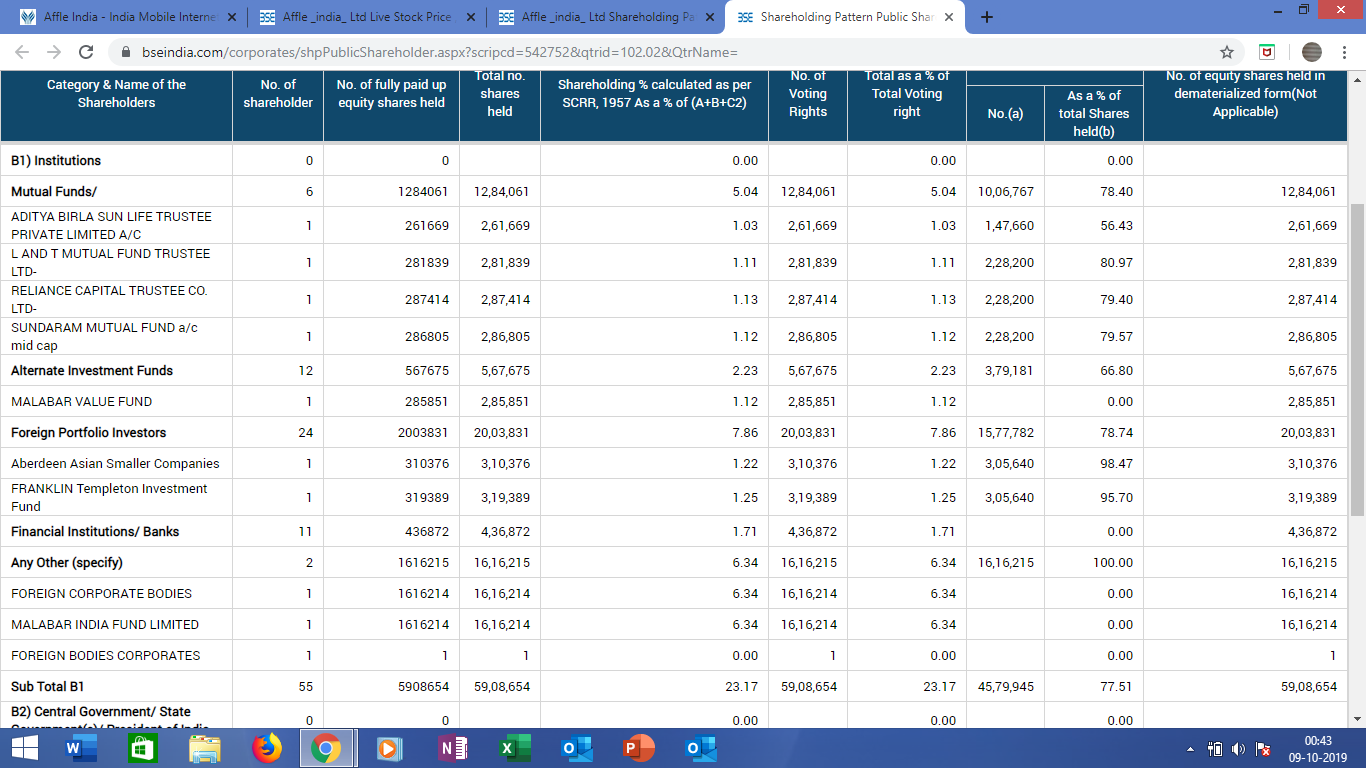

New IPO with current market capitalization of Rs2816crs. Promoter holding is 68.38%. Main public shareholders as below.

Affle India Limited is a Mumbai based company engaged in the business of mobile marketing with its digital platforms. The company offers a consumer and an enterprise platforms to its clients. With these products company tries to improve the ROI on digital marketing campaigns for clients, reduce the ad frauds, maintaining consumer privacy and more.

Affle India was initially incorporated as “Tejus Securities Private Limited” in 1994. It was then subsequently converted to a public limited company on July 13th 2018 and the name was changed to ‘Affle (India) Limited’

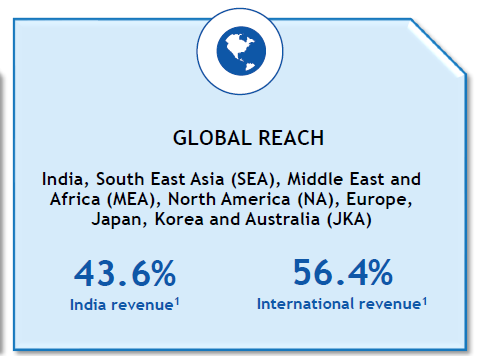

Affle Consumer Platform’s had approximately 2.02 billion consumer profiles as at March 31, 2019 of which approximately 571 million were in India, 582 million were in Other Emerging Markets (which comprises Southeast Asia, the Middle East, Africa, and others) and 867 million were in Developed Markets (which comprises North America, Europe, Japan, Korea, and Australia). During Fiscal 2019, the Affle Consumer Platform accumulated over 300 billion data points, which power their prediction and recommendation algorithm.

New IPO which listed on August 8, 2019

Promoters of the company

Anuj Khanna Sohum and Affle Holdings are the joint promoters of the company

How They Earn Revenue?

a) They Primarily earn revenue from their Consumer Platform on a cost per converted user (“ CPCU ”) basis, which comprises user conversions based on consumer acquisition and transaction models. The transaction model is usually in the form of a targeted user submitting a lead acquisition form or purchasing a product or service after seeing an advertisement delivered by the Affle .

b) They also earn revenue from their Consumer Platform through awareness and engagement type advertising, which comprises cost per thousand impressions (“CPM”), cost per view (“CPV”) and cost per click (“CPC”) models.

Industry they serve

Their products are used in e-commerce, fin-tech , telecom , media , retail and FMCG companies, both directly and indirectly through their advertising agencies

Asset Light Model

Their Consumer Platform business is asset-light and scalable as shown by the fact that company’s employee benefit expenses, depreciation and amortization expenses, and other expenses have remained relatively unchanged despite significant changes in our revenue in the last three fiscal years.

Other facts

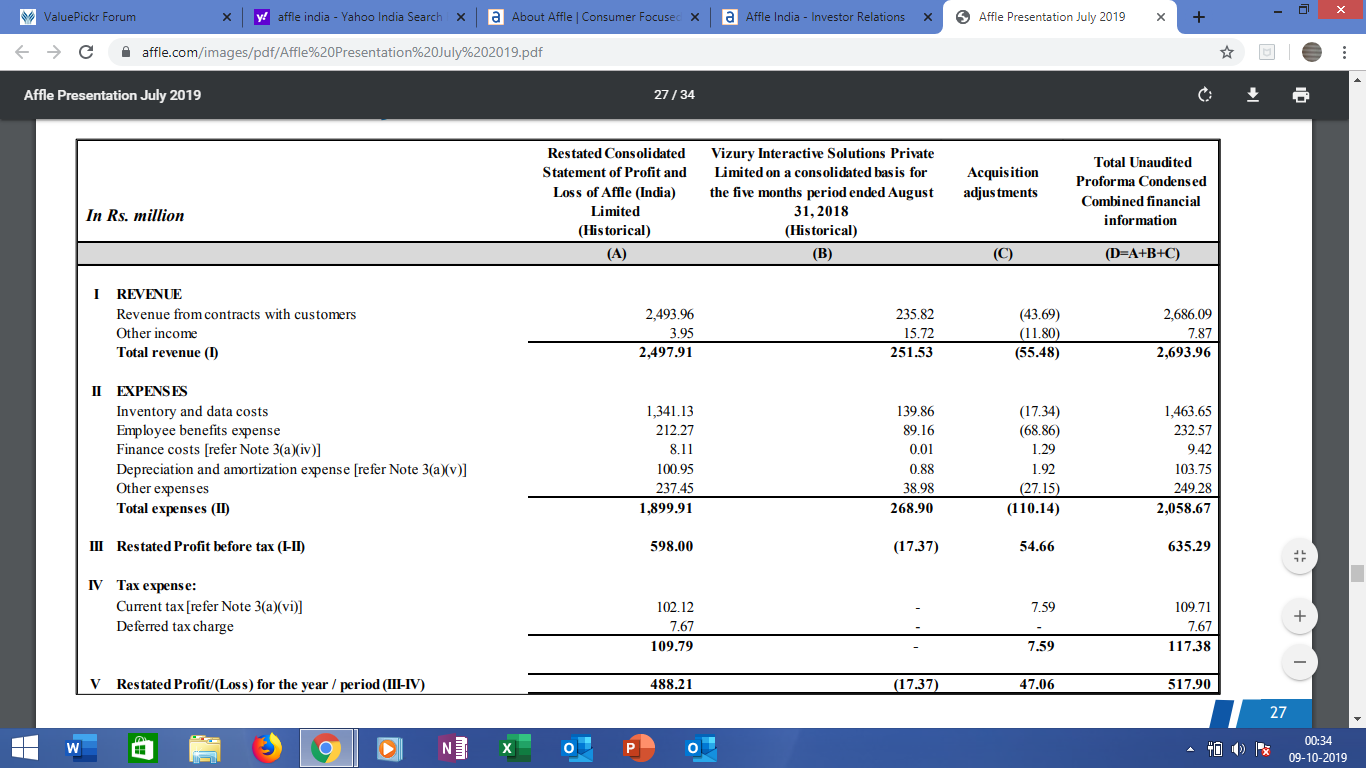

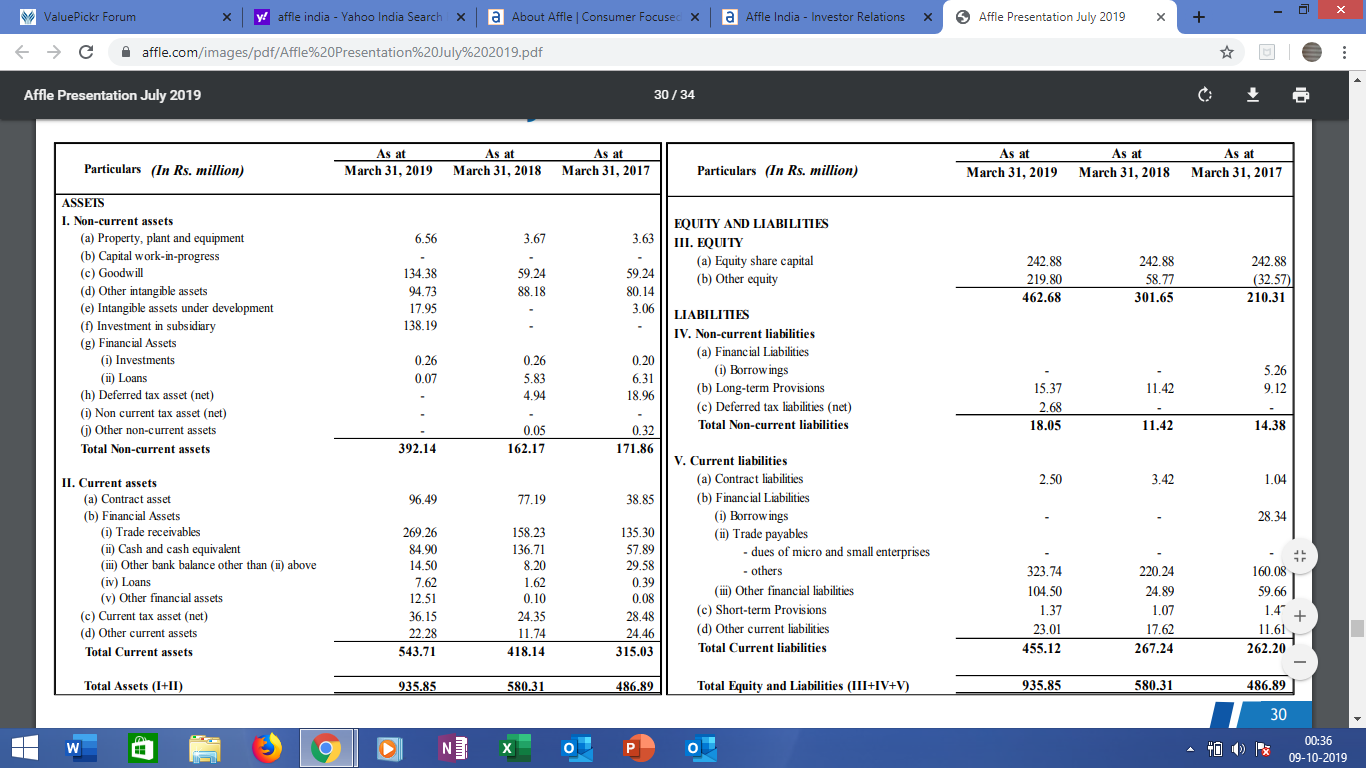

The company has acquired two subsidiaries in 2018-19 that is why Consolidated Financials have been prepared for this year.

The Company unlike tech startups not burning investors money but generating free cash which is a healthy sign for the business

Key Risks

If our ability to collect significant amounts of data from various sources is restricted by consumer choice, restrictions imposed by customers, publishers and browsers or other software developers, or changes in technology it may have a material adverse effect on our business, results of operations, cash flows and financial condition.

Regulatory, legislative or self-regulatory developments regarding data protection could adversely affect our ability to conduct our business.

If we fail to predict an engagement by consumers with mobile ads with a sufficient degree of accuracy, it could have a material adverse effect on business, results of operations, cash flows and financial condition.

The market in which we participate is intensely competitive and we may not be able to compete successfully with our current or future competitors. Although it is dominated by digital giants such as Google and Facebook, there are over a hundred companies around the world who offer one or more components of this solution. However, only a few companies/groups operate internationally, including, among others, us, InMobi, Criteo,

Tradedesk, Freakout, Mobvista and YouAppi.

If we are unable to protect our proprietary information or other intellectual property, our business, results of operations, cash flows and financial condition could be adversely affected.

Affle IPO RHP https://d2un9pqbzgw43g.cloudfront.net/main/Affle-India-Limited-Red-Herring.pdf

Financials Consolidated for FY19

DISCLOSURE: INVESTED