I believe they overpaid here. They should only invest in AdTech.

Disc: Reduced holding and small investment.

I believe they overpaid here. They should only invest in AdTech.

Disc: Reduced holding and small investment.

The assumption here is correct. Affle does not in fact use any cookies as that is a tech only applicable in the browser/web environment whereas affle is purely mobile /in app specific player.

However, privacy issues/regulatory concerns pertaining to digital advertising (mobile advertising being a sub -set of that) is going to restrict/lessen any ad tech player ability to precisely target the intended users compared how they used to do it before. OEM partnerships and SDK integration allows this phenomenon to mitigated when it comes targeting the intended users for which the advertisers pay big bucks.

The entire industry is coming up with sandbox solutions whereby the user privacy is not compromised and at the same time the ad tech players like affle can continue to attract big advertising dollars because of the value ad products that they have i.e. Appnext (in app targeting platform), Revx ( Retargeting platform) etc.

My view is that by buying all kinds of different ad tech platforms that they have in recent history will allow them to capture the advertising dollars that percolate outside of the walled gardens like Google and Meta. By acquiring significant scale they can outcompete all the long tail and smaller ad tech players.

This would for sure have lot of implications on their EBITDA margins and not to mention the difficulty of the integrating the various different cultures of the companies that were started in different countries like Brazil, Israel etc.

What is interesting to me also that unlike inmobi (the next biggest ad tech player in india focused on mobile advertising) has been constantly trying to incubate and create new products in programmatic, sdk /OEM partnerships etc in house and not relying on whole bunch in acquiring businesses from outside. Affle on the other hand is flushed with Capital which it has decided to deploy in acquiring different businesses with different offerings from different geos.

What strategy will work only time will tell !

Our 15-gen AI patent filings have strengthened our intellectual capital and the Rs. 7.5 billion recently raised cash capital has strengthened our financial balance sheet

We consciously invested in new product use cases and ecosystem-level partnerships to unlock premium inventories and touch points on connected devices including CTV, Apple SKAN, iOS App Store, and other OEM app stores both in India and international markets. This was the first significant step towards our long-term strategic direction as the premium converted users enable higher lifetime value for advertisers

We continued to enhance our consumer-centric platform offerings progressively delivering stronger than ever quarterly EBITDA of Rs. 967 million and PAT of Rs. 768 million. Our CPCU business

delivered about 84 million conversions during the quarter, at a CPCU rate of Rs. 57.0 helped us achieve CPCU revenue of Rs. 4.77 billion, an increase of 38.2% y-o-y and 19.2% q-o-q

We continue to witness a robust market opportunity as advertisers steadily accelerate their digital spending, resulting in broad-based growth in our CPCU business in global emerging markets.

Our growth in Developed Markets together with YouAppi was about 67% y-o-y and 14% q-o-q

While most of the other industry players are adopting Gen AI to optimize human capital and cost, Affle is investing in Gen AI-powered innovations to go much beyond cost efficiencies to enable long-term revenue growth and competitive advantages

We filed 15 new patents in India during Q3. These patents power futuristic use cases of interaction, training, and integration of Gen AI agents and cover advanced AI areas including personalization & recommendation, predictive analysis, privacy, and enhanced fraud detection

We have included 3 case studies, which are focused on travel, food tech, and e-commerce conversions for a global FMCG company

Our Affle2.0 Consumer Platform Stack continues to be recognized in the industry as the top performer and we recently won top rankings and awards across various industry forums and indexes.

The actual pain area of the business is developed market and RMG in India. Some of the Key abstracts from the concall for better understanding:

Page 6: In the developed markets, the growth what you are seeing has been long awaited. First of all, in developed markets we were degrowing for several quarters. We were dealing with deeply internal issue and sorting them out. We knew we would sort it out because we had a clear action plan. We have to see the growth in that context. This is the growth that we deserved, which belonged to us but had evaded us because of certain issues. We fixed those issues decisively and won it back.

The bad news of CY2023, the subdued quarters of developed markets, will appear as better performance in CY2024 because as we build up from here you will start seeing much bigger year-on-year positive trends for developed markets.

Question on RMG: We have seen some sequential weakness because of RMG to some extent. Is RMG now coming to the base and we will see good growth from here on?

Answer: RMG has impacted us basically in the last two quarters - in Q2 FY2024 and Q3 FY2024. In Q2 FY2024, RMG impacted us in midway because of certain regulatory changes, which impacted the fundamentals of the RMG category and kind of ROI measurement these people do. There was a clear impact and last quarter we quantified it. This quarter the impact was bigger because typically bigger budgets were expected from RMG, but they were holding back. The impact was for the whole quarter Q3 FY2024 versus half the quarter of Q2 FY2024.Once RMG budgets come back, we will be the first company to take them on to a profitable advertising campaign and deliver value for them.

During the quarter, the company witnessed robust market opportunity as advertisers steadily accelerated their digital spending resulting in a broad-based growth in their CPCU (Cost Per Converted User) business in global emerging markets and a successful turnaround in the developed markets.

During the quarter, the growth in revenue from India & Emerging markets was ~28% YoY. However, developed markets expanded by 105% YoY.

In Q4 FY24, the company witnessed a revenue growth of 15% YoY in India.

The other expenses increased by ~89% YoY & ~20% QoQ to ₹40 crore, on account of higher sales and marketing costs to support developed market growth during the quarter.

The organic growth for the company was ~18.5% YoY in Q4 FY24.

Data and inventory cost stood at ₹1,125 crore comprising 61.1% of revenue in FY24. The company is calibrating its platform to premium inventory touchpoints.

The overall market tailwind continued to be intact anchored on the accelerated consumer adoption of the digital and an enhanced organizational shift towards digitally enabled processes.

They are witnessing strong market opportunities as advertisers are consistently increasing their digital spending.

During the quarter, the company witnessed broad-based growth across verticals & geographies.

During FY24, 76% of the revenue contribution amounting to ₹1,407 crore was from direct customers.

Their strong anchoring across India and global emerging markets continued to be resilient and it contributed ~73% of the revenue in FY24.

In FY24, the CPCU model contributed 95% of revenue while the remaining 5% came from Non-CPCU.

The company has been pushing more for a CPCU-based business model to new customers as reflected in Q4 FY24 which constituted ~100% of the CPCU-based revenue.

The CPCU business revenue stood at ₹1,759 crore in FY24, a growth of 33% YoY. Converted users and average CPCU were 31.3 crore and ₹56.2, respectively.

Average CPCU grew by 10% on a YoY basis in FY24.

Conversions recorded a YoY growth of 22% during the year while the 5-year CAGR for the same was 54.5%.

The company filed 15 new patents, during the quarter. These patents power futuristic use cases of interaction, training, integration of Gen AI, etc.

They are calibrating carefully to ensure that it does not have any over-dependence on any specific vertical.

The management guided the effective tax rate to gradually inch upwards from current levels of 9% in FY24.

As long as consumer trends like smartphone usage and connected TV remain intact, they expect the business to grow at 20% in the long term.

GenAI benefits: Consumer Platform Stack to strengthen our 2Vs -

vernacular and verticalization strategy to drive greater innovation as well as operating efficiencies.

GenAI helping business in two dimensions:

One is innovation. Clearly, bringing new use cases and power of Gen AI to make our advertisers get better ROI.

The second area is improving efficiencies. Efficiencies means we can do the same things faster, better and with less manpower involvement and so on.

Whether it is coding, testing, creating media creatives, creating data science decision-making or reports, many things are getting automated inside the office. We are embracing Gen AI like a full embrace on the innovation, on the product side as well as on operating efficiency. There will be definite positive impact on the margin.

My Investment Thesis on Affle:

That’s a detailed and impressive analysis. I also firmly believe that the rate cuts will benefit Affle.

You nailed it with the threats. In the US it’s 5 more states now that have privacy laws.

R&D is a big one to stay ahead of changing technology, new standards, and regulation. There is no strong moat other than this.

@Udaibir Thank you for your positive feedback. What do you think about the recent earnings announcement by the company?

The management is very comfortable with the privacy laws and the antitrust cases. They believe that these are more threats to the walled garden players like Google, Meta and Twitter and they would rather be beneficiaries of it.

I am comfortable with the numbers reported by the company. Historically, Q3 has been the strongest quarter for the company owing to the festivities in these three months. The management in their earnings call mentioned that October has been the best month they have seen so far and Q3 to be on track to be the strongest. Hence, looking at these, I think the company still makes a compelling case to bought/hold. (Disc: Have invested a small position)

Wrote my detail thoughts on Q2FY25 Earnings here:

Hi

The festive season does give a boost to all things. We will see that spill into this quarter too for Diwali and also Xmas since US/EU markets are big customers.

Regulation is tricky for everyone equally. Big players have the resources to re-jig a system into compliance overnight. Affle is not a small player either by any means.

Reading into this deeoer - the bigger players would provide the data profiles as well - demographic, interest, behaviour. With privacy laws and iPhone data safety features , that is no longer allowed or feasible. Affle’s advantage is its other sets of services - DMP and others. There is an opening for players like Afflle for these services.

Google is working on a Topics API to target users throught the browser. It’s been in the work for 3-4 years and was rolled out now (phased roll out starting 2024 Q1). The fledgling tech will mature and close the advantage. However, the first version of it called FLoC (Federated Learnign of Cohorts) had a flaw and was not launched after 2 years of development. At the same time, Google has a lot of of weight but is not the industry standards body. Somehow the onus of creating this was taken up by Google (affects their business more?). That is another question for another discussion.

So far 7 US states have adopted a privacy law. More will follow but this also has taken 5 years or so.

Summing up - Affle like all other players will follow the change. There could be a window but not for long. Business as usual.

Yes, the Fed reducing rates and Trump in the White House will also boost consumption. Remmeber Trump gets sworn in end of Jan.

Does Applovin have similar products compared to Affle? Their stock has exploded recently, crossing $100bn market cap recently.

Yes, similar service - Acquire + Engage. They are much bigger, maturer and have great industry partnerships.

They also have Adjust, a product for attributing acquisition.

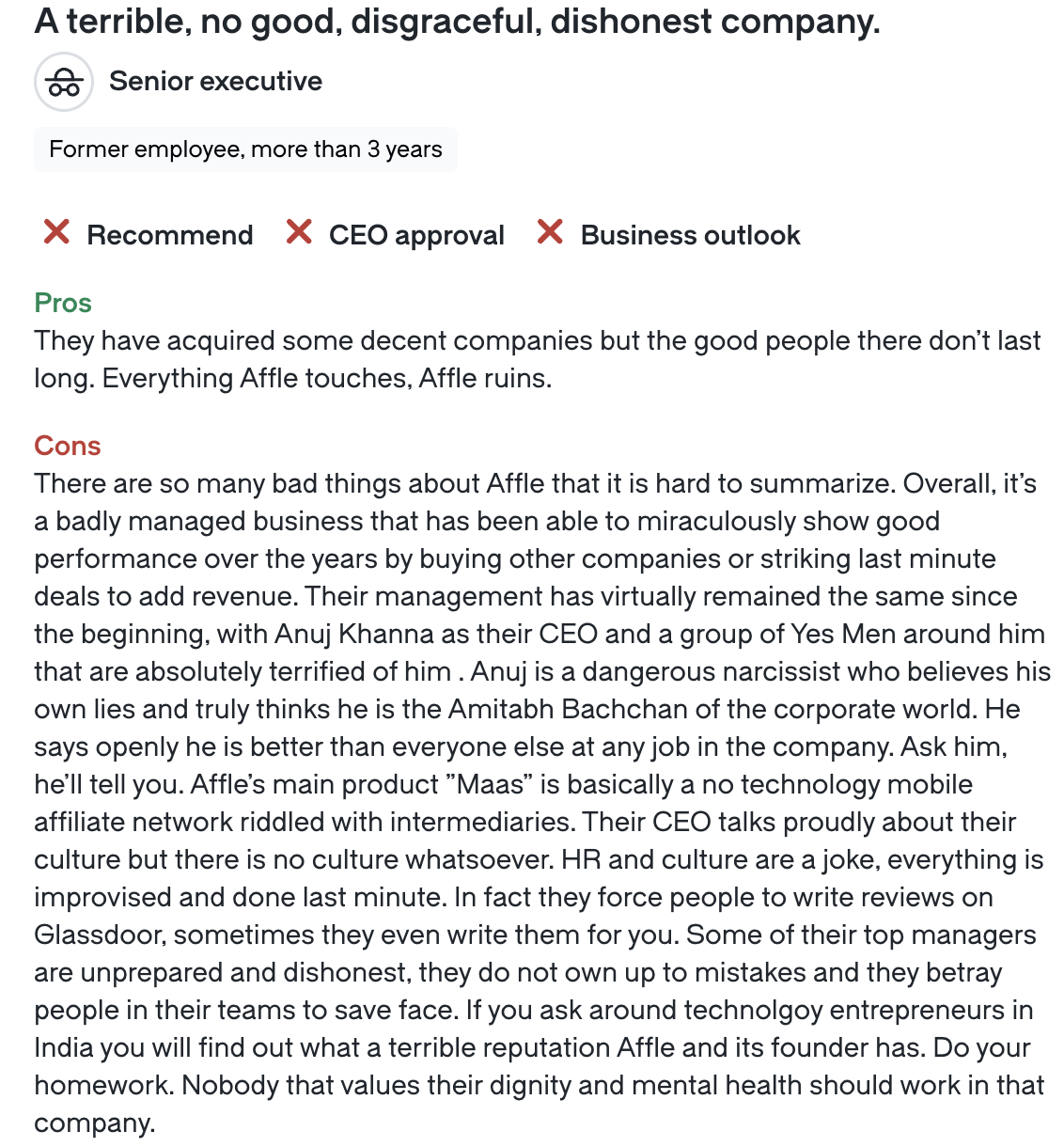

I came across these Glassdoor reviews after seeing the series of acquisitions they did. While, one has to discount that such acquisitions especially of foreign companies are hard to integrate I think its still worth considering some of the inputs provided by their former employees.

On bird eye view level they look very similar because they are into mobile app user acquisition market however look at the more nuanced perspective they have different markets captured through their products.

For example, applovin has a big market share in the gaming vertical and much better entrenched in the western markets compared to affle.

Doesn’t acquisition causes some lay offs especially in IT companies and employees from acquired company always feel the difference of work culture. At ground level folks business is as usual . I am from IT backgrounds hence I would not take the negative review totally at its face value.

Also, in the context of stock market , not sure how much we should rely on Glassdoor review

Almost all companies have some bad reviews.

Thoughts are welcome

Well, I think it distills down to the fact that sometimes a good business may not turn out to be a good stock and a good stock may not turn out to be a good business.

Yes, its true M&A could be a disruptive exercise and could potentially cause hard feelings toward the new management but based on the comments made by GD reviews

Two things that I think it’s warranted to dig deeper -

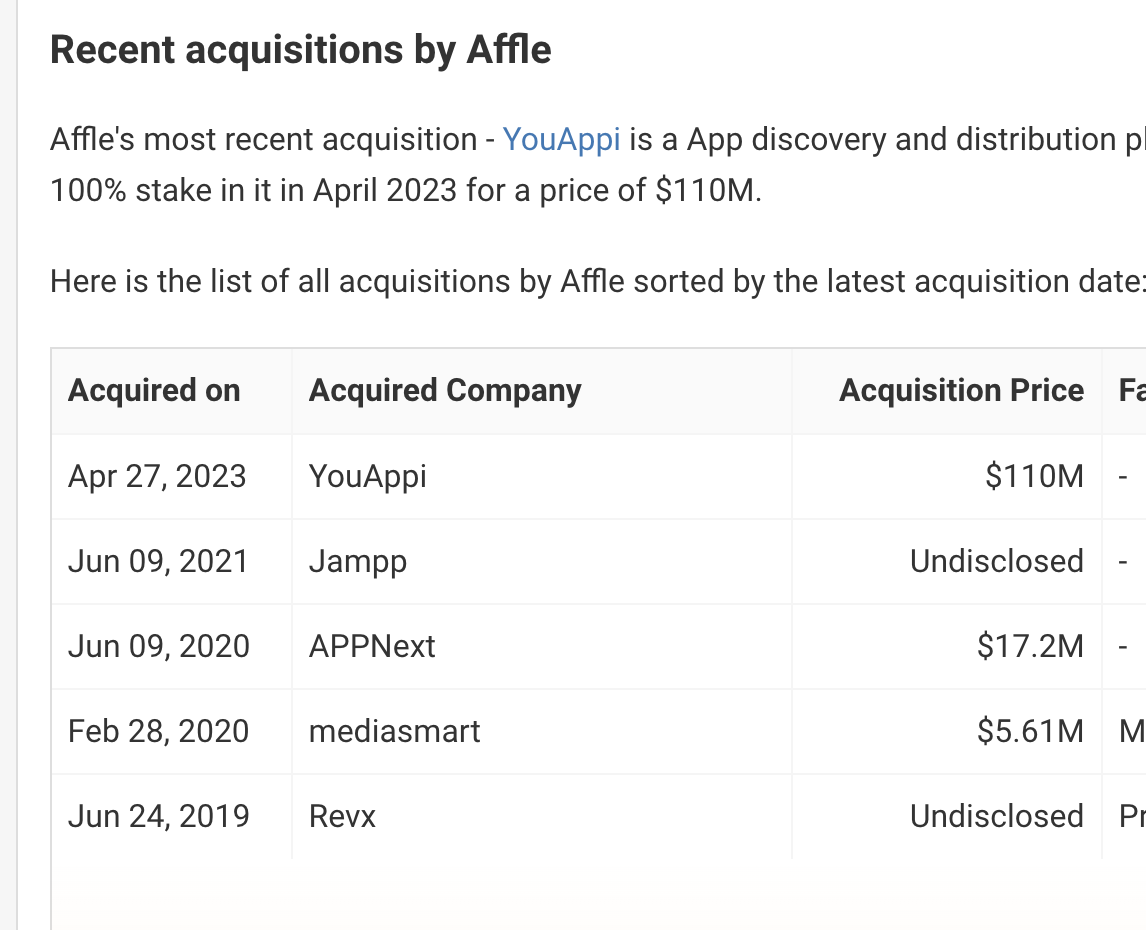

Also, was trying to trace the history of acquisitions that affle has engaged in since 2019. Reading the RHP around 2019 IPO

they had acquired

Vizury

Revx

Shoffr

and after IPO

list extended to

Youappi

Appnext

Jampp

Mediasmart

So, total of 7 acquisitions so far.

They also had some failed acquisitions like Appstudioz (based in noida) which was way before the IPO

Intro: Established in 2006, Affle (India) Ltd. (Affle) is a pioneer in programmatic

digital advertising for mobile devices in India. The Company’s unique

approach involves using a Return On Investment (ROI) linked Cost Per

Converted User (CPCU) model, where earnings are based on conversions and

positive ROI for advertisers, rather than the traditional Cost Per Click (CPC)

and Cost Per Mille* (CPM) models.

Digital Advertising Industry: The digital advertising industry has come a long way and has grown at a CAGR of 31% from CY16 to CY23, while the overall advertising industry has

grown at 9% over the same period. The digital advertisement industry has

been leading the growth rally by growing thrice at the overall industry rate

and is expected to grow by 25% in 2024.

Financial Growth Since IPO : Following its IPO in 2019, Affle experienced strong growth due to its unique business model. The Company has achieved its revenue and PAT at a CAGR of 49% and 44% from FY19 to FY24, respectively.

Operational Details

Key components of the advertising value chain

Vertical Focus: E, F, G, H

The Company focuses on high-growth areas known as EFGH verticals, which

include over 10 consumer tech industries. It provides custom solutions for each

of these verticals. These sectors are very profitable and continue to grow

despite competition. It generates 90%+ of the revenue from these 4 high

growth segments.

Quarter Results

My View

Company has its own Consumer Platform with 3.3bn devices connected and they want to achieve 10bn+ device connection by 2030 which says company wants to aggressively grow.

Realistically if people are watching mobile more than TV , its very hard for regulators to kill the cookie advertising market, mobile advertising tends to add more conversion for the customers and there fore market share and spend of digital market has grown from single digit in 2016 to 50% today.

Industry tailwind is there with proven profit and revenue growth therefore its an ideal candidate and deserves high pe , even if we assume 20% profit growth we are buying this company at 34 multiple on FY-27 forecasted earnings which is fair value .

Risk

If govts of the world decide to kill mobile and unwalled garden advertising then no one can save this company , personalised advertising is a trend and brings efficiency in advertising industry.

This is the biggest risk to the company because 70% of revenue comes from their own consumer platform business.

[/quote]