Affle reported a great set of numbers today for Q4-FY2022. Some quick notes

1- Q4-22 top-line came as 315 crores vs 142 crores in Q4-Fy21.

2- EBITDA for the quarter was 58.7 crores vs 34.5 crores last year same quarter.

3- PAT for the quarter was 68.5 crores vs 58.5 crores in Q4-21. Last year same quarter had a one- time 36 crores other income. Adjusting for that profit 98%.

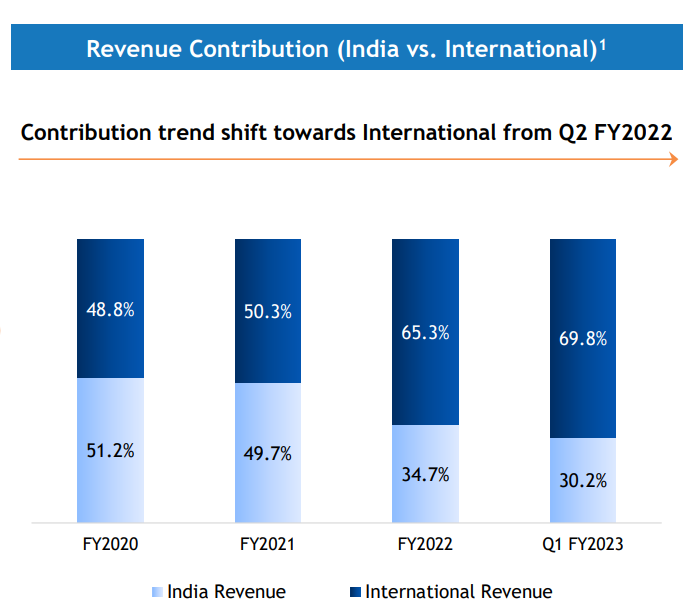

4-In Fy22 India revenue stood at 35% of total sales and 65% was from international markets.

5- Average CPCU saw a sharp increase from 41 rupees to 51 rupees year over year.

6- Converted users stood 5.66 crores in Q4-FY22 vs 29.6 crores in previous year same quarter.

Commentary on future prospects

1- With digital marketing continued to have good tailwind Affle would possibly continue to see good acquisition of new customers and retain old ones to have transactions/engagements.

2-The data enrichment and fraud models of Affle should stand for good in the medium and long term.

3- A major part of the story for Affle so far had been thoughtful acquisitions, and there is good reason to believe that it would continue on the same path.

4- For FY23, I expect Affle to clock about 25% top-line growth which would result in sales of 1350 crores. I also think that the operating profit margin to slowly increase from current 20% and possibly reach 22% for the full year Fy2023.

5- With 22% operating profit margin the operating profit for FY2023 would be 297 crores. Add about 63 crores of other income, and take out 5 crores interest and 35 crores of depreciation to that, and that would result in PBT of 320 crores. This would be about 30% of growth over the FY22.

6- Please note that there are a lot of floating variables with Affle and the calculations done by me could completely wrong. But I would continue to update after future quarterly results about how things are shaping.

Cheers,

Krishna

PS: The post above is based on the results and investor presentation. The earnings call is scheduled for Monday 16th May. I may edit the post after listening to earnings call. Also please note that I am not a SEBI certified analyst. This is not a buy or sell reco. I have ownership bias.