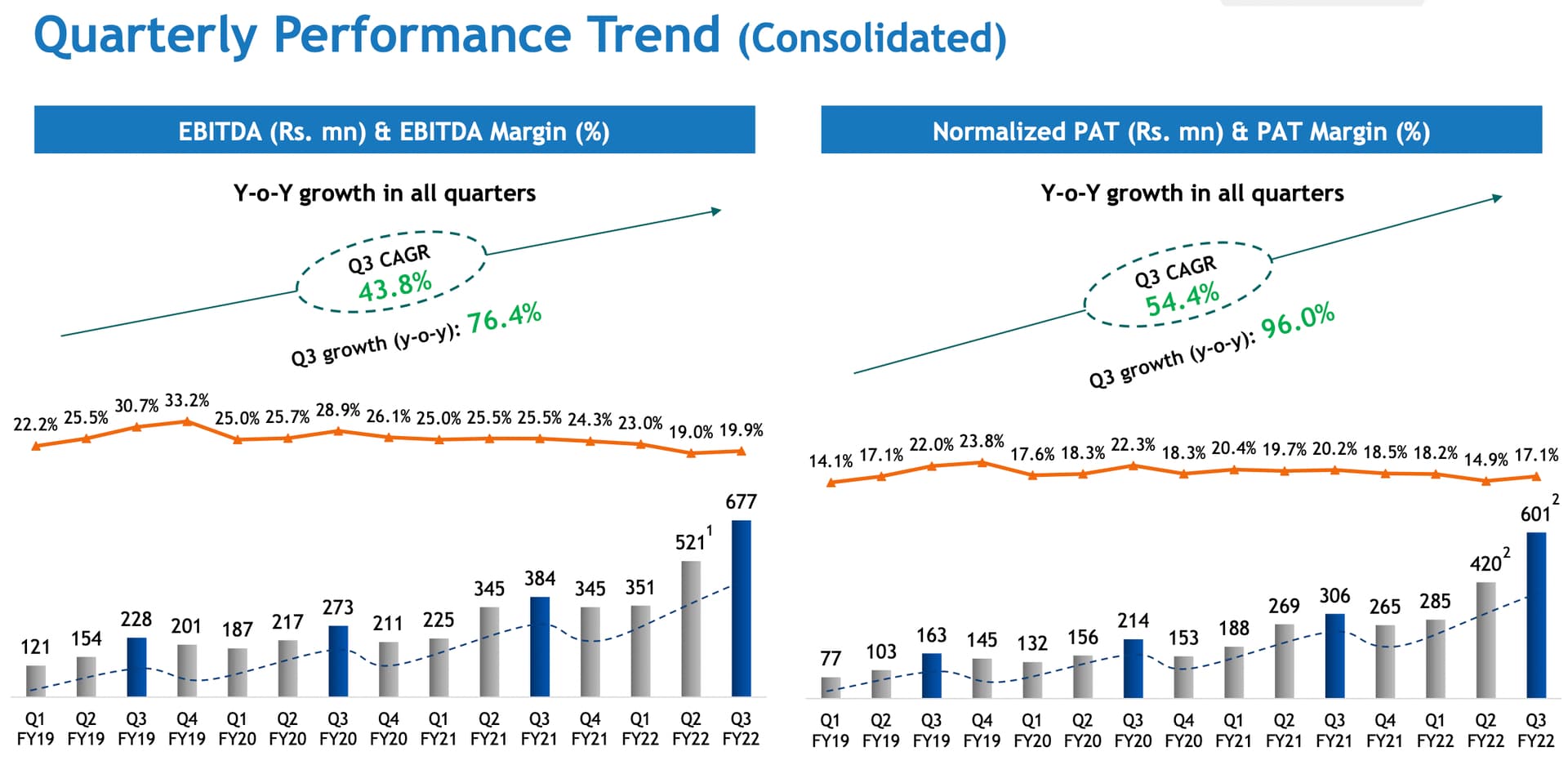

The drop in Margins for next few quarters was expected due to Jampp acquisition and same was communicated by the management during the investor call at the time of acquisition. So nothing new. Margins should be back to normal after 3-4 quarters may be?

Drop is not limited to this quarter itself, if you observe last 12-15 quarters it is on declining trend. Additionally if an acquisition is less profitable than parent company it really need to provide some strategic edge in future to justify the investment. Lets see how it pans out.

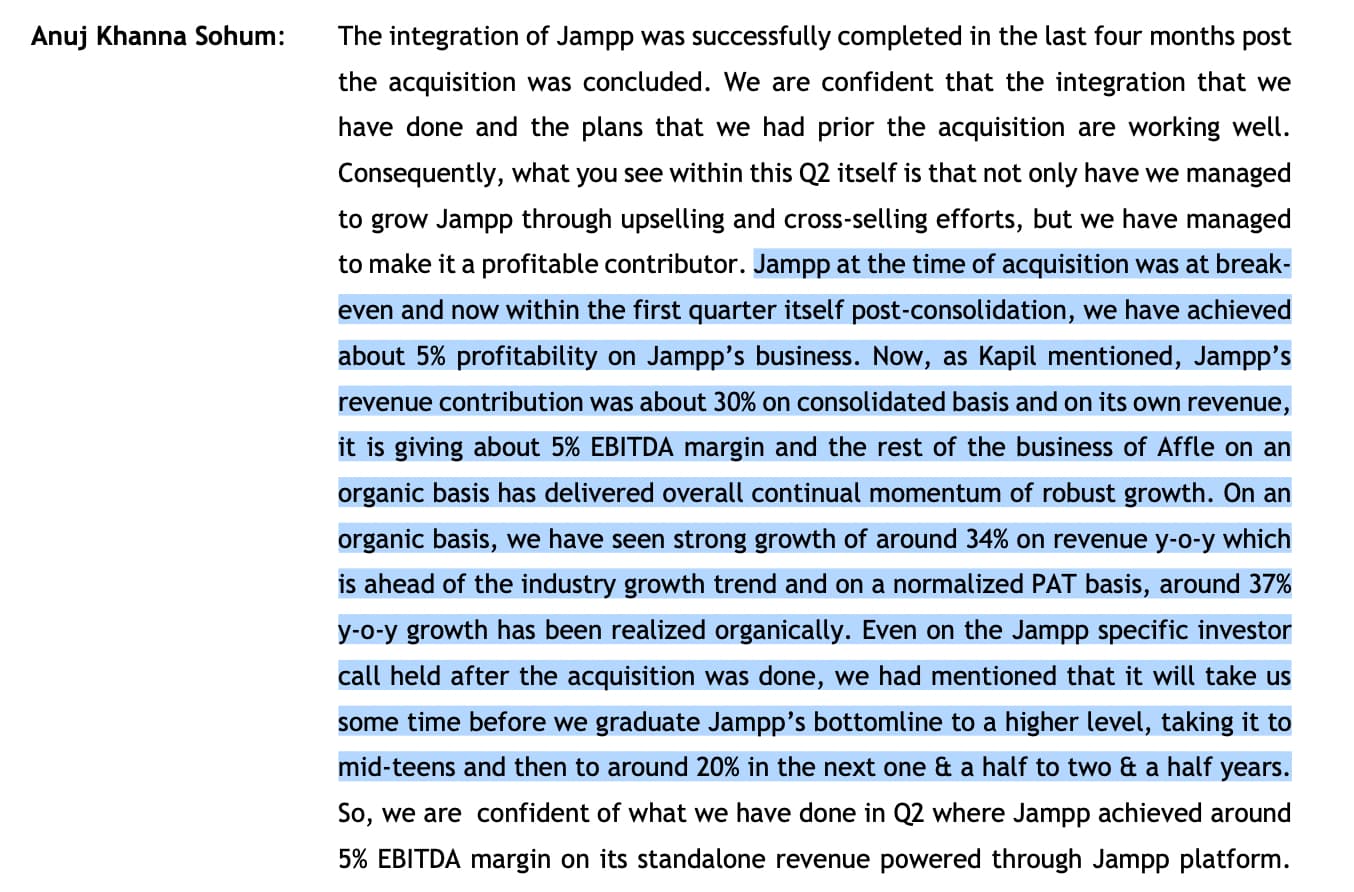

Jampp acquisition will provide Affle access to new markets. Hence Mr. Anuj Khanna was very upbeat of this acquisition and also he was smart to acquire this at very attractive deal.

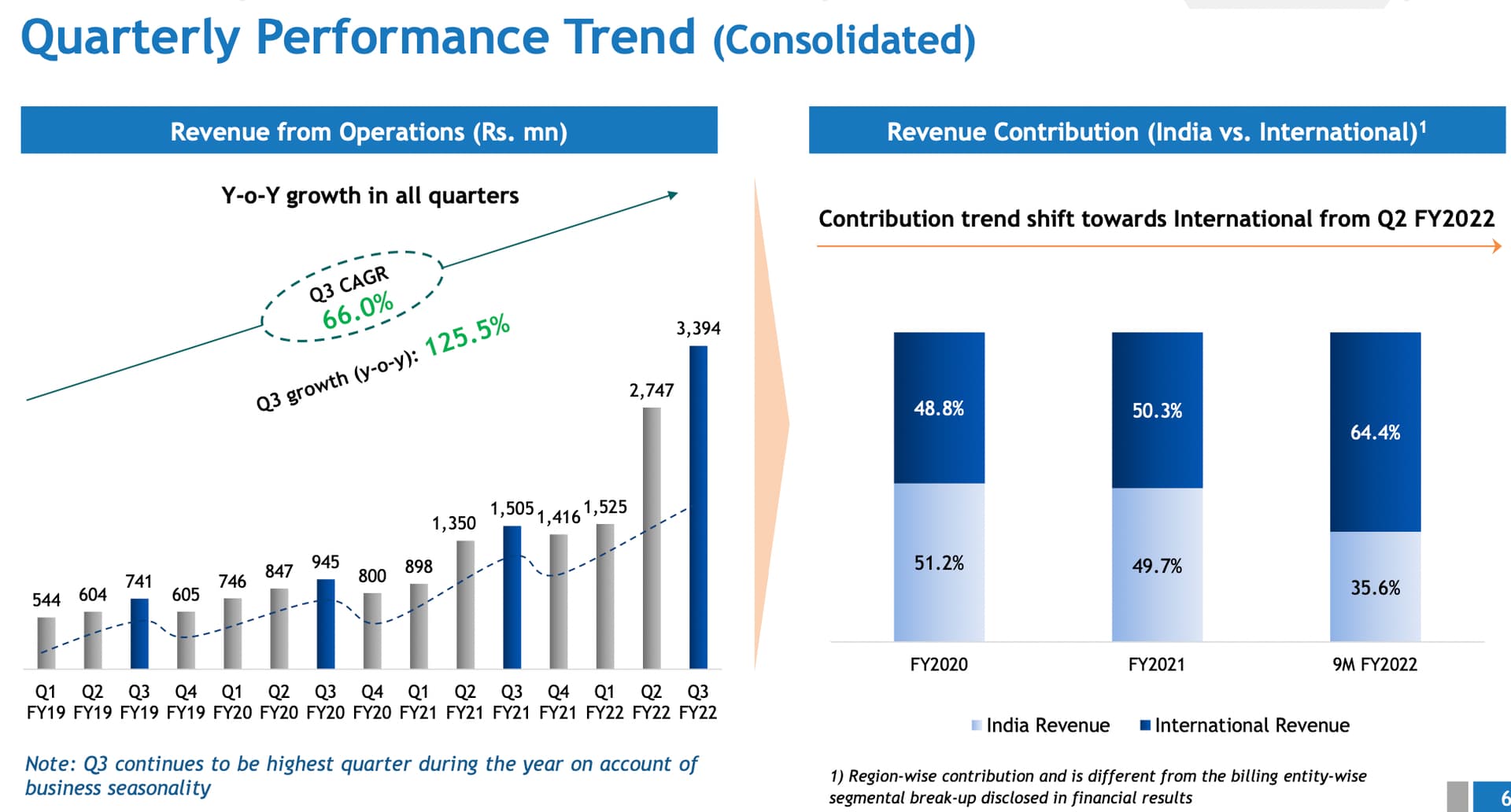

With the international expansion CPCU rate is bound to increase which is at 51 right now. Their goal is to get the new acquisitions more profitable and get to the Affle’s range which is good.

Has anyone had a close look at its acquisitions and employee cost capitalization. Seems to be very important given the high rate of growth in Goodwill and Capitalized Intangibles

If you screen for $1bn market cap co’s with 3yr Rev and PAT at 40% cagr, its a very short list of co’s and Affle really stands out for its business model, consistency and future growth potential.

In Q2, organic PAT growth was 37% yoy. The Jampp acquisition has also led to margin compression in Q2 and Q3 which is expected to gradually reverse over the next two years. This should provide a decent boost for earnings growth going ahead.