Criticism is always present when excess returns are generated in small time. How conveniently they have ignored a 20% Net Margin. A company having a high Pat margin will always look more expensive when valued based on Sales. (PS im not saying Affle is cheap, im just saying the tweet is deliberately using Mcap/Sales to portray its exorbitantly valued.)

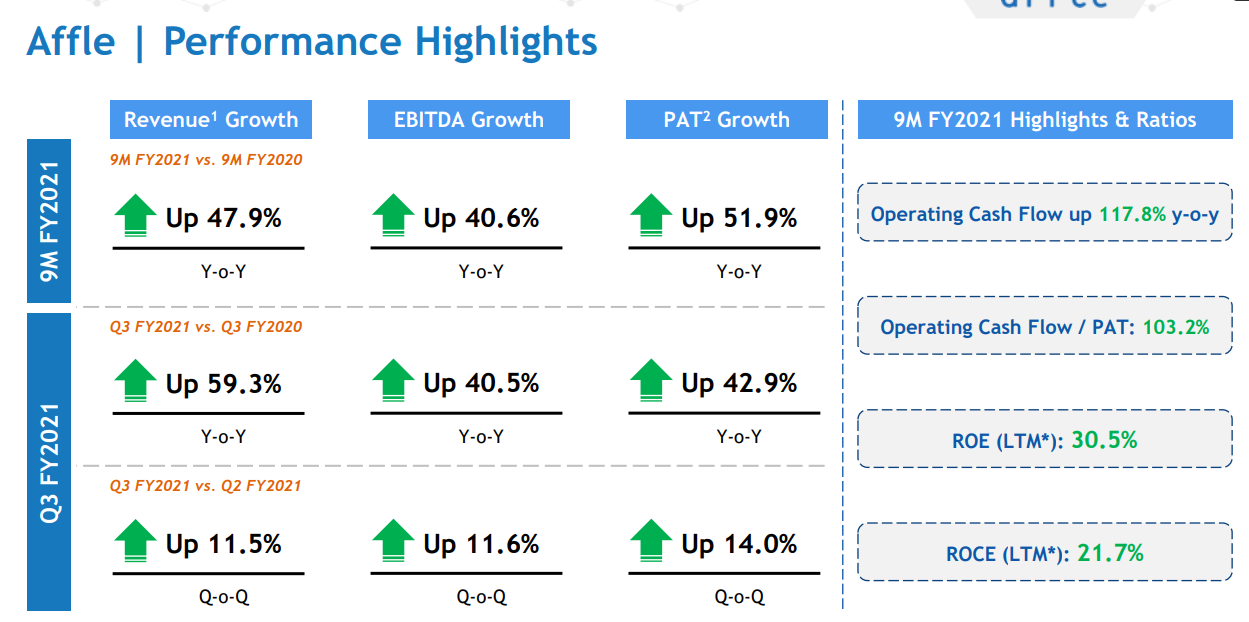

Also how conveniently they ignored the 60% YoY growth posted last qtr.

Also why would a company which has been continuously growing at 30%, backed by strong cashflows trade cheap?

I guess criticism is the best way to get famous on Twitter. Research a stock for 3 hrs and rant about it.

IMHO the price movement is certainly due to the factors that you have mentioned no doubt about that. I would like to add one more, there very less float available and retail investors have more money (disposable income , money that is otherwise spent , saved because working from home , no travel cost, no discretionary spending etc… ) Like to like example is Tesla .

I mean, DIIS and FIIS and Corporate investors they don’t transact much on day to day basis then come to the retail investors, who are always active. Happy to correct my understanding.

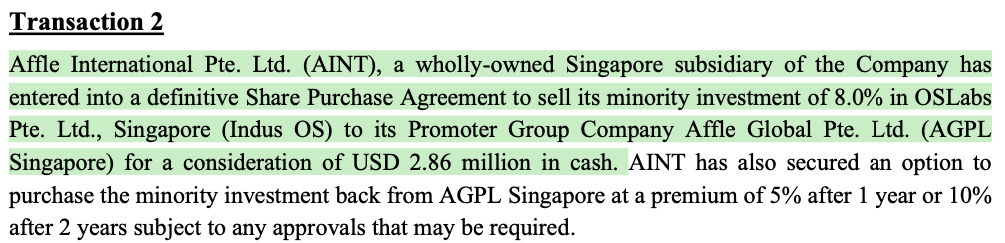

I think they have found a way to sell the stake to their promoter and international ops and increase cash in their India ops. Nothing much to read it but a way to handle tax/cash positions unless they state otherwise. However, these transactions should have been avoided since this transaction was touted as one of the highlight by the management and now it goes to the unlisted company.

Excellent temperament n conviction to stay invested among so much noise and adverse comments mostly from the guys in sector itself.superb returns from IPO at 745 in July 19 to nearly 4000. Kudos.

Does anyone know why they haven’t shared the basic financial data like revenue & PAT for Discover Tech Ltd. Generally this data is shared in the exchange filing. Or else we will have to wait for con call.

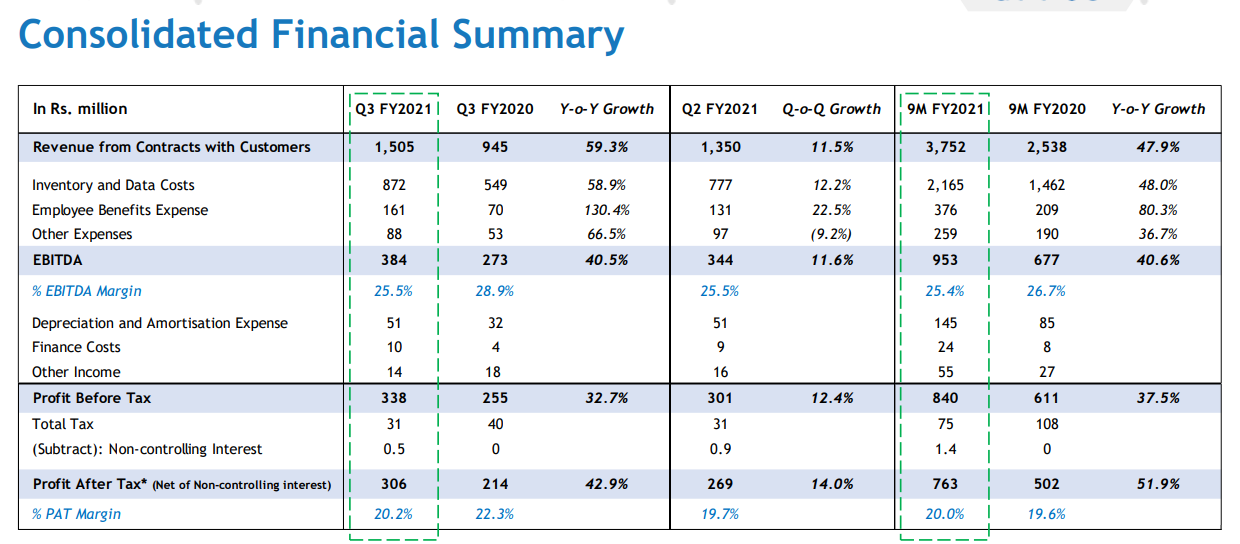

Good results. The inventory costs have also been managed very well. They are doing $ 20 Mn in Revenue per quarter. Need to see how Q1 pans out. The valuation is still 100x, but guess they are like D-Mart.

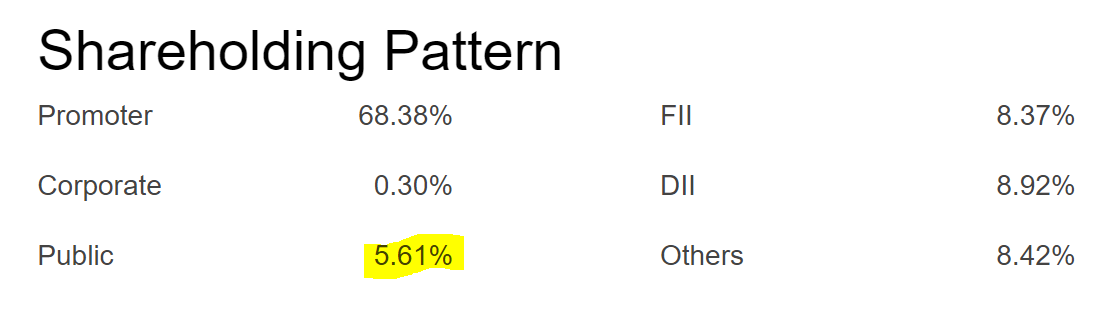

Dec quarter, promoters reduced the stake from 68.38% to 63.8%. Obviously that seems to be picked up by FIIs whilst DIIs consistently reduced their holding.

Today promoters sold another 3 lakh shares.

Any idea why would promoters consistently reducing their share holding? No doubt at these levels valuations are not cheap either. Any expert comments please ??

Airtel could become competition and has developed a beta for use on their own airtel apps very quickly. Could VPs discuss the actual moat for indian clients?

They listed the company at Rs. 700, and now Mr. Market is giving them 8x in a year and the PBT has not moved in a similar way. Any shareholder will think this is a good time to cash some part of the holdings.

The irony is the Director of Account Manager bought fresh shares for the first time at the Price Rs-5222 for 10 Lacks. It’s a market purchase. Not Sale.