Mobile ad spending and user engagement is skyrocketing:

As digital ad spends are growing, the next big thing is connected TV. https://www.beet.tv/2020/10/the-evolution-of-ctv-ad-measurement-inmobis-barthur.html

On separate news, Applovin will be going for IPO.

https://www.cnbc.com/2020/10/05/applovin-hires-morgan-stanley-to-lead-ipo.html

Vungle, Unity, IronSrc and Applovin are leading gaming networks and very active in South Asia.

Affle India the top performer in the AppsFlyer Performance Index across multiple categories

“Affle’s Mediasmart Platform launches its proprietary Audience Targeting and Household Sync

technology on Connected TV (CTV).”

https://www.bseindia.com/xml-data/corpfiling/AttachLive/90f1780e-cc60-4f47-829a-d198ac372379.pdf

MAX is a mediation network, and it helps publishers monetize better. Next step for Affle would be to build or buy a mediation network, to control monetization and publisher inventory.

1 Like

Q2 FY2021 Highlights (y-o-y):

- Revenue from Operations of Rs. 135.0 crores, an increase of 59.3% y-o-y

- EBITDA at Rs. 34.4 crores, an increase of 58.2% y-o-y

- PAT at Rs. 26.9 crores, an increase of 72.5% y-o-y

- PAT margin up by 1.4% to reach 19.7% from 18.3% in Q2 last year

H1 FY2021 Highlights (y-o-y):

- Revenue from operations of Rs. 224.7 crores, an increase of 41.1% y-o-y

- EBITDA at Rs. 56.9 crores, up by 40.7% y-o-y

- PAT at Rs. 45.7 crores, up by 58.6% y-o-y

4 Likes

very good results, op margins over last 3 qtrs are at 25% - was expecting some operating leverage to play out, nevertheless good results on expected lines of digital marketing push during this Qtr.

Would be interesting to understand organic vs inorganic numbers, didn’t find in presentation.

how are they keeping tax payout in single digit?

3 Likes

Fantastic nos. no doubt but some chinks that I could notice.

-

Operating leverage has stopped showing up as sales is moving in tandem with RM costs.

-

Nos. have been juiced up by lower other expense too.

Brokerages are moving up their targets but at 3500 it would be ~100x FY21 which will be extremely expensive IMO given that sales have got corona bump. One of the detailed report by Dolat capital to understand the biz model.

Disc. - Ended my 2nd innings here recently due to valuation. It remains on my watchlist though.

2 Likes

Dont disagree on valuations. But juiced up by lower operating expenses is a harsh statement A lot companies have cut down on other operating costs.

Very good results and the festival season still remains as October and November would have increases ad spends for Diwali/Navratri.

Also TradeDesk results for comparison.

My issue is around valuation and differentiation. Will need to wait and see on how this plays out.

2 Likes

A very good article on software monetization and how the Avergae Customer Value expands. Please read.

Pubmatic for $ 1bn IPO with ~ $ 120 Mn Revenue.

2 Likes

In the last con-call this question was asked and answered by management. If they question could have been rephrased, “what is the % of supply and revenue from direct SDK supply versus offline API supply via third party networks ?” would have given more clarity.

“Mythili Balakrishnan: Congratulations on a good set of numbers. I had a couple of questions which I

wanted to understand in terms of our business model itself. How much of our

supply would be from a propriety set of apps that we work with on a sole basis

or how much would it be from the broader general inventory that is available

across Ad exchanges.”

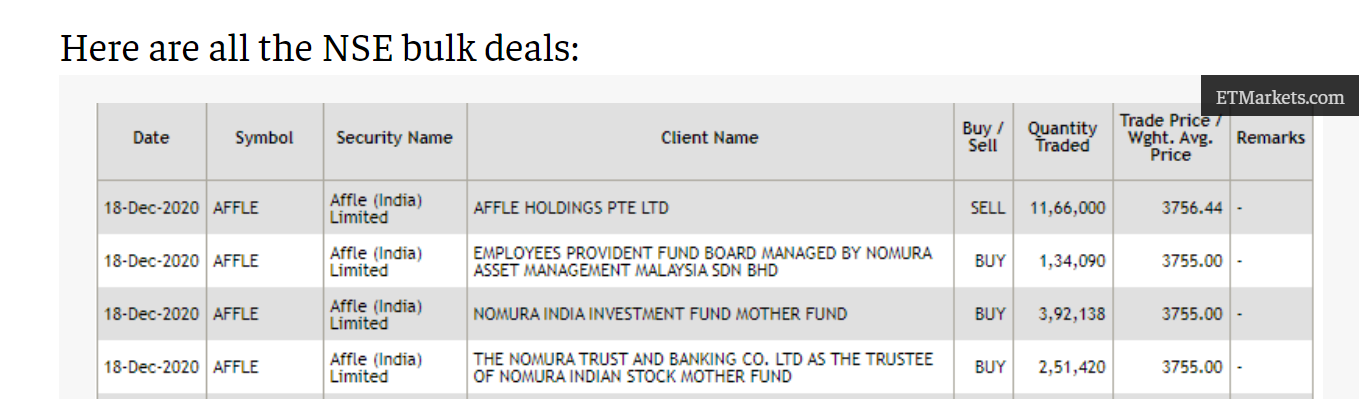

Disposal of 1,166,000 equity shares worth Rs 43800.09 lacs by promoter

That is almost 10% of promoter holding, not sure if they indicated any plans in recent past.

Was invested, exited after last qtr results - seeing major part of profit growth coming from tax savings, on watchlist though, like space but not comfortable with current valuations

1 Like

Nippon india sold i think most of their stake of 3.12%

I tried to lookup who bought them , is the above transaction is related to this ? Promoters tried to a bulk deal ?

1 Like

One reason I can think of is the bearish trend of Tanla platforms. At this point among the small-cap AI companies, Affle looks promising. Affle has given impressive results for the last few quarters. However, one need not trust the brokerage recommendations all the time.

1 Like

Even promoters have sold good chunk of >4.5% stake last week along with Nippon which is invested since IPO.

Being from IT background and a close friend of ex tyroo/SGC cxo who is running similar business today on his /her own just want to add few points:

- Most of IT co including tyroo employees have mac.Even the startup. Very few like IBM GBS and pure service based co are using windows laptop. On avg it would certainly cost > 50k per unit even for windows. I know the costing since I sign it approval for my org.The costing look ok if they dont have own servers and half of employees dont have laptops .

- Smile group/Tyroo , having similar business has several successful exit to PEs without ipo.

- SMS platform is not IP in today’s day. Its now commodity .

1 Like

Affle India: Expect strong trends to continue in 2021, says CMD Anuj Khanna Sohum

1 Like

Looks like this twitter thread is about Affle.

1 Like