As per recent disclosures, Aeroflex is largely funding working capital through internal accruals and some short-term borrowings, which is normal as the business is scaling exports. Also, the company is still net debt light, so interest cost risk looks manageable for now.

The real risk to track is whether receivable days increase sharply or operating cash flow turns negative for a long period. So far WC increase looks more growth related than stress related, but it is definitely a monitorable point.

Aeroflex Enterprises is a holding company with diversified investments across multiple businesses and startups, and it holds roughly two-thirds (~65–67%) stake in Aeroflex Industries, whose market cap is around ₹5300 crore, implying a stake value of approximately ₹3,500 crore. In addition to this listed stake, the company has exposure to several other subsidiaries, sectors, and startup investments, along with an estimated cash position of about ₹400 crore. Despite these underlying assets, Aeroflex Enterprises itself is currently trading at a market capitalization of roughly 1,200 crore, highlighting a significant gap between its market value and the value of its holdings.

Welcome to the world of “HoldCo Discount”.

Its is a prevalent feature of all such holding companies.

The reason I understand for such discounts are:

Lack of Liquidity & control : Holding company seldom sell their investments. Thus it makes difficult for shareholders to unlock full realization.

Complexity of valuing underlying asset: Complex reporting structures and multiple layers of subsidiaries make it difficult for investors to understand the business, often resulting in a discount.

Apart from KAMA Holding’s SRF investment there are many more examples like: Tata Investment Corporation Limited (TICL): often trades at a significant discount to the market value of its holdings, which include major Tata group companies like TCS and Tata Motors. Bajaj Holdings & Investment Limited: A well-known Indian holding company that often trades at a high discount compared to its investments. Berkshire Hathaway: A global example where the company’s diverse portfolio of businesses and investments might be valued differently by the market than if they were separate entities. Generally it trades in the range of 10-20% discount.

You can try reading more about HOLDIN COMPANY DISCOUNTS & CONGLOMERATE DISOUNTS, to understand the concept indepth.

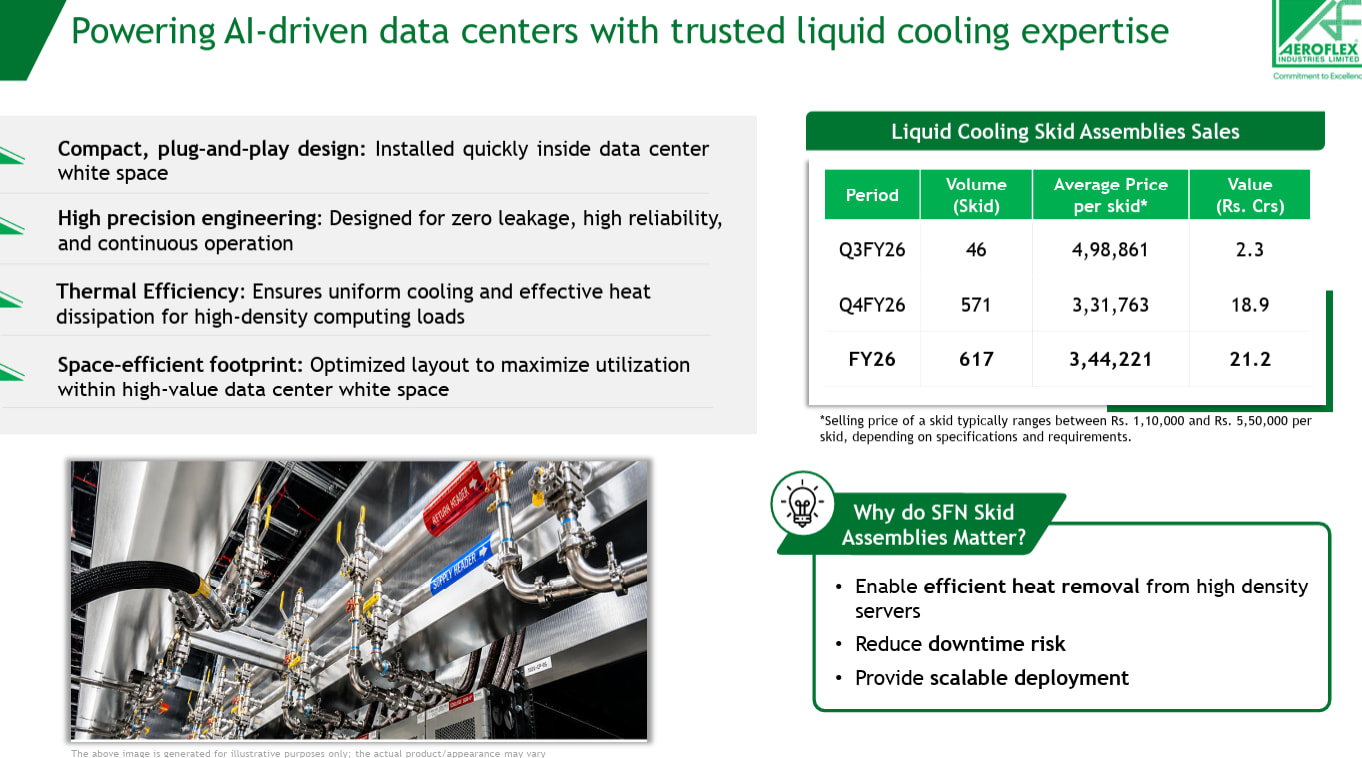

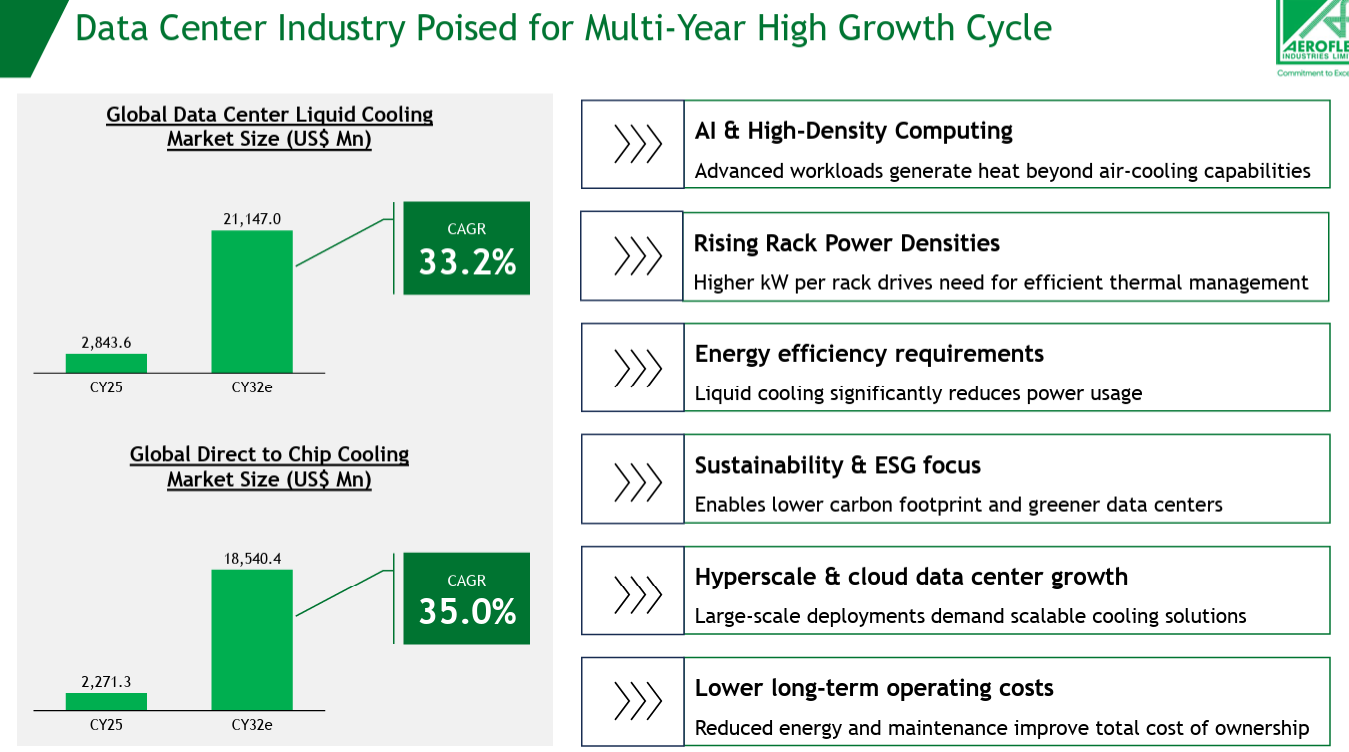

Management is quietly positioning it as a key enabler of the AI/data center cooling ecosystem.

expects 30-35% growth in FY27, scaling liquid cooling skid capacity from 2,000 to 15,000 units, backed by strong orders and a debt-free balance sheet.

If AI-driven data center capex continues globally this could evolve into a high-margin thermal management play but most of us know it and stock already up 2x from January lows and trading at ~122x earnings, execution has to be near perfect.

Hence I believe getting exposure via Aeroflex Enterprises is a better risk to reward play. Take a look at this (it is based on the calculations shared by @phreakv6here)

The auditor for Aeroflex has some history of pump stocks auditor. Charging only 6.5 lakhs for audit for FY 25-26. The break up also looks odd - almost half and half for statutory and tax audit. A flag worth noticing?

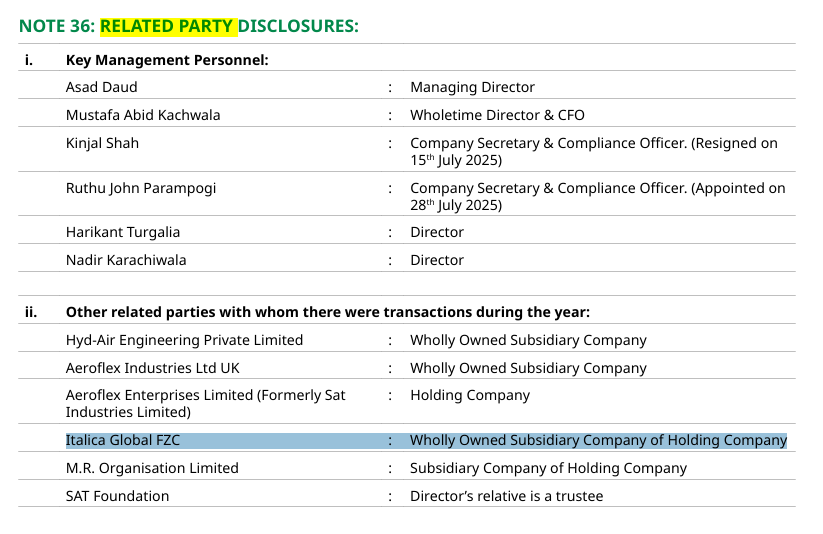

𝟭. The MD’s letter says Aeroflex is growing in the US, the Middle East and other markets. The Middle East part is hidden in the small print of Note 36.

𝟮. Aeroflex sold goods worth 22.56 crore in FY26 to a UAE company called Italica Global FZC. Last year that number was 2.84 crore. Sales grew 8 times in one year. A new service fee of 0.36 crore also showed up.

𝟯. Italica is not a stranger. The same family that owns 59.84 percent of Aeroflex also owns 100 percent of Italica. Italica itself owns another 5.63 percent of Aeroflex. The family’s real control is 65.5 percent, not 60 percent.

𝟰. Aeroflex spends its own money to build the factory and make the product. When Italica then resells the same goods to the actual Middle East buyer, the extra profit on that resale stays with the family, not with Aeroflex shareholders.

𝟱. Nothing illegal here. The real test is the next shareholders’ meeting. If the family asks permission to do 30 crore or less of such sales next year, the relationship is settled. If they ask for 60 crore or more, this is going to grow much further.

Wholly Owned subsidiary company of the Holding company. The holding company here is Aeroflex Enterprises Ltd, formerly SAT Industries Ltd, so it is not wholly owned subsidiary of Aeroflex Industries Ltd. It is a subsidiary of the holding company.