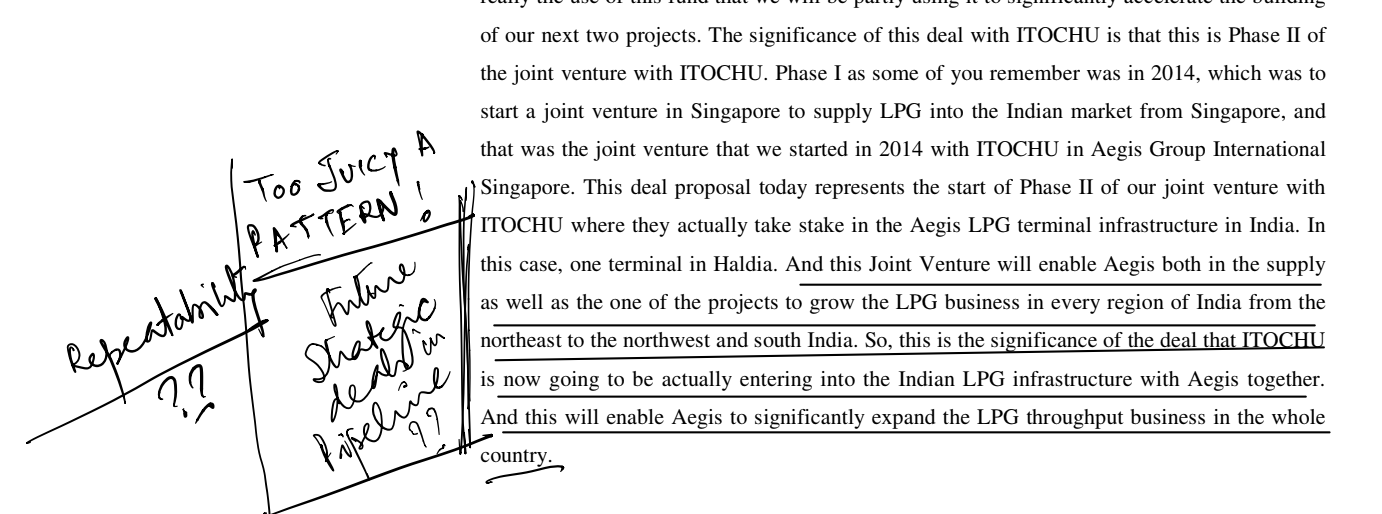

Can some guys help out in plotting locating bottling plant capacity along Kandla-Gorakhpur Pipeline - to establish firm demand?

Disclosure: Invested.

Disclosure: Invested.

Now hopefully some interest is stoked !!

So here is my attempt to rope in more of us in helping us speed up the investigation/collate data points - completely voluntary - only for those who have the bandwidth, the interest is sufficiently stoked, and woould like to help us do a much better job

Attaching some documents of pipeline & BP map along with link to India Ratings report of IHB. Looks like all the IOCL BPs on the pipeline route have a capacity of 120 TMT except Kanpur with 180 TMT. HPCL - Unnao and Gorakhpur are at 60 TMT.

From one of the docs - The LPG pipeline will be directly linked with 22 LPG bottling plants – of which three will be in Gujarat, six in Madhya Pradesh and 13 in Uttar Pradesh for product supply. This single pipeline will transport 8.5 million tpa of LPG, which is about 25 percent of India’s total LPG demand.

The pipeline will also supply bulk LPG through road-bridging to nine more LPG bottling plants in Uttar Pradesh, located at Shahjahanpur, Farrukhabad, Kashipur, Lakhimpur Kheri, Saleempur, Bareilly, Sultanpur and two plants at Gonda.

KGPL.pdf (585.2 KB) Kandala-Gorakhpur.pdf (778.8 KB) LPG SCM.pdf (2.3 MB)

@Donald - sorry Dada still catching up with you all on Aegis. I am done with ARs and now will be moving to concall transcripts.

I am listing down the items that you wanted help with to dig further:

If there are any other items that I may have missed please add. So before I start my day I will check open items here to plan my day’s work on Aegis.

Thanks @ashkrithik that was quick, @iivans, and @rupaniamit.

So 8.5 MTPA it is. Guess this will get divided up between Mundra and Kandla.

@desaidhwanil - if Kandla provides much better evacuation costs, then there is a case for higher allocation to Kandla, right? But of course

a) there could be pre-commitments for Mundra as well

b) and Aegis will need further investments to augment storage/throughput (assuming there is space)

I am sure this helps the Aegis veterans Dhwanil, Ankit and Aman with more time to spend on structuring their thoughts and the presentation. It also helps others like me trying to catch up fast

@rupaniamit - as of now yes, this was the small list. If we need help with more data points/cross-checks we will update here. Hey, you missed listing the 6 or 7 factors (we need to dig up) to throughput performance improvement - indicated by Mgmt to have been covered in earlier Concalls. Fully expecting more to this than Ivan’s listing 3 ways? And in my book, getting to the bottom of this is KEY to understanding Aegis/and its ability to keep increasing distance with peers - and thus one of the primary indicators for slotting Aegis Mgmt in a much higher slot (given say all other things being equal and passing our thresholds requirement for investment (for competing investment choices)). It indicates a Mgmt, who are always on top of Execution.

Great to see the energy guys. Love it!

I had a basic doubt here:

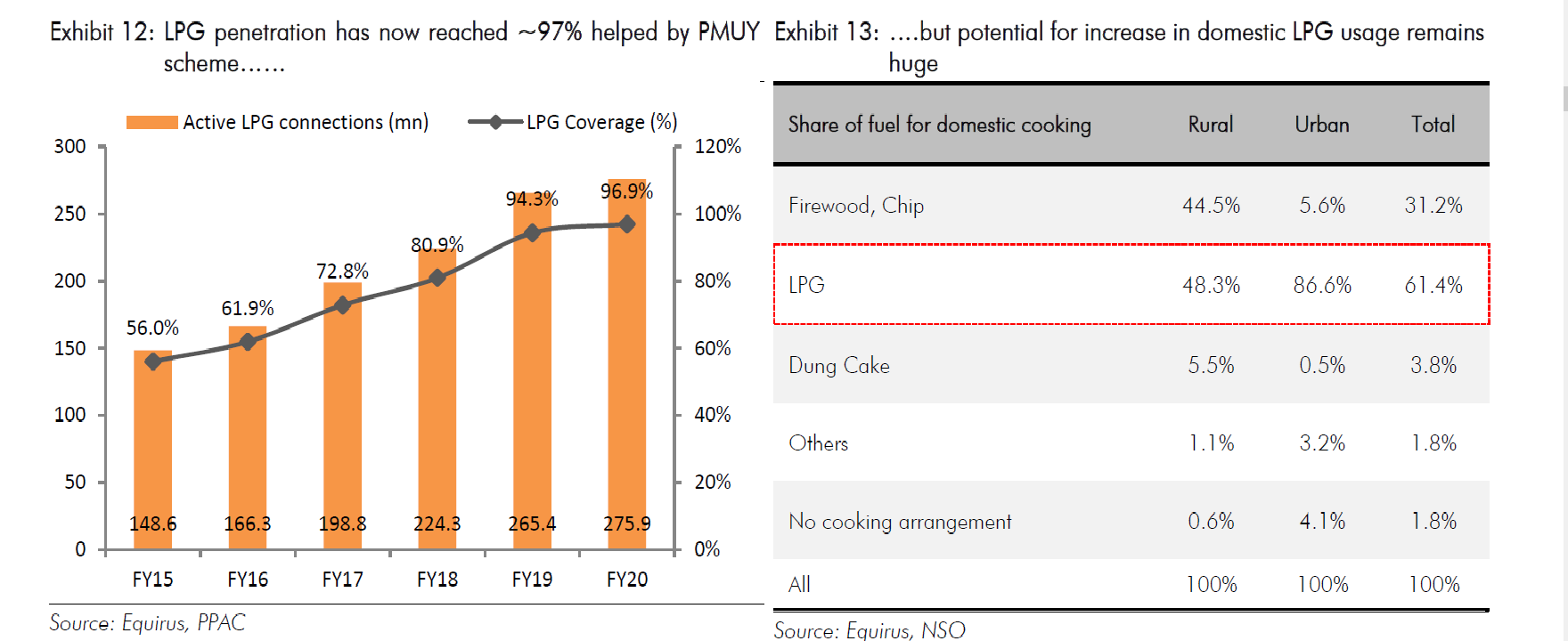

As I am working on LPG distribution side for Aegis - some interesting data point from PPAC which gives some idea as to how DBT transformed the LPG landscape. It is spellbinding in size and scale of impact it has had .

LPG_PPAC_Data.pdf (210.6 KB)

A Point to ponder for Aegis- a large part of LPG penetration is already achieved where penetration moved up from 56% to 98%. This led to substantial growth in LPG demand and hence LPG import too,…so with this level of penetration why would the demand not mellow down? - Of course now I am wearing the hat of a critic ![]()

Some brief notes on the LPG capacities:

| Terminal | Location | Capacity | |

|---|---|---|---|

| Aegis | Mumbai | 1.5 | |

| Aegis | Pipavav | 1.6 | |

| Aegis | Haldia | 2.5 | |

| SHV | Porbandar | 0.3 | |

| IPPL | Ennore | 1.7 | |

| SHV | Tuticorin | 0.2 | |

| JNPT | Mumbai | 0.8 | |

| Total | Mangalore | 0.6 | |

| MLIF | Mangalore | 1.8 | |

| IPPL | Haldia | 2 | |

| IOC | Kandla | 0.6 | |

| SALPG | Vizag | 1.8 | |

| Total - FY21E | 15.4 | ||

| IOC | Kochi | 1.5 | Being constructed |

| IOC | Paradeep | 1.5 | Being constructed |

| BPCL | Haldia | 1 | Being constructed |

| IOC | Kandla | 1.9 | Addition expected |

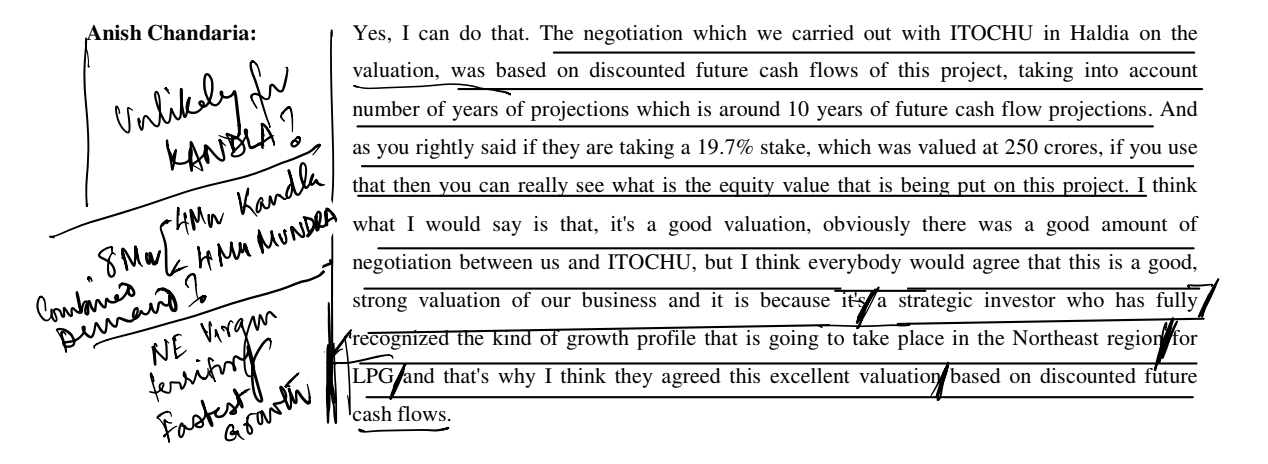

| Adani | Mundra | 3.6 | In progress |

| Aegis | Kandla | 4 | In progress |

| Total - FY25E | 28.9 |

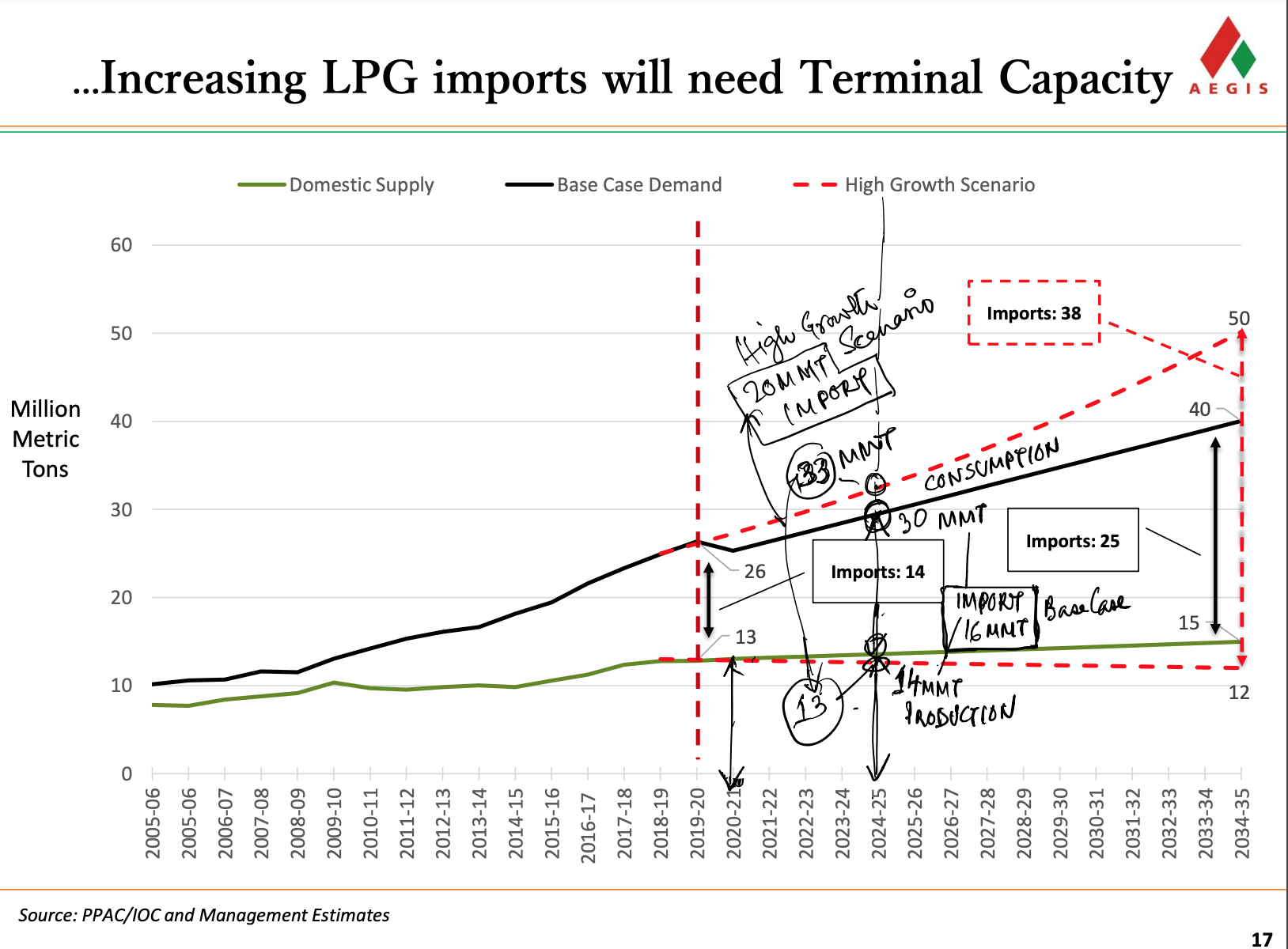

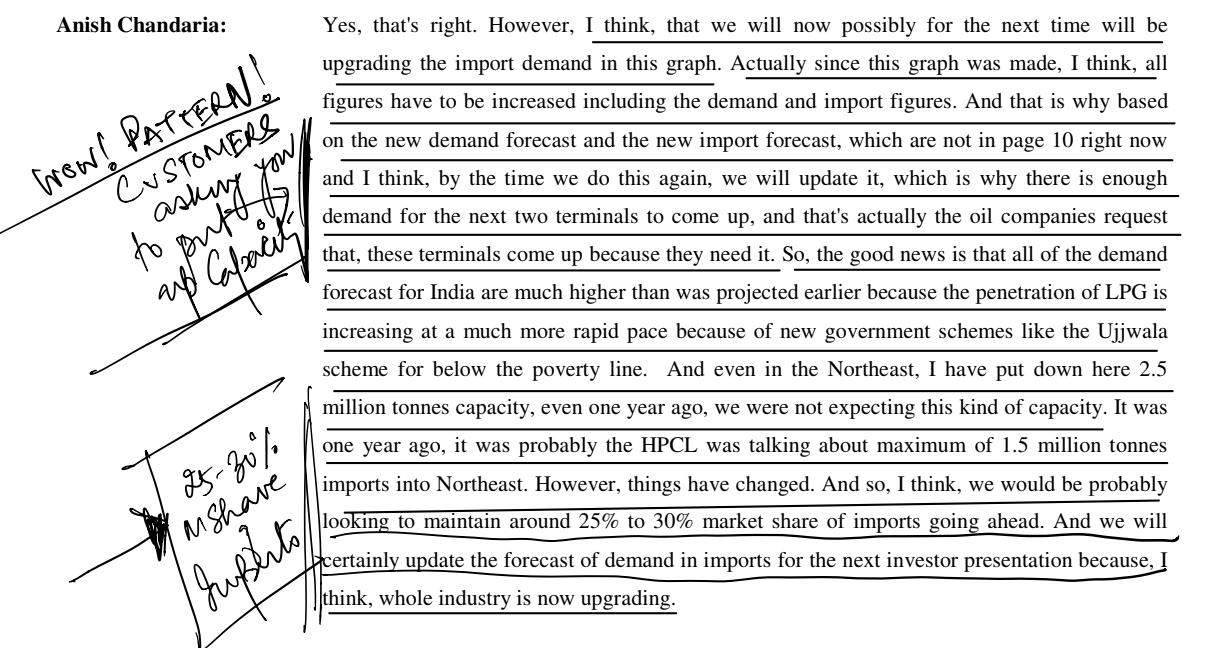

Even excluding IOC Kandla and Adani Dhamra, capacities coming on stream is 27 MTPA. While, projected import demand is only 20 MTPA in FY23 and 25 MTPA in FY30.

Something to ponder is how the market share dynamics will play out if IOC goes ahead with its Kandla expansion and Mundra gets connected to the KGPL pipeline and the 50% higher cost of having only road evacuation option at Mundra goes away. Kandla isn’t a deepwater port while Mundra is a deep water port which gives them an advantage of ~Rs. 800/MT (as quoted in their presentation).

Who are the players Aegis is likely to take market share away from roughly 5 years from now?

The mgmt had said they have plans to install one new terminal in South. Is there enough import demand to accommodate that Southern terminal?

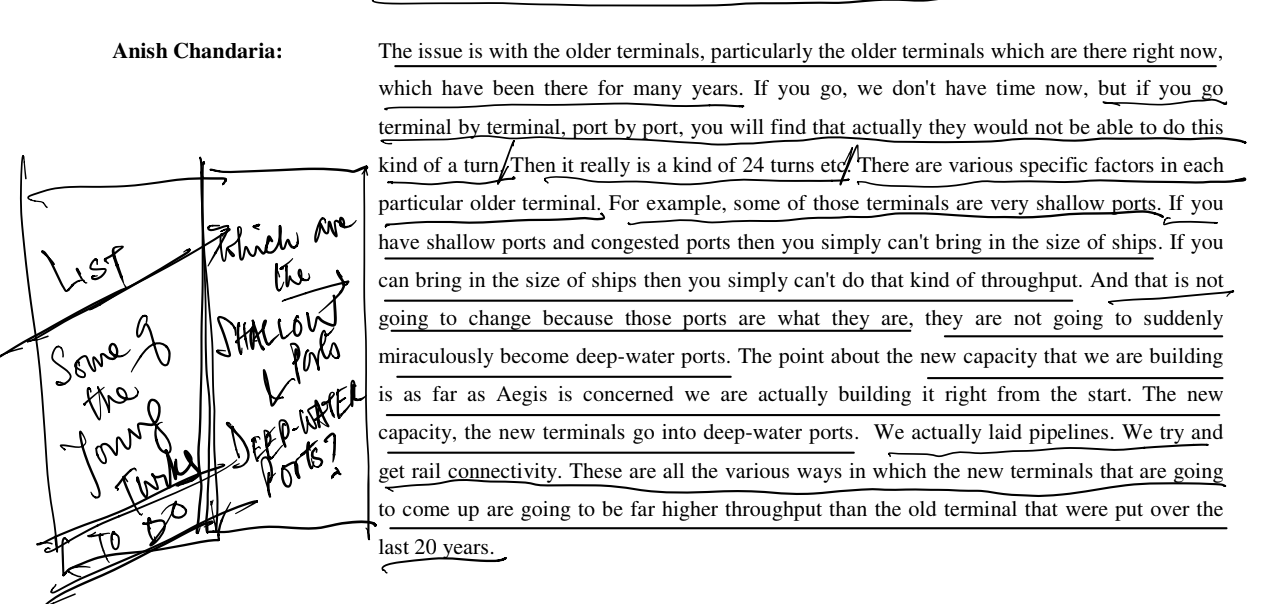

What is the disadvantage that both the big terminals of Aegis (Kandla & Haldia) aren’t deepwater ports that can accommodate VLGCs while both the proposed terminals of Adani (Mundra & Dhamra) are deepwater ports? Read somewhere that the company is trying to link Pipavav (deepwater port) terminal to the KGPL pipeline - does that mitigate that disadvantage to an extent?

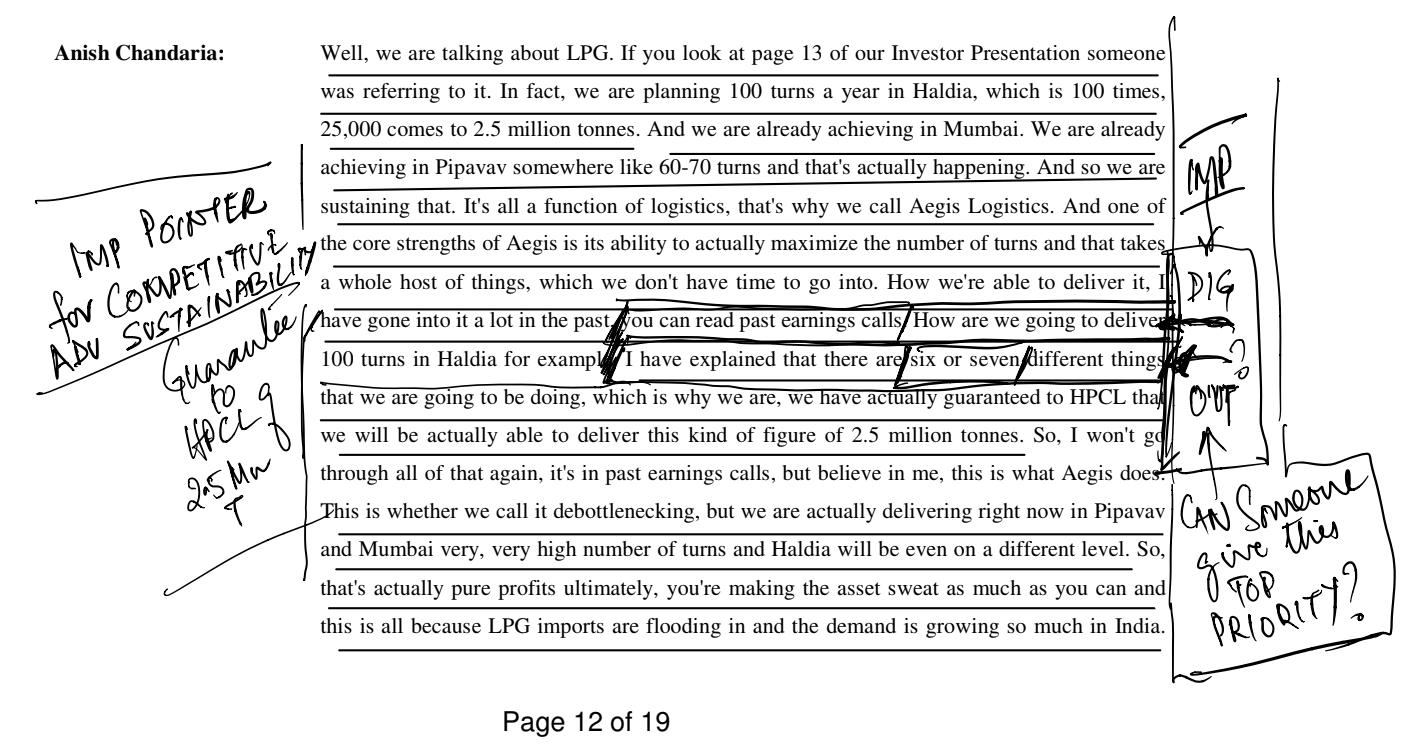

Snippets explaining how they achieve high throughputs:

Q3 FY 16 call

Q1 FY 17 call

Q3 FY 17 call

Disclosure: Invested

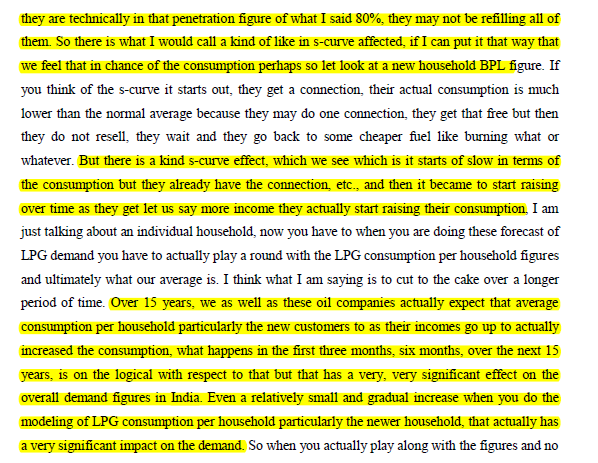

Although, government claims that LPG penetration levels have increase to 97% of the domestic households, there is some divergent data from NSO which claims that only 61.4% of fuel used for domestic cooking is LPG.

Furthermore, refill rates for economically weaker sections remains very low. The same is expected to increase over the years.

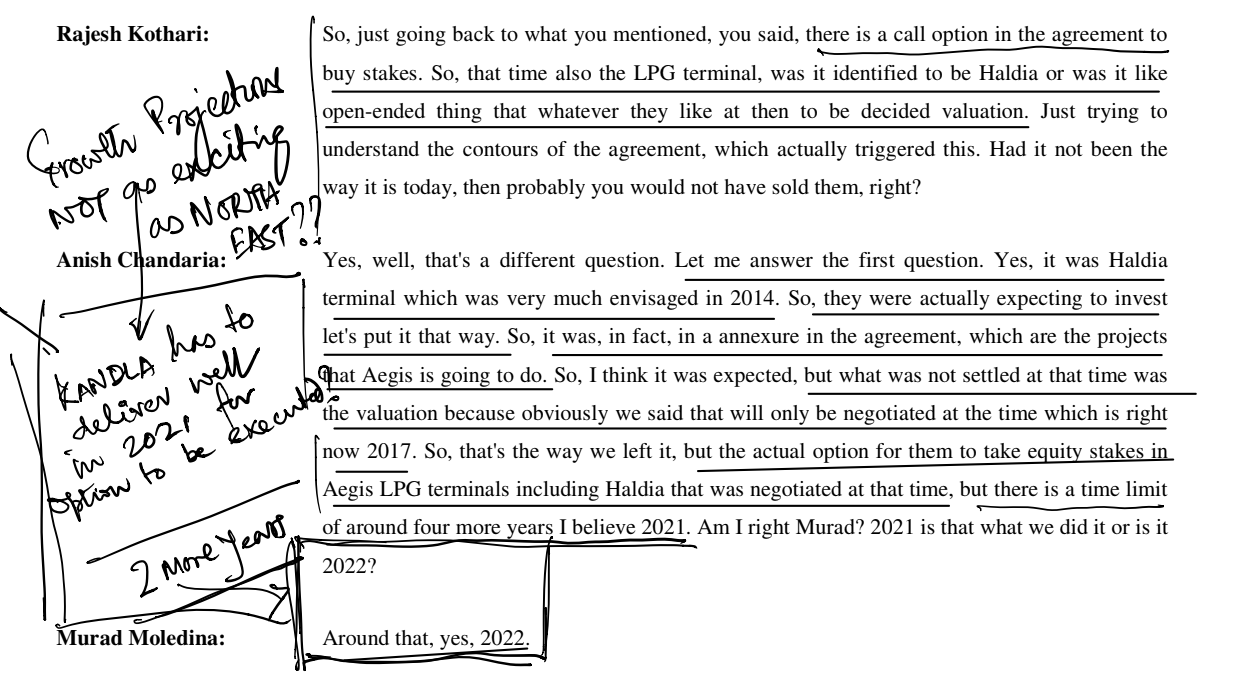

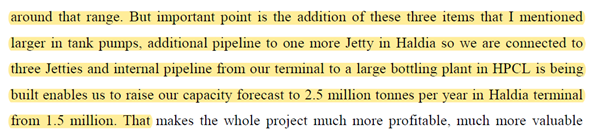

Coming to the LPG growth part, I think company along with other research reports are expecting 5 - 7% growth rate for LPG consumption in India with imported LPG growth to be higher if no significant refinery addition happens in India (need to verify that). Furthermore, the utilisation of Kandla 4 million tonne capacity will happen over the next 3 - 5 years from FY22. The market share gains will be from capturing new imported volumes over the next 3 - 5 years by mainly Kandla terminal and some from Haldia (1 million tonne is still left to be utilized) and Pipavav (railway gantry adding 0.3 - 0.5 million tonne) & Mumbai (Uran - Chakan pipeline adding 0.3 - 0.5 million tonne).

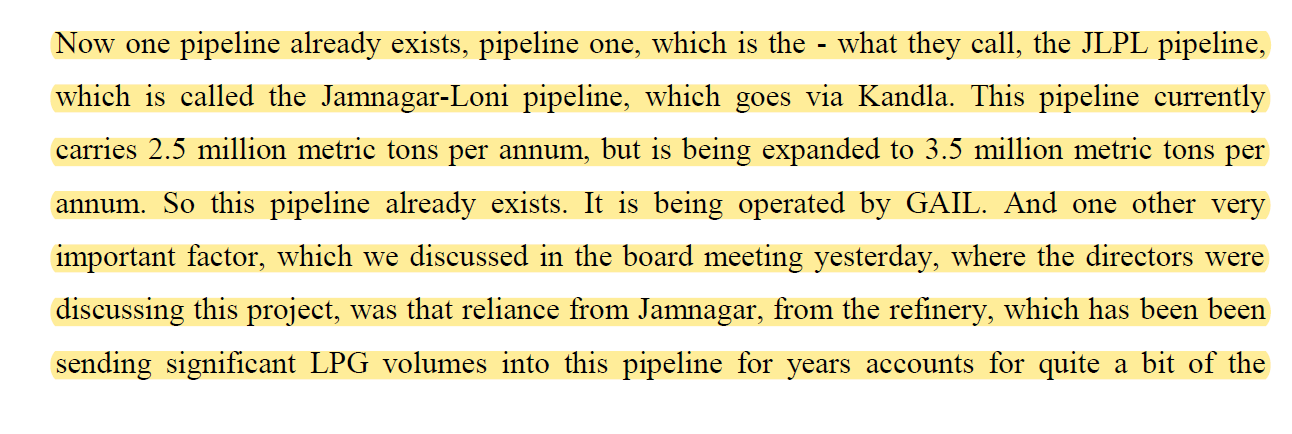

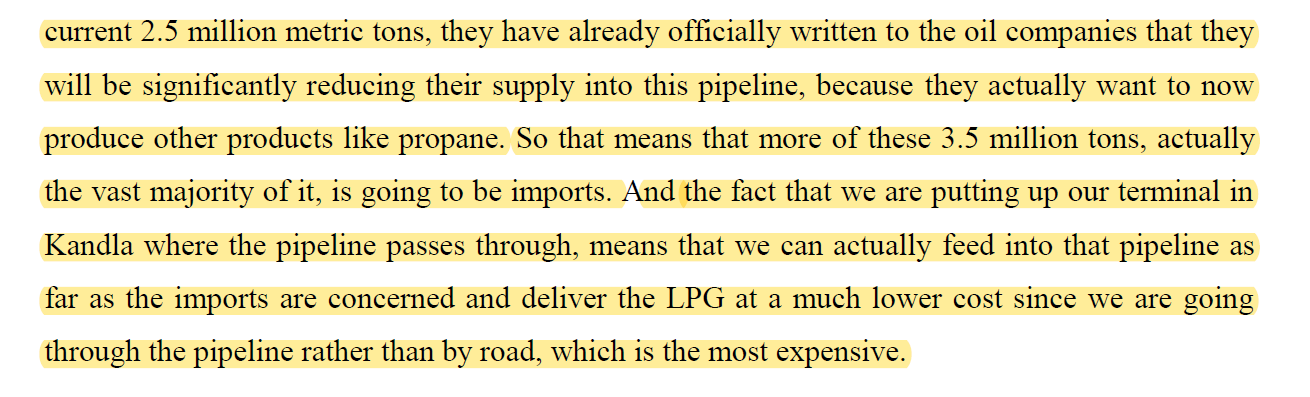

The concall transcript of Q3FY19 when they declared Kandla LPG project clears lot of doubt that we have regarding such huge terminal being put in Kandla. Furthermore, 2.5 million capacity of RIL’s Jamanagar refinery will stop production of LPG and shift to propane. Q3FY19 Concall transcript.pdf (183.2 KB)

@desaidhwanil

Something wrong with the abridged version you attached. LPG data points were missing. Re-attaching another version. Very interesting to see PMUY impact.

LPG_PPAC_Abridged_Data_Oct2020.pdf (669.4 KB)

The obvious questions remain on the bullishness of LPG longer-term import projections overall, and Aegis aggressiveness - the new South Terminal in particular implies their sanguineness about the need for more Terminal Capacity. Need better answers.

| Total - FY21E | 15.4 | ||

|---|---|---|---|

| IOC | Kochi | 1.5 | Being constructed |

| IOC | Paradeep | 1.5 | Being constructed |

| BPCL | Haldia | 1 | Being constructed |

| IOC | Kandla | 1.9 | Addition expected |

| Adani | Mundra | 3.6 | In progress |

| Aegis | Kandla | 4 | In progress |

| Total - FY25E | 28.9 |

If we were to take this slide from Aegis, Domestic Production being ~13-14 MMT today, it is hardly inching upto 14-15 MMT in 2025 in 4-5 years.Thats like only about 1 MMT additional Production in next 4 years. Want to check this data?

On the other hand, Import projections are also shown to be going up by only 4-5 MMT by 2025 even in the high-growth scenario (which itself is debatable?). But just Mundra (Adani) and Kandla (Aegis) Terminals are best-placed/supposed to achieve additional throughputs of ~4 MMT each (in 3-4 years) in order to meet 8.5 MMT Kandla-Gorakhpur Pipeline requirements?

@desaidhwanil - love to hear you explain the apparent anamolies we see

Couple of ways Aegis thinks about it, as I wrestled with the data above

a) Capacity is one thing - getting to peak throughput (planned) is another (like Aegis capacity currently is 5 Mn but achieved throughput in FY20 is ~3Mn)

b) Some of the capacities (existing & being put up) will remain much underutilised - those that fall way short of delivered-LPG-cost benchmarks set by Aegis

I will go on to check Aegis slide data on Production/Consumption (Import) projections with others available, next to see if there are any major differences/degrees of bullishness from different parties. Any PPAC projections anyone is aware of?

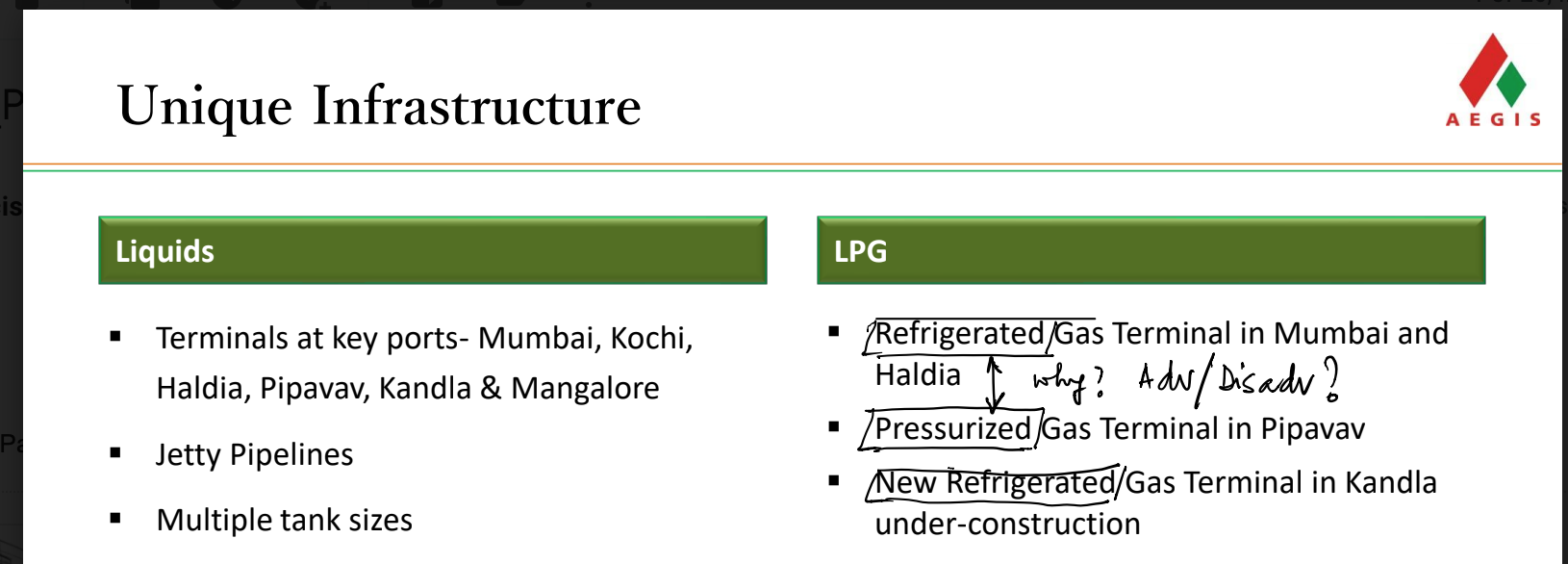

Also if anyone can answer refrigerated vs Pressurised Gas Terminals

There are few things we have to consider while evaluating the projected utilization and data points.

Important infrastructure like terminal, pipeline etc have life span of few decades or more (typically anywhere from 30-50 years). Considering that cost of duplicating the infrastructure in future is going to be far higher, business managers do create capacity that caters to the long term growth need of the underlying commodity (be it LPG/LNG/other petroleum products). Typically the capacity is planned with 65-70% base capacity utilization and the rest of the capacity is extra capacity that they build.

Second point to consider, and in my experience is more subtle but very important one, is in an energy starved country, creating infrastructure always precedes demand generation. One can take any example be it gas pipelines, LNG terminals or CGD networks. A player puts up an infrastructure based on it’s assessment of demand but almost always demand surprises on the upside over time. Entire gas grid in Gujarat was created based on this principle, it was envisaged at the time of setting up Gujarat was grid was that the state will consume 4-5 MMSCMD over time and today they transport 43 MMSCMD and planning to add more capacity. Same story in LNG terminals and CGD network. Central point here is that the latent demand for a commodity comes to fore only after infrastructure is available and commodity reaches to end consumer. Thus from Aegis perspective, as long as pipeline and distribution network gets created, demand will follow is my personal view. Of course we investors always think in terms of numbers in next 3-4 years, if you look at the PNGRB authorization document that @ashkrithik shared, they scale up to 5 MMT is there in next 3-4 years out of total 8 MT available between Mundra and Kandla - rest 3 can be through other pipeline and road network etc.

On the larger point on how to justify import terminal capacity based on import projections, my view is that company has to make it’s own assessment and take view because the data available in public domain by various company/govt agencies - has huge variance in terms of projection for domestic production ramp up etc and data points are collated/made to justify their own objectives for which the data is collected. Hence, to infer that whether import need will be there or not purely based on data available may not be accurate. Of course, this sound an evasive argument but in my experience of consulting I have seen that we used to pull up data from appropriate sources based on what we wanted to prove for/against capacity expansion.

I would again urge you Donald to go through Q3FY19 concall. I think concalls are treasure trove in case of better understanding of Aegis.

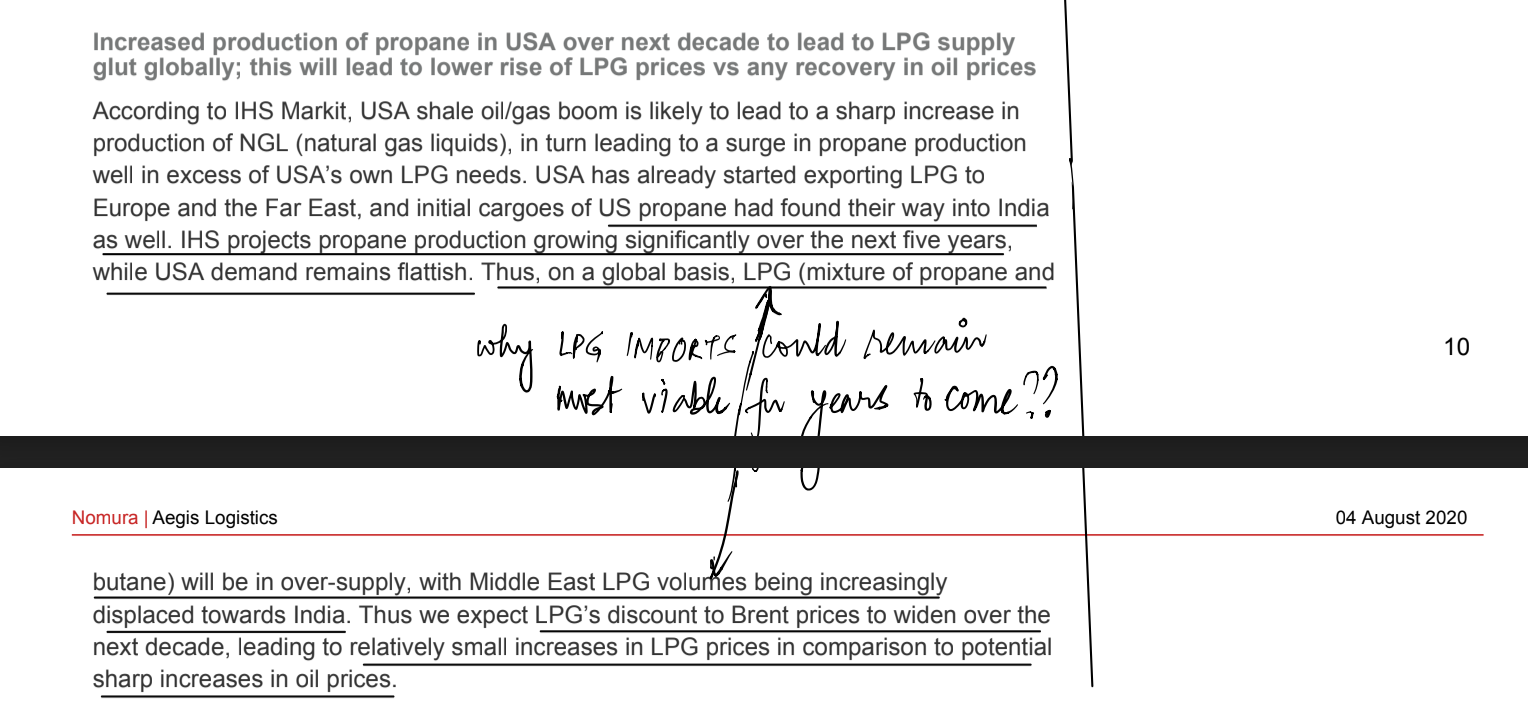

Important point to note is that domestic LPG capacities of Reliance and even Essar (as said in the Kotak conference today) are getting discontinued as LPG prices have fallen from USD 1200 to around USD 400 as US has become LPG surplus. In fact, Reliance had decided to move to propane in FY19 itself. Also, please note that Kandla Gorakhpur pipeline will only come after 3 - 4 years, might infact get delayed (BTW, Uran Chakan pipeline got delayed by 4 years due to some rehabilitation issue of a village). Jamnagar Loni pipeline (3.5 million tonne) which is already connected to Kandla will play a role in evacuation. Furthermore, Mundra - Kandla pipeline is being constructed by Adani themselves and will further cost Rs.350 crore (650 crore cost plus 350 crore pipeline cost). Snippet from Q3FY19 concall:

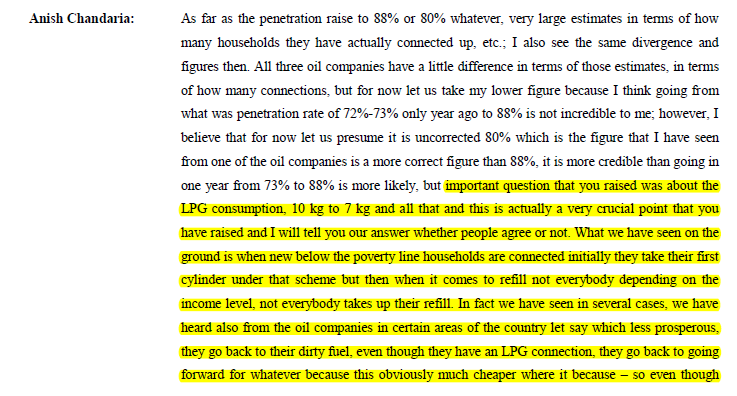

Another point on the penetration part of LPG is that 97% penetration is achieved by accounting that first cylinder is given free to all households under the UJWALA scheme. However, subsequent off take from the new connections is a big issue. In the conference today, management highlighted that in many of the new connections, average consumption of cylinders is just 1.3 per year as compared to 7 for matured connections in urban areas. Furthermore, these 7 cylinder consumption for matured connections can also move to 12 per annum.

Coming to IOC expansion at Kandla, the earlier terminal is almost a 30 year old and management said that work for expansion is yet to start. However, it will come in over the next few year for sure. BPCL Haldia terminal is becoming operational and in Haldia, HPCL is the anchor customer. Management expects volume at Haldia terminal to remain flat at 1.5 million tonne during FY22 as BPCL volumes shift from Aegis terminal to their own terminal. Kandla 4 million tonne utilisation will happen over the next 4 - 5 year atleast. Aegis management will also announce one more terminal in south pretty soon.

Yes, Government agencies might try to use/put up data to their advantage - especially the Ministry - like say for PMUY benefits. But is there any benefit any government agency derives by forecasting huge gaps between demand and supply (necessitating more imports) - other than to justify more local production?

The more viable arguments could be that increasingly domestic LPG production costs will not match up to international (also glut situation) and therefore it will always be more viable to import?

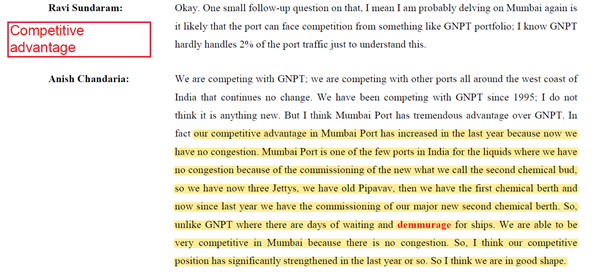

In reference to Aegis management talk on problem of congestion at ports, faster turn around time, data from ARs of ministry of shipping shows improving operating efficiencies in 13 major ports of India during last three years. ( There are few more data points available in ARs which may not be relevant)

| AVG TURN AROUND TIME/HRS | |||

|---|---|---|---|

| PORT | 2018-19 | 2017-18 | 2016-17 |

| KOLKATA | 92.08 | 91.2 | 113.52 |

| HALDIA | 72.96 | 90.24 | 82.8 |

| PARADIP | 60.35 | 79.48 | 119.76 |

| VISAKAPATNAM | 60.22 | 61.99 | 90 |

| CHENNAI | 47.41 | 52.99 | 60.24 |

| V.O CHIDAMBARANAR | 47.04 | 64.56 | 105.6 |

| COCHIN | 35.21 | 37.02 | 47.76 |

| NEW MANGALORE | 46.21 | 49 | 56.4 |

| MORMUGAO | 63.06 | 63.18 | 99.6 |

| JAWAHARLA NEHRU | 51.22 | 53.76 | 48.48 |

| MUMBAI | 60.42 | 65.57 | 78.84 |

| KANDLA(DEENDAYAL) | 72.24 | 60.24 | 105.6 |

| KAMARAJAR(ENNORE) | 47.27 | 52.86 | 64.8 |

| TOTAL | 59.51 | 64.43 | 82.56 |

| avg output per ship berth day(in Tonnes) | |||

|---|---|---|---|

| PORT | 2018-19 | 2017-18 | 2016-17 |

| KOLKATA | 4408 | 4132 | 4204 |

| HALDIA | 9593 | 8343 | 7491 |

| PARADIP | 26197 | 24810 | 23727 |

| VISAKAPATNAM | 13790 | 13528 | 13068 |

| CHENNAI | 17288 | 16014 | 15888 |

| V.O CHIDAMBARANAR | 15353 | 11961 | 10456 |

| COCHIN | 22839 | 20880 | 17450 |

| NEW MANGALORE | 18126 | 16378 | 17094 |

| MORMUGAO | 12163 | 14525 | 13461 |

| JAWAHARLA NEHRU | 26498 | 23290 | 23316 |

| MUMBAI | 10409 | 9043 | 8414 |

| KANDLA(DEENDAYAL) | 17363 | 18531 | 18464 |

| KAMARAJAR(ENNORE) | 24158 | 24590 | 22916 |

| TOTAL | 16541 | 15333 | 14583 |

Some clues about LPG Imports viability, here

US exported first LPG cargoes to India in 2019 | IHS Markit,

and here

@ashkrithik in Q3’19 concall, management mentions that Kandla terminal can cater to VLGCs.

Below snapshots provide some understanding towards consumption growth of LPG in India, in-line with what @ankitgupta pointed above from today’s management’s e-meet