ABSL AMC is the only non-bank backed AMC in the Top 5 Mutual Fund houses in India

It has to be on top of the game when it comes to sales growth as they don’t have the privilege of taking low hanging fruits.

Snapshot of 5 year performance

Main areas of focus

-

Maintaining strong relationships with its MFDs

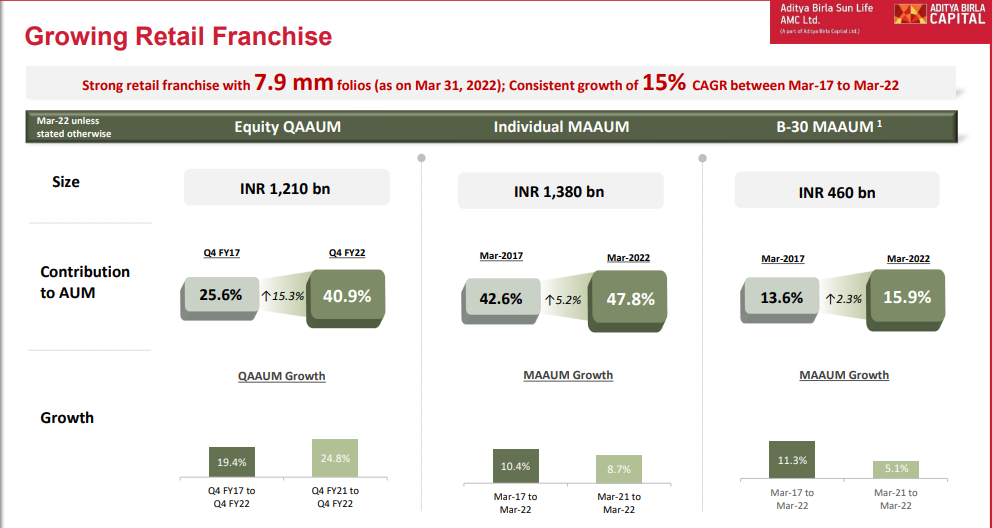

They mentioned during the concall that the sharing proposition with distributor remains at 60% which I think must be higher compared to bank backed AMCs. The incentive bias of the distributor reflected in its gain of market share in equity from 25.6% in Q4 FY17 to 40.9% in Q4 FY22 -

Increase revenue share from B-30 market even though it is less profitable in the short term

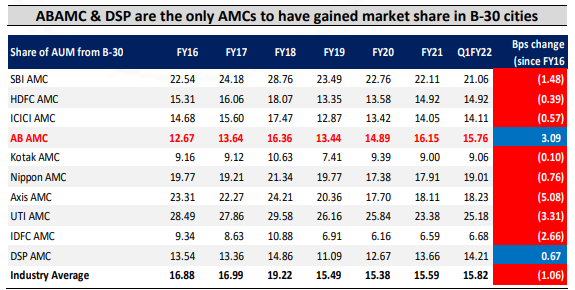

Based on my scuttlebutt, UTI and ABSL are having good distributor presence in B-30. T-30 is 75% penetrated and there is more ground for penetration in B-30. There is also a support from policy front to charge extra expense ratio in B-30 compared to T-30 to encourage more penetration. For Q4 FY22, B-30 share is 15.9%. 75% of AUM in B-30 is from Equity side which translates to more sales revenue.

Source - Ventura IPO Note

- increase SIP AUM which is sticky and good for long-term sustainable AUM

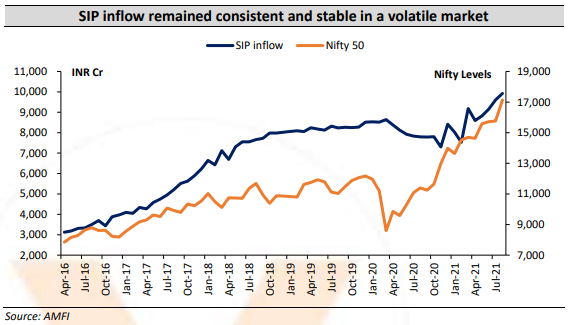

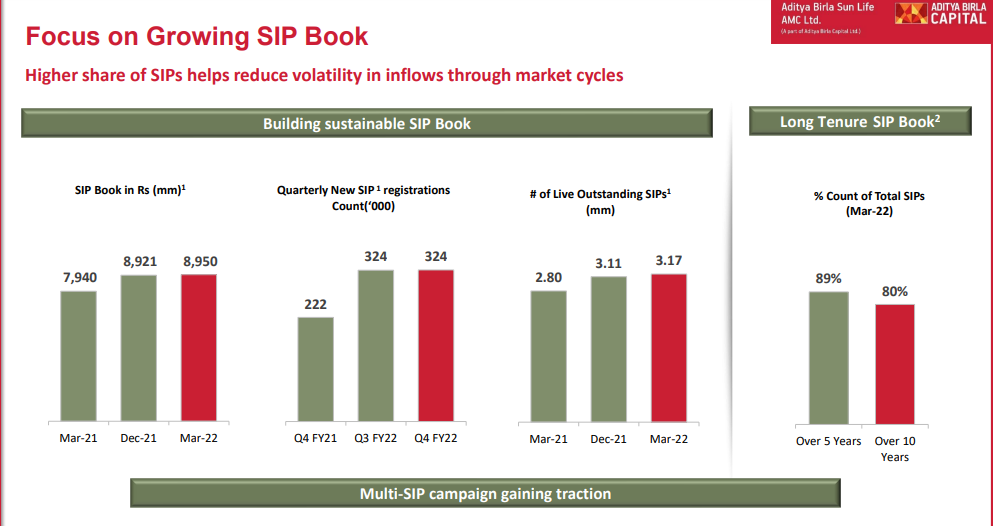

B-30 comes with low ticket inflows however, there will be more stability of inflows. The aspiration is to make 1000 Cr monthly SIP runrate. For Q4 FY22, it is at 895 Cr and with recent bull run, the SIPs will continue as shown in below screen-shot. The long-tenure SIP book is more consistent than HDFC AMC long-tenure SIP book

- Tap the NRI investments & Ramp up AIF/PMS

ABSL is the front runner in opening AIF fund in GIFT City among MF houses and they also have subsidiaries in offshore centers like Singapore, Dubai, Mauritius etc to attract NRI money. In Q4 FY22 concall, they mentioned about new international CIO who is ex-ASK PMS portfolio manager. Ideally, PMS is B2B and so may not be much profitable compared to regular MF schemes but AIF is something which can result in more revenue. As there is a push to make GIFT City attractive(Under PM’s radar), there can be encouragement in the form of less tax which can result in good inflows from NRIs.

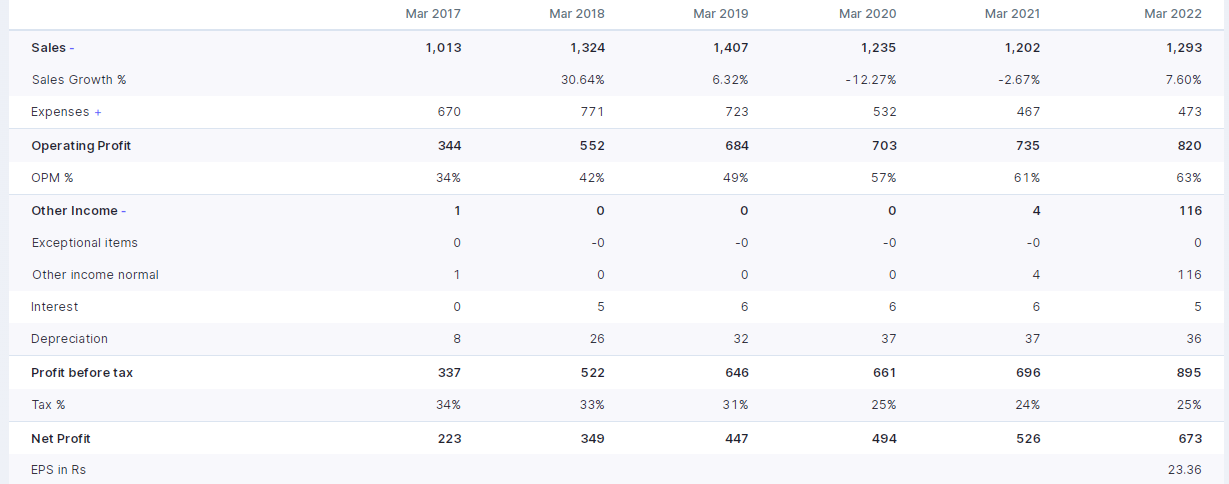

P&L Statement Analysis

-

Sales growth is not consistent

This is due to SEBI’s policy to move MF scheme specific expenses to scheme itself in 2018/19 and so, the sales revenue we see now are after scheme-specific expenses cut from respective MF schemes -

PAT increased YoY even though TER has been cut by SEBI

The primary reason is the reduction in tax rate from ~34% to ~25%. ABSL has effectively passed on the cut in the TER rate to distributors like other MF houses. There is a growth in equity segment in overall AUM from 25.9% to 40.9% in last 5 years.

Source - Ventura IPO Note

- Other Income of 116 Cr in FY22

ABSL AMC has investments worth 2121 Cr and my understanding is, the majority of this other income is from the returns generated out of the investments

- Reduction in expenses

The digital push due to Covid has helped in reduction of expenses. The management has also informed on their various tie-ups with fintechs to reduce the expenses further as can be seen in their digital onboarding

Valuation

Current Marketcap is ~12.2k Cr

Investments ~2.2k Cr

Total Outstanding Shares 28.8 Cr

Overall AUM ~3,00,000 Cr

Yield 0.41% of AUM ~1230 Cr per year

TTM PAT 673 Cr

TTM EPS 23.4 Rs

CMP 425 Rs

Removing the investment part(~73 per share) from CMP gives 352 Rs per share

P/E = 352/23.4 = ~15

At current CMP and 50% dividend payout, the dividend yield comes to 3%

I agree we are in peak earnings due to bull run but the underlying SIP business model ensures that AUM will keep on increasing. The recent bull run just gave more reasoning for distributors/retail to invest in stock market. Even as the expense ratio comes down, AMCs come up with new products/schemes like smart beta ETFs etc to increase yields compared to regular ETFs and it is a given that industry AUM will increase multi-fold in India going forward.

Conclusion

ABSL AMC survived multiple cycles without any backing of bank. They have more presence in B-30 market other than SBI which needs more hand holding. Like HDFC AMC, the funds of ABSL AMC are also not great with returns but then, the strength of a resilient business lies in its handling of operations during their downturn. The insider buying from market purchase also is a positive sign which I don’t see in other listed AMCs like HDFC, UTI or Nippon. This is a high quality business with almost no need of capital infusion and free cashflow generating. In the Q4 FY22 HDFC AMC concall, Navneet Munot mentioned that by 1970’s MF industry in US is already 5 decade old but the AUM has moved by 1000 times from then. The growth in MF AUM will be huge and there will be multiple winners in this industry. Like Ramdev Agarwal says, it is not just about the earnings but also the quality of earnings that matter. I believe the quality of earnings in AMCs are top notch compared to other cyclical industries.

Discl - Invested 4% of PF at 413