Theme:

Financialisation of Savings in India

Introduction and History:

Aditya Birla Sun Life (ABSL) AMC, a JV between Aditya Birla Capital Ltd and Sun Life AMC, is the 4th largest AMC on the basis of Quarterly Average AUM (QAAUM) as of 30th June 2021. It was formed in 1994 and is one of the oldest players in the Mutual Funds (MF) Industry.

One point that I would like everyone to note here is that though it is the 4th largest player, it is the largest non-bank player, and they even surpass the MF players which are backed by large banks such as Kotak and Axis Bank. This truly speaks volumes about their execution as banks have an inherent advantage when it comes to the distribution of MF products.

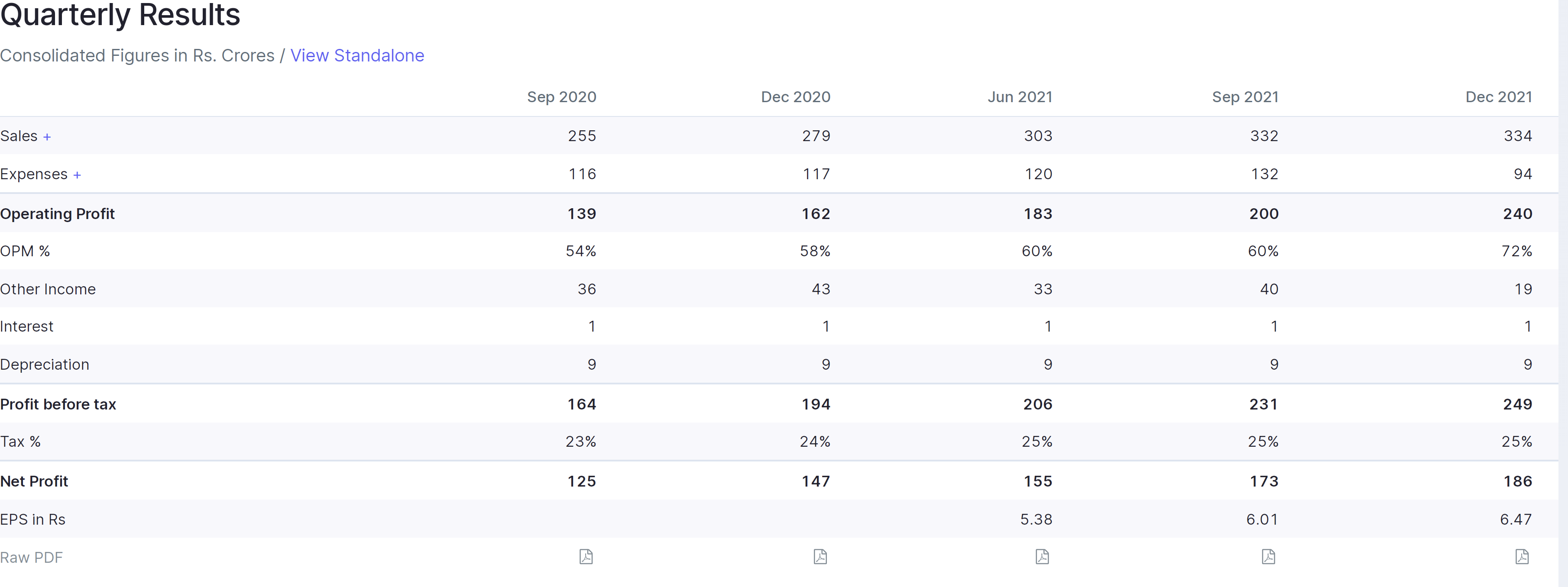

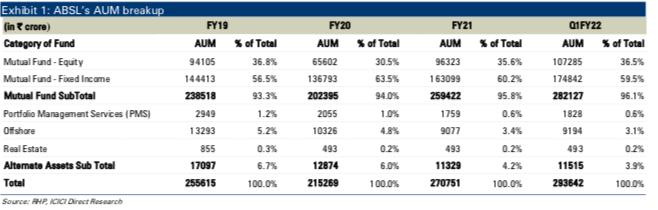

In terms of mutual fund business, ABSL manages 118 schemes with QAAUM of ~| 2.7 lakh crore as of June 2021. Apart from mutual fund business, ABSL also offers PMS, offshore, and real estate offerings which comprise AUM- 11515 crores. In FY21, revenue stood at | 1191 crore, i.e ~39 bps of AAUM. PAT came at 526 crores (~19 bps of AAUM), with RoE at 33.7%.

Branches and Distributors:

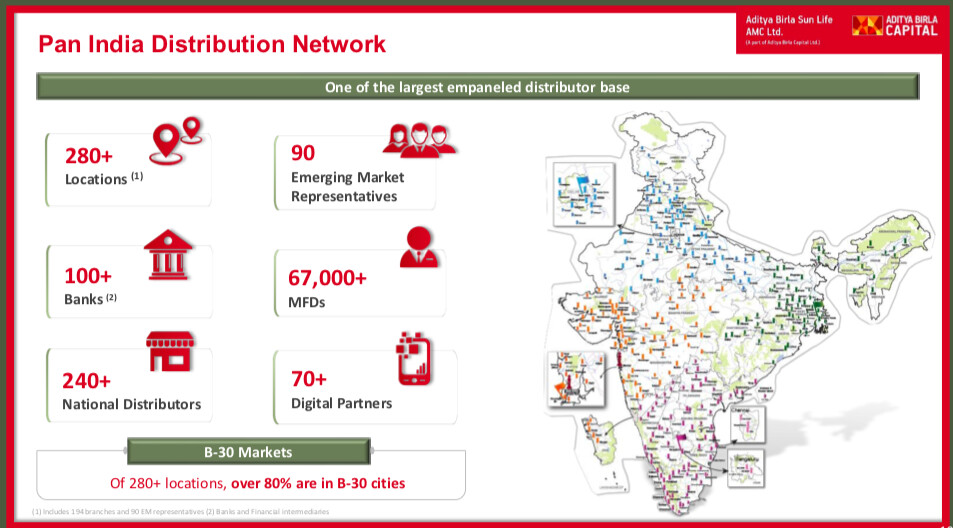

It has established a strong geographical presence comprising 194 branches (covering 284 locations) spread over 27 states and 6 union territories. ABSL has an extensive & multi-channel distribution network with over 66000 mutual fund distributors, over 240 national distributors, and over 100 banks/financial intermediaries.

In my opinion, one very important point to note here is to find out the number of branches that its parent- AB Capital has. It has a number of other businesses like life and general insurance, Brokerage, and financing, which also requires the setting up of branches. The management of AB Capital in various interviews has said that they have become very aggressive in cross-selling each of the financial services to its customers. So, if any of the parents’ businesses set up a branch, this increases the distribution and marketing/brand reach of ABSL AMC. Thus, they could compete with the distribution reach of even larger bank-backed MFs.

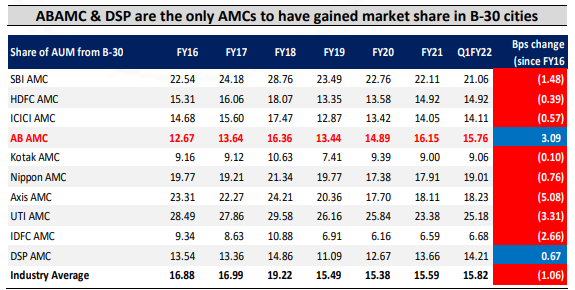

Focus on B-30 Cities:

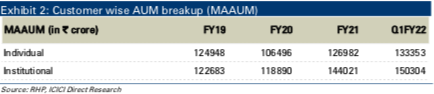

ABSL is focused on expansion in B-30 cities which has helped to grow retail customer acquisition and retention rates. As of June 30, 2021, MAAUM from B-30 cities was 44701 crore; the market share of individual MAAUM from B-30 cities at 7.8%. A large part of industry growth is expected to come from B- 30 cities, and ABSL with an existing large presence & distribution capabilities in B-30 cities, remains well placed to attract customers.

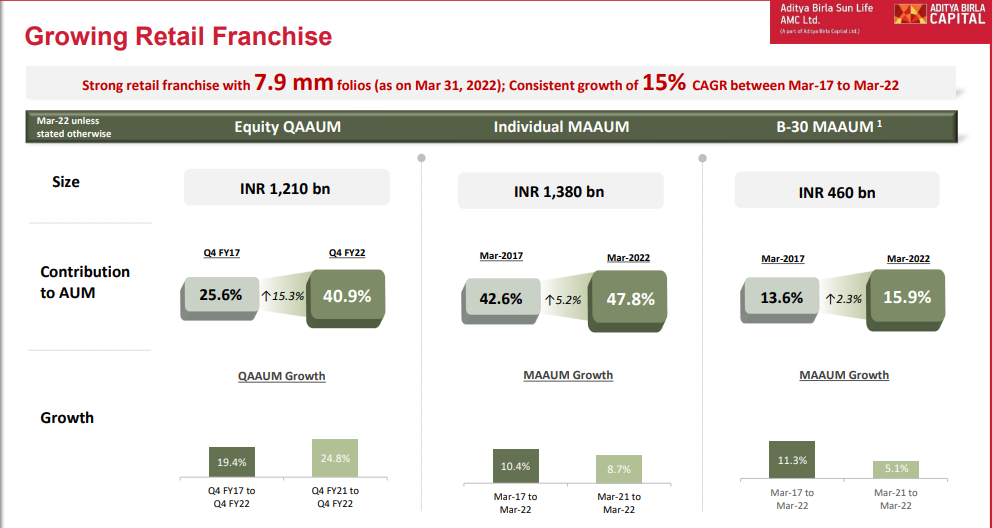

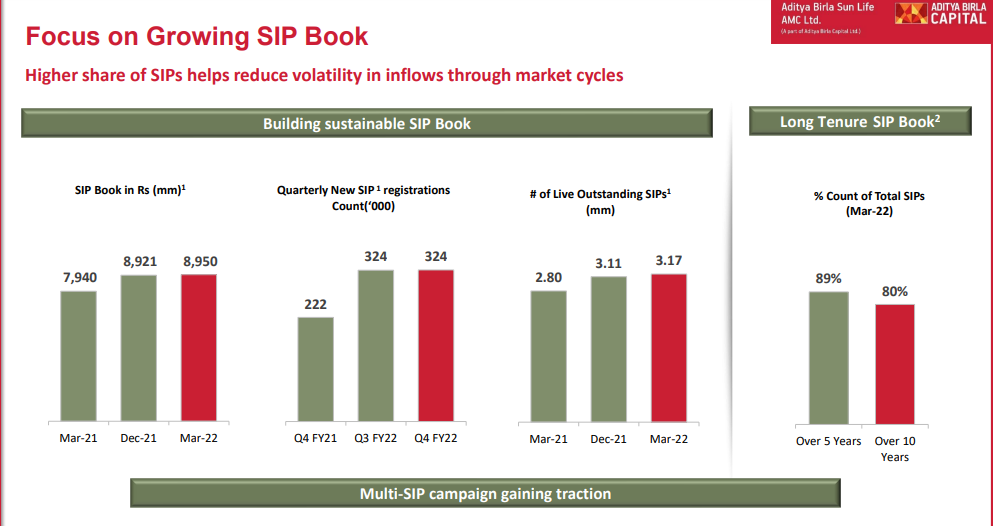

Now, I am sure most of us have heard interviews of many AMCs saying that they are focusing on B-30 cities, but I have come across a few of the AMCs who are not really walking the talk. So, to verify this I will add a slide from the latest quarterly earnings presentation of the AMC.

As you can see in the image, more than 80% of their branch locations are in B-30 cities, even though not even 20% of their AUM comes from them. I also did a bit of scuttlebutt to verify this with a few local MF distributors in my town. They told me that one of the most aggressive AMCs is ABSL.

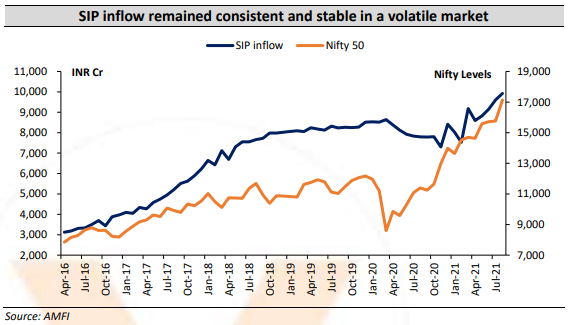

SIP Growth:

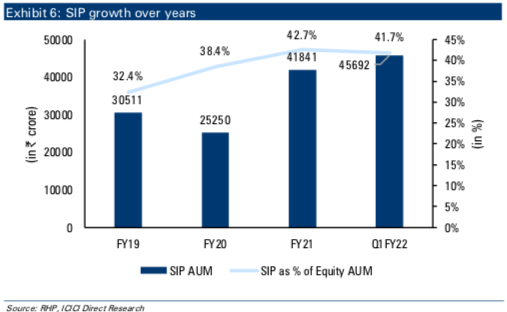

SIP growth maintains consistency of AUM and thus earnings. Hence it is important to know this about every AMC. ABSL’s individual investor MAAUM has seen growth at a CAGR of 18.38% in FY16-21. The company offers a range of systematic transaction options and add-on features including SIPs, STPs, and SWPs. As of June 30, 2021, SIPs have become a material portion of AUM accounting for ~41.7% of total equity-oriented mutual fund AUM and ~34% of total individual investor mutual fund AUM.

As you can see in the above image their SIP as a % of their AUM has been continuously growing.

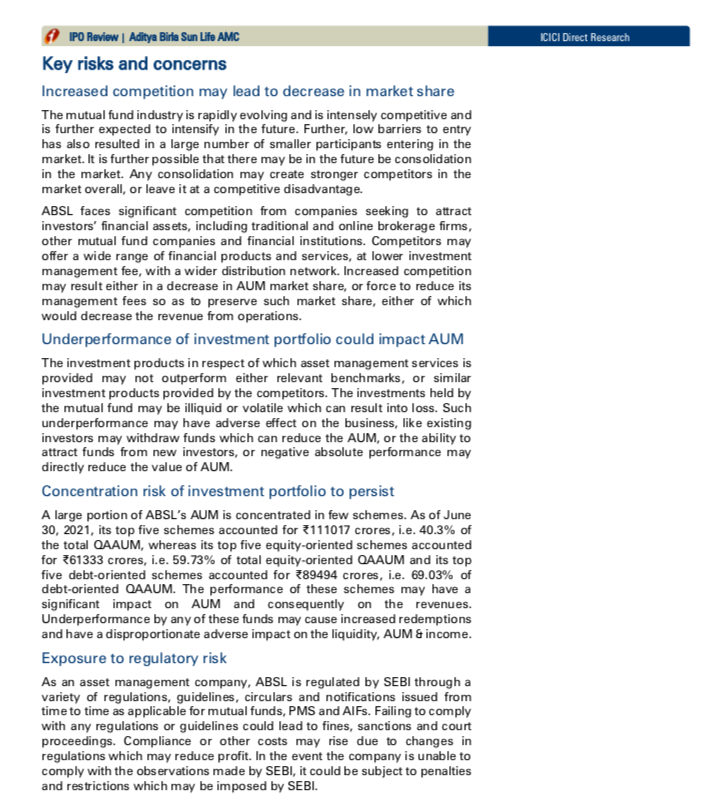

Anti-Thesis:

I have added a slide from the ICICI Direct IPO note for this purpose, as the concerns of nearly all AMCs are quite similar.

Valuations:

On an FY21 Earnings basis, the stock is currently trading at a PE of 31 and on the basis of H1FY22 annualized earnings, it is trading at 26 PE.

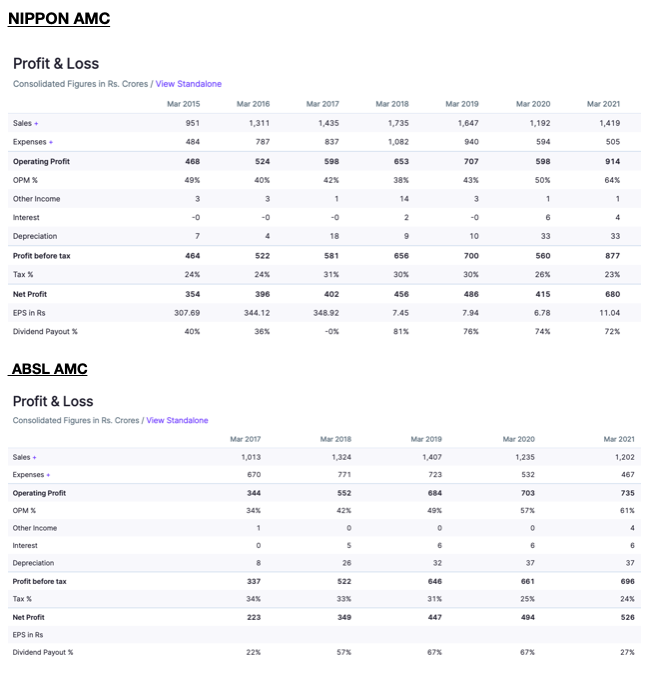

Now, I would just like to compare this company with its larger non-bank peer- Nippon AMC. I am not Comparing it with HDFC AMC as it is a bank-backed player and thus deserves better valuations.

Now, ABSL AMC is trading at FY21 PE of 31 with a market can of around 16,700 crores and Nippon AMC at an FY21 PE of 29 and a market cap of 22,400 crores.

Now, I believe that ABSL AMC should at least be trading at a market cap higher than Nippo. And I will tell you why:

-

If you look at the earnings comparison between the two, you will see that on a 3-year basis, the PAT of ABSL has grown at a 15% CAGR while NIppon’s has grown at 11% CAGR.

-

It is very important to note the period of earnings between 2018 and 2020 when the stock market was going through a severe downturn, especially in the mid and small caps. Here, you will see that Nippon’s PAT fell drastically over the 2 years. On the other hand, ABSL’s PAT grew as consistently as it did. In fact, in FY20 ABSL’s PAT, was far higher than that of Nippon’s. The reason for this is that Nippon has Equity heavy AUM whereas ABSL has about 60% Fixed Income AUM. Fixed income is far more consistent and thus the book of ABSL is far more stable. And stability deserves a premium. Nippon will possibly go through similar situations when the stock market decelerates.

-

Lastly, I am not sure whether this is only true for the region that I live in, but Aditya Birla has a much better and recognizable brand name than Nippon. Especially, after Reliance’s brand was removed from it. To the ordinary citizen, the brand is very important when it comes to their savings. That is why people have FDs in SBI and HDFC rather than Equitas and RBL, even though the latter gives much better returns.

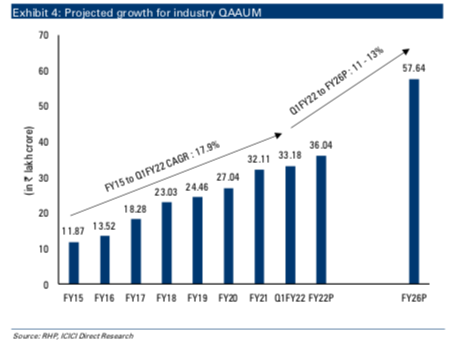

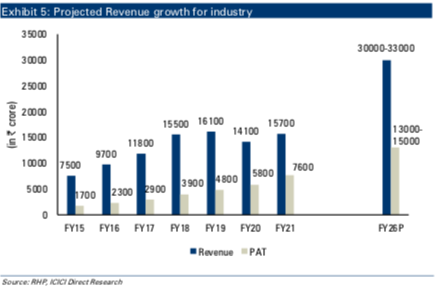

Future of Industry:

Financials and other important information:

Disclosure: I am a relatively new investor and thus please do your own research when it comes to my opinions on some of the information in regard to the company. I have a 4% allocation to it in my portfolio and thus my views may be biased.