Any view on latest results. The profit has dropped 31% YoY and management also announced their exit from Myanmar port project due to the pressure from US sanctions…

When comparing with other Adani group stocks, APSEZ is trading very cheap. Considering its cash flow and nature of business it should be valued more than other business. Any specific reason APSEZ is trading low among the packs…

Is there anything I am missing out here… ?

Adani had 2 international deal in ports business. One is in Israel - Haifa port, another in Africa (Tanzania)…

Adani now going globally and trying to become like DP port of Saudi Arabia…

Investigative Report:

I am an investor in Adani Port fot a Year now.

So just putting down my thoughts on the same.

My investing approach is to invest in monopoly, duoploy business . Valuations are generally not my cup of tea so i let them run ahead / behind the fair value and keep pyramiding up when stock moves 30-50% from my average price. Page, IEX, CDSL, Adani Port are part of the same theme and stocks may be right, prices in short term may not but in long term i believe earning growth = stock price growth.

If India to grow at 7-8%, inflation at 4-6%, Adani port has to grow at 15-18% . My hope is more of 18% over next 10+ years, hence invested.

In 10 years all major Indian ports on east and west coast will be bought/ developed by Adani. So any and every import , export , china+1, PIL, manufacturing boom will help Adani.

I would stick my head out and say that they have got world class ports.They have acquired ports in both east and west coast and maybe in a few years it would be a monopoly kind of business. With the port trusts undergoing decline , this can be a good bet, once the debts are retired. This is a good cash flow business with good margins. If the new port at Vizhinjam comes up and transforms itself into a major transhipment port replacing Colombo it could be a bonus.This is one Adani business with solid assets and this is a sector i work in.Iam investing in the present downfall in stock price.

What is the appropriate multiple for a ports business? Has anyone studied international companies to figure out where Adani ports stands.

Also, what is the most appropriate multiple or metric to use in this sector?

I don’t really think the stock trades on fundamentals anymore.

As I see it, for a while, stock performance will be driven by the actions of the Adanis and news flow.

Is there an argument for the stock to perpetually trade at a discount? Probably.

I didn’t think it was expensive even at 800-900.

For what’s a collection of ports in the fastest growing economy that’s increasingly becoming outward facing with an aggressive promotor engaging in a lot of smart M&A and adding adjacencies (logistics/warehousing)

one can compare with DP world (dubai ports) and APM terminals( AP Moeller Maersk). What i can see is DP average price to earnings is mid teens, APM is hard to figure because there are multiple businesses in it.The newest acquisition for Adani ports is Haifa port, just have to keep a keen eye on debt and progress on new projects like Vizhinjam and the newly announced port in West Bengal. Some of the ports that they bought like Karaikal in the east coast or Dighi in the west coast could not be run profitably by previous owners(debt could not be serviced). will study more and compare with DP world on metrics.

One can compare with Gujarat Pipavav port, it has only one terminal in Pipavav, whose ultimate parent is ap moeller, a world class operator.It is like a steady state business where one can’t expect growth, The last 5 years median p/e is around 20,debt free and dividend yield of 4%, i would consider this expensive with no growth, Adani has two ports across the gulf of khmbat in Hazira/Dahej which can take away Pipavav business

Disclaimer: I have made a small investment in both Ambuja Cement and the Adani Port.

Unfortunately, the thread on the Ambuja Cement is closed.

Unfortunately, there is no post mentioning the business dynamics so would like to share my limited knowledge on APSEZ and ports business sector fundamentals. I have power/infrastructure project finance background and had done a feasibility study to set up a green field port project.

Adani Ports Business Summary:

It is the largest commercial port operator in India with 25% share of port cargo movement in India. The company has evolved from a single port dealing in a single commodity to an integrated logistics platform. The company has a pan-India presence in ten locations (nine are operational) with the flagship Mundra port, India’s largest commercial port, in the Gulf of Kutch. It has a large land bank of 8,481 hectares of contiguous land at Mundra.

- Total ~70% of APSEZ’s revenues is contributed by its port operations. Rest

is led by harbour (11%), logistics (7%) and others. - In FY22, container, bulk, liquid mix were at 36%, 55%, 9%, respectively

Further financial and operating parameters can be found at screener.in so not wasting time on that.

Port & ICDs sector:

Construction of ports is quite challenging as the new age large container ships require deep channel depth just adjacent to land plateau. There would be very few sites where this is naturally formed. Gautam Adani was able to identify this opportunity at Mundra where no one had an idea and he jumped into port business with no prior experience!

Building a port where such natural occurrences are not available can lead to huge capex depending on site conditions. So yes it’s not that ports can be constructed anywhere. Also in India constructing ports itself has other challenges like environment clearances, fishermen agitations, PILs, etc.

Also, just building the port is not enough. The heart of ports is its connectivity to hinterland, inland container depots (ICDs), warehousing, etc. It is of prime importance to shipping liners that there is quick turn around of movement of cargoes as they have many ports to call. They will pay a premium for such facilities. Many ports in India are govt operated and there may be inefficiencies in them, leading to better business opportunities for pvt players. Building roads, train tracks, etc. itself is a humongous task with getting related approvals, etc. with extra capex costs.

Adani has and in future may keep acquiring key ports at strategic locations. This can create a monopoly business with pricing power. There are many future key trigger points like DFC connectivity to Mundra, acquisition of Concor, etc. It will take too much time and effort to actually understand the growth factors with so many acquisitions and future growth triggers (make in india, pli, china +1, new logistics policy, etc.)

My current take on the business and situation:

APSEZ was in my watchlist since last 3-4 yrs but had anticipated that one day there would be sell off in group companies due to extremely high valuations and it would have a spill over effect on Ports as well. Now with all this imbroglio I think it was apt time to enter Adani Ports.

Being from project finance background, I am more comfortable with high debt levels than average investor but will not get into that. Port business probably the best cash cow for Adani group but never understood the market irony of giving it less valuation than other businesses.

Even with this downturn in group companies, APSEZ has corrected less than others and as per recent news mutual funds are accumulating in last couple of days. Even Moody’s and others have maintained their grades while downgrading other group cos.

Disc: Not a registered analyst. Information for education and not recommendation. Invested and biased.

Adani ports Q3 -

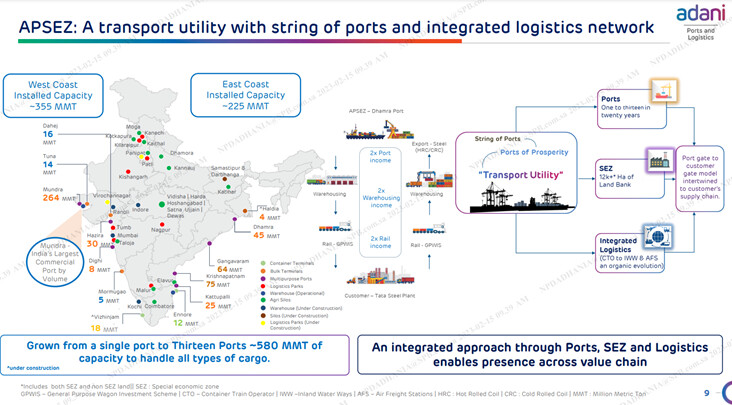

Network of 13 Ports across India’s coastline. No concentration risk

India’s largest player. Rail,warehouses connecting ports to consumer gates

Huge land banks which can be developed into SEZs

Covers entire gamut - dredging to evacuation, 70 pc port margins

Has diversified from bulk and liquid cargo into LNG

Acquisitive and turnaround strategy has ensured quick upscaling of new ports to company level EBITDAs

Net Debt/EBITDA at 3.2 - manageable

Aim to be carbon neutral by 2025

Port capacities including warehouses & Agri Silos -

( grown from 01 to 13 ports in 20 Yrs )

West Coast -

Mundra - 264 MMT ( India’s largest )

Dahej - 16 MMT

Tuna - 14 MMT

Hazaria - 30 MMT

Dighi - 8 MMT

Mormugao - 5 MMT

Vizhinjam - 18 MMT

East Coast -

Haldia - 4 MMT

Dhamra - 45 MMT

Gangavaram - 64 MMT

Krishnapatnam - 75 MMT

Kattupalli - 25 MMT

Encore - 12 MMT

Inland logistics parks -

01 at Nagpur

02 in Punjab

01 in Haryana

01 in Karnataka

01 in Rajasthan

02 in Maharashtra

Logistics infra - 87 trains ( to take it to 200 trains by 2026 )

Currently owned railway track at 620 Km ( to take it to 2000 km by FY 26 to become the largest track owner )

Last 9 months acquisitions - Hafia port in Israel ( largest port there )

Indian Oil Tanking Ltd ( largest operator of liquid storage facilities in India )

Gangavaram Port ( India’s third largest private sector Port )

Ocean Sparkle (India’s leading third party marine service provider)

Additionally-Adani Ports is the highest bidder for Karaikal port

Adani Agri Logistics - won contracts in 8 states for Grain storage silos ( at 70 locations ). Will take their Silos capacity from 2.8 MMT to 4 MMT

Cargo handling breakdown -

Containers -37 pc

Coal -38 pc

Dry cargo (non coal) -15 pc

Crude -6 pc

Other liquids -3 pc

Gas -1 pc

Financials (Consol)-

Sales -5334 vs 4576 cr

EBITDA -3328 vs 2889 cr

PAT -1426 vs 1658 cr(Q3 FY 23 PAT includes 320 cr forex hit)

Revenue contribution, standalone-

Ports -3936 vs 3431 cr @ 70 pc EBITDA

Logistics -490 vs 300 cr @ 29 pc EBITDA

SEZ -169 vs 124 cr @ 64 pc EBITDA

Gross Debt at aprox 45500 cr Net Debt at aprox 39300 cr

Net Debt/EBITDA at 3.2

Strong internal accruals supporting organic and inorganic growth

Avg Debt maturity profile at 6 yrs Aprox 75 pc debt is foreign currency denominated ( mostly USD )

Disc: holding, biased

Some of Key insights of Q2 FY24

- Nikhil: Understood. Got it. And the second question I had was then on the Vizhinjam port. Good to see progress on the port, but it would be helpful if we could get clarity on when does scalable commercial operations start at that port?

Karan Adani: So we expect all the equipments to be at port by March of 2024. As you know, it’s a semi automated terminal. It will take us 3 to 4 months to get all the cranes and equipment commissioned. So we would look at basically second half of FY '25 to commission – to start full-fledged operation.

How Adani’s Genius strategy of Transhipment Port is making India powerful? : Business Case Study - YouTube](https://www.youtube.com/watch?v=_2-JIfqStOc&t=4s)

-

Terminal Investment Ltd (TiL), an associate of MSC Mediterranean Shipping Company (MSC), the world’s largest container shipping line, acquires 49% stake in Adani Ennore Container Terminal Pvt Ltd (AECTPL) for an equity consideration of Rs 247 crore.

Microsoft Word - Letter11 (bseindia.com) -

Issuance of Debentures up to Rs 5000 Cr

and NCPRS of ~Rs 250 Cr

Microsoft Word - Letter11 (bseindia.com)

Basis of two annonument , they are now creating short term and long-term fund arrangement for business. The company also in advance stage of Gopalpra , Orissa project with SP Group.

Is there a reason why it fell 5% today? Is it because of its high valuation. is the results on Feb 1st ??

When it went up at 2:30pm on Saturday for absolutely no reason you didn’t ask this question. But now when the stock came back to the same level the next day you are looking for a fundamental reason for which it fell. Pre-Budget usually there is a lot of volatility and some selling pressure given the risk of government policy change.

As far as the results are concerned, the company gives monthly data on the volumes, and the results are rarely surprising.