CMP - 267

Review of Sep’16 Results - Adani Ports cargo volumes continued to surge in a weak trade scenario on account of expanding market share as its smaller ports clocked robust spurt—YoY growth of 56% handling 14.7MT while consolidated volume at 43MT was up 17% (container volumes jumped 30%).

Volume growth momentum is expected to sustain as Kattupali scales up, CT-4 is commissioned at Mundra and new service liners commence operations. As cargo mix has shifted in favour of containers and other high-value cargo, average realizations have also increased. This, coupled with INR650mn incentive income and INR1.9bn service income for development of CT-4, led to a strong EBITDA margin beat—66% versus 63% estimated. Reduction in interest cost by INR400mn and healthy treasury income resulted in PAT at INR10.9bn surging 60% YoY.

Net debt down by INR13bn on reduction in working capital

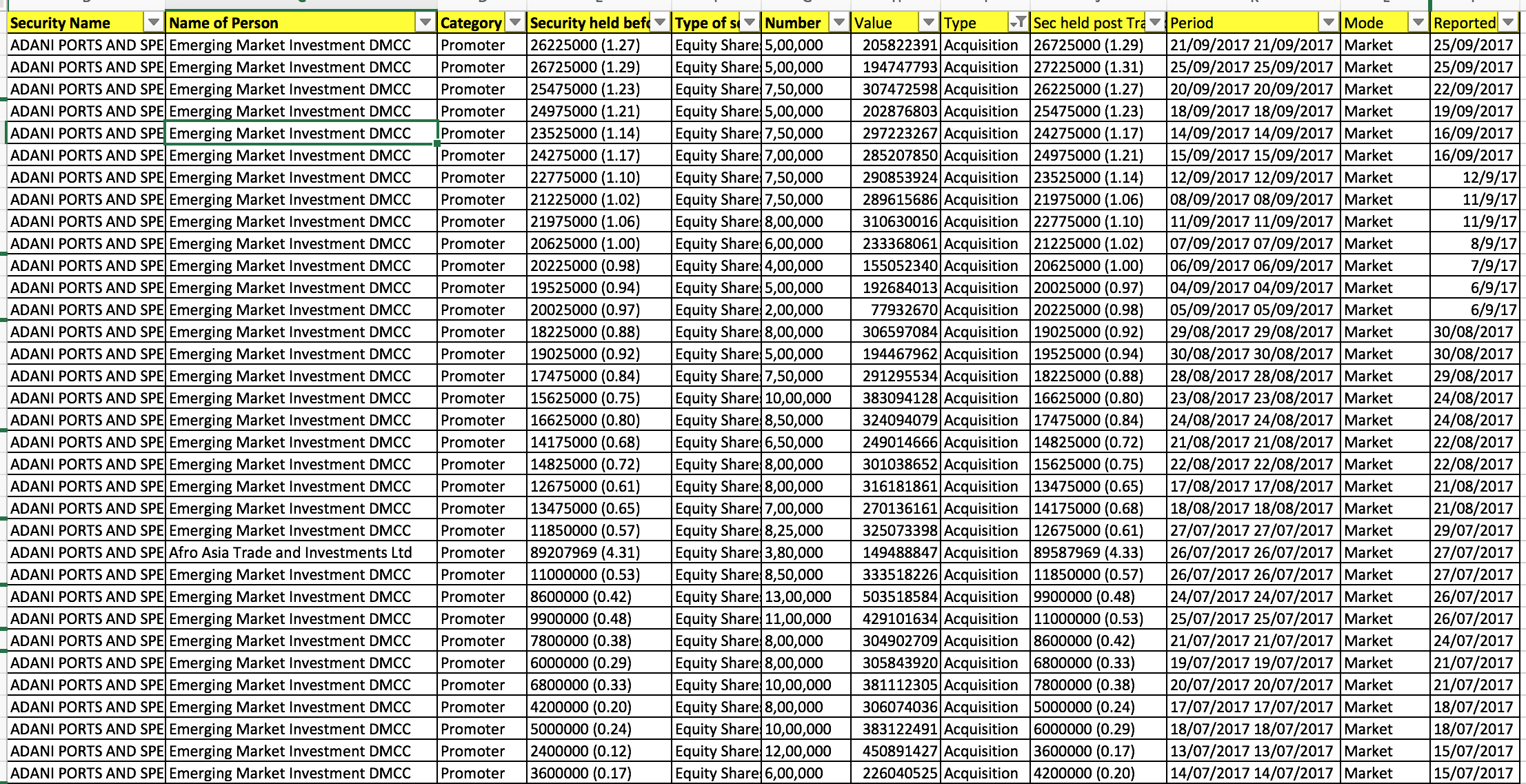

In line with management’s earlier guidance of pruning loans and advances to related parties, APSEZ has cut the exposure by INR10bn. This helped prune net working capital and reduce net debt by INR13bn in H1FY17 and targets to eliminate them completely by FY17 end.

Few highlights of conference calls

-

Demerger process of Kattupali on track and should get completed by year end.

-

The company is targeting 4MT of coastal cargo and is on track to achieve the same. Margin profile for coastal movements is similar to EXIM cargo.

-

Hazira port is averaging 30-40k TEUs and the company expects an increase in these

volumes.

-

Agri, iron & steel and minerals registered double digit growth.

-

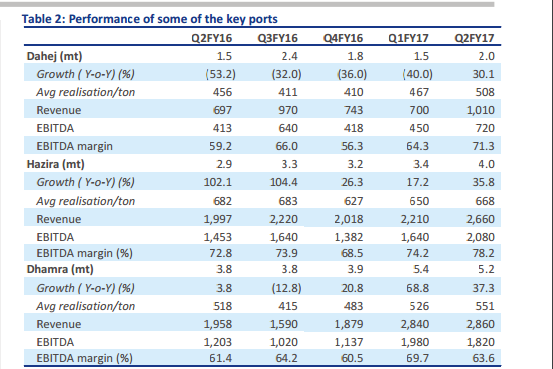

Kattupali, Dhamra and Hazira are the fastest growing ports. Dahej and Dhamra expected to handle fertiliser cargo from Q3FY17.

-

On the bid for green field port in Dhamnapadu in Andhra Pradesh, the company is still awaiting outcome.

-

It operationalised berth 3 at Dhamra port and 3 new services started at Mundra port. At Hazira, the company added Far East to Mediterranean lines.

-

Maersk has shifted from Chennai to Katupalli. Management stated that Katupalli can be hub for auto.

-

Ennore ports likely to be operationalised in Q4FY17 and containers at Dhamra likely to start from Q4FY17.

-

Adani Logistics is the largest private rail operator in India and the company has

expanded to warehousing and providing end-to-end solutions to various costumers like

Maruti, Wilmar, Hero, Aditya Birla etc. The company perceives robust volumes in

logistics business.

-

Terminal volumes jumped 21% YoY.

-

Capex is being done at Hazira and partly at Mundra. Management stands by its capex

guidance of INR30bn. Net finance cost for the company reduced by INR3.43bn since March 2016.

-

On the group leverage, management stated that long-term debt at the group level is at

INR 760bn, EBITDA at INR240bn and therefore debt to EBITDA at 3.15 is comfortable

considering the nature of business.

-

Strategy for the next 2-3 years will be focus on coal, container and crude, coking coal

and coastal traffic.

Strong pipeline of projects; expansion on the radar

The company has a strong portfolio of projects on the Indian west coast other than the flagship Mundra port. The projects are a mix of brown-field port development i.e. currently at Dahej & Hazira and as terminal operator at the major ports i.e. coal terminal under development at the Murmagao port. Such projects would help the company gain a pan India presence. While the company is looking at setting up a large port on the east cost of India, it has also been scouting for opportunities to go global and has recently evinced interest in port development projects in Australia and Indonesia, in line with its long-term strategy.

Potential Risks

Uncertainty in traffic at ports: Since cargo at ports is contingent on international trade, any

slowdown in it could affect Mundra Port as well.

Regulatory changes regarding SEZs: The existing SEZ policies and benefits outlined by the

government to promote exports are relatively new and are being continuously reviewed.

Any changes in the form of reversal of current tax benefits to units under the SEZ umbrella

will significantly undermine incentives for industries to setup units in the SEZ, hampering

current plans of land sale. Land parcel sale at the SEZ is yet to pick up.

Huge debt can work against the company if growth in economy doesnt take off.

Disclosure - Constitutes only 0.25% of my portfolio. Will look to increase weightage to 1% if the stock becomes available at 220-180.